Sunday, June 1, 2014

New federal database will track Americans' credit ratings, other financial information

As many as 227 million Americans may be compelled to disclose intimate details of their families and financial lives -- including their Social Security numbers -- in a new national database being assembled by two federal agencies.

The Federal Housing Finance Agency and the Consumer Financial Protection Bureau posted an April 16 Federal Register notice of an expansion of their joint National Mortgage Database Program to include personally identifiable information that reveals actual users, a reversal of previously stated policy.

FHFA will manage the database and share it with CFPB. A CFPB internal planning document for 2013-17 describes the bureau as monitoring 95 percent of all mortgage transactions.

FHFA officials claim the database is essential to conducting a monthly mortgage survey required by the Housing and Economic Recovery Act of 2008 and to help it prepare an annual report for Congress.

Critics, however, question the need for such a “vast database” for simple reporting purposes.

In a May 15 letter to FHFA Director Mel Watt and CFPB Director Richard Cordray, Rep. Jeb Hensarling, R-Texas, and Sen. Mike Crapo, R-Idaho, charged, "this expansion represents an unwarranted intrusion into the private lives of ordinary Americans."

Crapo is the ranking Republican on the Senate Banking, Housing and Urban Affairs Committee. Hensarling is chairman of the House Financial Services Committee.

Critics also warn the new database will be vulnerable to cyber attacks that could put private information about millions of consumers at risk. They also question the agency’s authority to collect such information.

Earlier this year, Cordray tried to assuage concerned lawmakers during a Jan. 28 hearing of Hensarling's panel, saying repeatedly the database will only contain “aggregate” information with no personal identifiers.

But under the April register notice, the database expansion means it will include a host of data points, including a mortgage owner’s name, address, Social Security number, all credit card and other loan information and account balances.

The database will also encompass a mortgage holder’s entire credit history, including delinquent payments, late payments, minimum payments, high account balances and credit scores, according to the notice.

The two agencies will also assemble “household demographic data,” including racial and ethnic data, gender, marital status, religion, education, employment history, military status, household composition, the number of wage earners and a family’s total wealth and assets.

Only 12 public comments were submitted during the 30-day comment period following the notice's April 16 publication.

The mortgage database is unprecedented and would collect personal mortgage information on every single-family residential first lien loan issued since 1998. Federal officials will continue updating the database into the indefinite future.

The database held information on at least 10.1 million mortgage owners, according to a July 31, 2013, FHFA and CFPB presentation at an international conference on collateral risk.

FHFA has two contracts with CoreLogic, which boasts that it has “access to industry’s largest most comprehensive active and historical mortgage databases of over 227 million loans.”

Cordray confirmed in his January testimony that CoreLogic had been retained for the national mortgage database.

The credit giant Experian is also involved in the mortgage database project, according to an FHFA official who requested anonymity.

Rep. Randy Neugebauer, R-Texas, who sits on the Hensarling panel and who has followed the mortgage database's development, said he was “deeply concerned” about the expansion.

“When you look at the kinds of data that are going to be collected on individuals, just about anything about you is going to be in this database,” he told the Examiner in an interview.

Critics of the database span the financial spectrum, including the U.S. Chamber of Commerce's Center for Capital Markets Competitiveness and the National Association of Federal Credit Unions.

In a May 16 letter to FHFA, NAFCU's regulatory affairs counsel, Angela Meyster, said the database "harbors significant privacy concerns" and "NAFCU believes greater transparency should be provided by the FHFA and CFPB on what this information is being used for."

Meyster told the Examiner that "it goes back to the breadth of information that they’re asking for without really speaking to what they will be used for."

Meyster said she was unconvinced. "It seems they’re just adding information and they’re not really stating where it’s going or what it’s going to be used for. There’s no straightaway answer. They say they are trying to assemble as much information that they can."

Neugebauer agreed. "Why are we collecting this amount of data on this many individuals?" he asked in the interview.

The Chamber of Commerce said that while Congress did ask for regular reports, it never granted FHFA the authority to create the National Mortgage Database.

“Congress did not explicitly require (or even explicitly authorize) the FHFA to build anything resembling the NMD,” the Chamber told Watt in its May 16 letter.

Cordray in his testimony told the House, "We’re making every effort to be very careful" but he could not promise there would never be a data breach.

Neugebauer said the hacker threat is real. "If someone were to breach that system, they could very easily steal somebody’s identity."

Meyster said she doubts the government can protect the data. “We’re essentially concerned that these government systems don’t have the necessary precautions to make sure that individual consumers are identified through the database,” she said.

Computerized theft of government and commercial data is a major concern for federal officials. Indictments were made public last week for five Chinese military members who allegedly hacked into the computer systems of six American corporations.

A December report from the Government Accountability Office on breaches containing personally identifiable information from federal databases shows unlawful data breaches have doubled, from 15,140 reported incidents in 2009 to 22,156 in 2012.

A May 1 White House report on cybersecurity of federal databases also recently warned, "if unchecked, big data could be a tool that substantially expands government power over citizens.”

