A few days after Christmas, 1.3 million Americans who have been out of work for a significant period of time will see their unemployment

benefits disappear. Democrats had pushed for a renewal of the extended

unemployment benefits that have been available since shortly after the

crash, but as Rep. Tom Cole (R-Oklahoma) put it, “the Republican position all along has been, ‘we need to go back to normal here at some point’.”

Unfortunately, the labor market

isn’t back to normal. There are almost three Americans looking for work

for every full-time position that’s available, a ratio that’s tougher

than it was during the worst days of the 2000 recession, according to

the Economic Policy Institute.

As Evan Soltas points out in an article for Bloomberg News, North Carolina offers us a glimpse of the struggle that the long-term unemployed will face nationwide…

Retired people protest in Lisbon over plans to cut pensions. The

pattern of seizing workers’ retirements by slashing pension benefits or

raiding the funds in order to reduce budget deficits has been seen

across Europe and in the U.S.

In states like Illinois and large cities like Detroit in the U.S., as well as in countries like Greece, Spain, Portugal, the U.K., and elsewhere,

pension agreements have been treated as dispensible contracts in the

wake of the financial crisis that took hold in 2008. Even as wealthy

individuals and corporations remain insulated from higher taxes,

governments have increasingly looked at gutting public worker pensions

as a way to pay off debt or reduce annual deficits.

But in Portugal on Thursday, where the government has imposed

draconian austerity policies in order to please the “Troika”—the

European Union, International Monetary Fund and European Central Bank—a

court ruled that a new government ploy to cut pension payments to

retired workers would be “illegal” as it would threaten the “principle

of trust” on which such agreements are based.

As Euronewsreports:

Demonstrations appears to have paid off in Portugal,

where the constitutional court ruled unanimously that one of the

government’s key austerity policies was illegal.

The government had planned to slash public sector pensions over 600

euros a month by 10%, but the court ruled that would constitute a

“violation of trust”.

The decision represents a significant reverse for the centre-right

government’s 2014 austerity budget. It would have saved some 388 million

euros, or nearly 10% of the 3.9 billion euro public spending cuts the

government wants to introduce.

Other ways of making savings must now be sought, with the government warning it may have no alternative but to raise taxes.

However the troika helping Portugal reduce its debt note that rises

would threaten economic recovery. One of the current governments

coalition partners, the Conservatives, have already ruled out any such

hike.

________________________________

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 License.

Source: Common Dreams

The first weapon Federal Reserve Chairman Ben S. Bernanke deployed against the worst recession since World War II owes a singular debt to Paul M. Warburg, a banker in the 1900s who understood money markets more than any contributor to the Federal Reserve Act.

When President Woodrow Wilson signed the act on Dec. 23, 1913, its central purpose was to serve as a backstop to a financial system that had lurched

from one crisis to the next in the preceding decades. The concept of

backstop lending came from Warburg, a native of Germany whose writings

reveal concern that he never got appropriate credit for his role.

Nearly 100 years later, his ideas

were vindicated when Bernanke used the so-called discount window on

Oct. 29, 2008, to provide banks with $111 billion in loans as short-term

credit markets nearly froze in the wake of the Sept. 15 bankruptcy of

Lehman Brothers Holdings Inc. The Fed chairman also used emergency

powers to support money markets, which Warburg had flagged as critical

to financial-system liquidity.

Warburg “is the father of the discount window in the United States” and “the grandfather of the Federal Reserve,” said Michael Bordo, director of the Center for Monetary and Financial History

at Rutgers University in New Brunswick, New Jersey. If his “plan had

been followed, the Fed would have done a lot better in the 1920s, and

the Great Depression might not have been so bad.” Source: Library of Congress via Bloomberg

The concept of backstop lending came from Paul M. Warburg, one of the first Fed... Read More

Unusual Choice

Warburg, who served

from 1914 to 1918 as one of the first Fed governors and the second vice

chairman, was an unusual political choice for a foundational seat on

America’s new central bank. He was an investment banker at Kuhn, Loeb

& Co. when Congress was suspicious of financial power. He disliked

the decentralized scheme the American political system devised for the

Fed and fought to consolidate it. At the heart of his concern was the

need for a centralized money market the Fed would support if a panic

erupted.

The U.S. was still on a gold standard, and Warburg saw

that one way to create flexibility in such a rigid currency system was

for banks to be able to discount, or sell, short-term liabilities in

exchange for money. Today, they routinely fund themselves with

short-term commercial paper and repurchase agreements that allow them to

use securities as collateral for short-term loans.

In the

course of daily business, the central bank wouldn’t be an active player,

simply a buyer of last resort if a bank couldn’t secure funding. The

cost of direct loans from the Fed would be the discount rate, which banks would pay to access the discount window. Source: Library of Congress via Bloomberg

The Federal Reserve Board stands with bankers in 1914. Paul M. Warburg stands in the... Read More

Warburg ‘Aghast’

During a January 1913 hearing on

banking and currency reform before a House subcommittee, Warburg told

its chairman, Carter Glass -- who guided the Federal Reserve Act into law -- that he was “aghast” at the conditions of U.S. money markets when he arrived in America.

“I

saw money rates of 25 and 30 percent,” he told Glass. “There was then

one of those discussions going on, as they have been going on ever

since, as to what to do.”

Later in the hearing, he said he knew exactly what action should be taken.

“Neither the banks nor the central reserve itself would be safe without the introduction of commercial

or banking paper as a means of exchange,” Warburg said. “The key, if

you please, to the vaults of the central reserve is furnished” by

short-term debts that banks could turn quickly into cash.

Opposed Ideas

Wilson

and Glass opposed some of his ideas, with Glass even criticizing the

notion that Warburg contributed anything to the act.

“Warburg did not draft a sentence of the bill,” Glass wrote to his life-long friend Robert Latham Owen in a letter that was found in an archive of Glass’s papers at the University of Virginia’s Albert and Shirley Small Special Collections Library. Owen sponsored the act in the Senate.

Still,

both Wilson and Glass insisted Warburg serve on and help navigate the

central bank in its formative years. His expertise was broadly

recognized at the time, even among the general public.

“Such appointments as yours and your colleagues must tend to restore confidence toward establishing the new financial system,” F.W. Kelsey, head of a Manhattan nursery company, wrote Warburg in a May 8 letter found in the Paul Moritz Warburg papers, manuscripts and archives of the Yale University Library in New Haven, Connecticut.

‘Highest Standing’

Marcus

Marks, Manhattan borough president, called Warburg “the best equipped

man in the country to take on the duties of this position” in a May 5

letter. William Sproule, president of the Southern Pacific Railroad, wrote on May 6 he had a “sense of refreshment” that “a professional banker of the highest standing” accepted the job.

After

graduating from school in Hamburg at 18, Warburg began apprenticeships

in various financial houses, including the British investment bank

Samuel Montagu & Co. and his great-grandfather’s firm, M.M. Warburg & Co., founded in 1798. He came to the U.S. in 1902, following his marriage to Nina Loeb, daughter of the founder of Kuhn Loeb.

Warburg’s European experience in import-export financing and commercial trade in the money markets would define his approach

to central banking. In his view, the financial system needed a

centralized, secondary money market where banks could immediately raise

funds by taking commercial paper and trade credits, known as bankers

acceptances, and selling them. He called them “quick assets,” a term

that reflected his sense of securities almost as fungible as cash

itself.

Critical Lesson

A century later, Gary Gorton,

a professor of management and finance at the Yale School of Management,

wrote that one of the critical lessons from the 2008 financial turmoil

was that short-term debt can serve as a form of private money.

