Detroit's bankruptcy case is another example of how Wall Street wins, according to The New York Times.

Fixing Detroit's financial dilemma is supposed to be done by "shared

sacrifice" between pensioners and municipal bond investors. Nice idea in

theory, but the big banks — which helped cause the city's financial

problems — don't seem to be sharing that sacrifice, according to The

Times' editorial board.

Meanwhile pensioners are vulnerable, as their pensions are not federally insured and many do not get Social Security.

Editor’s Note: 75% of Seniors Make This $152,000 Social Security Mistake (See Easy Fix)

Under its settlement in the works with creditors, the city will pay

approximately $250 million to UBS and Bank of America to settle

derivative deals, know as interest rate swaps.

In the swap deals, the banks would pay the city if rates rose, while the

city would pay the banks if they fell. As it turned out, rates fell and

the city had to pay the banks about $50 million a year and pledge $11

million a month in casino tax revenue as collateral.

Under the settlement, which still needs to be approved by a bankruptcy

judge, the banks agreed to take a 25 percent haircut. That doesn't mean

they'll suffer, The Times notes, as they've already made money of the

swaps.

"The banks' 25 percent hit is nothing compared with the 90 percent cut

to pensions suggested by the city — a cut that would be disastrous in

both human and political terms and that the State of Michigan must

prevent from happening," The Times argues.

"Municipal officials are prey for Wall Street," the paper asserts.

The Dodd-Frank Act law instructs regulators to improve protections for

municipalities and other clients who deal with Wall Street. But the

Securities and Exchange Commission has yet to complete rules, and the

Commodity Futures Trading Commission's rules are so weak, the newspaper

says, they practically invite banks to exploit municipalities.

"The special treatment banks receive when debtors are in or near

bankruptcy," the editorial board states, "is unfair and economically

destabilizing."

Banks' swap deals are inadequately regulated and typically not subject

to court rulings. In Detroit's bankruptcy case, banks are paid before

other secured creditors, which is destabilizing because it encourages

recklessness, according to The Times.

Ironically, Detroit's swaps deals worsened its pension obligations,

according to The Wall Street Journal. They were supposed to help

alleviate its debt load, but ended up cutting off access for the casino

revenue.

The bankruptcy case will probably set precedents for handling swaps

counterparties, as well as bondholders and pensioners, Reuters predicts.

Editor’s Note: 75% of Seniors Make This $152,000 Social Security Mistake (See Easy Fix)

© 2013 Moneynews. All rights reserved.

Monday, August 19, 2013

Indian, Indonesian currencies come under fire

By Wayne Cole

SYDNEY (Reuters) - India's currency cartwheeled to historic lows on

Monday while markets in Indonesia took a spill, evidence of how rising

U.S. yields are making it harder for emerging nations to fund their

current account deficits.The turbulence heightened investor caution ahead of Wednesday's minutes of the Federal Reserve's last policy meeting, with many fearing they might only add to the confusion about when it might scale back stimulus.

That helped gold reach its highest in two months, while keeping share markets constrained across Asia.

In Europe, Britain's FTSE futures inched up 0.2 percent in early deals. The German DAX futures were down 0.04 percent, as bund yields climbed to the highest since early 2012.

The Indian rupee slid as far as 62.50 per dollar, emphatically breaching the previous low of 62.03. The share market (.NSEI) lost 1.4 percent, on top of a 4 percent drubbing last Friday.

The currency has been hurt by investor frustration at the slow pace of economic reform in India, which has made it harder for the country to finance its hefty current account shortfall.

The Reserve Bank of India has tried to restrict how much Indian residents and companies can send offshore, but that only raised fears of outright capital controls that would further undermine the confidence of foreign investors.

"The foreign investor community want tangible and ambitious reforms that look and feel like a worthy ‘second generation' to the fundamental measures adopted in the early 1990s," Westpac analysts said in a note.

They also found it "curious" the central bank would be fighting against a depreciation in the rupee given that it would help boost exports and limit imports over time.

Indonesia's rupiah shed 0.9 percent to four-year lows at 10,475 per dollar, with share and bond markets weakening in the wake of data showing a sharp widening in the country's current account deficit.

The task of attracting funding for these shortfalls has become ever tougher as investors priced in a start to Fed tapering and pushed up U.S. market rates.

Yields on 10-year Treasury debt were up near two-year highs at 2.87 percent on Monday, putting upward pressure on borrowing costs across the globe.

The strain showed in MSCI's broadest index of Asia-Pacific shares outside Japan <.miapj0000pus> which fell 0.5 percent. It had ended last week with gains of 1.45 percent, but that merely recovered ground lost during the previous two weeks.

