Our

lead story: This week Stanford said that it would divest all of its

investments in coal-mining companies, becoming the wealthiest US

university to pledge divestment from sectors of the fossil fuel

industry. Erin gives you her take on the situation.

For our interviews today, we

look at peak oil theory with Richard Heinberg and James Hamilton.

Heinberg argues that we have reached peak oil supply and that will have

major economic consequences for our future prospects of economic growth.

Hamilton on the other hand sees this as more of a demand issue. Take a

look.

Finally in today’s Big Deal,

Edward Harrison and Erin take a look at the return of the subprime auto

loan market. Is this another example of perverse incentives in the

search for yield? Edward gives you his take.

It

fits the pattern of gratuitous bank enrichment perfectly, but this

time, the big beneficiaries of the Fed are foreign banks. A JPMorgan

analysis, cited by the Wall

Street Journal,

figured that in 2014 the Fed would pay $6.74 billion in interest to

the banks that park their excess cash at the Fed – half of that

amount, so a cool $3.37 billion, would line the pockets of foreign

banks with branches in the US.

This

is where part of the liquidity ends up that the Fed has been handing

to Wall Street through its bond purchases. Currently, the Fed

requires that

banks keep a minimum balance of $80.2 billion at the Fed. Banks can

keep up to $88.2 billion at the Fed as part of the “penalty-free

band.” In theory, as “penalty-free” implies, there’d be a

penalty on balances above $88.2 billion.

But the total balance was $2.66 trillion in

April, up from $2.62 trillion in March and from $1.83 trillion a year

ago. The balances in excess of the “penalty-free band” have

reached $2.57 trillion. The highest ever. The penalty on that?

Forget

that. The Fed’s raison

d’être is

to enrich the banks regardless of what the costs to the economy, the

rest of society, and savers. So instead of penalizing banks for these

excess reserves, it pays the

banks 0.25% interest not only on the required balances but also on

all other balances. Spread over the year 2014, as JPMorgan estimated,

interest payments on these balances would amount to $6.74 billion.

It’s a marvelous system. The banks’ cost of

funds, given the heroic efforts the Fed has undertaken to repress

interest rates, is near zero. Banks can borrow short-term from their

depositors – that’s you and me – and from money-market funds –

that’s you and me again – at near zero cost, so maybe 0.10%.

Instead of lending it out, banks put that money on deposit at the Fed

to earn 0.25%. It’s the laziest no-brainer in banking history. A

pure gift from the Fed.

But

there’s a kink. Non-US-charted banks with branches in the US

benefit even more. The Bank for International Settlements, the

umbrella organization for the world’s largest central

banks, revealed how

these non-US banks were taking advantage of the new FDIC insurance

charges on wholesale funding (borrowing from other banks, short-term

repos, or funding from affiliates outside the US). They’d figured

out that these extra costs didn’t apply to them. They only applied

to US-chartered banks.

The wider FDIC charge added 2.5 to 45 basis

points to the costs of large and complex US chartered banks’

short-term wholesale funding. The calculation is complex and its

result by bank is not disclosed, but the rate for the largest US bank

was said to be 8 basis points…. With wholesale rates of 10 basis

points or less, the new FDIC charge made bidding for such funds and

parking them at the Fed at 25 basis points unattractive for many

US-chartered banks but not to the US branches of foreign banks, which

pay no FDIC fee.

These “seemingly small regulatory

differences” at the FDIC, the report points out, turned the Fed

into a special profit center for non-US banks. In this chart from the

report, foreign banks’ balances parked at the Fed (blue area in

dollars, and red line in percent) started shooting up at the end of

2008, and by mid-2013, reached about 50%. It resulted in “massive

changes” in the balance sheets of internationally active banks.

As foreign banks took advantage of the laziest

no-brainer in history, the Fed’s money-printing and bond buying

regime led to an enormous inflow of money into the US – about $1.3

trillion so far. It’s the risk-free banking version of the hot

money. And the $2.6 trillion in excess reserves that economists are

expecting to flow into the US economy sooner or later to really stir

things up? Half of it is that hot money. It won’t ever flow into

the US economy. It won’t fuel the “escape velocity” that has

been forecast for five years in a row. It’ll dissipate.

The

Fed has an excuse for

this banking gravy train: “eliminate effectively the implicit tax

that reserve requirements used to impose on depository institutions,”

it said. OK, I get it, concerning the “penalty-free” $80.2

billion that banks are required to deposit at the Fed. Fine. Pay them

0.25% on that. I don’t get paid that much on my money at the bank.

But what the heck. Let’s not quibble over pocket change, which is

what billions have become to the megabanks these days. But what about

the annual interest on $2.6 trillion in excess reserves?

Ah, the Fed has an excuse for that too: it’s

of course – I mean, how could I possibly not think of this on my

own? – “an additional tool for the conduct of monetary policy.”

A policy whose goal it is to fan reckless speculation, inflate asset

bubbles, enrich the banks and those who run them at the expense of

savers, and douse the entire neighborhood, namely Wall Street, with

free money.

Under

this relentless regime, the labor force participation rate has

shriveled to 62.8%. You have to go back to February 1978 to see

worse. It’s a terrible indictment of the Fed’s policies that

favor capital over labor, Wall Street over savers. New Zealand’s

central bank didn’t follow the Fed’s lead in monetary policy. And

there, the labor participation rate just set a new record high.

Read…. Scorched-Earth

Monetary Policy in the US, And What Happened in New Zealand

Dr Jim Willie has been talking about the BRICS

nations (Brazil, Russia, China, India and South Africa) being joined

by other nations to take down the dollar. He says there are

now 80 nations in the BRICS alliance who have joined together to end

the dollar’s reign as the international reserve currency. China

could have taken down the US economy any time it wanted to after it

had accumulated more than a trillion dollars in US Treasury bonds.

All it had to do was to sell them and buy real assets until the US

government collapsed and surrendered.