“An

important misunderstanding revealed by the crisis is that regulators

and economists did not know what firms were banks or what debt was

‘money,’” he said in his 2012 book “Misunderstanding Financial Crises:

Why We Don’t See Them Coming.” “They thought that banks were only the

firms that had bank charters and that money was only in currency and

demand deposits.”

As Gorton points out, investors can write

checks against their money-market mutual funds, which hold commercial

paper, as easily as they can against cash deposits in their bank

accounts. The financial crisis was mainly a modern-day run on these

forms of money as confidence in the firms or assets that sponsored them

eroded, which is what caused Bernanke to support these markets with

emergency facilities.

Fed Roots

The central bank “has

rediscovered its roots, in the sense that the Fed was created to

stabilize the financial system in times of panic,” Bernanke said at a

Dec. 18 press conference explaining the contributions of his

chairmanship, which ends Jan. 31. “And we did that, and we used tools

that were analogous in spirit to what the central banks have done for

many hundreds of years, but of course adapted to a modern financial

system.”

Warburg’s papers at Yale show tireless effort to start

the market for bankers acceptances, which were more secure than

commercial paper because they were backed by a bank that had “accepted”

or put its name on the short-term credit, enhancing its appeal in

secondary markets.

He spent hours refining regulations, drafts in his notes show, and scolded Benjamin Strong, the first head of the Federal Reserve Bank of New York, for not being more excited about the market.

“Do

not get into the most discouraging and disappointing attitude of saying

that no business can be done by the Federal Reserve Banks when, as a

matter of fact, I know it can be done, and if I were in charge in New

York, I know I could buy millions of bank acceptances,” Warburg wrote to

Strong on Feb. 17, 1915.

Unmistakable Fingerprint

However

much Glass, Owen and others might have tried to minimize Warburg’s

contribution to the act, the original document bears his unmistakable

fingerprint in the preamble.

In addition to establishing regional reserve banks and furnishing an elastic currency, the third directive reads: “to afford means of rediscounting commercial paper.”

In his 1930 memoir, Warburg called Glass and others who took credit for the act “pleaders in their own cause.”

“The

Reserve System is the product of the labors of many minds,” Warburg

wrote. The development of America’s central bank “must be looked upon as

a national monument, like the old cathedrals of Europe, which were the

work of many generations and of many masters and are treasured as

symbols of national achievement.”

Europe has betrayed Ireland over commitments to ease the cost of saving banks, opposition politicians have claimed.

The allegation was levelled after European Commission chief Jose

Manuel Barroso claimed that Ireland was the cause of the euro crisis,

not the victim.

The outspoken remarks just days after the bailout loan programme

ended have done real damage to claims from the Government that a legacy

bank debt deal is a long-term target.

The top official in Brussels also said that the proposed banking

union across Europe is to protect against future losses in finance

houses and not past.

Michael McGrath, Fianna Fail finance Spokesperson said his damaging

remarks were a betrayal of previous commitments made by EU leaders that

the Irish debt crisis would be treated as a "special case".

"President Barroso's blunt comments about Ireland are not open to misinterpretation," he said.

Source and full story: Irish Independent, 20 December 2013

In this MUST WATCH clip, Bloomberg Industry’s Kenneth Hoffman shockingly reveals that London’s gold vaults are “virtually empty“: “You could go into a vault in

London a couple of years ago. The vaults were packed to the rafters with

gold, and the gold would trade from me to you to somebody else. You can walk into those vaults today and they are virtually empty.

All that gold (26 million ounces) has been transferred from London and

has gone to Switzerland where it has been recast to higher grade formats

and shipped off to Hong Kong and then to China never to return.” Hoffman discusses What’s Happening to All the Gold? openly on financial MSM below:

Fed Chairman Ben Bernanke announced Wednesday that the Federal

Reserve would begin tapering its $85 billion monthly bond-buying program

in January.

The $10 billion dollar monthly cut to the Fed’s purchases of

Treasuries and mortgage-backed securities comes amid a series of

positive economic indicators including a falling unemployment rate,

higher GDP and improving housing numbers.

Bernanke stated that he expected further tapering at future meetings and hinted that interest rates would not rise before 2015.

Markets reacted to the news by jumping to record highs, which may seem counterintuitive to some.

“We didn’t get a pure tapering, we got two messages: one is they’re

going to begin tapering in modest amounts and the other was that they’ve

made it very clear that they’re not going to raise interest rates for a

very long time,” says Jim Rickards, senior managing partner at Tangent

Capital. “What the Fed is saying is ‘Don’t worry we’ve got your back,

you can borrow money for as long as you want,’ and that’s what the stock

market wanted.” http://finance.yahoo.com/blogs/daily-ticker/fed-to-wall-street–don-t-worry–we-ve-got-your-back-151902965.html

About 30 percent of the major global cereal crops – rice, wheat and corn

– may have reached their maximum possible yields in farmers' fields,

according to University of Nebraska-Lincoln research published this week

in Nature Communications. These findings raise concerns about efforts

to increase food production to meet growing global populations.

Yields of these crops have recently decreased or plateaued. Future

projections that would ensure global food security are typically based

on a constant increase in yield, a trend that this research now suggests

may not be possible.

Estimates of future global food production and its ability to meet the

dietary needs of a population expected to grow from 7 billion to 9

billion by 2050 have been based largely on projections of historical

trends. Past trends have, however, been dominated by the rapid adoption

of new technologies – some of which were one-time innovations – which

allowed for an increase in crop production.

As a result, projections of future yields have been

optimistic – perhaps too much so, indicates the findings of UNL

scientists Kenneth Cassman and Patricio Grassini, of the agronomy and

horticulture department, and Kent Eskridge of the statistics department.

They studied past yield trends in countries with greatest cereal

production and provide evidence against a projected scenario of

continued linear crop yield increase. Their data suggest that the rate

of yield gain has recently decreased or stopped for one or more of the

major cereals in many of the most intensively cropped areas of the

world, including eastern Asia, Europe and the United States.

The Institute of Agriculture and Natural Resources scientists calculate

that this decrease or stagnation in yield gain affects 33 percent of

major rice-producing countries and 27 percent of major wheat-producing

countries.

In China, for example, the increase in crop yields in wheat has remained

constant, and rate of corn yield increase has decreased by 64 percent

for the period 2010-2011 relative to the years 2002-2003 despite a large

increase in investment in agricultural research and development,

education and infrastructure for both crops. This suggests that return

on these investments is steadily declining in terms of impact on raising

crop yields.

The authors report that sustaining further yield gain likely would

require fine tuning of many different factors in the production of

crops. But this is often difficult to achieve in farmers' fields and the

associated marginal costs, labour requirements, risks and environmental

impacts may outweigh the benefits.

One of my favorite web spaces is meetinnovators.com.

It interviews startup entrepreneurs, people who created something new

and made it successful. Through casual conversation, it investigates

their thinking, mode of working, trials and tribulations, breakthroughs,

and visions of the future. Just hearing these people talk gives you a

real lift.

Major media don't usually cover this world, which is strange because the

technologies we use and the businesses we trade with define a major

part of our lives. The trouble is that most people just take it all for

granted.

"Of course there's an upgrade." "Of course there's an app." "Of course I

can make a video call from a wireless device to a person on the other

side of the world for free!"

I recently caught up with an old history professor, and it would have

made sense to talk about big ideas (about which we both really care).

But actually, and very quickly, we gravitated to more interesting stuff.