Stocks in Shanghai (.SSEC) rebounded to be up 0.6 percent, The Korean market (.KS11) eased 0.1 percent but Thai shares shed 1.2 percent (.SETI) as data there showed the economy slipped into recession last quarter.

As usual Tokyo's Nikkei share average (NIK:^9452) went its own way and rose 0.8 percent on Monday, brushing aside data showing the third-largest trade deficit on record as imports rose even faster than exports.

Australia's S&P/ASX 200 index (.AXJO) was dead flat.

Crucial later in the week will be an early reading on Chinese manufacturing from HSBC. Recent data suggested the economy might be stabilizing and any improvement in the purchasing manager index will be welcomed by Asian investors.

GOLD ON A ROLL

The U.S. dollar gave up early, modest gains to stand at $1.3326 per euro, barely moved from Friday. Against the yen it pulled back to 97.59, while the dollar index was a shade firmer at 81.324 (.DXY).

The dollar has been in gradual decline for the past six weeks so, in part on concerns the prospect of Fed tapering would scare foreign investors out of U.S. bonds.

Figures out last week showed China and Japan -- the two largest foreign holders of U.S. debt -- were at the forefront of a $66 billion exodus from long-term U.S. Treasuries in June, dumping a net $40 billion.

Still, at some point yields should reach levels that are attractive to investors once more.

"We continue to believe that tapering will begin at the September meeting and, hence, support the USD, especially against high-yielding currencies," analysts at Barclays said in a note.

They added, however, there was a chance the Fed may have begun discussing lowering its threshold rate for unemployment as a way to convince investors that rates will remain near zero for a long time to come.

"Any discussion in this regard is likely to be viewed as a dovish surprise by the market and lead to a near-term rally in the belly of the Treasury curve," said Barclays. The dollar would also be vulnerable in such an event.

Hopes for a pick-up in growth globally has also supported commodities recently, with copper holding at $7,372 a tonne (1.1023 ton) after hitting a 10-week peak of $7,420 on Friday.

Gold and platinum have gained as well, though they could be threatened if the Fed does wind down its stimulus. Gold made a fresh two-month high of $1,384.10 an ounce.

Oil futures shrugged aside early losses to sneak higher, having recorded their the biggest weekly percentage gain in six weeks as turmoil in Egypt and Libya stoked worries about supply.

Brent crude futures for October were little changed at $110.38 a barrel, was were U.S. oil for September at$107.39.

(Editing by Eric Meijer)

China probe is latest legal headache for JPMorgan

By David Henry

NEW YORK (Reuters) - A federal bribery investigation into whether

JPMorgan Chase & Co. hired the children of key Chinese officials to

help it win business is just the latest in a series of legal and

regulatory headaches for Chief Executive Jamie Dimon.Dimon piloted the bank through the financial crisis, but it is now facing at least a dozen investigations from federal agencies and state and foreign governments, including over the "London Whale" trading scandal that cost it more than $6.2 billion.

In the latest probe, the Securities and Exchange Commission (SEC) is looking at whether the bank's Hong Kong office hired the children of powerful heads of state-owned companies in China with the express purpose of winning underwriting business and other contracts, a person familiar with the matter said.

The SEC is questioning JPMorgan's relationships with at least two families in China that may have legitimate explanations, the source said.

U.S. law does not stop companies from hiring politically well-connected executives. But hiring people in order to win business from relatives can be bribery, and the SEC is investigating JPMorgan's actions under the U.S. Foreign Corrupt Practices Act.

SEC spokeswoman Florence Harmon declined to comment on the investigation. A Hong Kong-based spokeswoman for the bank declined to comment beyond what was in the bank's regulatory filings and said the bank was cooperating with probes.

REGULATORY HEADACHES

Whatever the outcome of the latest investigation, Dimon's time is increasingly being consumed by regulatory matters.

Federal prosecutors on Wednesday brought criminal charges against two former JPMorgan traders, accusing the pair of deliberately understating losses in the "Whale" scandal. The SEC is seeking an admission of wrongdoing from the bank in a parallel civil action, a rare step for the government agency.

Earlier this month, the bank revealed that it was facing parallel criminal and civil probes by the U.S. Department of Justice in California into mortgage bonds that it sold before the financial crisis.

And last month, the bank agreed to pay a $285 million penalty and give back $125 million of trading profits in a settlement with the Federal Energy Regulatory Commission for alleged power market manipulation. JPMorgan neither admitted nor denied violations.