IMF board approves $4.6 bln in aid for Greece

(Reuters) - Greece is set to receive $4.6 billion from the International Monetary Fund after the institution's board on Friday signed off on the latest review of Greece's rescue package.

The disbursement comes after the IMF and Greece's European lenders finished analyzing Greece's progress under its 173 billion euro ($236 billion) bailout in March, ending six months of protracted negotiations. Greece last got an IMF aid disbursement in July 2013, of $2.3 billion.

The IMF has so far lent Greece about $15.8 billion under a four-year program, meant to help Athens recover from a sovereign debt crisis, rebuild its economy and return to markets.

Given the delay with the fifth review, Greece should get the equivalent of three more disbursements this year, spread out over any remaining reviews, the IMF said.

The Washington-based global lender praised Greece's progress in cutting its debt and bringing its primary budget into surplus ahead of schedule.

"Greece has gone from having the weakest to the strongest cyclically-adjusted primary fiscal balance in the euro area in just four years," Naoyuki Shinohara, deputy managing director at the IMF, said in a statement. The primary balance excludes interest payments and other one-off items.

"(But) public debt is projected to remain high well into the next decade, despite a targeted high primary surplus," Shinohara said.

Greece's budget surplus, announced in April, is a sign of the progress the euro zone country has made to fix its finances after four years of tough bailout-imposed austerity that wiped out almost a quarter of its GDP and sent unemployment to record highs of nearly 28 percent. [ID:nL6N0NF2MX]

But the country's total debt is still about 175 percent of its annual economic output, a level economists consider as unaffordable in the long run. The IMF believes Greece must bring debt down to 110 percent of GDP by 2022 to keep it sustainable.

Greece is unlikely to reach that level without further debt relief from euro zone governments, which now hold more than 80 percent of Greece's public debt. The European Union in late 2012 promised to provide further debt relief to Greece as long as it meets targets for its primary budget surplus and reforms.

But it is unclear when the debt relief would come through or what form it could take. The European Commission last month said discussions would start in the second half of this year.

The IMF's Shinohara repeated that the IMF welcomed European pledges of further support to Greece. Under its rules, the IMF cannot continue to lend to countries if it believes their debt is unsustainable.

($1 = 0.7328 Euros)

(Reporting by Anna Yukhananov; Editing by James Dalgleish and Chizu Nomiyama)

Google Street View Shows Decay of Detroit Neighborhoods Since 2008

Since there’s some attention coming this way, I should probably take a

moment to explain this blog — which has mostly been a context-less

index of stuff found while virtually driving the streets of Detroit.

I’ll start with this:

"Detroit’s getting better — sure, there are neighborhoods that have problems, but they’ve been that way for 30 or 40 years."

I’ve heard statements like this a number of times in conversation and online. The idea that problems with Detroit’s property issues are decades old. Some of the root causes are certainly buried that far back, but this idea distorts what I think is still a little understood fact: The 2008-9 financial crisis had a devastating impact on the state of property in Detroit.

2009

2011

July 2013

August 2013

Continue reading and see more images: http://goobingdetroit.tumblr.com/

"Detroit’s getting better — sure, there are neighborhoods that have problems, but they’ve been that way for 30 or 40 years."

I’ve heard statements like this a number of times in conversation and online. The idea that problems with Detroit’s property issues are decades old. Some of the root causes are certainly buried that far back, but this idea distorts what I think is still a little understood fact: The 2008-9 financial crisis had a devastating impact on the state of property in Detroit.

2009

2011

July 2013

August 2013

Continue reading and see more images: http://goobingdetroit.tumblr.com/

Siemens may slash 12,000 jobs says boss

German

industrial giant Siemens has said it is weighing cuts of nearly 12,000

jobs around the world as part of a major restructuring.

Chief executive Joe Käser told a conference of investors and analysts in New York on Thursday that a previously announced cost-cutting drive would create "noticeable changes all across the entire organisation", a spokesman, Michael Friedrich, confirmed.

Some 7,600 positions will be "affected" as part of a company overhaul announced by Käser on May 7 in which 16 divisions will be consolidated into nine and certain levels of hierarchy will be eliminated, Friedrich said.

Another 4,000 jobs are in question as part of a regrouping of regional activities due at the start of the fiscal year on October 1.

However Käser attempted to calm the waters in a letter to staff, insisting that not all 11,600 positions would be slashed.

Source and full story: The Local (Germany), 31 May 2014

Chief executive Joe Käser told a conference of investors and analysts in New York on Thursday that a previously announced cost-cutting drive would create "noticeable changes all across the entire organisation", a spokesman, Michael Friedrich, confirmed.

Some 7,600 positions will be "affected" as part of a company overhaul announced by Käser on May 7 in which 16 divisions will be consolidated into nine and certain levels of hierarchy will be eliminated, Friedrich said.

Another 4,000 jobs are in question as part of a regrouping of regional activities due at the start of the fiscal year on October 1.