We talked about technologies: operating systems, smartphones, cloud vs.

local software, servers and databases, tablets and laptops, moving on

to social networks, email clients, download sites, and, of course,

games!

This prattle had us engaged for an entire hour, and

then I had to leave. I wonder if it occurred to this man, whom I recall

as ideologically uninterested in economics, much less free enterprise,

that all the stuff we talked about are benevolent gifts to us resulting

from capitalist acts?

People love talking technology these days. And we should similarly love

the world of commerce for giving technology to us through

entrepreneurial drive and innovation. It does so much to better our

lives. Commerce is ultimately responsible for the dramatic increases in

global living standards since the world opened up after 1989.

Startup entrepreneurs deserve much of that credit. They are not only the

creators of new products and services, things that improve our lives at

the margin every day. They are also the major driving force of new jobs

in a market environment that is otherwise rather stagnant.

Comparing startup culture to politics is a study of opposites. In

politics, people promise things ("Healthcare for everyone!" "A world

without immorality!") and just hope that constituents will believe that

pulling a lever will bring change. It never happens, but it doesn't

matter, because there is no real test, no real accountability. Politics

lives on tricks coming and going.

In enterprise, you have this test—both an inspiring North Star and a

wicked crucible. It's called profit and loss. Every day a business must

face that test. To make it, you need to persuade people that you have

something or can do something sufficiently valuable for your customer to

surrender real property in exchange for your product. You must get more

back in property than you surrender to make whatever you're selling.

One dollar over costs and you are growing. One dollar under costs and

you are sinking. The balance sheet rules the day and determines winners

and losers.

Politicians and bureaucrats never face such a reality check. In this

sense, they are completely unhinged from reality. Their revenue is

ensured, and their jobs are based not on sales but manipulation and

position.

Listening to all these interviews with techy entrepreneurs, I'm reminded

of a series of books I read a few years ago about Gilded Age

entrepreneurs. It was a different time and they had different tools—and

they had far fewer struggles with government than we have today—but the

motivations, methods, and impulses are the same.

Here is a list of 10 features of enterprise that entrepreneurs exhibit or discover in the course of their great adventures.

1. Business starts with the desire to do something wonderful, not just to make money.

This seems to be a universal trait. But it flies in the face of nearly

all propaganda you hear about capitalism, which is supposed to be based

on greed and material acquisition. Actually it is rooted in the desire

to make the world a better place, and you can tell it in the voices of

these achievers. Profits are the sign and the seal of a job well done,

but not the driving motivation. The dream is what entrepreneurs chase.

2. Most people will tell you a million reasons why you will fail.

Before jumping in to make a business, these people will typically

survey their friends. Their friends always warn against it. No one will

want that product. Someone already offers that product. That's way too

risky and it won't work. Why not get a regular job like everyone else?

Finally, the person realizes that he or she has to go it alone.

3. All businesses face the universal terror of uncertainty of the future.

The only certainty we have is in looking back at history, at the stuff

that already unfolded. What tomorrow will bring is guesswork. You can

get close. You can make forecasts. But in the end, humanity is fickle

and unpredictable.

And by the way, every single business faces the same ghastly reality of

uncertainty. They are all rock climbing with blindfolds on, feeling

their way up as they go.

4. You can't really know the market until you test the market. Of

course you do market surveys. You ask friends. You look for other

examples of success. You follow your own instincts. But surveys,

examples, and instincts can't substitute for the live test in which you

are asking people to give up their stuff for your stuff. Every success

seems like a no-brainer in retrospect ("Of course people want to buy

books online"), but this is wholly illusory. You never really know until

you try.

5. All entrepreneurs are maniacally focused on serving others.

This also contradicts the conventional wisdom that business is mainly

self-interested. That cannot be true because the whole impetus of

business is to seek out the interests, desires, and motivations of

others. It's the only way to discern the path to success. The consumer

is king, and the entrepreneur serves.

6. Every business needs dreamers and accountants. The dreamers

are the people who imagine a future that doesn't yet exist, a

configuration of the world that is different from today. They take

nothing and make something of it. That requires a wild imagination.

But more is needed to make any project work. Your balance sheet, along

with someone who can skillfully manage and interpret it, is essential.

The accountant is always the one with the bad news.

7. Don't try to start from scratch. One of many benevolent gifts

of capitalism is that it offers us examples of success. These examples

are publicly available to be studied and understood. The best

entrepreneurs know how to copy success and then improve the model on the

margin, just enough to cause a switch in consumer loyalty or recruit

new consumers. You can't be shy about this. Great business people

"steal" ideas; ideas are part of the commons.

8. No matter how digital the service or product is, success comes only peer-to-peer.

Internet successes do not think of their customers as nodes but as

people who need love and care. Nor are customers cash cows; they are

real people with real needs and must be treated as such. All appeals are

personal appeals. All marketing speaks to individuals.

9. Enterprise is an incredible amount of grueling work. To be an

entrepreneur means to be all in. There is no time off. Nothing takes

priority, especially in the start-up period. You need fanaticism, a

near-maniacal devotion to making sure that all that can go right will go

right. Nothing is assumed, ever. These people know that their odds are

never in their favor. So they must apply themselves as never before.

10. You never finally win. Enterprise is not like a board game

with a beginning and an end. Every day the struggle starts anew. Every

season might be your last. And it gets ever harder because the more you

succeed, the more people will copy you. They let you do the test run,

then copy your methods, tweaking them to enhance efficiency or reduce

costs. There is no "final release" in business—not in any business that

plans to stay alive.

These points are coming home to me now, having been at work on a new

business venture for the past several months. The business is Liberty.Me, a complete social and publishing solution for liberty-minded individuals.

The whole focus is to provide a positive, solutions-based information

and communication service for living a freer life. I see a burning need

here to use every bit of advanced technology to do something wonderful

for a cause I believe in. Yes, I'm sure it will be marvelous. But as a

commercial service, there will be a test. It's both thrilling and

terrifying. An idea is facing the crucible. As someone told me recently,

you will soon be a fool or a genius.

You wonder why prosperity is such a rare feature in the history of the

world? It's because merchantcraft is rarer still, attacked often and

avoided by all but the craziest people in our midst—the entrepreneurs

who dream and work and face the crucible of profit and loss—to bring us

what we love.

If you're interested to learn from the life experiences of a

successful entrepreneur, read Doug Casey's new book, Right on the Money.

In his inimitable, provocative style, the well-known resource

speculator provides opinions, anecdotes, and actionable advice on how to

become wealthy and protect one's assets from the long arm of the

government. Click here to read more.

The unelected central planners at the Federal Reserve have decided that

the time has come to slightly taper the amount of quantitative easing

that it has been doing. On Wednesday, the Fed announced that monthly

purchases of U.S. Treasury bonds will be reduced from $45 billion to $40

billion, and monthly purchases of mortgage-backed securities will be

reduced from $35 billion to $30 billion. When this news came out, it

sent shockwaves through financial markets all over the planet. But the

truth is that not that much has really changed. The Federal Reserve

will still be recklessly creating gigantic mountains of new money out of

thin air and massively intervening in the financial marketplace. It

will just be slightly less than before. However, this very well could

represent a very important psychological turning point for investors.

It is a signal that “the party is starting to end” and that the great

bull market of the past four years is drawing to a close. So what is

all of this going to mean for average Americans? The following are 8

ways that “the taper” is going to affect you and your family…

1. Interest Rates Are Going To Go Up

Following the announcement on Wednesday, the yield on 10 year U.S.

Treasuries went up to 2.89% and even CNBC admitted that the taper is a “bad omen for bonds“.

