http://democracynow.org – Extended web-only interview with Raymond

Offenheiser, president of Oxfam America. The group just issued the

report, “An Economy …

We have previously shown just how bad the situation in the US heavy

trucking space - trucks with a gross weight over 33K pounds - was most

recently in "US Trucking Has Not Been This Bad Since The Financial Crisis"

in which we looked at November data and found, that "Class 8 truck net

orders at 16,475, were 59% below a year ago and the lowest level since

September 2012. This was the weakest November order activity

since 2009 and was a major disappointment, coming in significantly below

expectations. All of the OEMs, except one, experienced unusually low orders for the month."

For those who missed the proverbial wheels falling of the heavy trucks, so to speak, the charts below do the situation justice:

So with 2015 in the history books, and as we start 2016 where the

base effect was supposed to make the annual comps far more palatable, we

just got the latest, January data. In short: the drop continues to be

one of Great Recession proportions, manifesting in yet another massive

48% collapse in truck orders in the first month of the year as demand

appears to have gone in a state of deep hibernation. From Reuters:

U.S. January Class 8 truck orders fell 48 percent on the year,

preliminary data from freight transportation forecaster FTR showed,

indicating that 2016 could be another weak year for truck makers.

FTR estimated that orders for the heavy trucks that move

goods around America's highways totaled 18,062 units in January. This

follows on from a full-year decline in 2015 of nearly 25 percent to

284,000 units from 276,000. "It is not looking to be a strong year," for the market, FTR chief operating officer Jonathan Starks said in a statement.

Amid uncertainty over U.S. economic growth and a lackluster performance for retailers in the fourth quarter, trucking companies have been holding back on buying new models

As a reminder, unlike trains, which one can say are used to transport

oil and coal, Class 8 trucks make up the backbone of U.S. trade

infrastructure and logistics: what they represent is both domestic and

global trade. Or in this the devastating collapse thereof.

Should one be concerned by this precipitous drop? Absolutely not: as

the Federal Reserve would certainly say "it's probably nothing" and

blame it on the weather.

Some brushed it off, saying one

should never look at gross derivative exposure but merely net, to which

we had one simple response: net immediately becomes gross when just one

counterparty in the collateral chains fails – case in point, the Lehman

and AIG failures and the resulting scramble to bailout the entire world

which cost trillions in taxpayer funds.

With European banks sitting at multiyear lows, one widely followed

market watcher said some of the biggest ones could go bankrupt.

Former hedge fund manager and Goldman Sachs alumnus Raoul Pal said

his scenario is one most investors aren’t looking at right now.

Pal said the banking issues have the potential to overtake risks associated with China’s growth slowdown and cheap oil.

“So many of these [bank stocks] are falling so sharply. I think

people haven’t even caught up with what is going on, and that really

concerns me,” the founder of Global Macro Investor told CNBC’s “Fast Money”

on Tuesday. “I look at the big long-term share charts of them, and I

think this looks very terrifying indeed. I have not seen anything like

this for a long time.”

For Pal, negative interest rates are the chief reason why the bank

stocks are in trouble. He said European banks have a tougher time coping

in the environment than U.S. banks. http://www.cnbc.com/2016/02/03/european-banks-near-terrifying-crisis-raoul-pal.html

Kyle Bass – China banks months away from ‘danger territory’ China’s banking system has grown to $34.5 trillion, more

than three times the country’s GDP. The country is due for a loss cycle

as cracks begin to show in its economy. http://www.cnbc.com/2016/02/03/kyle-bass-china-banks-months-away-from-danger-territory.html UBS Bank Shares Plunge As Rich Investors Withdraw Money

Swiss bank UBS saw its shares slide on Tuesday on news that investors

had pulled billions out of its division serving wealthy clients http://hosted.ap.org/dynamic/stories/E/EU_SWITZERLAND_EARNS_UBS?SITE=AP&SECTION=HOME%26TEMPLATE=DEFAULT%26CTIME=2016-02-02-06-56-54

Some brushed it off, saying one should never look at gross derivative

exposure but merely net, to which we had one simple response: net

immediately becomes gross when just one counter party in the collateral

chains fails – case in point, the Lehman and AIG failures and the

resulting scramble to bailout the entire world which cost trillions in

taxpayer funds.