However Käser attempted to calm the waters in a letter to staff, insisting that not all 11,600 positions would be slashed.

Source and full story: The Local (Germany), 31 May 2014

Report: 90% of Private Employers Will Drop Insurance by 2025

A new report by !Q Capital found that by 2025 only 10% of employers will offer insurance to their employees.

'National disaster': Spain sees 500% rise in ‘very long-term unemployment’

Over one million people in Spain - the eurozone's fourth largest economy - haven't had a job since 2010, according to a report by Spain's National Statistics Institute. Although this number continues to rise, the government says it's witnessing recovery.

The numbers, published on May 23, show that “very long-term unemployment” in the country has risen by more than 500 percent since 2007. That year, about 250,000 Spaniards were unemployed after losing their job at least three years prior. That number drastically rose to 1.27 million in 2013 - 234,000 more than in 2012.

Generally, long-term unemployment includes jobless workers who have not been employed for more than 27 weeks. The recent study shows that this category in Spain has transformed to very long-term unemployment, with hundreds of thousands people without a job for at least three years, and is now represented by over 23 percent of the total jobless population in Spain.

The number is much higher than in other countries in the region at the same economic level, with another recent study showing that 26 percent of the country's population is on government benefits in Spain - the second highest total in the EU after Greece.

Still, politicians claim the nation emerged from years of on-and-off recession in mid-2013 and the situation continues to improve. On May 29, Spain reported its fastest economic growth since 2008, when the ten-year property bubble burst and prompted a financial crisis.

With millions of people searching for work in vain in the eurozone's fourth largest economy (behind Germany, France, and Italy), the International Monetary Fund said this week that the country's recovery is here to stay. “Spain has turned the corner,” the IMF's annual report on the country's economy stated.

Earlier this year, Spain’s Economy Minister Luis de Guindos told parliament that in 2013 the economy saw the fastest growth the country had seen in six years. A couple months later, a study by Spain’s second biggest bank, BBVA, said that unemployment rates would take over a decade to recover to pre-crisis levels.

Older jobless Spaniards are in a worse position than younger ones, who are more flexible and can emigrate and try to find work in other countries. But those with families and financial commitments are in danger of never finding work again. Edward Hugh, a British economist based in Spain, told the Spain Report that the situation is disastrous: "Many of these people are now 'structurally unemployed,' and many of those over 50 may never work again. It’s a national disaster,” he said.

Spain's new, smaller parties earned a relatively high number of votes in the recent EU elections. One of the newcomers, the Podemos (We Can) party, received almost eight percent of the votes, enough for five seats in the European Parliament. One of the political movement's MPs told The Spain Report that "a howl of protest against the unfairness, crushed dreams and hopeless futures caused by the existing economic system” is at the heart of the new party's support base.

Among the thousands of people who have taken to the streets protesting Spain's austerity measures and unemployment situation over the years, males who studied environmental protection and females with degrees in architecture and construction training are in the worst positions in terms of finding a job. The latest report shows that unemployment rates in these sectors are the highest, up to 47 percent. The programs that showed the lowest rates of unemployment for both genders were mathematics and statistics.

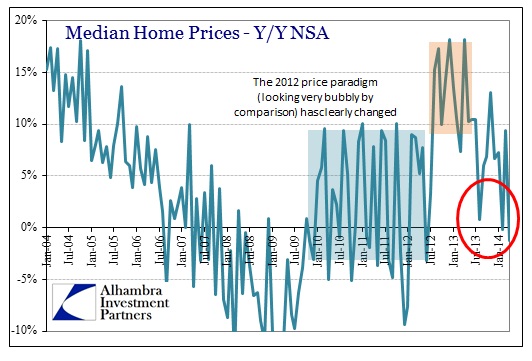

Last Year’s QE Boost To Housing Is Already Over And Done

I often

stand in amazement at what passes for conventional wisdom, or more

precisely what is being attempted as such. Only one year ago the

tendency to view the housing market as the next great growth engine was

ubiquitous all across economic commentary. It had “clearly” and

“unarguably” turned from a maddening headwind to a comforting tailwind.

More than a little backslapping in policy quarters had taken place;

victory laps and all that.

There was some growing discomfort with the pace of expansion, particularly in comparison with prior experience during the “obvious”

bubble days, but such concerns were thought to be minor in the

afterglow of “successful” QE. Going back further in time, the third

episode and its adventure in MBS TBAwas expressly offered for just that intent – to restart housing nearly from scratch.

Now the

tune has changed dramatically, to the point of being unable to

recognize those same conclusions. What was obvious last year has been

lost and replaced with no end of contradiction.

“Mortgage financing is extremely tight,” said Ellen Zentner, senior economist at Morgan Stanley in New York. “And that’s not something the Fed can manipulate.”

How do

you reconcile that statement with last year? The whole point of QE3 was

to “loosen” mortgage finance to the point housing could be manipulated

into an economic growth factor. The very mechanics of QE3 follow exactly

that course, as it created an increase in spread (lower production

coupons) that made lending in volume more profitable. That’s not

something the Fed can manipulate? That was the entire point.