Thousands of other interest rates in our economy are directly affected

by the 10 year rate, and so if that number climbs above 3 percent and

stays there, that is going to be a sign that a significant slowdown of

economic activity is ahead. 2. Home Sales Are Likely Going To Go Down

Mortgage rates are heavily influenced by the yield on 10 year U.S.

Treasuries. Because the yield on 10 year U.S. Treasuries is now

substantially higher than it was earlier this year, mortgage rates have

also gone up. That is one of the reasons why the number of mortgage

applications just hit a new 13 year low.

And now if rates go even higher that is going to tighten things up even

more. If your job is related to the housing industry in any way, you

should be extremely concerned about what is coming in 2014. 3. Your Stocks Are Going To Go Down

Yes, I know that stocks skyrocketed today. The Dow closed at a new

all-time record high, and I can’t really provide any rational

explanation for why that happened. When the announcement was originally

made, stocks initially sold off. But then they rebounded in a huge way

and the Dow ended up close to 300 points.

A few months ago, when Fed Chairman Ben Bernanke just hinted that a

taper might be coming soon, stocks fell like a rock. I have a feeling

that the Fed orchestrated things this time around to make sure that the

stock market would have a positive reaction to their news. But of

course I absolutely cannot prove this at all. I hope someday we learn

the truth about what actually happened on Wednesday afternoon. I have a

feeling that there was some direct intervention in the markets shortly

after the announcement was made and then the momentum algorithms took

over from there.

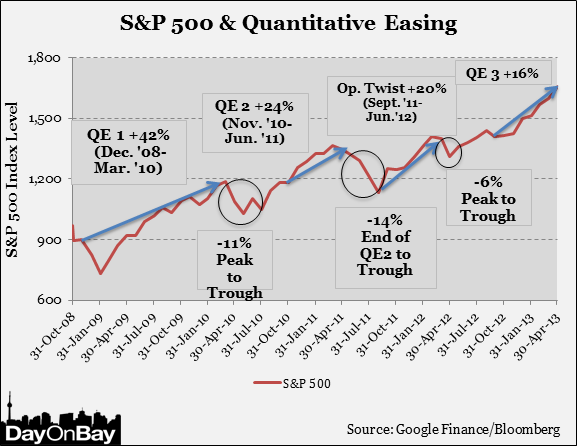

In any event, what we do know is that when QE1 ended stocks fell dramatically and the same thing happened when QE2 ended. If you doubt this, just check out this chart.

Of course QE3 is not being ended, but this tapering sends a signal to

investors that the days of “easy money” are over and that we have

reached the peak of the market.

And if you are at the peak of the market, what is the logical thing to do?

Sell, sell, sell.

But in order to sell, you are going to need to have buyers.

And who is going to want to buy stocks when there is no upside left? 4. The Money In Your Bank Account Is Constantly Being Devalued

When a new dollar is created, the value of each existing dollar that

you hold goes down. And thanks to the Federal Reserve, the pace of

money creation in this country has gone exponential in recent years.

Just check out what has been happening to M1. It has nearly doubled

since the financial crisis of 2008…

The Federal Reserve has been behaving like the Weimar Republic,

and this tapering does not change that very much. Even with this

tapering, the Fed is still going to be creating money out of thin air at

an absolutely insane rate.

And for those that insist that what the Federal Reserve is doing is

“working”, it is important to remember that the crazy money printing

that the Weimar Republic did worked for them for a little while too before ending in complete and utter disaster. 5. Quantitative Easing Has Been Causing The Cost Of Living To Rise

The Federal Reserve insists that we are in a time of “low inflation”,

but anyone that goes to the grocery store or that pays bills on a

regular basis knows what a lie that is. The truth is that if the

inflation rate was still calculated the same way that it was back when

Jimmy Carter was president, the official rate of inflation would be

somewhere between 8 and 10 percent today.

Most of the new money created by quantitative easing has ended up in the hands of the very wealthy,

and it is in the things that the very wealthy buy that we are seeing

the most inflation. As one CNBC article recently stated, we are seeing

absolutely rampant inflation in “stocks and bonds and art and Ferraris and farmland“. 6. Quantitative Easing Did Not Reduce Unemployment And Tapering Won’t Either

The Federal Reserve actually first began engaging in quantitative

easing back in late 2008. As you can see from the chart below, the

percentage of Americans that are actually working is lower today than it

was back then…

The mainstream media continues to insist that quantitative easing was

all about “stimulating the economy” and that it is now okay to cut back

on quantitative easing because “unemployment has gone down”. Hopefully

you can see that what the mainstream media has been telling you has

been a massive lie.

According to the government’s own numbers, the percentage of Americans

with a job has stayed at a remarkably depressed level since the end of

2010. Anyone that tries to tell you that we have had an “employment

recovery” is either very ignorant or is flat out lying to you. 7. The Rest Of The World Is Going To Continue To Lose Faith In Our Financial System

Everyone else around the world has been watching the Federal Reserve

recklessly create hundreds of billions of dollars out of thin air and

use it to monetize staggering amounts of government debt. They have been warning us to stop doing this, but the Fed has been slow to listen.

The greatest damage that quantitative easing has been causing to our

economy does not involve the short-term effects that most people focus

on. Rather, the greatest damage that quantitative easing has been

causing to our economy is the fact that it is destroying worldwide faith

in the U.S. dollar and in U.S. debt.

Right now, far more U.S. dollars are used outside the country than

inside the country. The rest of the world uses U.S. dollars to trade

with one another, and major exporting nations stockpile massive amounts

of our dollars and our debt.

We desperately need the rest of the world to keep playing our game,

because we have become very dependent on getting super cheap exports

from them and we have become very dependent on them lending us trillions

of our own dollars back to us.

If the rest of the world decides to move away from the U.S. dollar

and U.S. debt because of the incredibly reckless behavior of the Federal

Reserve, we are going to be in a massive amount of trouble. Our

current economic prosperity greatly depends upon everyone else using our

dollars as the reserve currency of the world and lending trillions of

dollars back to us at ultra-low interest rates.

And there are signs that this is already starting to happen. In fact, China recently announced that they are going to quit stockpiling more U.S. dollars. This is one of the reasons why the Fed felt forced to do something on Wednesday.

But what the Fed did was not nearly enough. It is still going to be

creating $75 billion out of thin air every single month, and the rest of

the world is going to continue to lose more faith in our system the

longer this continues. 8. The Economy As A Whole Is Going To Continue To Get Even Worse

Despite more than four years of unprecedented money printing by the

Federal Reserve, the overall U.S. economy has continued to decline. If

you doubt this, please see my previous article entitled “37 Reasons Why ‘The Economic Recovery Of 2013′ Is A Giant Lie“.

And no matter what the Fed does now, our decline will continue. The tragic downfall of small cities such as Salisbury, North Carolina are perfect examples of what is happening to our country as a whole…

During the three-year period ending in 2009, Salisbury’s poverty rate

of 16% was about 3% higher than the national rate. In the following

three-year period between 2010 and 2012, the city’s poverty rate was

approaching 30%. Salisbury has traditionally relied heavily on the

manufacturing sector, particularly textiles and fabrics. In recent

decades, however, manufacturing activity has declined significantly and

continues to do so. Between 2010 and 2012, manufacturing jobs in

Salisbury — as a percent of the workforce — shrank from 15.5% to 8.3%.