We then followed it up one year later with “The Elephant In The Room:

Deutsche Bank’s $75 Trillion In Derivatives Is 20 Times Greater Than

German GDP.” http://www.zerohedge.com/news/2014-04-28/elephant-room-deutsche-banks-75-trillion-derivatives-20-times-greater-german-gdp

Then, just last June, we asked the most pointed question yet: “Is

Deutsche Bank The Next Lehman?” only this time it wasn’t just the bank’s

gargantuan balance sheet risk shown below…

And let us not forget our domino friend :)

ISSUES:

•In order to have standing, must a party seeking to foreclose have an

interest in both the mortgage and the promissory note, or just an

interest in either the note or the mortgage?

•When a promissory note is discharged in bankruptcy, does a party

seeking to foreclose only need to show it has an interest in the

mortgage to have standing, or must it have both an interest in the note

and mortgage?

Oh look! Another ($3.1 billion) lawsuit against Deutsche Bank:

From Reuters at 4:33 EST today: http://www.reuters.com/article/us-deutsche-bank-lawsuit-idUSKCN0VC2NY

Per Saumya Vaishampayan at the WSJ blog today at 3:30 EST: “Puts protecting against a 33% fall in U.S.-listed Deutsche Bank

shares by April were particularly popular Wednesday. Analysts at

Susquehanna Financial Group characterized the trading in Deutsche Bank

options as “crash put buying.”

Look out below. The banks are the Elephants in the Room

They got the exposures. The Primary Exposures. Then the derivatives.

Then the derivatives on the derivatives. And the counter-party risk on

counter-party risks and NO NOTHING OFFSETS/NETS because each contract is

a one off. (Well, for all intents and purposes)

There are the beys. The best on the bets. The leveraged bets on the

bets. The leveraged leveraged bets on the bets that are leveraged with

all sorts of untold counter-party risks inside each of the bets.

Good Luck and Good Night

BTW. A bud of mine. Semi-retired senior guy at a major WS firm.

He’s exposed. Big time. To the firm and his own portfolio. He’s

scared to death and perhaps near paralysis. And this is a guy who knows

what the fucks going on. Greed, hubris, denial and so on. The bad

stuff happens slowly at first, nobody believes it. It accelerates… it’s

transitory. Pretty soon, serious damage is done. Then it appears too

late accompanied by hope… empty hope …. And after a while nights become

sleepless. People become irritable and irrational.

Get safe The best portfolio is the safest portfolio. The safest

portfolio is a boring portfolio. Take the day off. Go golfing or see a

movie. Watch the world closely. Walk through a mall… look at how the

traffic is and how many are carrying packages. Breathe in the air.

Meditate. Let it go. You’re safe and will be whole. You’re being

taken care of.

(Examiner) – Last Friday, Japan was the first major economy to cross

the ‘Rubicon’ by implementing negative interest rates (NIRP) in an

attempt to force their people to spend, and slow deflation as the 3rd

largest economy moves into recession. However, in this Japan is not an

island, with several other nations already preparing to do the same to

protect their diminishing economies.And in all of this there is one

surprising country that appears to also be preparing for NIRP as on Feb.

3, coalition group of German legislators introduced a bill to limit the

use of cash, and to ban the use of the 500 Euro bill in personal and

non-bank transactions.

The significance of this is that when a central bank implements

policies that make holding your money in a bank a liability, then the

natural recourse is for depositors and account holders to simply take it

out and move their wealth into assets that are either outside their

nation’s currency, or into commodities such as gold and silver which

provide no benefit to an economy that desperately needs its people to

spend and create inflation and growth.

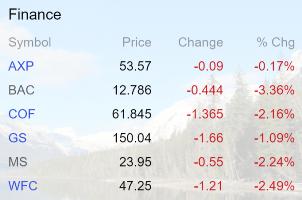

Not surprisingly, US bank stocks are getting whacked. As of 9am on Wednesday Feb 3:

Bank of America (BAC) stands out as especially cringe-worthy, having

fallen from north of $18 per share to below $13 in just a few weeks:

What does all this mean? The broad-strokes answer is that these huge,

nearly-omnipotent entities that have dominated and defined the world’s

economic and political landscape may finally be receding towards a more

reasonable level of power. One way to gauge this is by the rhetoric

coming out of the current presidential candidates, all of whom have

decided that it’s not just safe, but profitable to bash Wall Street.