The Chinese are

playing a much more sophisticated game. Their goal is to take down

the dollar and the British pound but not to hurt their customers in

Africa, Latin America, Australia and elsewhere. He thinks a Northern

euro will emerge leaving southern Europe and France far behind.

Italy’s future was hurt when they mistakenly decided to send half

of their gold to New York. That gold is in Asia along with the

bullion from the Netherlands and Germany.Dr

Willie agrees with Jim Rickards who says the dollar will be devalued

80%. This will make imported goods 500% more

expensive. And it will also enable foreigners to buy food off the

shelves of America and Great Britain. Please note that the British

pound is being targeted by the BRICS 80 as well.

The signs of inflation continue to appear in

the economy.

The Fed is ignoring this because the Fed is

afraid of deflation… despite food prices, energy prices, healthcare

costs, home prices and stocks soaring.

· FedEx is

increasing prices by 42% for some shipments.

· Commonwealth

Edison is raising electricity rates by 38% in June.

· Chipotle is

raising prices for the first time in three years.

· Netflix is

raising prices on new customers.

·

Colgate-Palmolive is raising prices.

These

are simply explicit price increases. Many companies have been raising

prices via a “stealth” price hike by simply charging the same

price for less of

a product. The latest example of this is bacon, but companies such as

Kellogg’s, Snickers, Tropicana, Bounty, Heinz, and others have been

using this tactic for some time.

Against

this backdrop, the Fed is openly stating that it wants to

create inflation. Put another way, the Fed is not only oblivious to

the fact inflation is already appearing in the broader economy, the

Fed actually wants to create more inflation!

Small wonder the US Dollar is teasing with

breaking multi-year support.

In its quest to fight the brief deflation of

2008-2009, the Fed has unleashed a wave of inflation. These

developments take time to unfold. But the signs are already there.

The grand theme for 2014 will see prices moving higher.

This

concludes this article, swing by www.gainspainscapital.com for

several FREE investment reports including Protect

Your Portfolio, & The

Gold Mountain: how to buy Gold at $273 per ounce.

The signs of inflation continue to appear in

the economy.

The Fed is ignoring this because the Fed is

afraid of deflation… despite food prices, energy prices, healthcare

costs, home prices and stocks soaring.

· FedEx is

increasing prices by 42% for some shipments.

· Commonwealth

Edison is raising electricity rates by 38% in June.

· Chipotle is

raising prices for the first time in three years.

· Netflix is

raising prices on new customers.

·

Colgate-Palmolive is raising prices.

These

are simply explicit price increases. Many companies have been raising

prices via a “stealth” price hike by simply charging the same

price for less of

a product. The latest example of this is bacon, but companies such as

Kellogg’s, Snickers, Tropicana, Bounty, Heinz, and others have been

using this tactic for some time.

Against

this backdrop, the Fed is openly stating that it wants to

create inflation. Put another way, the Fed is not only oblivious to

the fact inflation is already appearing in the broader economy, the

Fed actually wants to create more inflation!

Small wonder the US Dollar is teasing with

breaking multi-year support.

In its quest to fight the brief deflation of

2008-2009, the Fed has unleashed a wave of inflation. These

developments take time to unfold. But the signs are already there.

The grand theme for 2014 will see prices moving higher.

This

concludes this article, swing by www.gainspainscapital.com for

several FREE investment reports including Protect

Your Portfolio, & The

Gold Mountain: how to buy Gold at $273 per ounce.

One in four recently separated U.S. veterans may not be able to

consistently put food on their tables, according to a new report

released Wednesday.

The Public Health Nutrition journal study,

titled “Food Insecurity & Iraq/Afghanistan Veterans,” surveyed more

than 900 young veterans and found 27 percent reported problems with

getting enough food for three meals a day. That’s about twice as high as

the overall national rate.

Study author Rachel Widome, a

University of Minnesota health professor, called the findings “shocking

and disheartening.” Investigators launched the study two years ago after

tracking reports about financial hardships among young veterans.

“We

really had no idea how common it was that Iraq and Afghanistan war

veterans were struggling to afford food,” she said. “Given anecdotal

accounts, I thought food insecurity might be somewhat of an issue, but

really had no idea of the extent.”

About 12 percent of the

veterans surveyed were classified as having “very low food security,”

marking severe difficulties in reliably getting meals.

The study

was conducted with the Minneapolis VA Health Care system and featured

only veterans from Minnesota. Authors said the findings indicate serious

challenges for younger veterans and their families.

Widome said

veterans struggling with food problems also reported struggling with

other life stress, including sleep problems, substance abuse and

employment difficulties.

“For those of us who work with Iraq and

Afghanistan war veterans either in health care or social service

settings, it is important to be aware that these veterans may also have

another hidden struggle,” she said.

“We need to work on connecting

veterans in need with food assistance programs, or even better,

assisting them with finding employment that provides a secure livable

wage after deployment.”

Chinese will not be allowed to invest in gold or diamond mining, or

hi-tech projects, Russia hopes to lure cash from the world’s

second-biggest economy into industries from housing and infrastructure

construction to natural resources. Chinese President Xi Jinping and

Russian President Vladimir Putin will meet in Shanghai May 20/21 and

Chinese officials have already confirmed bilateral cooperation

in the areas of investment and finance has made major progress as local

currency settlement in two-way trade increases. Forget sanctions, just remove the US from the world trade equation... As Bloomberg reports,Russian President Vladimir Putin plans to open the door to Chinese money as

U.S. and European sanctions over Ukraine threaten to tip the economy

into recession, according to two senior government officials.

The move would roll back informal limits on Chinese investment

as Russia seeks to stimulate growth, said the officials, who have

direct knowledge of talks and asked not to be identified as the

information isn’t public. The government wants to lure cash from the

world’s second-biggest economy into industries from housing and

infrastructure construction to natural resources, they said.

The Chinese won’t be welcome in all areas: Russia plans to set “red lines” around significant gold, platinum-group metals, diamond mining and high-technology projects, the officials said.

...

Putin’s decision, coming as competition from U.S. and European financing slows, may offer China a good opportunity to gain access to Russia’s economy.