But the truth is that you don’t have to travel far to see evidence of

our economic demise for yourself. All you have to do is to go down to

the local shopping mall. Sears has experienced sales declines for 27 quarters in a row, and at this point Sears is a dead man walking. The following is from a recent article by Wolf Richter…

The market share of Sears – including K-Mart – has dropped to 2% in

2013 from 2.9% in 2005. Sales have declined for years. The company lost

money in fiscal 2012 and 2013. Unless a miracle happens, and they don’t

happen very often in retail, it will lose a ton in fiscal 2014, ending

in January: for the first three quarters, it’s $1 billion in the hole.

Despite that glorious track record, and no discernible turnaround,

the junk-rated company has had no trouble hoodwinking lenders into

handing it a $1 billion loan that matures in 2018, to pay off an older

loan that would have matured two years earlier.

And J.C. Penney is suffering a similar fate. According to Richter, the company has lost a staggering 1.6 billion dollars over the course of the last year…

Then there’s J.C. Penney. Sales plunged 27% over the last three

years. It lost over $1.6 billion over the last four quarters. It

installed a revolving door for CEOs. It desperately needed to raise

capital; it was bleeding cash, and its suppliers and landlords had

already bitten their fingernails to the quick. So the latest new CEO,

namely its former old CEO Myron Ullman, set out to extract more money

from the system, borrowing $1.75 billion and raising $785 million in a

stock sale at the end of September that became infamous the day he

pulled it off.

So don’t believe the hype.

The economy is getting worse, not better.

Quantitative easing did not “rescue the economy”, but it sure has made our long-term problems a whole lot worse.

And this “tapering” is not a sign of better things to come. Rather,

it is a sign that the bubble of false prosperity that we have been

enjoying for the past few years is beginning to end.

The Pentagon building is the headquarters of the US Department of

Defense, located in Arlington, Virginia and is the symbol of the US

military.

The United States Senate has approved a massive $632.8

billion worth of military spending, including $80.7 billion for the war

in Afghanistan and $17.6 billion for nuclear weapons programs.

The Senate Thursday passed the National Defense Authorization Act,

84-15. The House of Representatives overwhelmingly passed the bill last

week on a strong bipartisan vote.

The spending measure for the 2014 fiscal year will now go to President Barack Obama for his signature.

The House and Senate Armed Services Committees had each passed their

own version of the bill in June. During late November, Republicans and

Democrats on the committees worked out a compromise bill that

incorporated elements of their competing versions.

The bill would authorize everything from overall spending on wars and

military salary to procurement of weapons systems and military-related

foreign policy issues.

It also includes more than 30 provisions aimed at overhauling the

Pentagon’s response to sex crimes, giving greater support to victims and

reforming the military justice code to enable a tougher response to

sexual assaults.

The Pentagon has estimated that 26,000 members of the military may

have been sexually assaulted last year, though thousands were afraid to

come forward for fear of inaction or retaliation.

The huge military budget comes as US lawmakers are considering a

compromise five-year farm bill that would cut the food stamp program by

$8 billion over the next 10 years.

The Supplemental Nutritional Assistance Program provides food stamps for nearly 48 million Americans.

On Wednesday, the Senate gave final passage to a two-year budget plan

that keeps the government funded at over $1 trillion a year through

2015 and avoids potential government shutdowns in January and again in

October.

The budget plan gives sequester relief of $22 billion to the Pentagon

in fiscal 2014 while allowing unemployment benefits for 1.3 million

Americans to expire.

AHT/HJ

I'm drawing it out. The last two years NO COST OF LIVING

WAS EVEN CONSIDERED FOR THOSE THAT NEEDED IT WHILE PRICES WERE CLIMBING EVERY

MONTH - THIS YEAR PRICES HAVE TRIPLED - AND I JUST GOT their NOTICE I'M

GETTIN A $10 INCREASE TO COVER ALL THREE YEARS F*ck the government but especially their total ponzi scheme

that is so ACCURATELY laid out below...

- kirwan

From dickee

I couldn't agree more with this woman...and have felt that way ever since

I began drawing my s.s. checks when I turned 62 - 8 years ago. Entitlement

my ASS! We all DESERVE THAT MONEY THEY MADE US PAY... never giving

us a choice, and now after they have illegally USED our money for their

own benefit (which is ILLEGAL), they have the nerve to tell us it is an

entitlement. BULLSHIT! We deserve to get it back, and should

be getting interest tacked on to it for all they years they held on to

it for their benefit.

Written By A Woman Who Has Her Facts Correct...

AND WHO DIED BEFORE EVER COLLECTING A SOCIAL

SECURITY CHECK!

HOW MANY FOLKS DIED, BEFORE THEY EVER COLLECTED

$1 OF SOCIAL SECURITY THEY PAID IN TO OUR GOVERNMENT?

I don’t know who wrote this, but it is worth

reading before you forward it, or delete it. Food for thought.

KEEP PASSING THIS AROUND UNTIL EVERY ONE HAS

HAD THE OPPORTUNITY TO READ IT... THIS IS SURE SOMETHING TO THINK ABOUT.

THE ONLY THING WRONG WITH THE GOVERNMENT'S CALCULATION

OF AVAILABLE SOCIAL SECURITY IS THEY FORGOT TO FIGURE IN THE PEOPLE WHO

DIED BEFORE THEY EVER COLLECTED A SOCIAL SECURITY CHECK. WHERE DID

THAT MONEY GO?

Remember, not only did you and I contribute to

Social Security but your employer did, too. It totaled 15% of your income

before taxes. If you averaged only $30K over your working life, that's

close to $220,500.

Read that again....

Did you see where the Government paid in one

single penny? We are talking about the money you and your employer put

in a Government bank to insure you and I that we would have a retirement

check from the money we put in, not the Government.

Now they are calling the money we put in an entitlement

when we reach the age to take it back. If you calculate the future invested

value of $4,500 per year (yours & your employer's contribution) at

a simple 5% interest (less than what the govt. pays on the money that

it borrows), after 49 years of working you'd have $892,919.98.

If you took out only 3% per year, you'd receive

$26,787.60 per year and it would last better than 30 years (until you're

95 if you retire at age 65) and that's with no interest paid on that final

amount on deposit! If you bought an annuity and it paid 4% per year, you'd

have a lifetime income of $2,976.40 per month.

Another thing with me.... I have two deceased

husbands who died in their 50's, (one was 51 and the other one was 59

before one percent of their social security could be drawn. I worked all

my life and am drawing 100% on my own social security). Their S.S. money

will never have one cent drawn from what they paid into S.S all their

lives.

THE FOLKS IN WASHINGTON HAVE PULLED OFF A BIGGER

PONZI SCHEME THAN BERNIE MADOFF EVER DID.

Entitlement my foot, I paid cash for my social

security insurance! Just because they borrowed the money for other government

spending, doesn't make my benefits some kind of charity or handout.

Remember Congressional benefits? free healthcare,

outrageous retirement packages, 67 paid holidays, three weeks paid vacation,

unlimited paid sick days. Now that's welfare, and they have the nerve

to call my social security retirement payments entitlements?

We're "broke" and we can't help our own Seniors,

Veterans, Orphans, or Homeless. Yet in the last few months we have provided

aid to Haiti, Chile and Turkey. And now Pakistan...home of bin Laden.

Literally, BILLIONS of DOLLARS.

Our retired seniors living on a 'fixed S.S. income'

receive no additional federal aid nor do they get any financial breaks,

while our government and religious organizations pour hundreds of billions

of $$$ and tons of food to foreign countries.

They call Social Security and Medicare an entitlement

even though most of us have been paying for it all our working lives,

and now, when it's time for us to collect, the government is running out

of money. Why did the government borrow from it in the first place? It

was supposed to be in a locked box, not part of the general fund.