Dimon, Blankfein, et al are clearly not the bullies they once were.

More immediately it means there’s a new black swan in the sky. As a

group the world’s biggest banks are leveraged to an extent that probably

has the authors of the Glass-Steagall Act

spinning in their graves. The notional value of their over-the-counter

derivatives books dwarfs the global economy, while their exposure to

now-moribund sections of the oil and gas industry guarantees massive

write-offs in the year ahead. The question isn’t whether the big banks

will report huge losses, but whether one of them will be destroyed in

the process, giving us another Lehman Moment.

So, sure, they’re still looking

pretty good when compared to the oil and gas industry, which is in a

depression, laying off well-paid people, from director-level engineers

to roughnecks. Contractors are out of work. Revenues are plunging.

Losses are piling up. Cash is running out. Bankruptcies and debt

restructurings are now a common occurrence. The junk-bond bubble that

funded the US drilling boom is imploding. Banks are starting to

recognize losses on their loans. But the sector has been through this

before. It’s temporary. When the price of oil rises again, the survivors

and new players will thrive, hire, and expand.

That’s not the case with brick-and-mortar retailers.

But it’s a slow process. Some bigger operations have already gone

bankrupt recently or have defaulted on their debts. Junk bonds that fund

much of the industry are swooning. Liquidity is drying up. And many

private equity firms that bought these retailers during boom times and

loaded them up with debt are now stuck with them [Defaults and Restructuring Next for Retailers].

Among the list of brick-and-mortar retailers to warn of crummy

holiday sales is luxury jeweler and specialty retailer Tiffany and

Company. It reported

this morning that sales during the holiday period fell 3% on a

constant-currency basis: 5% in the Americas and 6% in the Asia-Pacific

region. Sales at stores that were open at least a year dropped 5%. And

it lowered its guidance.

So it will do what American companies do best: There will be an

undisclosed number of job cuts, and there will be “occupancy reductions”

at its corporate office. This cost cutting will cost the company about 4

cents per share in the current quarter.

Shares fell 5.1% today to $64.22. They’ve plunged 41% from their all-time high of $108.68 at the end of December 2014.

Scrambling to not fall too far behind reality, analysts unleashed a

hail of downgrades, including Cowen & Co. which slashed its price

target from $90 to $75 and Nomura which chopped it from $100 to $90.

Tiffany is selling to the privileged, to the beneficiaries of QE’s

“wealth effect” in the US and around the globe. It’s selling to people

who benefited from the astounding debt-funded booms in Asia and

elsewhere over the past few years. Has the recent stock market rout

dented their purchasing power, or their willingness to splurge?

Tiffany blamed the “pressure from the strong US dollar”; it blamed

“foreign tourist spending” at its stores in the US; it blamed

“restrained consumer spending tied to challenging and uncertain global

economic conditions.”

But this has been Tiffany’s song and dance for a while. A year

ago, on January 12, 2015, Tiffany’s shares plunged 14% and three days

later hit the $85-range, down 21% from their all-time high two weeks

earlier.

The problem back then? It had reported

lousy holiday sales; it had lowered its outlook; it had blamed

“significant headwinds from the stronger US dollar” along with “other

global economic pressures.” Copy and paste.

But wait… Stock markets were booming back then. The China bubble was

in full swing. Asian millionaires were printed on an hourly basis.

European stocks were on steroids. Even the S&P 500 was still

trudging toward its high.

But it’s been getting tougher for brick-and-mortar retailers, and a

slew of them warned since November that holiday sales would be crummy,

and some warned more recently that holiday sales were in fact crummy.

Some, including Gap and Wal-Mart, are shuttering some of their stores.

Tiffany faces some jewelry-industry issues: “Jewelry is no longer at

the top of the Christmas list,” Neil Saunders, CEO of research firm

Conlumino, wrote in a note to clients, cited by Business Insider. “For a brand like Tiffany, where lavish gifting is an important driver of buying, such a trend is distinctly unhelpful.”

There are Tiffany-specific issues, including that it faces a “more

competitive environment for jewelry and the rise of other brands,”

Saunders said. “Against this backdrop Tiffany has lost some of its

relevance, especially to more moderate-spending shoppers.”