Since 2011, the bank has been writing in its quarterly filings with regulators that it "is currently experiencing an unprecedented increase in regulation and supervision, and such changes could have a significant impact on how the firm conducts business". In its last quarter, JPMorgan estimated that it could have legal losses that are $6.8 billion beyond an undisclosed sum that it has already set aside to cover those charges.

Wall Street analysts may be understating the extent of the bank's future litigation expenses, said independent analyst Charlie Peabody of Portales Partners.

JPMorgan's annual litigation costs have been around $4.9 billion for each of the last two years, and Peabody expects the cost will be $1.5 billion to $2 billion over each of the next two quarters. On average Wall Street expects roughly $300 million to $500 million per quarter, he added.

While major U.S. banks have faced a litany of probes since the financial crisis, Dimon has repeatedly griped in public about how regulations designed to prevent the next financial crisis are stifling banking and its ability to help the economy.

A report from a U.S. Senate subcommittee described an episode where Dimon shouted at his then-chief financial officer for giving information to a regulator. The bank's board of directors has made it clear to the chairman and chief executive that he must improve his relationship with regulators, a source familiar with the matter told Reuters earlier this year.

Even with heavy litigation costs, JPMorgan posted $21.28 billion of net income last year, its highest level ever even after it suffered from $6.2 billion of trading losses from the bad derivatives bets made by Bruno Iksil, the trader nicknamed the "London Whale".

"ELEPHANT HUNTING"

In the China case, the New York Times said that JPMorgan at one point hired Tang Xiaoning, the son of Tang Shuangning, chairman of the China Everbright Group, a state-controlled financial conglomerate. He also had been a Chinese banking regulator, the Times reported.

After the younger Tang joined JPMorgan, the bank secured several important assignments from the Chinese conglomerate, including advising a subsidiary on a stock offering, according to the newspaper.

Another matter the SEC is probing is JPMorgan's hiring Zhang Xixi, the daughter of a now-disgraced Chinese railway official. The bank went on to help advise the official's company, which builds railways for the Chinese government, on its plans to go public, the Times said.

The bank has not been accused of wrongdoing, the New York Times said, citing a government document. There is no documentary evidence that Zhang Xixi or Tang Xiaoning were unqualified, but the SEC is checking whether the bank's Hong Kong office routinely won business from companies connected to its employees, the newspaper reported.

Marie Cheung, a Hong Kong-based spokeswoman for the bank, said on Sunday that the bank had publicly disclosed the investigation in its quarterly regulatory filing earlier this month, and was cooperating with regulators.

The quarterly filing said that the SEC's enforcement division had requested "information and documents relating to, among other matters, the firm's employment of certain former employees in Hong Kong and its business relationships with certain clients".

The practice of hiring politically-connected bankers in China was widespread in the early to mid-2000s, when Wall Street firms engaged in so-called 'elephant hunting', a term used to describe the chasing of mandates to manage the multi-billion dollar stock offerings of the country's big state-owned enterprises.

One of the more well-known China bankers from that era is Margaret Ren, the daughter-in-law of former Chinese Premier Zhao Ziyang, who has worked at several banks. Most major investment banks have employed a politically connected Chinese banker, whether a high level professional such as Ren or a college age associate, at some stage in the last decade.

Many senior investment bankers in China now feel that the heyday for such underwriting contracts has passed, with far fewer jumbo state-owned company listings happening. But banks and private equity firms alike still prize connections to top decision makers.

(Additional reporting by Michael

Flaherty and Lawrence White in Asia, Tom Brown and Ian Simpson in the

United States; Editing by Dan Wilchins, Peter Henderson and Alex

Richardson)

Fiat Empire (Full Version)

This documentary with RON PAUL, G. EDWARD GRIFFIN, EDWIN VIEIRA and TED

BAEHR is an excellent primer for the citizen who wants to get an

understanding of how money is created and why the U.S. government is in

partnership with the elite banks.

The True Cost of Health Care (Full Lecture)

Forget everything you ever thought you knew about health care costs!

In this video I reveal that:

-Most generic medications cost less than most insurance copays

-Hospitals routinely bill ten or more times what they expect to be paid

-Most outpatient tests and procedures are very inexpensive to perform

-Health insurance companies deliberately manipulate these costs to maintain their profits

And much more!

From the website of Dr. David Belk: http://truecostofhealthcare.org

In this video I reveal that:

-Most generic medications cost less than most insurance copays

-Hospitals routinely bill ten or more times what they expect to be paid

-Most outpatient tests and procedures are very inexpensive to perform

-Health insurance companies deliberately manipulate these costs to maintain their profits

And much more!

From the website of Dr. David Belk: http://truecostofhealthcare.org

Nonprofit delaying defaults on clients' homes through layered scheme

Published: Saturday, August 17, 2013 at 11:25 p.m.