Sad isn't it? …. 99% of people won't

have the guts to forward this.

IN THIS INTERVIEW with Jason Burack, Rob Kirby, & Andy Hoffman:- Fed tapers* $10 billion (creates $75 billion/mo instead of $85 billion/mo), this is “propaganda.” (0:53)

- No free markets in the U.S., “Everywhere I look I see fraud” (6:35)

- “Quantitative Easing” is market manipulation and a bank bailout in disguise (9:49)

- Does the Fed need a bailout themselves?** Bail-ins in the U.S. soon (12:08)

- Bloomberg reports*** London gold vaults nearly emptied by Chinese

because “[The Chinese] don’t want to have U.S. dollars anymore, they

want to have gold.” (19:48)

Researching economic publications on the first century of the Federal Reserve

System provides a wealth of financial information that attempts to

explain the way the central bank works. Rarely will the academic studies

and official reports address the raw nature of a money creation by a

private banking monopoly. The common practice of disparaging sources

outside government or corporatist business circles, attempts to avoid

addressing, much less confronting the plutocracy that controls the debt

created money system.

One such source list of the ownership of the Federal Reserve, compiled by Thomas D. Schauf appears on The Federal Reserve Scam!

However, before getting to the particulars of the actual families

behind the central banking cabal, it is important to go directly to the

source of the primary chronicler who investigated and exposed the

scheme. The late, Eustace Mullins - Secrets of The Federal Reserve, video reveals the entire sordid background.

Now review 25 Fast Facts About The Federal Reserve You Need To Know, from ETF Daily News that advises investors. The way these items play into the central banking model practiced by all 187 nations

that belong to the IMF, demonstrates that banksters of the most select

rank, are behind continued debt bubbles that are strangling the world.

On the Left Hook site by Dean Henderson, a five part series on the Federal Reserve provides added documentation. Mr. Henderson cites from Part 1 in this series, The Federal Reserve Cartel: The Eight Families,

"They are the Goldman Sachs, Rockefellers, Lehmans and Kuhn Loebs of

New York; the Rothschilds of Paris and London; the Warburgs of Hamburg;

the Lazards of Paris; and the Israel Moses Seifs of Rome."

With

such definitive information available and widely known within financial

circles, why is the public so content to remain in the dark? They live

under the aftermaths of the Federal Reserve is a Cache of Stolen Assets, but resign themselves to the oblivion of lost expectations and the burden of diminished opportunities.

"Think about who really owns the land, the buildings and the

resources in our country. In order to really understand the scope and

extent of the economy, the differential between actual Main Street

enterprise, that feeds, clothes and shelters the population, is

minuscule when compared to the financial assets, both liquid and real

property, that is under the command and control of the central bank."

The political class and the business establishment simply refuse to buck the controllers of the currency. Attempts for a Jackals of Jekyll Island - Federal Reserve Audit,

are pushed aside because any accountability for the Fed would ripple

throughout the entire world fiat paper banking system. "The FED’s grip

on the global moneychangers’ racket is based upon maintaining the U.S.

Federal Reserve funny money, as the reserve currency for the planet. The

value and worth of Treasury Bills and Bonds are on the path to have the

value of.

Reichsbank marks. Recognize the enemy that is destroying the country and world economy."The Cato Institute provides a working paper, Has the Fed Been a Failure?,

that traces the history, avowed mission and actual results of the

Federal Reserve System. This scholarly approach acknowledges that other

financial frameworks are "relatively easy to identify viable

alternatives to the adoption of the Federal Reserve Act in 1913."

"However, recent work suggests that there has been no

substantial overall improvement in the volatility of real output since

the end of World War II compared to before World War I . . . the Fed

cannot be credited with having reduced the frequency of banking panics

or with having wielded its last-resort lending powers responsibly. In

short, the Federal Reserve System, as presently constituted, is no more

worthy of being regarded as the last word in monetary management than

the National Currency System it replaced almost a century ago."

Lastly, the essay, Who Owns The Federal Reserve?,

by Ellen Brown, substantiates that the "Fed is privately owned, and its

shareholders are private banks. In fact, 100% of its shareholders are

private banks. None of its stock is owned by the government." Since

the adoption of a private banking, money creation venture, the dollar

has lost virtually its entire store of value. The currency has lost its

universal acceptance, as multiple alternatives circulate to replace its reserve status.

The Federal Reserve’s First 100 Years: A Dismal Record

by Dan Ferris, identifies the ultimate consequence of the stewardship

under a central bank. "The century prior to the Fed, despite setbacks,

was a century of improvement in the dollar’s value. The century after

it, despite enormous gains in productivity, was a century of rampant

Federal Reserve destruction of the dollar’s value."

This failure

to maintain and preserve the integrity of the dollar is no accident. The

actual purpose of the architects of the Federal Reserve System has

never changed. Consolidate the control of money into a concealed cartel

of banking houses that ultimately decide economic and political policy.

Dispensing

of credit to corporatist projects, owned or run by reliable operatives

of the cabal is the objective. The only beneficiaries are the original

stockholders.

"Under the terms of the Federal Reserve Act,

public stock was only to be sold in the event the sale of stock to

member banks did not raise the minimum of $4 million of initial capital

for each Federal Reserve Bank when they were organized in 1913 (12 USCA 281).

Each Bank was able to raise the necessary amount through member stock

sales, and no public stock was ever sold to the non-bank public."

For

the rest of Americans, the Federal Reserve conspiracy is an ongoing

theft syndicate. It only takes the will to admit the undeniable. Without

the courage to abolish this usury monster, the next century will

witness the total destruction of the country.

Wang Jing, the Chinese billionaire behind the plan to build a

waterway across Nicaragua to rival the Panama Canal, is on an

international infrastructure binge.

While Ukraine digs itself deeper into political crisis, Beijing

Interoceanic Canal Investment Management (BICIM) has been quietly

getting on with business.

The Wang-controlled BICIM has agreed to invest US$10 billion in the

construction of a port and economic zone in Sevastopol, Ukraine’s second

largest port.

Wang and newly embattled Ukrainian president Viktor Yanukovych met

vice-premier Ma Kai in Beijing last week after which he explained to

reporters that the first US$3 billion phase of the project would include

an economic development zone with high-tech logistics and industrial

parks.

Phase two will need another US$7 billion for the construction of a

refinery, liquefied natural gas production plant, an airport and a

shipyard. Partnering with BICIM in the project is a Ukranian company

called Kievgidroinvest.

BICIM is the parent company of HKND Group, an infrastructure

developer that won the concession to build the Nicaragua canal. The

experience it will gain in building the canal appears to be one of the

reasons BICIM was awarded the contract by the Ukrainian government.

The Sevastopol deep water port will improve China’s shipping access

to Europe, cutting thousands of kilometres off the Asia- Europe journey.

BICIM will hold a larger share than its Ukrainian partner but Wang

declined to reveal details of the other investors, only to say that

financial support had been secured.

Wang has also declined to reveal the global investors that he claims

have been secured to pour money into the Nicaragua canal project. So far

the route for the 286-kilometre canal has been fixed.

A legal challenge to stop the project was dismissed by the Nicaragua

Supreme Court yesterday after it found the canal construction would not

violate the country’s constitution. Work is scheduled to begin by the

end of next year and take six years to complete

However, Wang said the investment required for the project has been

increased from US$10 billion to US$50 billion, which should be raising

red flags among investors. Infrastructure budgets often need to be

revised upwards, although 500 percent is a bit rude.

But then it’s close enough for government work.