Then there are issues all retailers struggle with: Millennials, the

largest demographic these days, tend to spend more on experiences and

less on things, including expensive baubles. And retailers are facing

strung-out American consumers. But Tiffany isn’t actually targeting

strung-out consumers. It’s targeting the wealthy.

And here’s the problem for all our beleaguered brick-and-mortar

retailers: online sales this holiday season jumped 12.7% to a record $83

billion, Adobe Systems reported

today. And when push came to shove right before Christmas, with

delivery perhaps uncertain, the buy-online-pick-up-in-store option

kicked in. So it’s not like Americans have stopped shopping. They might

shop a tad less, but they’re shopping increasingly online.

That’s a structural problem that is gnawing its way into all

retailers’ earnings reports. It will never go away. It will only get

worse. So they drag out the “strong dollar,” “global headwinds,” “warm

weather,” or whatever other less indigestible excuses they can find. And

companies can simply copy and paste last year’s excuses into the next

earnings warning rather than admitting that online sales are gradually

but relentlessly eating their lunch.

So with impeccable timing – the very morning the Commerce Department

reported declining retail sales – Wal-Mart Stores disclosed in an SEC

filing that it was “committed to growing,” but was “being disciplined

about it.” Read…Wal-Mart Rubs Salt on Deepening Retail Wounds

Royal Bank of Scotland

warns his clients for a “cataclysmic year”, a deflationary global crisis

with oil down to $16 a barrel and a stock market correction with a

fifth. J.P. Morgan advises for the first time in 7 years to sell shares

on the bounce instead of buy the dip.

RBS credit team sais all alarm bells are ringing. They see the same stress alerts before the Lehman Brothers crisis in 2008. They said in a client note:

“Sell everything except high quality bonds. This is

about return of capital, not return on capital. In a crowded hall, exit

doors are small,”

Both global trade and loans are contracting, a nasty cocktail for

corporate balance sheets and equity earnings, and uncharted waters given

that debt ratios have reached record highs. China is ready for a huge correction and it will snowball the rest of the world.

Brent oil prices will continue to slide after breaking through a key

technical level at $34.40, with a “bear flag” and “Fibonacci” signals

pointing to a floor of $16. OPEC doesn’t seem to find the answer to the economic slowdown in Asia.

Beside oil prices, bond rates will also fall to new

lows. RBS predicts a 0,16% rate on the German Bund in a flight to

safety. Negative rates on the 10-year Bund is even possible when

deflation persist. And the ECB will lower short-term rate to -0,70%

in an attempt to fight deflation.

US Treasuries will fall to rock-bottom levels in sympathy, hammering

hedge funds that have shorted US bonds in a very crowded

“reflation trade”.

J.P. Morgan: selling shares on the rally

J.P. Morgan also send a note to his clients advising to sell stocks on any bounce. This is the first time in 7 years they advise selling shares:

“Our view is that the risk-reward for equities has

worsened materially. In contrast to the past seven years, when we

advocated using the dips as buying opportunities, we believe the regime

has transitioned to one of selling any rally,” said Mislav Matejka, an

equity strategist at J.P. Morgan.

There are not only technical issues for the stock market, but also

fundamental reason to sell. Fourth quarter results will probably be the

worst since the financial crisis. They won’t save the stock market this

time.

Further adding to the grim outlook is the slowdown in the

manufacturing sector, which pushed J.P. Morgan’s profit-margin proxy — the gap between pricing power and the wage costs — into negative territory in the fourth quarter for the first time since 2008.

The positive correlation between oil prices and earnings on top of

the sustained gains in the U.S. dollar — which has an inverse

correlation to results — will also weigh on the market.

(Jeff Nielson)

I spend most of my time dealing with U.S. economic lies simply because

it’s much easier to make my analytical points. There is a lot more

data, it’s splashed all over the place, and (usually) the lies are even

bigger South of the Border, which makes the analytical point more vivid.

However, in the month of December, the prices for fresh produce (in

Vancouver) spiked in the month of December at the highest rate I have

ever seen in my life, almost across the board. Prices rose for most

fresh produce by between 10% and 30% IN ONE MONTH, with some of the prices increase even larger.