The trouble from the Fed’s perspective is that many of the forces holding housing back are outside of its control. While the Fed can influence mortgage rates through its conduct of monetary policy, it can’t do much, if anything, to counteract the other causes of faltering demand: lagging household formation, stingy lenders and wary borrowers.

Those

factors were readily evident last year too. Lenders were stingy then as

lending standards have remained tight throughout; it is only recently that

the GSE’s are being courted to reduce standards and head back toward

bubble profligacy. Those wary borrowers were the exact opposite before

May 2013, particularly in refis, attracted so because of the behavior of

interest rates.

It is the inclusion of household formation that stands out here, however. All of these factors cited are common as remnants of past monetarism.

The author of the article is blaming past monetarism for the failures

of current monetarism, without acknowledging that it was current

monetarism that changed the character of housing from last year to this

year. The FOMC was nearly omniscient last year, but now is utterly

helpless?

The

tortured asset and housing markets are merely the expressions of using

those channels for policy aims. And this is more than a little bit

childish – when it moves in the “right” direction, the Fed meant to do

it; when it moves in the “wrong” direction someone or something else is

to blame. The real truth lies in interest rate targeting and the fusion

of that with the desire to control “aggregate demand.” Destroying price

signaling, as this “control” does (including artificial financial profit

subsidies), renders “markets” overly susceptible to bubbling.

The current “helplessness” of the central bank is nothing more than the inevitable downside of its own experimentations.

The pace of new home sales recently seems to have hit a ceiling.

It is

more than a little curious that such a ceiling is located right at the

bottom edge of what I would call the historical range. That provides as

much evidence for a bubble as anything, since prices have advanced at a

pace consistent with the middle of the last decade on only a fraction of

the volume. In the grand scheme of the economy, that is actually

fortunate in that the leftovers of the last bubble (household formation,

lending standards) have actually prevented a wider misallocation. In

other words, actual market forces are preventing policy aims from making

it far, far worseonce again. But to policymakers, that was a “drag” to be overcome.

The

problem for the rest of this year is whether or not those that have

ignored actual market signals for the comfort of last year’s central

bank “omniscience” will be forced to the exits in an orderly fashion; or

whether recent signals from the “utterly helpless” part of the FOMC

blame deflection apparatus will spark something more like disorder. The

former will be unhelpful; the latter would be more than a small drag.

In any case, whether or not you feel the Fed is helpless here does not take away ownership of all of these zig zags tracing back into the 1990’s.

Europe has an even bigger crisis on its hands than a British exit:

If Europe's policy elites could not

quite believe it before, they must now know beyond much doubt that

they have lost Britain. This island is no longer part of the European

project in any meaningful sense.

British defenders of the status quo were knouted on Sunday. UKIP won 27.5pc of the vote, or 29pc after adjusting for the negligence - or worse - of the Electoral Commission in allowing a spoiler party with much the same name to sow confusion. Margaret Thatcher's Tory children are scarcely more friendly to the EU enterprise.

Britain's decision to stay out of monetary union at Maastricht sowed the seeds of separation, as pro-Europeans fully understood at the time, though almost nobody expected EMU officialdom to clinch the argument so emphatically by running the currency bloc into the ground with 1930s Gold Standard policies and youth unemployment levels above 50pc in Spain and Greece, and above 40pc in Italy.

European leaders must henceforth calculate that the British people will vote to leave the EU altogether unless offered an entirely new dispensation: tariff-free access to the single market along lines already enjoyed by Turkey or Tunisia; and deliverance from half the Acquis Communautaire, that 170,000-page edifice of directives and regulations that drains away sovereignty, and is never repealed.

Ideological hardliners would prefer to see Britain leave rather tolerating any reversal of the one-way Monnet Doctrine, and some talk of shutting British goods out of the European markets. They are fanatics. Others know that the EU's global credibility would be shattered if one of its largest states - and twin-leader in projecting military power - were to walk away in disgust, as Germany's Wolfgang Schauble has repeatedly warned. - See more at: http://xrepublic.tv/node/9183#sthash.142c3mYA.dpuf

British defenders of the status quo were knouted on Sunday. UKIP won 27.5pc of the vote, or 29pc after adjusting for the negligence - or worse - of the Electoral Commission in allowing a spoiler party with much the same name to sow confusion. Margaret Thatcher's Tory children are scarcely more friendly to the EU enterprise.

Britain's decision to stay out of monetary union at Maastricht sowed the seeds of separation, as pro-Europeans fully understood at the time, though almost nobody expected EMU officialdom to clinch the argument so emphatically by running the currency bloc into the ground with 1930s Gold Standard policies and youth unemployment levels above 50pc in Spain and Greece, and above 40pc in Italy.

European leaders must henceforth calculate that the British people will vote to leave the EU altogether unless offered an entirely new dispensation: tariff-free access to the single market along lines already enjoyed by Turkey or Tunisia; and deliverance from half the Acquis Communautaire, that 170,000-page edifice of directives and regulations that drains away sovereignty, and is never repealed.