Existing resource projects will probably be more appealing than

starting from scratch, Moscow-based George Buzhenitsa, Deutsche Bank AG

analyst said by phone on May 7.

... “Given that China has a shortage of raw materials from iron

ore to coal to copper, it may be extremely interested in gaining access

to such projects in Russia,” Buzhenitsa said.

And China seems more than willing to step up...

China is ready to join with Russia to increase two-way investment, Chinese Vice Premier Zhang Gaoli said here Thursday.

...

Their talks were focused on bilateral investment and practical

cooperation in the financial area, in preparation for the forthcoming

meeting between the two heads of state. Chinese President Xi Jinping and Russian President Vladimir Putin will meet

when Putin attends the Fourth Summit of the Conference on Interaction

and Confidence Building Measures in Asia (CICA), on May 20 and 21 in

Shanghai. Zhang said bilateral cooperation in the areas of investment

and finance has made major progress. China has increased investment in

Russia and become the country's fourth largest source of foreign direct

investment. He said financial cooperation between China and Russia is

growing as local currency settlement in two-way trade increases and

consultations on a package of currency swaps are on-going.

Zhang expressed the hope that the two sides increase mutual

investment via the China-Russia investment fund and carry out the first

batch of investment projects as planned. He said the two sides should increase investment in the forms

of greenfield investment, equity investment, bond issuance and mergers

and acquisitions.

Zhang asked the Russian side to help Chinese enterprises to invest in special economic zones in the Far East region of Russia.

Who needs sanctions when China is your friend? And it would seem no

matter what card the US tries to play, Putin has a trump (for now).

In an interview with Bloomberg’s Stephanie

Ruhle and Erik Schatzker Athenahealth CEO Jonathan Bush said this

morning on “Market Makers,” he “messed up” when he promised

net income growth and that he feels the reason Einhorn called out

Athenahealth was because he is the ” quintessential value guy.

He likes Apple now that Jobs is dead.” Bush said he wants investors

who “dream of a health-care cloud.”

Bush also said: “I don’t know what we’re

worth. I know we’re worth $1,000 a share at some point in the

future.”

Anchor Stephanie Ruhle concluded the interview

saying “And here we thought David Einhorn was quirky” to which

Bush replied “I am a strange guy, but I’ve found a great thing to

do with my life so I’m just happy.”

**BLOOMBERG

TELEVISION’S “MARKET MAKERS”**

Highlights:

On

promising net income was going to grow:

“I messed up. If I said net income is

going to grow infinitely and then you see this opportunity basically,

the big arbitrage for us is suddenly we’ve got – so we’ve lots

of doctors. Half of our doctors work for hospital companies.

Those hospital companies are saying you must push this network in

through our hospitals. We don’t want the cloud to be

something that happens outside the hospital and then we’re stuck on

Enterprise software inside the hospital. So we said, look, this

is a chance. They’re asking us to serve them. Let’s

double down on R&D. We finally got a good enough reputation

that we can hire as many developers as we want with our standards not

wavering. Let’s do it.”

On

growth targets:

“We believe we need to grow 30 percent a year

– or that we can and we should. To grow more than that,

you’ll have a hard time building out the infrastructure and if you

grow less than that, you might not be able to build the national

network that you’re trying to build, you want to be relevant.

We’ve always said you have to grow the margins of all products to

make them scalable and reliable. It is the natural way of

things in a software enabled service, in a network company, which we

are. So our margins have improved in every product, every

year. But when we add new products, those start at low margins

and then, as we grow them and remove the work, the scut work that is

sort of rotting the walls of health care, the margins go back up

again.”

“You have been to the doctor’s office.

I mean, the clipboard is still there and the phones and faxes.

It’s like that movie, “Brazil,” sort of this weird future where

the Internet never shows up. And finally Athena’s got a

business model that allows us to bring health care onto a secure

sector of the Internet, we call it the health care cloud, in order to

eliminate that kind of scut work.”

On

David Einhorn saying he like Athenahealth and Bush as CEO:

“In the South, that’s when they like bless

your heart.”

On

how he defends his valuation:

“I don’t know what we’re worth.

What I do – I know we’re worth $1,000 a share, no problem, at

some point in the future. And it’s up to David and others to

decide when by discounting back what they think… I pulled [the

valuation] out of my ear. I mean, the point is — what I know,

what David – the only David missed that I can see is that he

doesn’t see what a software enabled service is. So that’s —

we are not a BPO company by any stretch. We are not an

Enterprise software company. We are not even a SAS company.

We’re a company that’s a software enabled service. We give

out our software, Internet native software, to all of our customers

for free. Then we use that software to deliver a series of

complicated services that they hate and stink at. And then,

once we’re doing that, we start to realize this extraordinary

network effect where the margins go up and up and up as we eliminate

paper.”

On

why growth rate didn’t increase when he cared less about margins:

“I can have high gross margins, I just

want to put that money into R&D for new products and sales and

marketing. That income, what’re you going to do, pay 40 percent

taxes to Barack and then stop growing? We’ve got 3 percent of

the doctors; we need them all. We need at least half of them.

I’m shooting for half of the doctors, not 3.5 percent of doctors. ”

On

the Athenahealth network effect:

“So there are today there are 52,000

caregivers — nurse practitioners, doctors, et cetera — who in

their office look at a little iPad or a whatever, a laptop, a

browser, with Athenanet on it. They do all the work. In

the background, all of them are connected to one instance of one

software, one database. Every time any of them get a single

claim denied, any one guy in North Dakota, the Athena analysts in a

room not as sexy but close as this, get to the root cause, build code

that night into the network, and then no doctor ever gets that claim

denied again. So the margin associated with following up and

appealing and dealing with the insurance company turns into a new

level of profit. Similarly, a doctor wants to send a patient to

a laboratory. Athena will build a connection into that

laboratory and then any doctor in the country that ever wants to send

a patient who that laboratory is automatically lit up and connected

like you’ve added a new cable channel. That creates a huge

revenue — margin arbitrage. Because what used to be a Athena

sending a fax and receiving a fax and typing it in becomes an

instantaneous, real-time, all-margin.”