– broccoli from $3/lb to $4/lb, a 33% increase (at the cheaper supermarkets)

– celery from $2/lb to $3/lb, a 50% increase

– strawberries from $4/lb to $8/lb, a 100% increase

But we’re used to seeing inflation numbers expressed as annualized

figures, so let’s convert those monthly numbers to annual numbers

broccoli – 400% inflation

celery – 600% inflation

strawberries – 1200% inflation

Now obviously I do not expect the numbers to rise again next month,

or even the month after. So I won’t go “Chicken Little” here, and claim

that hyperinflation has already arrived in Canada. But, the food

inflation rate in Canada is rising EXPONENTIALLY, overall. It was

roughly 20% per year, then roughly 30% per year, and (with even one or

two more price-shocks) we could easily be looking at a FOOD INFLATION RATE in CANADA of 50%.

Now the lies:

Cost of food in Canada increased 3.70 percent in December of 2015

over the same month in the previous year. Food Inflation in Canada

averaged 3.98 percent from 1951 until 2015, reaching an all time high of

20.18 percent in July of 1978 and a record low of -7.14 percent in

December of 1952. Food Inflation in Canada is reported by the Statistics

Canada.

Now lets compare the lies to the Truth (as evidenced by my grocery

receipts). Even if we assume that all other grocery spending is flat,

produce spending alone accounts for a large portion of every shopping

dollar.

I’ve gotten to know the manager quite well, at the supermarket where I

do most of my shopping. He tells me that I’m not alone in having

switched away from chemical-filled, GMO-polluted packaged foods, and

that a large portion of shoppers now exhibit that similar pattern. From

watching other shoppers, I think it’s relatively safe to say that those

who do not shop in this pattern are either older people (set in their

ways) or people who are simply too poor to shop healthier.

For a produce-heavy food basket, in Vancouver, in the month of

December, overall prices rose at least 10% (and looking at my own

grocery bills, it was more likely 15%). We’re forced to eat more fruits

and vegetables, because of EXPONENTIALLY RISING MEAT PRICES. Thus an explosion in prices for fresh produce will have a major impact on most (healthy) shoppers.

Even a 10% rise (in one month) translates to an annual, overall, food inflation rate in December of 120%. And it’s hard to believe that prices were not rising at a similar rate in much/most of Canada. Now back to the lies.

Cost of food in Canada increased 3.70 percent in December of 2015…reaching an all time high of 20.18 percent in July of 1978.

120% versus 3.7%That is a Big Lie. It just goes to show that in 2016, we here in Canada can now lie like the Americans…

Linux Mint 17.3 is the best Linux desktop operating system and it might be the best PC operating system, period, for you.

My buddy David Gewirtz recently wrote about the question of whether you should move from Windows 7 to Windows 10 or a Mac. I have another suggestion: Linux. Specifically Linux Mint 17.3, Rosa, with the Cinnamon desktop. Linux Mint 17.3 is a great replacement for Windows 7. In fact, it's a great desktop operating system period.

sjvn

Yes,

I'm serious. I use all the above desktops -- yes I'm a Windows 7 and 10

user as well as a Linux guy -- and for people I think Mint 17.3 makes a

great desktop.

I've been using Mint as my main Linux desktop for years now. Unlike some desktops I could name -- cough, Windows 8,

cough -- Linux Mint has never had a flop. Every year that goes by, this

operating system keeps getting better. The other desktops? Not so much.

Let's take a closer look.at Windows 7 vs. Linux Mint 17.3 UI Differences

There's really not much. While it's even easier for a Windows XP user to move to Mint

than a Windows 7 user, any Windows user won't have any trouble picking

up Linux Mint with Cinnamon. There's a Start Menu and settings are easy

to find.

I regard Cinnamon 2.8

as the ultimate Window, Icon, Menu, Pointer (WIMP) interface. Is it

ideal for tablets or smartphones? No. Is it perfect for long-time PC

users? Yes.

Cinnamon does add some nice features. For example, if

you mouse over the Window list, you'll now see a thumbnail for each

application. It also has improved performance, system tray status

indicators, and music and power applets.

What I like best about Cinnamon is that it doesn't get

in the way. There's no learning curve. You may have never used Linux in

your life but you can just sit down and start opening directories,

running applications, and modify your PC's settings.

One small

feature I like a lot, since I always run multiple workspaces, is that

the workspace switcher applet now shows a visual representation of

what's running in each workspace.