Ideological hardliners would prefer to see Britain leave rather tolerating any reversal of the one-way Monnet Doctrine, and some talk of shutting British goods out of the European markets. They are fanatics. Others know that the EU's global credibility would be shattered if one of its largest states - and twin-leader in projecting military power - were to walk away in disgust, as Germany's Wolfgang Schauble has repeatedly warned. - See more at: http://xrepublic.tv/node/9183#sthash.142c3mYA.dpuf

Ukraine’s GDP to drop by 5% in 2014 – Fitch

Fitch Ratings has predicted that Ukraine’s GDP will diminish by five percent in 2014, as the crisis will continue to weigh on the protest-torn country's economy.

“We forecast GDP to contract by 5 percent this year,” Charles Seville, director for sovereigns at Fitch Ratings in London, said in an article titled 'New Ukrainian President Faces Major Challenges.'

“Ex-Crimea, industrial production shrank 6 percent year on year in April, and consumer spending is well down, especially in the east,” he continued.

While inflation in April was 3.3 percent, the agency predicts it will rise due to gas tariffs and pass-through of exchange rate depreciation.

“Public finances are under pressure but the government has increased tax collection and contained spending, narrowing the fiscal deficit,” the article states.

Earlier this month, effective May 1, Ukraine increased the minimal rate for natural gas for the needs of the population by 51.1 percent. From June 1, it will increase the fees for electricity by between 20 to 60 percent, depending on the volume of electricity consumption.

At the same time, “political stability, sustainable growth, and moderation in fiscal and external imbalances would be credit positive and could ultimately result in an upgrade.”

Ukraine's presidential election may reduce near-term political uncertainty and, hence, offer some support to its sovereign credit profile as well “potentially” bring partial agreement with Russia, according to Fitch’s Seville.

The country’s “most pressing problems” include instability and uprising in the east, the dispute with Russia over gas payments, obeying the IMF program - as the execution risk remains high - and maintaining reserves while meeting external funding needs, Seville wrote.

“Some immediate risks have receded. The disbursement of US$3.2 billion by the IMF and issuance of a $1 billion bond guaranteed by the US on May 16 eased immediate external liquidity concerns and covers Ukraine's scheduled $1 billion Eurobond maturity next week. But external repayments remain heavy in 2014, including Naftogaz's government-guaranteed September Eurobond,” he added.

BlackRock’s Rieder: Treasuries ‘aren’t that bad’; we’ve shifted some assets out of the peripheral

BlackRock Inc., Co-Head

Americas Fixed Income, Rick Rieder said BlackRock has shifted some

assets out of peripheral bonds and yields will remain in a “low range

for a long while.” Rieder said U.S. treasuries — which he predicts will

“drift higher” – “don’t look that bad compared with the rest of the

world” after a bond-market surge pushed yields to the lowest level in a

year.

The manager of BlackRock

Strategic income made remarks this morning in an interview with

Bloomberg’s Tom Keene, Scarlett Fu and Adam Johnson on “Bloomberg

Surveillance.”

*CREDIT: BLOOMBERG TELEVISION’S “SURVEILLANCE”**

Read more at http://investmentwatchblog.com/blackrocks-rieder-treasuries-arent-that-bad-weve-shifted-some-assets-out-of-the-peripheral/#xHSDisIGt6RC5Feu.99

Gold And Silver – Debt Is Trouncing Precious Metals, For Now.

Animal Farm and 1984, meet 2014. The Western world no longer makes any sense, and

common sense has been sidelined for decades. It is lies, deceit, and debt ruling supreme.

The “American Way” [which once was a standard for emulation] is now a source of

embarrassment, advanced by the bankrupt federal government doing the bidding of the

moneychangers, those who adhere to and hide behind the Rothschild formula. What is

that formula? It has been expressed here on several occasions:

common sense has been sidelined for decades. It is lies, deceit, and debt ruling supreme.

The “American Way” [which once was a standard for emulation] is now a source of

embarrassment, advanced by the bankrupt federal government doing the bidding of the

moneychangers, those who adhere to and hide behind the Rothschild formula. What is

that formula? It has been expressed here on several occasions:

Give me control of a nation’s money, and I care not who makes the laws.”

Mayer Amschel Rothschild.

Mayer Amschel Rothschild.

Whether Rothschild actually said it or not, this is the most profound statement, and its

reality has seized the entire wealth of the Western world. Rothschild learned early on how

incredibly profitable it was to lend to nations instead of individuals, and at times of war,

profits soared even more. Wars were expensive. Troops had to be paid, munitions bought,

and over a period of time, the expense of war drained a nation’s treasury.

reality has seized the entire wealth of the Western world. Rothschild learned early on how

incredibly profitable it was to lend to nations instead of individuals, and at times of war,

profits soared even more. Wars were expensive. Troops had to be paid, munitions bought,

and over a period of time, the expense of war drained a nation’s treasury.