On

whether he thinks Einhorn feels he was made promises that

shareholders are not getting:

“If you ask me, the guy’s a quintessential

value guy. He likes Apple now that Jobs is dead, right, because

all they’re going to do is drive up, drive up, drive up. He’s

not going to be – Steve’s not going to be running around

demanding some crazy new space age product with all of their money,

right? He doesn’t even like Amazon. Look at how Jeff’s

pushing more and more and more into not sure we need drones, but

maybe I’m wrong. Maybe the drones are key to the grocery

business. So, I’m more in that sort of line of thinking, which is

not his. And those who buy our stocks should not be sort of

bottom watching value investors. They should be people who

dream of a health care cloud.”

On

wanting value investors to understand the company:

” I’m looking forward to the cage match

between Einhorn and Morgan Stanley, because they’re the ones who

are doing the bottom up stock pricing. David seems to be doing

well financially, so maybe there’s reasons. All I am saying

is I know that this health care cloud is a really good idea.”

On

Einhorn’s concern about getting inside hospitals:

“So lucky for us, a lot of hospitals, 550

hospitals, are already clients. We just do the doctors they

employ, and they’re saying, hey, finish the job. Move on

through. We just announced Steward Healthcare, which is a

service-backed hospital chain, that’s allowing us to start

performing services toward the in-patient side and we’re going to

roll out a new service called Enterprise Coordinator that moves

through. It’s also worth noting that hospital chains, like

Ascension, which is the largest nonprofit Catholic hospital chain in

the country, has already chosen us for billing and then said to

doctors, hey, you guys — if you want to keep the Enterprise

software that you already have for your medical records, you can, we

won’t make you leave. And six out of seven of the ministries

have switched to Athena Clinicals even though they just have these

new Enterprise software based EMRs. Enterprise software is not

a competitor to Athena; it’s a sort of previous era substitute.

And as the cloud rises up, you throw out your software.”

On

whether he sees Athena partnering with Epic:

“Totally. Run by a great lady and a

great guy. You know, they have to protect business model, which

I think is obsolete, but they do a very good job within the context

of that business model. We’ll work with them all over.”

On

hospitals having a harder time bringing doctors into the fold unless

they are willing to connect with Athena’s software:

“The average hospital today in this buying

spree since Obama was elected is up to $180,000 per doc per year

loss, subsidizing doctors to use the hospital operations and the

hospital systems. That can’t last forever. And even if

it does last for the ones they’ve bought, they’re not going

to be able to go and buy the other half of the doctors, but they’re

going to want patients. So they’re going to need to connect.”

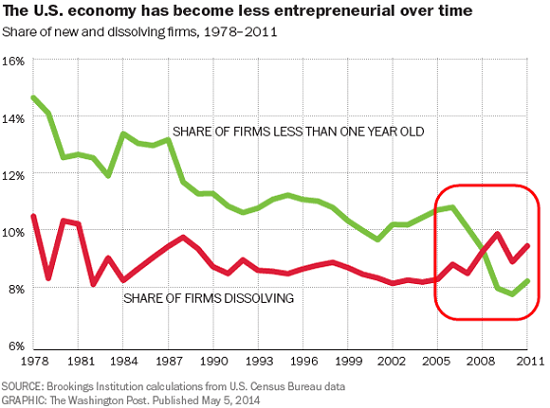

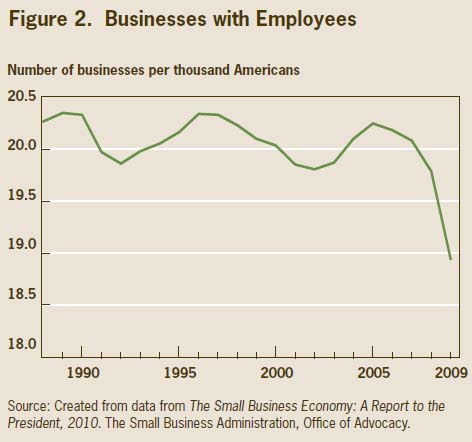

The only way to not just survive but thrive

as an entrepreneurial enterprise is to destroy fixed costs and labor

overhead.

It is not coincidental that the middle class

and small business are both in decline.Entrepreneurial enterprise

and small business have long been stepping stones to middle class

incomes and generational wealth, i.e. wealth that is

passed down to future generations rather than consumed. As the

headwinds to entrepreneurial enterprise and small business rise, the

pathway to middle class prosperity narrows.

The decline of small business also hurts

employment. Successful small businesses expand and hire

employees. As small businesses close, jobs vanish en masse.

What are the headwinds to entrepreneurial

enterprise and small business? Here are a few key dynamics:

1. Barriers erected by cartels and the

government. Cartels prosper by eliminating competition, and

the easiest, cheapest way to restrict competition is to influence

government to create regulatory barriers that raise the cost to

levels no small business can afford. There are dozens of examples of

regulations that do little to “protect the public” (the usual

rationalization) whose primary intent and effect is to suppress

competition.

Sickcare and higher education, to take two

egregious examples, are protected from real competition: there is

little real transparency in pricing and little accountability for the

efficacy of the product (diplomas, wellness).

2. Overcapacity. Supply exceeds

demand in almost every nook and cranny of the global economy. There

aren’t many high-value opportunities to pursue because every field

is already crowded or restricted.

The market ultimately sets the value of any

output. You can ask $30 for a lunch plate but the market will

determine the value. If your cost is $20 per plate and the market

value is $15, you will lose money and go out of business.

3. High cost structure. Many people

are calling for small businesses to pay their employees a living

wage. I understand the emotional source of this demand: a desire to

close the income gap and raise the standard of living of the working

poor. But since the market sets the value of any enterprise’s

output (good or services), and the business has fixed costs (rent,

utilities, business licence fees, taxes, inventory, back-office

overhead such as accounting, etc.), a business can only pay wages and

labor overhead out of gross profit–what’s left after fixed costs

are deducted from revenue.