Don't like Cinnamon? Unlike any version of Windows, Linux Mint comes with many different desktops. These include KDE, MATE and Xfce. Find one you like and enjoy, Application Selection

It's

true that Linux doesn't have as many application choice as Windows

does. But, how many applications do you really need in 2016? I do most

of my work these days on the cloud with software-as-a-service (SaaS)

applications. These apps work just as well on Chrome, my favorite Web

browser, on Mint as they do on any other desktop.

That said, there are many excellent Linux desktop programs. For example, instead of Microsoft Office I use LibreOffice 5.

I don't use it because it's free, although most Linux desktop

applications won't cost you a cent, but because it's an excellent office

suite in its own right.

I also use Evolution instead of Outlook for e-mail and GIMP

instead of Photoshop for my basic graphic editing needs. The bottom

line is that are many great Linux programs that you can use in place of

Windows appliations.

Are there some Windows programs that you can't live without? Well, you don't have to live without them.

There are two ways to run Windows programs on Linux. One is to use CodeWeaver's CrossOver Linux. This program enables you to run many popular Windows applications on Linux. Supported Windows applications include Microsoft Office (from Office 97 to Office 2010), Quicken, and some versions of Adobe Photoshop.

The application you absolutely must have won't work with CrossOver? Then run it on a virtual machine (VM) program such as Oracle's VirtualBox.

I use both methods and they work well. Mobile Ecosystem Compatibility

I don't care what some people say, Windows Phone is dead to me. And, pretty much everyone else.

Mint,

however, is a pure desktop play. Yes, Android is Linux, but it runs in

parallel with the desktop Linux distribution. That may change as Android

creeps toward the desktop, but we're not there yet. Ubuntu, which is Mint's foundation Linux distribution, parent company Canonical

is working hard on making its same code base work on PCs, smartphones,

and tablets. So, eventually, you may be running Mint on smartphones. I'm

not holding my breath.

If you want one operating system family

on all your devices, don't waste your time -- for now -- on either Linux

or Windows. Just go ahead and buy an iPhone and a Mac and be done with

it. Reliability

This is not even a conversation.

While Windows 7 is far more stable than any other version of Windows, I haven't had Linux Mint ever -- ever -- stop working.

If you want a desktop that can take a licking and keep ticking, you want Linux, not Windows or Mac OS X. Security

Really? Do you even have to ask?

Every lousy day a new piece of Windows malware shows up. Windows is more secure than it once was, but it's still easy to bust.

Linux, on the other hand, despite the garbage you read about Linux viruses and such, is almost never sucessfully attacked.

Oh,

yes, Linux has been broken into multiple times. But, in almost every

case, the attack relies on a user with super-user priviledges working

hand in glove with an attacker to break in. If a system administrator

installs malware who's really to blame for the cracked computer? The

operasting system or the incompetent system manager? I know which one

I'd be kicking out of my office. Upgrade Cost

Windows

10 is usually free now -- even if you don't actually want it. Micrsoft

continues to find new and interesting ways to shove it down your throat

such aa making Windows 10 a recommended update.

Mint,

though, was free when it began, it's free now, and will always be free.

If you decide a particular version of Mint is the cat's meow, you can

keep using it until the bits fall off the hard drive because of rust. Switching Costs

Windows

10 can run on most newer Windows 7 systems without any fuss. On the

other hand, I can run Mint on Windows XP systems. Give me 512MBs of RAM,

and I'm in business with Mint.

Mind you, I'd much rather have

2GBs, but you really can run Mint on pretty much any hardware hiding out

in your office's back room.

The real cost will be in traning and

applications. As I mentioned earlier, however, Mint doesn't have much

of a learning curve. As for applications, almost all Linux programs are

free. If, as many offices do now, you realy on SaaS apps for producivity

you won't see one thin dime more in software migration costs. Directory Integration

What's that you say? You use Active Directory (AD) for system management and supporting it is a must? No problem.

You just install BeyondTrust's PowerBroker, formerly Likewise, and in a few minutes your Mint machines will be in your AD forest. Next question? The Bottom Line

Linux Mint is an excellent Windows 7 replacement. I've used it for years now and I've found it to be the best desktop out there.