One of the cards read, "Keep Calm, It's Christmas", and the other

"Don't Panic, Christmas Is Not Banned".

CAIRO – In a gesture of goodwill, a leading

British Muslim organization has released Christmas cards, congratulating

the public on the festive season and assuring them that Muslims do not

want to ban Christmas.

"Who wants to ban Christmas? Not Muslims," the Muslim Council of Britain said on its website.

"So put up the Christmas tree, prepare the roast, wrap the presents and spread the Yuletide joy.

"None

of us will be offended if you go ahead and enjoy the Christmas cheer.

We'll remember too the blessings Jesus gave to all of us. He was, after

all, an important Prophet to Muslims.”

Issuing the cards, the MCB wanted to assure public that Muslims would not oppose Christmas Celebrations.

One of the cards read, "Keep Calm, It's Christmas", and the other "Don't Panic, Christmas Is Not Banned".

Moreover, the council added that Muslims, either those celebrating Christmas or no, will not be offended by the season.

"Some Muslims will join in those celebrations, remembering too that Jesus was an important Prophet of Islam.

"Others

will not join. But very few Muslims will be offended at the

celebrations taking place, and no one should be obliged to change their

celebrations at risk of offending Muslims.

"So whether you are celebrating Christmas or not, may these holidays bring joy and happiness to you and your loved ones."

Britain is home to a sizable Muslim minority of nearly 2.7 million.

Christmas

is the main festival on the Christian calendar. Its celebrations reach

its peak at 12:00 PM on December 24 of every year.

Muslims believe

in Jesus as one of the great Prophets of God and that he is the son of

Mary but not the Son of God. He was conceived and born miraculously.

In the Noble Qur’an, Jesus is called "Isa". He is also known as Al-Masih (the Christ) and Ibn Maryam (Son of Mary).

Muslim

scholars assert that Muslims have their own identity and in order to

keep this identity they must not celebrate Christmas or holidays of

non-Muslims.

By participation in Christmas, they say, it is

possible that slowly one may lose his or her consciousness of this basic

point of difference between Islam and Christianity.

Today gold slid under $1200 per ounce, dropping to a level not seen in

three years. Judging by the price action one would think that gold is

not only overflowing from precious metal vaults everywhere, but can be

found thrown away on the street, where nobody even bothers to pick it

up. One would be wrong. In fact, as Bloomberg's Ken Goldman reports,

"you could walk into a vault in London and they were packed to the

rafter with gold, and the gold would trade from me to you to somebody

else. You could walk into these vaults today and they are virtually

empty. All that gold has been transferred out of London, 26 million

ounces...." To find out where it has gone and why it is never coming

back, watch the clip below (spoiler alert: listen for the line: "the Chinese don't want US dollars anymore, they want gold").

Credit Suisse Group AG (CSGN) defrauded

investors of more than $1 billion by misrepresenting the risks

of its residential mortgage-backed securities, acting New Jersey

Attorney General John J. Hoffman said in an interview.

Hoffman’s office sued Credit Suisse over claims it misled

investors about the risk involved in more than $10 billion in

securities issued in 2006 and 2007, before the housing market

collapsed. The lawsuit follows one by New York Attorney General

Eric Schneiderman, who claimed last year that the bank misled

investors about its review of mortgages underlying securities.

“Credit Suisse was greedy and irresponsible,” Hoffman

said yesterday. “The losses are in excess of $1 billion and

likely in the billions.”

Credit Suisse, the second-biggest Swiss bank, faces other

state and federal investigations that could lead to a

consolidation of claims filed by governments, Hoffman said. The

Zurich-based bank has asked a judge to dismiss the New York

case, and criticized the New Jersey complaint announced

yesterday.

“This complaint is without merit,” Drew Benson, a Credit

Suisse spokesman, said in an e-mail. “It recycles baseless

claims and uses inaccurate and exaggerated figures. We look

forward to presenting our defense in court.”

‘High Risk’

The state claims Credit Suisse Securities (USA) LLC and two

affiliates didn’t disclose that loans didn’t meet underwriting

standards and originators had “poor track records characterized

by alarming levels of defaults and delinquencies.”

Such red flags showed the securities “posed a high risk of

delinquency and default, which could -- and ultimately did --

inflict enormous losses on the investors,” according to the

complaint, filed in state court in Trenton.

The securities were based on pools of mortgages not backed

by Fannie Mae (FNMA) or Freddie Mac, the two government-sponsored

enterprises that provide liquidity to the housing market by

packaging loans into securities. Credit Suisse bought those

loans from originators that failed to conduct proper due

diligence, according to the complaint. Investors received

prospectuses that failed to disclose “rampant abandonment of

underwriting guidelines,” according to the complaint.

Defective Loans

Credit Suisse maintained a “Watch List Committee” to weed

out risky originators, yet still bought their loans, according

to Hoffman’s complaint. The bank made “tens of millions of

dollars in reimbursements” tied to defective loans, he said in

a statement.

Hoffman, whose office sued Standard & Poor’s earlier this

year over how it rated mortgage securities, said almost a dozen

people in his office are working on such cases. He declined to

say what other banks, if any, might be under investigation.

“We’re taking an aggressive, affirmative look and

perspective towards institutions responsible for defrauding

investors,” he said. “To the degree that involves additional

lawsuits, that’s the direction we’re heading in.”

Hoffman is part of the Residential Mortgage-Backed

Securities Working Group, which has pulled together the U.S.

Justice Department and state attorneys general to bring cases.

In October, JPMorgan Chase & Co. (JPM) agreed to pay $13 billion over

mortgage-related malfeasance.

Additional Suits

The group approach is shaping litigation, and could affect

how New Jersey pursues the Credit Suisse case, Hoffman said.

“Given that there are other state and federal entities

investigating, and New York has already brought suit, there’s

likely to be coordination in identifying the reach of the

complaint,” he said. “If additional suits are filed, I’m sure

there will be some coordination in how to make restitution.”

Hoffman said he has worked well with Schneiderman in

discussing substantive and procedural matters over Credit

Suisse.

“We have similar claims and interests and end goals,”

Hoffman said. “We have slightly different complaints because

two different groups looking at this independently will have a

different perspective. But our purposes are aligned.”

Such alignment extends to the other investigators, he said.

“In many respects our conversations with General

Schneiderman are also with the working group,” he said.

Hoffman declined to say what other companies might be in

his cross hairs.

The Credit Suisse case, he said, isn’t just about money.

“In the context of resolving this case, we’ll try to

institute remedial measures so that there will be greater

accountability and transparency,” he said. “It’s not just

about money. It’s about this not happening again.”

Hoffman was appointed by Governor Chris Christie, a

Republican, in June. He previously served as executive assistant

attorney general under his predecessor, Jeffrey Chiesa, who

stepped down to serve as a U.S. senator.

Hoffman also worked for six years as a federal prosecutor

in New Jersey and for eight years as a trial attorney in the

Justice Department’s civil division.

The case is Hoffman v. Credit Suisse, Superior Court of New

Jersey, Mercer County (Trenton.)

WASHINGTON, Dec. 19 (UPI) -- First-time

unemployment benefits claims rose by 10,000 to 379,000 in the week

ending Saturday, the Bureau of Labor Statistics said Thursday.The

department also revised the previous week's jump in claims from 368,000

to 369,000, which puts the two week total at 79,000 fresh claims for

benefits.

The four-week rolling average of first-time unemployment benefits claims rose by 13,250 to 343,500.

The

largest increases in initial claims for the week ending December 7 were

in California with a gain of 12,876, New York with 14,322 additional

claims and Pennsylvania with 14,004.