Fixed costs and labor costs are both

skyrocketing. Commercial landlords have inflated

expectations of rent, thanks to the Fed-induced real estate bubble:

since they overpaid for the building, they need to charge high rents

to cover their mortgage payments and property taxes.

As I have explained in previous entries in this

series on the middle class, the costs of labor overhead–healthcare

insurance, pensions, payroll taxes, worker compensation, etc.–are

rising. That leaves less available for wages.

Local governments are responding to their own

soaring healthcare and pension costs by raising junk fees and taxes

on small business: in many areas, a new small business faces a

blizzard of fees for licenses, permits, etc.

The fundamental context of our economy is

not conducive to small business or conventional employment: the

cost of human labor keeps rising while technology that replaces human

labor gets cheaper; fixed costs keep rising while overcapacity and

anti-competitive barriers reduce high-value opportunities.

Any enterprise exposed to free-market forces

must create value. If businesses can only create low value good and

services, i.e. goods and services with thin margins, they can only

pay low wages–not just to employees, but to the

owners/entrepreneurs.

The only way to not just survive but thrive

as an entrepreneurial enterprise is to destroy fixed costs and labor

overhead. The food services enterprises that will thrive are

those that share the expensive fixed costs of a

kitchen. The enterprises that thrive will not own vehicles, they will

share vehicles. The enterprises that thrive will not have employees,

they will draw upon self-employed people who organize to complete a

specific project/task and share the revenue.

The way to destroy fixed costs and labor

overhead is to pay no business rent, own no vehicles, have no

employees, owe no debt, own your own tools/means of production and

nurture human and social capital. This model for small

enterprise is overturning all the skimming cartels and bureaucracies:

commercial real estate, local government fees and property taxes,

etc. etc.

The future of middle class prosperity is

entrepreneurial enterprise and joining the class of Mobile Creatives

who minimize fixed costs and overhead and maximize productive

cross-fertilization of skills, human and social capital and debt-free

ownership (or shared access to) the means of production.

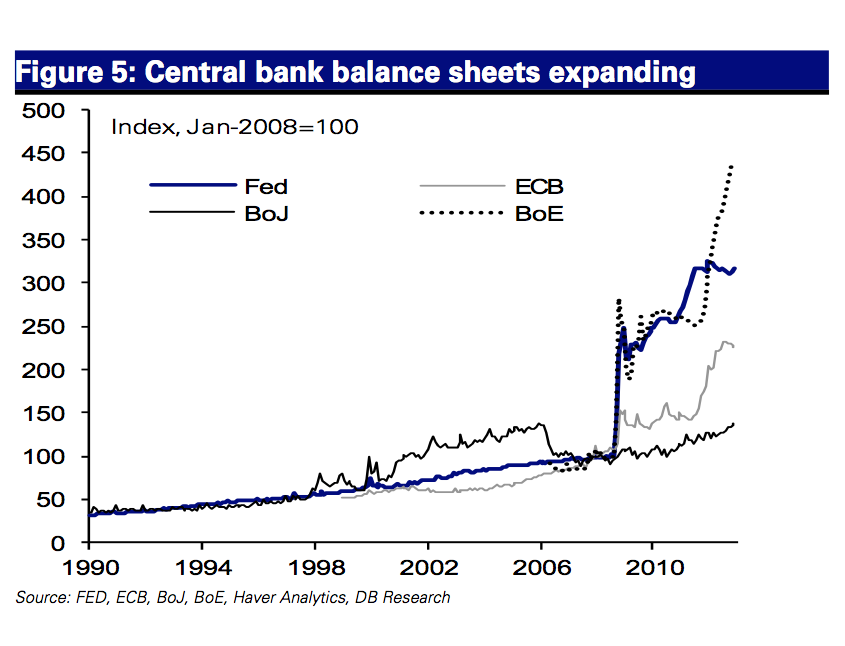

Central banks around the world are following one core mission. That mission revolves around expanding debt to goose equity markets

and attempting to solve a debt crisis with more debt. Even the more

conservative European Central Bank bowed down to easy digital money

printing by announcing they too would follow in the footsteps of the Fed

and Bank of Japan. Global banking is now fully addicted to non-stop

debt. Every dollar of debt is having a smaller impact on what it can do

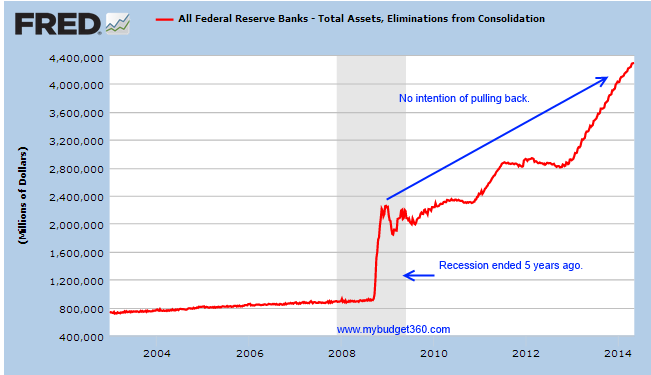

to the real economy. The Fed’s balance sheet is now well over $4.3 trillion

and while talks of tapering are made in public, there is no visible

action being taken to show this is the intended goal. At the core of the

global crisis was an expansion built on too much debt. Banks attacked

this issue as one of liquidity but in reality this was a crisis of

solvency. Banks never dealt with writing down assets but have decided to

use modern day inflation methods

to boost banking profits at the expense of working class families.

Global debt has now reached a terminal velocity mode and central banks

have no choice but to continue to expand their balance sheets.

Central banks follow one mandate

Some people act as if the crisis never happened. US stock markets are

at record levels and those with access to wealth continue to get

richer. The policies that are creating a massive low wage economy

in the US are also part of the other side of the coin expanding debt

based bubbles. It is no coincidence that items financed by debt (i.e.,

college, housing, cars, etc) are seeing inflation many times higher than

that of wages. In fact, wages are stagnant. Central banks realize that

keeping interest rates low through whatever means necessary is the only

endgame for their current charade.