Is it better than Windows 10? I think so. It's certainly more stable and secure.

Should

you move to it? I recommend you try it for yourself. Like all desktop

Linux distributions, it's easy to try and it's free. Just download a copy of Mint, 64-bit Cinnamon would be my pick, and install it. If you're installing Mint on a system with UEFI Secure Boot, you may have to jump through a few hoops. I say "may" because neither I nor J.A. Watson have had any trouble with it.

Once you're done, I think you'll soon find that Mint is a great replacement for Windows 7.

Anyone with no coverage is going to be hit hard this tax season.

Originally it was $95. What a great fucking scam you muslim loser. Blame

the supreme court that sold out america. HOW CAN YOU MANDATE SOMEONE

HAVING COVERAGE AND FINE THEM?

Straight from the official government website.

The fee for not having health insurance in 2016

The fee is calculated 2 different ways – as a percentage of your

household income, and per person. You’ll pay whichever is higher.

Percentage of income

2.5% of household income

Maximum: Total yearly premium for the national average price of a Bronze plan sold through the Marketplace

Per person

$695 per adult

$347.50 per child under 18

Maximum: $2,085

Penalize people that work that can’t afford the coverage to give to

losers that sit on their ass and get the free coverage. Maybe just maybe

one day this government will collapse on the weight of their own

stupidity and corruption.

You cannot force someone to own a product, especially a govt product.

AC

Wells Fargo & Co (WFC.N) has the largest exposure to loans to

energy companies among major U.S. lenders, a report from Raymond James

said, amid concerns that banks may have to set aside more money to cover

bad loans to the industry.

The bank also topped the list with the biggest exposure to energy

companies whose public debt was trading less than 35 percent of par, the

brokerage said on Thursday.

Wells Fargo was followed by Bank of America Corp (BAC.N), Citigroup Inc (C.N), Comerica Inc (CMA.N) and BB&T Corp (BBT.N).

http://www.reuters.com/article/us-usbanks-research-idUSKCN0RO29220150924

West Virginia Woman Sues Wells Fargo Over Alleged Home Loan Modification Misrepresentations

In early 2015, she contacted the company about modifying her loan. At

that point, a rep for Wells Fargo Home Mortgage instructed her not to

make payments while the modification was being processed.

Relying on the information from the rep, the woman stopped payment,

while providing all necessary paperwork for the modification.

In June 2015, Wells Fargo re-sent the woman a packet requesting

duplicate documents. The following month, the woman says she began

receiving debt collection calls.

When the woman called Wells Fargo about the collection calls, she was

told that her account was mistakenly removed from the modification

program and placed in foreclosure. West Virginia Woman Sues Wells Fargo Over Alleged Home Loan Modification Misrepresentations

Wells Fargo & Co, No.3 U.S. bank by assets

* “At current price levels, we would expect to have a higher oil and gas losses in 2016.”

Morgan Stanley, No.6 U.S. bank by assets

* “We’ve seen an increase in negative marks within corporate loan book, focus is around energy.” http://www.zerohedge.com/news/2016-01-21/what-big-banks-say-about-their-energy-exposure

Wells Fargo to pay $1.2 billion for bad mortgages

Wells Fargo & Co. said Wednesday that it has agreed to pay $1.2

billion to settle a long-running suit that accused the company of

“reckless” lending and leaving a federal insurance program to pick up

the tab.

The agreement settles civil charges with the U.S. Justice Department,

two U.S. attorneys and the Department of Housing and Urban Development

The government sued Wells Fargo in 2012, accusing the U.S. mortgage

lender of engaging in “regular practice of reckless origination and

underwriting” of government-backed loans. The action was one of several

brought under the Federal False Claims Act against a lender accused of

bilking the Federal Housing Administration, which has historically

backed loans to first-time buyers and those with low incomes. http://www.marketwatch.com/story/wells-fargo-to-pay-12-billion-for-bad-mortgages-2016-02-03?link=MW_home_latest_news

The US car maker is cutting costs across Europe but production workers will be spared, with admin and marketing staff hit.

Car maker Ford is to shed hundreds of jobs in the UK and Germany as part of a programme to save $200m (£138m) a year.

The group said it was launching a voluntary redundancy

programme as it looked to slash costs across its European business, in

the face of mounting regulatory costs.