The largest decreases were in Ohio, Kentucky and Vermont with declines of 1,095, 838 and 400, respectively.

If Reid really cared about poor people and a dwindling middle class, he would help us get rid of the Federal Reserve Kurt Nimmo

If Reid and the Democrats really cared about poor people and a dwindling middle class, they would get rid of the Federal Reserve.

Senate Majority Leader, Nevada Democrat Harry Reid, wants the government to steal more money from the middle class and dole it out the victims of the Federal Reserve created economic depression.

“Even as the economy creates jobs, too many Americans find themselves

on the sidelines watching as the rich get richer, the poor get poorer

and the middle class are getting squeezed and squeezed,” Reid said on

Thursday.

“There is no greater challenge this country has than income inequality. And we must do something about it.”

Reid’s solution to income inequality is to tax and borrow more and

give money to the unemployed. Democrats like to tell you this money will

come from the super rich. But they know the super rich don’t pay taxes.

From offshore tax havens to shell games, foundations and equity swaps,

the rich rarely if ever pay taxes. Large multinational corporations with

teams of lawyers don’t pay taxes either. GE, for instance, avoided

paying taxes by socking $108 billion overseas.

So when Harry Reid talks about redistributing more money to the

unemployed, he’s talking about taxing the middle class. He’s also

talking about taxing the small businessman who can’t afford fancy tax

lawyers and does not have the option to move money to the Cayman Islands

or Lichtenstein.

According to recent Small Business Administration and the Bureau of Labor Statistics

figures, around 85 percent of all new jobs are created by small

business. If Harry Reid and the Democrats raise taxes on small business,

the net result will be less capital for business and less jobs created.

Higher taxation leads to business cutting expenditures and laying off

people. Harry Reid and the Democrats will create even more unemployment

and misery.

There is, however, an upside to Reid’s demand, at least for Democrat

career politicians. It will create more Democrat voters. Many of them

will not have jobs. But they will vote for Democrats in order to

continue receiving unemployment insurance and food stamps. Amnesty is

basically the same thing. It will create millions of new Democrat

voters.

If Reid and the Democrats really cared about poor people and a dwindling middle class, they would get rid of the Federal Reserve,

throw out the bankers who designed the last so-called recession, and

restore honest money instead of fiat currency based on nothing and

exploited by fractional reserve criminals.

Corporatists and banksters

controlling government and the money supply is the problem. Harry Reid

knows this. His top election donors include JP Morgan Chase, AT&T,

MGM, Comcast and big gambling casinos.

That’s who he answers to. Not the American people.

With permission

Source: Infowars

Published on Dec 19, 2013100 years ago, this December, the United States

Congress created a central bank today, we know it as the Federal Reserve

Bank of the United States. What most people don’t know is that the bank

isn’t a federal entity and candidly, it really has nothing in reserves.

Is the Federal Reserve good for the United States? Is it even possible to get rid of it?

The first step toward truth is to be informed.

US lawmakers are considering a compromise five-year farm bill

that would cut the food stamp program by $8 billion over the next 10

years.

Senator Tom Harkin (D-Iowa) told Reuters on Thursday that changing

eligibility rules and disqualifying up to 4 million Americans who depend

on food stamps would also help the US government save $40 billion over a

decade.

As part of the new US farm bill, the Republican-controlled House of

Representatives proposed to cut nearly $40 billion from nutrition

programs, the largest cuts in a generation. However, the

Democratic-controlled Senate voted to reduce food-stamp funding by $4.5

billion.

Food stamp benefits are the most politically contentious component of the first US farm bill since 2008.

œFrom everything I’ve seen, we are now within a few items of having

this agreed to,” said Harkin who is a member of the select committee

responsible for reconciling the bills passed by the two chambers of the

US Congress.

Activists want to know whether the select committee has agreed to

change eligibility rules in exchange for the relatively small cuts.

Last year, US lawmakers failed to pass a new farm bill and approved a

one-year extension of the 2008 bill which expired in September.

If lawmakers on Capitol Hill fail to bring a new bill to the floor in

January, Scott Faber of the Environmental Working Group said, Americans

will œbe looking at a two-year extension” of the now-expired 2008 law.

The Supplemental Nutritional Assistance Program provides food stamps for nearly 48 million Americans.

ISH/ISH

With permission

Source: Press TV

Today, the Obama administration announced that people whose insurance

plans were canceled this year will "temporarily" be exempted from the

law's individual mandate. Here's how they're doing it -- and what it means for the law.

HHS

Secretary Kathleen Sebelius jyst delayed the individual mandate for

people whose plans have been canceled. (Photo by J. Scott Applewhite/AP)

1. The individual mandate includes a "hardship exemption." People who

qualify can either ignore the individual mandate altogether or purchase

a cheap, bare-bones catastrophic insurance plan that's typically only

available to people under 30.

2. According to HHS,

the exemption covers people who "experienced financial or domestic

circumstances, including an unexpected natural or human-caused event,

such that he or she had a significant, unexpected increase in

essential expenses that prevented him or her from obtaining coverage

under a qualified health plan."

3. Today, the administration agreed with a group of senators, led by

Mark Warner of Virginia, who argued that having your insurance plan

canceled counted as "an unexpected natural or human-caused event." For

these people, in other words, Obamacare itself is the hardship. You can

read HHS Secretary Kathleen Sebelius' full letter here. HHS's formal guidance is here.

4. How may people does this affect? No one quite knows. Republicans

estimate that about 5 million people have seen their plans canceled. The

Obama administration believes the number, at this point, is actually in

the hundreds of thousands. There's no truly reliable figure here.

5. The Obama administration argues that there's little reason to fear

that these people won't purchase health insurance if they could

otherwise afford to. After all, they were already buying health

insurance on the individual market before there was any penalty at all.

They clearly want health insurance. This just smooths their transition

and, in the cases where there really is financial strain, gives them

time to figure out a solution.

6. But this puts the administration on some very difficult-to-defend

ground. Normally, the individual mandate applies to anyone who can

purchase qualifying insurance for less than 8 percent of their income.

Either that threshold is right or it's wrong. But it's hard to argue

that it's right for the currently uninsured but wrong for people whose

plans were canceled.

7. Put more simply, Republicans will immediately begin calling for

the uninsured to get this same exemption. What will the Obama

administration say in response? Why are people who plans were canceled

more deserving of help than people who couldn't afford a plan in the

first place?

8. The same goes for the cheap catastrophic plans sold to customers

under age 30 in the exchanges. A 45-year-old whose plan just got

canceled can now purchase catastrophic coverage. A 45-year-old who

didn't have insurance at all can't. Why don't people who couldn't afford

a plan in the first place deserve the same kind of help as people whose

plans were canceled?

9. The insurers aren't happy. "This latest rule change could cause

significant instability in the marketplace and lead to further confusion

and disruption for consumers," says Karen Ignani, head of the trade

group America's Health Insurance Plans. They worry the White House is

underestimating the number of people whose plans have been canceled and

who will opt to either remain uninsured or buy catastrophic insurance

rather than more comprehensive coverage.

10. This puts the first crack in the individual mandate. The question

is whether it's the last. If Democratic members of Congress see this as

solving their political problem with people whose plans have been

canceled, it could help them stand against Republican efforts to delay

the individual mandate. But if congressional Democrats use this ruling

as an excuse to delay or otherwise de-fang the individual mandate for

anyone who doesn't want to pay for insurance under Obamacare, then it'll

be a very big problem for the law.

{kind=link}