Would you lend someone money if you knew you would never get paid

back? Probably not. Yet this is the trajectory being followed by central

banks. Take a look at the below illuminating chart and tell me if

central banks are operating as if we are in a full recovery:

Central banks are taking on policies that appear to indicate a deep

and profound recession. The only issue with this is that the US

recession ended in 2009. Why continue expanding at such an aggressive

pace? The chart above shows continued aggressive expansion of central

bank balance sheets. First, many US banks were fully insolvent. That is,

they had overplayed their hand and were holding onto assets that were

way overvalued. This led to the foreclosure crisis. But a funny thing

happened. The US allowed these toxic assets to fall into the Fed’s

balance sheet and policy makers allowed mark to market accounting to be

suspended. Little by little banks inflated the housing market back up.

This dramatically helped banks stay afloat while fully manipulating the

market at the public’s expense. Keep in mind millions of people lost

their homes yet every large major bank actually has become bigger and

salaries of these financiers are back to where they once were. In an

incestuous twist, many of those foreclosures are now owned by the new

rentier class as they chase yields in every asset class.

The Fed’s balance sheet only continues to grow since they essentially own the US mortgage market:

Where is the taper talk being reflected in the chart above? The Fed

now has a $4.3 trillion balance sheet. The Fed is operating in full

crisis Great Recession mode. Don’t believe any of the hype that the Fed

is in control here. Look at the Bank of Japan and you will realize that

when you are a debt making hammer, everything looks like nail.

The global markets are controlled by central banks. This is a central

bank market rally. It is also, once again, causing global property

bubbles from Canada, China, Australia, to the United States (again). The

small globally connected elite realize this and that is why you have

foreign money buying condos in New York, flats in London, and single

family homes in California. They understand what is playing out and are

doing their best to purchase real assets before the public starts waking up to this slow inflationary robbery despite what official statistics show.

Central banks have no desire to taper. Once you give a market low

rates, an addiction takes hold. Similar to low wage capitalism, once

people get used to a low price good luck trying to push higher costs.

Everything gets driven down for the prosperity of the few. We live in a

world of limited assets and central banks dealt with this debt crisis by

creating more debt. So it is no surprise that global property bubbles

are once again raging.

The fact that tapering talks have been going on for some time with no

real reversal (take a look at the Fed balance sheet chart above), you

start to realize central banks are in full terminal velocity mode. They

only have one hand to play. Convince the public they have all of this

under control until it spirals out of control, again. Keep in mind Ben

Bernanke thought the housing market issues were confined to the subprime

market in 2007, right at the peak of all the global debt madness. All

central banks are playing out of the same rule book; keep pushing rates

lower for the main purpose of keeping wealth inflated for those that actually have wealth higher by simply going into deeper debt.

Famed

commodity investor Jim Rogers is on Kitco News to speak about the

Chinese and US economy, gold, and even bitcoin. Rogers has some very

interesting thoughts about the yellow metal and where he thinks it may

be headed. “Gold is still correcting… I expect there to be another

opportunity to buy gold sometime in the next year or two.” He also

shares his insights on the US economy and how he is not so confident in

the US dollar given the country’s elevated debt levels. “No country in

world history has got itself into this kind of situation and got out

without a crisis or semi-crisis.” He also shares some insights on

bitcoin and what he thinks of the cryptocurrency. Tune in now to watch

the latest edition of “On the Spot” with Daniela Cambone. Kitco News,

May 8, 2014.

Nearly half a billion dollars in federal money has been spent

developing four state Obamacare exchanges that are now in shambles —

and the final price tag for salvaging them may go sharply

higher. Each of the states — Massachusetts, Oregon, Nevada and

Maryland — embraced Obamacare, and each underperformed. All have

come under scathing criticism and now face months of uncertainty as

they rush to rebuild their systems or transition to the federal

exchange.

The federal government is caught between writing still more

exorbitant checks to give them a second chance at creating viable

exchanges of their own or, for a lesser although not inexpensive sum,

adding still more states to HealthCare.gov. The federal system is

already serving 36 states, far more than originally anticipated.

As for the contractors involved, which have borne most of the

blame for the exchange debacles, a few continue to insist that fixes

are possible. Others are braced for possible legal action or waiting

to hear if now-tainted contracts will be terminated. The $474

million spent by these four states includes the cost that officials

have publicly detailed to date. It climbs further if states like

Minnesota and Hawaii, which have suffered similarly dysfunctional

exchanges, are added.

MORENO

VALLEY, Calif. — The freeway exits around here are dotted with people

asking for money, holding cardboard signs to tell their stories. The

details vary only slightly and almost invariably include: Laid off. Need

food. Young children.

Mary

Carmen Acosta often passes the silent beggars as she enters parking

lots to sell homemade ice pops, known as paletas, in an effort to make

enough money to get food for her family of four. On a good day she can

make $100, about double what she spends on ingredients. On a really good

day, she pockets $120, the extra money offering some assurance that she

will be able to pay the $800 monthly rent for her family’s

three-bedroom apartment. Sometimes, usually on mornings too cold to sell

icy treats, she imagines what it would be like to stand on an exit ramp

herself.

“Everyone

here knows they might have to be like that,” said Ms. Acosta, 40,

neatly dressed in slacks and a chiffon blouse, as she waited for help

from a local charity in this city an hour’s drive east of Los Angeles.

Both she and her husband, Sebastian Plancarte, lost their jobs nearly

three years ago. “Each time I see them I thank God for what we do have.

We used to have a different kind of life, where we had nice things and

did nice things. Now we just worry.”

Photo

PATCHING TOGETHER A LIVING Mary

Carmen Acosta and her husband, Sebastian Plancarte, with their

daughter, Camila, outside their apartment in Moreno Valley, Calif.Credit

Emily Berl for The New York Times

Five

decades after President Lyndon B. Johnson declared a war on poverty,

the nation’s poor are more likely to be found in suburbs like this one

than in cities or rural areas, and poverty in suburbs is rising faster

than in any other setting in the country. By 2011, there were three

million more people living in poverty in suburbs than in inner cities,

according to a study released last year by the Brookings Institution.