It comes after Ford recently revealed that its European

operation had returned to profit for the first time in four years in

2015.

Production and product development workers will not be

affected by the job cuts. The company said they were mainly likely to go

in administration and marketing.

Ford no longer makes cars in Britain but still employs

14,000 workers in the country. Plants in Dagenham and Bridgend make car

parts and there are also sites in Dunton in Essex, Daventry in

Northamptonshire, and a head office at Warley in Essex. The company

employs 53,000 people in Europe.

Jim Farley, head of Ford's European, Middle East and Africa

business, said: "In the past three years, Ford of Europe has improved

its business in all areas and moved from deep losses to a $259m (£179m)

profit in 2015. This is a good first step.

"We are absolutely committed to accelerating our

transformation, taking the necessary actions to create a vibrant

business that's solidly profitable in both good times and down cycles.

"We are creating a far more lean and efficient business that can deliver healthy returns and earn future investment.

"Our job is to make our vehicles as efficiently as possible,

spending every dollar in a way that serves customers' needs and

desires, and creating a truly sustainable, customer-focused business."

Ford has already shut three car plants in western Europe in

2013 and reached cost-saving agreement with unions in Germany and said

that it was continuing to "enhance its cost efficiency and manufacturing

capacity utilisation".

Its latest announcement on jobs involves what the company calls a "voluntary separation programme".

Meanwhile, Ford is also boosting its product line in Europe with seven new and updated vehicles being launched this year.

Hybrid and electric vehicles are to be introduced in Europe

by 2020 as part of Ford's previously-announced $4.5bn (£3.1bn)

investment in electrified vehicles.

By John Vibes

The homeless people in Hackney, London are facing expulsion

from the street due to a new law will allow the police to give out

fines and other legal penalties to homeless people who are found

loitering, begging and sleeping in commercial places.

This “Public Space Protection Order” which was introduced by the

council of Hackney will place a fine of £1000 on homeless activities.

The order has been met with numerous criticisms, with many pointing out

that the new laws effectively outlaw homelessness.

Matt Downie of homelessness charity Crisis, one of the major

opponents of this legislation, said that the homeless population in

London has been victimized enough.

“Rough sleepers deserve better than to be treated as a nuisance –

they may have suffered a relationship breakdown, a bereavement or

domestic abuse. Those who sleep on the streets are extremely vulnerable

and often do not know where to turn for help. These individuals need

additional support to leave homelessness behind, and any move to

criminalize sleeping rough could simply create additional problems to be

overcome,” Downie said.

A similar scenario was supposed to happen in Oxford, but during the

consultation process, there was so much outcry from the local population

that the government was forced to pull back on their proposal. In the

case of Hackney, there was not a single consultation before the policy

was introduced.

The policy has been largely rejected by people in Hackney, and there

have been thousands of people to sign petitions that ask for the ban to

be lifted. However, it is not clear if the city has any intention of

paying attention to these people.

We have covered many other instances of homelessness being

criminalized in recent months. As we reported just a few weeks ago, that

homeless people and supporters in Sacramento were protesting a recent ordinance

that makes it illegal for them to camp in the city. Many of them were

camped out in front of city hall for the past month and are demanding a

reversal of the camping ban. Soon after, police invaded the encampment in riot gear and made several arrests.

In another story, we recently covered a homeless man was arrested in Fairfax Virginia this week after police discovered a home that he made for himself in a local park.

This article (http://www.trueactivist.com/new-law-in-london-would-fine-homeless-1000-for-sleeping-outside-or-loitering/New

Law In London Would Fine Homeless £1,000 For Sleeping Outside Or

“Loitering”) is free and open source. You have permission to republish

this article under a Creative Commons license with attribution to the author and TrueActivist.com. John Vibes is an author and researcher who organizes a number of

large events including the Free Your Mind Conference. He also has a

publishing company where he offers a censorship free platform for both

fiction and non-fiction writers. You can contact him and stay connected

to his work at his Facebook page. You can purchase his books, or get your own book published at his website www.JohnVibes.com.

Here's a step-by-step guide to get Windows XP running on an Oracle VirtualBox-based virtual machine on Linux Mint

Here's a step-by-step guide to get Windows XP running on an Oracle VirtualBox-based virtual machine on Linux Mint

By John Vibes

By John Vibes