Being recognized as the source for available funding, kings and rulers readily turned to

the Rothschild family for money. The Rothschilds always demanded gold and silver in

repayment, and when that ran out, control over the issuance of a nation’s money was

then demanded. Long story short, with its unparalleled, and unfathomable by most to

the extent of its accumulation, the Rothschild banking clan became almost the only

source of money to run a country.

the Rothschild family for money. The Rothschilds always demanded gold and silver in

repayment, and when that ran out, control over the issuance of a nation’s money was

then demanded. Long story short, with its unparalleled, and unfathomable by most to

the extent of its accumulation, the Rothschild banking clan became almost the only

source of money to run a country.

While this may seem repetitive and, to some degree accepted as true, the review is

presented as context for what follows.

presented as context for what follows.

What may not be as widely known is that the English Rothschild bank funded the North

in America’s Civil War, while the French Rothschild bank funded the South. It did not

matter who would win, the Rothschild’s were going to increase both their wealth and,

more importantly for them, their influence in US politics. That had always been their

primary objective.

in America’s Civil War, while the French Rothschild bank funded the South. It did not

matter who would win, the Rothschild’s were going to increase both their wealth and,

more importantly for them, their influence in US politics. That had always been their

primary objective.

Lincoln did not want to pay the bankers up to 36% interest for loans to fund the war.

He decided to issue Greenbacks by the US government, interest free so that the country

was not burdened with any interest costs, a very big deal. Lincoln was assassinated, [draw

your own conclusions], and after his death, Congress immediately repealed the Greenback

law. It should be known that when Lincoln announced his use of interest-free money as a

source of funding, bankers stormed to Washington D C t o complain bitterly.

He decided to issue Greenbacks by the US government, interest free so that the country

was not burdened with any interest costs, a very big deal. Lincoln was assassinated, [draw

your own conclusions], and after his death, Congress immediately repealed the Greenback

law. It should be known that when Lincoln announced his use of interest-free money as a

source of funding, bankers stormed to Washington D C t o complain bitterly.

Message: Never mess with bankers.

Prior to the Civil War, the individual states that comprised the United States were the

primary source of power. After the Civil War, the Federal government started to take

control of power from the states and placed them under its umbrella. The bankers,

under the control of the Rothschilds, were gaining the influence for which they had

been scheming.

primary source of power. After the Civil War, the Federal government started to take

control of power from the states and placed them under its umbrella. The bankers,

under the control of the Rothschilds, were gaining the influence for which they had

been scheming.

A few decades later, the Federal Reserve Act of 1913 was [illegally] passed, and control

of this nation’s money supply was now in the banker’s hands. It took 2 more decades

to officially bankrupt the United States and cause the nation to cease printing any of

its own U S Treasury Notes, which were backed by silver and gold, at the time. It was

then that Roosevelt declared a “banking holiday.” The banking system was shut down

for a few days, and when banks reopened, there were then under control of the Federal

Reserve and a few Wall Street banks. [JP Morgan, Goldman Sachs, Chase]

of this nation’s money supply was now in the banker’s hands. It took 2 more decades

to officially bankrupt the United States and cause the nation to cease printing any of

its own U S Treasury Notes, which were backed by silver and gold, at the time. It was

then that Roosevelt declared a “banking holiday.” The banking system was shut down

for a few days, and when banks reopened, there were then under control of the Federal

Reserve and a few Wall Street banks. [JP Morgan, Goldman Sachs, Chase]

For clarity: The Federal Reserve is a privately owned corporation. It is not federal,

there are no reserves, and what it issues are not Notes. The third sentence of this

article states, It is lies, deceit, and debt ruling supreme. Congress is mandated

by Article 1 section 8 clause 5 of the original Constitution “To coin Money, regulate the

Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures;”

there are no reserves, and what it issues are not Notes. The third sentence of this

article states, It is lies, deceit, and debt ruling supreme. Congress is mandated

by Article 1 section 8 clause 5 of the original Constitution “To coin Money, regulate the

Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures;”

Nowhere in the original constitution does it allow for a private corporation to control

and issue this nation’s currency. Here you see the power of the bankers to come in and

take control of the policies, laws, and banking functions. The government, as most

people believe exists, in fact does not. The government is under total control of the

central banking system, the Federal Reserve.

and issue this nation’s currency. Here you see the power of the bankers to come in and

take control of the policies, laws, and banking functions. The government, as most

people believe exists, in fact does not. The government is under total control of the

central banking system, the Federal Reserve.

The Federal Reserve does not issue money. To be clear, the Federal Reserve does

not issue money! It issues debt. Each and every Federal Reserve Note, [FRN] is a debt

instrument. The United States does not issue it own currency. When the US needs

money, it is borrowed from the Federal Reserve, and interest is paid on each and every

dollar and cent issued by that private banking cartel. When a nation no longer issues its

own currency, it is no longer sovereign. Guess who has to pay the interest on the nation’s

debt?

not issue money! It issues debt. Each and every Federal Reserve Note, [FRN] is a debt

instrument. The United States does not issue it own currency. When the US needs

money, it is borrowed from the Federal Reserve, and interest is paid on each and every

dollar and cent issued by that private banking cartel. When a nation no longer issues its

own currency, it is no longer sovereign. Guess who has to pay the interest on the nation’s

debt?