As a result, suburbs are grappling with problems that once seemed

alien, issues compounded by a shortage of institutions helping the poor

and distances that make it difficult for people to get to jobs and

social services even if they can find them.

In

no place is that more true than California, synonymous with the

suburban good life and long a magnet for restless newcomers with big

dreams. When taking into account the cost of living, including housing,

child care and medical expenses, California has the highest poverty rate

in the nation, according to a measure introduced by the Census Bureau

in 2011 that considers both government benefits and living costs in

different parts of the country. By that measure, roughly nine million

people — nearly a quarter of the state’s residents — live in poverty.

Not

long ago, the Inland Empire, as the sprawling suburban area east of Los

Angeles is known, attracted people hoping to live out that good life.

Before the recession, it was booming; housing developments were cropping

up all the time, quickly followed by big box stores and strip malls to

cater to the new residents.

The

region was — and still is — the fastest growing in the state. But the

jobs have never really followed the people who come here looking for

cheaper housing. The median home value is $325,000 and the median rent

is $1,690, according to the real estate database Zillow. That compares

with $462,000 and $1,860 in Los Angeles.

For

many, those costs are still unaffordable. Unemployment in the region

hovers around 10 percent and nearly one-fifth of all residents live in

poverty, the highest rate among the largest metropolitan areas in the

country. By the official federal measure, nearly one-third of all

children here are poor. The number of poor in San Bernardino and

Riverside Counties nearly doubled over the last decade.

Many

would-be workers lack office skills or more than a basic education,

making minimum-wage jobs the norm for them. Many here are immigrants —

some living in the United State illegally, making them ineligible for

most government benefits. But like Ms. Acosta, many others came here

legally decades ago and had a strong foothold in the American economy — a

job, a house, cars and regular travel.

Photo

Ice pops being made at the family’s home for sale on the street.Credit

Emily Berl for The New York Times

“This

is where poor people live now, and this is where they are going to

live,” said Alan Berube, an author of the Brookings Institution study.

“When poverty moved out of the inner cities it didn’t just go next door,

it went 30 miles away. But at the time those families might not have

been poor — they were just chasing the middle-class dream. Then, boom,

that evaporated.”

Prosperity Slips Away

Most

mornings Sebastian Plancarte, 39, puts on a freshly laundered, collared

polo shirt, carefully tucked in. He gets his daughter, Camila, dressed

for kindergarten and makes sure his son, Sebastian, has his homework

ready for middle school. They are out the door by 7:30 a.m. and he is

home nearly two hours later, back to wander parking lots selling ice

pops before the afternoon pickup routine begins. He is happy to be

involved in his children’s lives, but this is hardly the kind of

fatherhood he once imagined.

For

years, the couple thought of themselves as wealthy. They bought a

five-bedroom house in a suburb just a few miles east of downtown Los

Angeles, where they both worked in the jewelry district — she inspected

diamonds and he designed bracelets and rings. Making $16 an hour, plus

commissions, they earned as much as $2,000 a week. They traveled to San

Diego and Las Vegas, they bought their two children the toys they asked

for. Just more than a decade after they had emigrated from Mexico, they

believed their hopes had become a reality.

But

in 2011, Ms. Acosta was laid off. So was Mr. Plancarte, just a few

months later. They soon sold the house for far less than they had paid.

They drove east, looking for something they could afford to rent, and

landed in Moreno Valley, a city 60 miles inland that has become a common

outpost for those priced out of Los Angeles. They live in a sprawling

apartment complex designated for low-income families.

The

paletas have become a centerpiece of their lives. The couple constantly

think about the best prices for ingredients and how many pops are in

their small freezer; they take orders by phone to deliver to backyard

parties. When their son asks to get hamburgers at the local In-N-Out,

they have a standard response: “The mathematics are very simple,” Ms.

Acosta said. “If you want to eat there, we need you to sell $25” of the

ice pops.

“The

hardest part is the shame,” Mr. Plancarte said, sitting at his kitchen

table as his wife and daughter ate mango paletas doused in chamoy, a

blood-red sugary hot sauce. “People say to me, ‘Why don’t you find a job

over there, or at that factory or that place?’ First of all, they

aren’t there, I’ve tried. But even if they have a job, it’s going to be

paying me $8 an hour. So I’ll spend no time with my family to make less

money than I make now selling these.”

By

Ms. Acosta’s calculation, the couple earned about $25,000 last year,

nearly all of it in cash. And while it is nearly $2,000 above the

official poverty line for a family of four nationally, it is hardly

enough to meet their basic needs. By the time they pay for rent, gas,

phone, electricity and food, they have spent about $2,000 a month, Ms.

Acosta said.

Her

husband is still looking for work; in the winter months they relied

mostly on whatever she could make selling cosmetics and costume jewelry

door to door. Their lives reflect the contradictions of many living on

the edge. They have a 2001 Jeep Cherokee, a small flat-screen television

and a few remaining pieces of jewelry. They don’t have health insurance

or any savings, and they have not bought new clothes for nearly two

years.

For the last year, Ms. Acosta spent much of her time at the local Catholic Charities office,

taking self-help classes with other women in similar circumstances. She

earned $100 a month enrolling women in courses on healthy diets,

balancing checkbooks and parenting skills. She keeps a folder thick with

certificates she has earned in such classes. A letter from President

Obama thanking her for volunteering at her son’s school, calling her a

“shining example,” is tucked in a protective plastic sleeve. The few

friends she has made here, she said, are the women she has met at

Catholic Charities.

“My friends in L.A., the ones who still have money, it’s like they forgot all about us,” she said.

The

family’s economic descent has proved most difficult for 12-year-old

Sebastian, who remembers Christmas trips to Universal Studios and

regular mall excursions. Camila, 5, cannot recall anything different

from what she has now. Neither child knows that their Christmas gifts

came from charity. They are all contributing to the piggy bank in the

kitchen; if they can save enough, Ms. Acosta has promised to take them

to Disneyland this year. For now, even going to the beach an hour west

would cost too much for gas. The local park is hardly a fun outing — it

reminds them of their work selling ice pops most weekends.

Photo

Jewelry that the couple sell door to door.Credit

Emily Berl for The New York Times

“We

have to be really good actors,” Ms. Acosta said. “But after they go to

bed, we just sit and worry about how we are going to pay for things we

want to give them.”

When

his son asked for pizza recently, Mr. Plancarte took a silver bracelet

he had given his wife to a pawnshop, where he was offered a fraction of

what he thought it was worth. He accepted, too embarrassed to tell his

son they could not have pizza. Ms. Acosta recently went back and saw the

bracelet priced at $90 — more than twice what her husband had received.

Traveling More to Make Less

Sitting

inside Catholic Charities offers a glimpse of the constant need: this

family needs extra cash to pay the utility bill; this single mother

cannot find child care to allow her to work a graveyard shift; that

elderly man who came from Mexico has no way to pay for his medication.

Imelda

Santana, whose desk is just a few feet away from the entrance, is often

the first stop for requests. Ms. Santana is empathetic — just a couple

of years ago she needed help after her husband left her and she lost her

job as a loan officer amid the housing crisis. After working as a

volunteer for months, Ms. Santana was hired to sift through requests to

see which families the organization might assist. Even on the best days,

she said, there are more demands than they can handle.

“We

have people here who used to make donations now knowing what it is to

run out of toilet paper in their house and not have the money to buy

more,” she said. “Even if they get food stamps, it does not cover

toiletries. There’s just never enough.”

Yadira

Rodriguez, 35, has traveled hundreds of miles looking for work in this

county, which is roughly the size of New Jersey. When her husband

stopped earning enough to pay for monthly expenses for their three young

children, she took a job in a factory packing boxes to be shipped to

retail stores. But the $8-an-hour job was 30 miles north of her Moreno

Valley apartment, taking her more than an hour in traffic, twice that if

she needed to take the bus.

Since

she was classified as a temporary worker, she would leave her home at 4

a.m. only to find out at 6 a.m. that she would not be hired for the

day. On days there was work, she would arrive back home 12 hours after

she left.

“I

could not understand how this was worth the money,” Ms. Rodriguez said.

“I would get home and the kids would be tired and cranky and I didn’t

have energy for them. How was this going to make my life better?”

After

three months, she quit. Her family relies on $800 a month from the

state’s temporary cash assistance program to pay for groceries and

utilities, and gets occasional help from charities. The landlord has let

the family slide on the rent at times, Ms. Rodriguez said.

Like

Ms. Rodriguez, many would-be employees see unpredictability as a fact

of life. Many social workers see more clients working two part-time

minimum wage jobs, juggling schedules to make sure they do not

disappoint any boss and hustling to cobble together child care for

shifts that can begin or end before dawn. Many are immigrants who speak

only basic English after years of living in Latino enclaves, first in

Los Angeles, and now here.

“This

is the edge of affordability; people came here because they were pushed

out to the only place where they could afford,” said John Husing, a

local economist who has studied the region for years. “When they came

here the primary wage earner could find a job to pay the bills. The

problem is that time has passed and we don’t have a lot of jobs that

allow that anymore.”

Photo

AD HOC AID A clothing giveaway at Victoria Elementary School in San Bernardino, Calif. The school also sponsors a medical clinic.Credit

Emily Berl for The New York Times

While

many of the state’s coastal areas have begun to see signs of an

improved economy, the inland region has continued to struggle.

Unemployment and foreclosure rates remain stubbornly high here and there

are few signs that the area will boom as it did a decade ago. Housing

prices have inched up as wages have stagnated, making it even more

difficult for families to stay afloat.

“What

we have out here is more need and fewer centers of resources,” said Dom

Betro, the executive director of Family Services, a nonprofit group

that provides child care and food to needy families in Riverside County.

“We have more working poor than anyone can know how to handle. People

travel further distances to work for less pay because they have to. Even

if there is help — and that’s not always — people who need it can’t get

to it.”

Social workers here often point to a 2009 study by the James Irvine Foundation,

which showed that the region has far fewer nonprofit groups per capita

than the rest of the state, with less money funneled in from local

foundations.

“There’s

all these new problems but no new philanthropic dollars there to

address them,” said Mr. Berube, from the Brookings Institution. “In many

places there are these de facto systems in place but not the kind of

leadership to really address what’s needed.”

When

Larry Ellwell became principal of Victoria Elementary School in San

Bernardino a few years ago, he was stunned by the number of families who

could not afford necessities like clothes and dental care. When he

worked with poor students closer to Los Angeles, he said, they knew

where to find aid. But in the Redlands school district, home to a

university and well-appointed mansions, there were few free clinics or

other outlets for assistance. So he began to offer them — now the school

hosts a roving clinic staffed by medical students and a clothing

giveaway known as Victoria’s Closet.

“It’s

a lot of triage work — who needs something the most and what do they

most need,” Mr. Elwell said. “There’s no stigma anymore, because so many

people are just trying to scrape by and make it work.”

For

Ms. Acosta, scraping by recently took a new turn: She moved to the

other side of the desk at Catholic Charities, taking a job as an intake

worker. She works about 30 hours a week at $12 an hour, giving people

the same kind of help she seeks. Even now, she is not earning enough to

stop selling ice pops.

Just

a couple of years ago, when the dry cleaner called reminding her to

pick up a pair of pants, Ms. Acosta told him to give them to charity.

“Now I am one of the people taking giveaways,” she said. “I see people

all the time in worse positions than we are in. The kids are healthy, we

have a roof. Maybe that’s the best we can hope for.”

A version of this article appears in print on May 10, 2014, on page A1 of the New York edition with the headline: Hardship Makes a New Home in the Suburbs. Order Reprints|Today's Paper|Subscribe