Read Article 14, first sentence of section 4 of the now Federal Constitution:

Section 4. The validity of the public debt of the United States, authorized by law,

including debts incurred for payment of pensions and bounties for services in

suppressing insurrection or rebellion, shall not be questioned.

including debts incurred for payment of pensions and bounties for services in

suppressing insurrection or rebellion, shall not be questioned.

This will come as a surprise to most Americans, but it was the Rothschild faction,

the money controllers, the elites, who had that section written into the federal

constitution. No one is allowed to question the validity of the public debt, no

matter how invalid it may be! Theft had become legalized with the passage of that

Article 14 of the federal constitution.

the money controllers, the elites, who had that section written into the federal

constitution. No one is allowed to question the validity of the public debt, no

matter how invalid it may be! Theft had become legalized with the passage of that

Article 14 of the federal constitution.

It is your debt, Americans, and to make matters worse, you have to pay interest on

every single dollar and cent loaned into circulation. Forget about what happens to

how FRNs are treated once in circulation, their very existence is debt. There is no

money in circulation. This country, the world, has been deceived into believing

that a FRN is a “dollar,” just because the word appears on each debt instrument.

every single dollar and cent loaned into circulation. Forget about what happens to

how FRNs are treated once in circulation, their very existence is debt. There is no

money in circulation. This country, the world, has been deceived into believing

that a FRN is a “dollar,” just because the word appears on each debt instrument.

It was no accident that Roosevelt passed his useless but effective Executive Order

that mandated all “persons” turn in their gold in 1933. In law, a “person” is a

corporation. Unless one worked for the federal government as an officer or was a

corporation, the deceit of the Executive Order was a pure ruse, as is the entire de

facto bankrupt federal government.

that mandated all “persons” turn in their gold in 1933. In law, a “person” is a

corporation. Unless one worked for the federal government as an officer or was a

corporation, the deceit of the Executive Order was a pure ruse, as is the entire de

facto bankrupt federal government.

The reason for it was that the elites wanted to eliminate competition for its fiat

FRN. We cannot say it is backed by nothing, for it is backed by the birth of every

14th Amendment “US citizen,” a status which never existed prior to the elite mandated

passage of the 14th, another ruse to enslave American citizens within their own country

by a handful of elites who controlled the money which controls the government. If

anyone should doubt that, where does the US government turn when it wants money?

To the Fed banking cartel, and that same cartel issues debt that earns them interest.

FRN. We cannot say it is backed by nothing, for it is backed by the birth of every

14th Amendment “US citizen,” a status which never existed prior to the elite mandated

passage of the 14th, another ruse to enslave American citizens within their own country

by a handful of elites who controlled the money which controls the government. If

anyone should doubt that, where does the US government turn when it wants money?

To the Fed banking cartel, and that same cartel issues debt that earns them interest.

[The point of the birth certificate is that it is used as security for loans based on the

premise that each birth will live for so many years, earn money and pay taxes back

to the elites. The bith certificate is a form of security.]

premise that each birth will live for so many years, earn money and pay taxes back

to the elites. The bith certificate is a form of security.]

The debt, by the way, can never be repaid. It is a mathematical impossibility

because the interest owed is never loaned into existance.

because the interest owed is never loaned into existance.

This is a brief overview of how the US government has come to be usurped by a banking

cartel that controls everything: government, media, corporations, food supply, etc, etc,

all because of their control over the money supply in the Western world. We may

continue this theme in another article, for it is incredibly complex and rife with plausible

deniability by [puppet]governments acting at the behest of the totally in control elites.

cartel that controls everything: government, media, corporations, food supply, etc, etc,

all because of their control over the money supply in the Western world. We may

continue this theme in another article, for it is incredibly complex and rife with plausible

deniability by [puppet]governments acting at the behest of the totally in control elites.

Gold and silver are the exact opposite of debt. When you own gold and silver, you own

it outright. It is substance without any third-party obligation[s]. You know by the

unrelenting manipulation of the price for both by the central bankers how desperate

they are to keep it from challenging their grand fiat scheme. Many thought the Ponzi

scheme was unraveling last year, and many still believe fiat will be jettisoned in favor of

gold and silver this year, sooner rather than later. That does not appear to be the case.

it outright. It is substance without any third-party obligation[s]. You know by the

unrelenting manipulation of the price for both by the central bankers how desperate

they are to keep it from challenging their grand fiat scheme. Many thought the Ponzi

scheme was unraveling last year, and many still believe fiat will be jettisoned in favor of

gold and silver this year, sooner rather than later. That does not appear to be the case.

We are adherents of letting the market interaction of price and volume, as found in the

charts, speak loudest and silence a great many “opinions” offered from a variety of

sources.

charts, speak loudest and silence a great many “opinions” offered from a variety of

sources.

The explanation on the monthly chart is a sufficient summation. Gold has been moving

lower the past few months, but guardedly when it would be expected otherwise.

lower the past few months, but guardedly when it would be expected otherwise.

The promise of a strong rally in gold is far less than the luster on the metal itself. We did

not add the no. 3 so referenced. It was to be the wide range lower from the last swing

high in March. To a lesser degree, when compared to silver, the sell-offs have not been

very authoritative, despite the increasingly failing efforts of the central bankers. Within

the confines of an almost year-long TR, [Trading Range], neither side has a pressing

advantage, which says more for buyers holding their own against sellers.

not add the no. 3 so referenced. It was to be the wide range lower from the last swing

high in March. To a lesser degree, when compared to silver, the sell-offs have not been

very authoritative, despite the increasingly failing efforts of the central bankers. Within

the confines of an almost year-long TR, [Trading Range], neither side has a pressing

advantage, which says more for buyers holding their own against sellers.

In line with the theme of buyers somewhat containing sellers near recent lows, there is a

degree of support that sellers have to overcome if buyers are to be routed, which seems not

to be a large threat, near term.

degree of support that sellers have to overcome if buyers are to be routed, which seems not

to be a large threat, near term.

Silver has moved lower, relative to gold, and has been kept more suppressed, but without

much to show for the effort of selling agents. The fact that last month was the smallest

range in 7 years is a tell against the inability of sellers to extend the range lower at an area

where they should be able to control buyers. The market activity says otherwise.

much to show for the effort of selling agents. The fact that last month was the smallest

range in 7 years is a tell against the inability of sellers to extend the range lower at an area

where they should be able to control buyers. The market activity says otherwise.

Charts give a pictorial that explains more than words can. Note the relative ease of the last

two rallies, dark bars, and the greater difficulty, especially in time, for price to decline.

This is not to say silver will not go lower in the next week or two, rather that moves to the

downside have not been very convincing.

two rallies, dark bars, and the greater difficulty, especially in time, for price to decline.

This is not to say silver will not go lower in the next week or two, rather that moves to the

downside have not been very convincing.

The daily shows in more detail how sellers are struggling to move price lower. The fact

that the bars overlap so much indicates sellers are being met almost equally by buyers.

Of course, the edge remains with sellers, but any ground gains lower are accomplished

grudgingly.

that the bars overlap so much indicates sellers are being met almost equally by buyers.

Of course, the edge remains with sellers, but any ground gains lower are accomplished

grudgingly.

Overall, while silver has not been able to gain as well as gold over the past several months,

it has been holding its recent lows fairly well. For as long as silver can hold it lows, as it

has, the downside for gold may be equally limited, on a relative basis.

it has been holding its recent lows fairly well. For as long as silver can hold it lows, as it

has, the downside for gold may be equally limited, on a relative basis.

Argentina Reaches Agreement with Paris Club Preventing IMF Austerity

WASHINGTON - May 30 - Argentina reached agreement with the Paris

Club, a 19-member block representing some of the world's wealthiest

countries, to repay nearly $10 billion in debts. The agreement ended a

dispute that dates back to Argentina's 2001 default and ensures that

there will be no International Monetary Fund (IMF) promoted austerity

programs. Further, Argentina has renewed access to capital markets and

strengthened its position within the G20.

"Argentina negotiated an agreement that keeps the IMF out of Argentina," said Eric LeCompte, Executive Director of the religious anti-poverty organization Jubilee USA. "IMF austerity programs have wreaked havoc in both poor and wealthy countries."

"One of the principle problems with Paris Club negotiations is the unwillingness to assign fault to lenders that kept corrupt governments in power that abused their people. We are sending the wrong message to emerging democracies when they are forced to pay for the sins of their oppressors," shared LeCompte, who is also an expert to United Nations working groups on these issues.

"Argentina negotiated an agreement that keeps the IMF out of Argentina," said Eric LeCompte, Executive Director of the religious anti-poverty organization Jubilee USA. "IMF austerity programs have wreaked havoc in both poor and wealthy countries."

According to Spain's El Pais, two-thirds of the debt is rooted in previous Argentine dictatorships and corrupt regimes.

"One of the principle problems with Paris Club negotiations is the unwillingness to assign fault to lenders that kept corrupt governments in power that abused their people. We are sending the wrong message to emerging democracies when they are forced to pay for the sins of their oppressors," shared LeCompte, who is also an expert to United Nations working groups on these issues.

Meanwhile, on May 27th the country filed its final arguments

at the US Supreme Court in its dispute with hold-out creditors NML

Capital and Aurelius Capital. These predatory hedge funds seek more than

$1 billion in debt payments and refuse a deal that nearly 93% of

Argentina's creditors accepted after its default. The high court is

expected to decide in June whether or not to take the case. Because of

the case's impacts on poor populations, global debt restructuring and

poor country access to credit, Jubilee USA filed an amicus curiae brief to the Supreme Court.

###

Subscribe to:

Posts (Atom)