Last Modified: Saturday, August 17, 2013 at 11:25 p.m.

A Sarasota nonprofit advertised as a government-sponsored

foreclosure rescue is using its clients' homes for a sweeping real

estate scheme — delaying defaults through recurrent bankruptcy filings

while renting the houses out, a Herald-Tribune investigation has found.

Keeping Kids in Their

Home Foundation Corp. and related entities have enticed scores of

severely delinquent borrowers from Tampa to Miami to hand over their

deeds for just $100, while using dubious techniques to evade mortgage

lenders and skirt taxes on those transactions.

The

parents of famed wire-walker Nik Wallenda, real estate flippers, a

karate sensei and a local pastor are among the borrowers who took out

multiple loans against their homes during the housing bubble. When the

market slumped and foreclosure was imminent, each turned to Aleksandr

Filipskiy and his foundation for help.

Filipskiy

has managed to stall those defaults for years by routinely transferring

properties to new shell companies and nonprofits he creates, filing for

bankruptcy protection under each entity to block the foreclosure

proceedings.

All the

while, he leases the distressed homes back to their troubled buyers,

rents them to others and even lives in one with his family. His brother

inhabits another, the Herald-Tribune's investigation revealed.

“There's

a lot of misrepresentation here,” said Andrew Rose, a special agent

supervisor with the Florida Department of Law Enforcement. “Someone

should never deed their house over to anyone without the bank's consent.

These guys are predators. It's just sad and disgusting.”

What Does it Mean to be an Outsider in a Capitalist Society?

Copyright © 2013 by Alissa Quart. This excerpt originally

appeared in Republic of Outsiders: The Power of Amateurs, Dreamers, and

Rebels published by The New Press

The traditional duality between insider and outsider has, to some extent, broken down. Media renegades, for instance, tend to be people who in a previous era would have been marginalized from established newspaper and media culture; now they create separate spheres where their voices are often more popular than the output of traditional news organizations. But then the most popular of these once-outsider voices are seemingly inevitably swallowed up by the big media brands. Or take a look at formerly fringe stances such as “animal protection,” which has become so familiar that it’s appropriated by burger franchises.

So what constitutes rebellion, originality, and resistance in a culture of remix? What is rebellious thought? In fact, what does it mean to be an outsider in a contemporary culture where “selling out” has almost become an honorific?

The results vary, of course. Sometimes rebels’ attempts fail. Sometimes they succeed on their own terms. Whether these identity innovators fail or succeed, the outcomes can be attributed to the aggressively viral and short life span new ideas are now afforded in America. The line between the outsider and the establishment seems to shift by the day. Once upon a time, an established band or a musician disseminating music from her own small label was maverick or newsworthy; a few years later, that’s closer to the industry standard. Some of the cases in the book, such as the once-disruptive technologies I first reported on years ago and considered for inclusion in these pages, including Craigslist and Pandora, have since become part of a new establishment. Craigslist radicalized sales and publishing, but sooner rather than later its owner had been recast as a kindly philanthropist whose site the New York Times dubbed stodgy and reactionary.

This trajectory isn’t entirely surprising. In the last two generations, centrist culture in the United States has taken on and been enriched by novel, countercultural ideas, movements, and products, including civil rights, workplace safety laws, community antismoking campaigns, “green” architecture and cars, and the widening acceptance of gays (even in the military). And the digital has altered what’s inside the categories “outsider,” “indie culture,” and “niche market”: the Web has increased visibility at the margins because every rebel or amateur can publish or post his or her opinion. There is also a chance of anyone’s output going viral. That in itself changes what is considered outsider or marginal and how “fringe culture” operates: alternative or subcultures no longer assume their messages are for the few or the like-minded. The idea of a mainstream is, at the very least, a useful cliché. Yet it becomes less of a cliché when we recognize that all cultures—the establishment culture included—are dynamic.

Of course, today’s forces of rebellious style can also act as

mere supplements to the mainstream. The stances, practices, or

styles are often borrowed and watered down. Sometimes these

outsiders are voluntarily co-opted, or what I call “self-co-opted,”

offered up to a more homogenous populace by the renegades themselves.

While the Internet has enabled saboteurs, it has also created an ephemeral culture where alternatives to the mainstream arise only to crash almost instantly or be absorbed into the established order overnight. Instead of a broad-based participatory democracy, digital culture has given us millions of fragments; while some offer a respite from the endless churn of late capitalism, the escape provided is usually fleeting.

This is not the first era in which this has occurred. Throughout history, movements, aesthetics, and disruptive technologies would eventually be formalized, institutionalized, and capitalized. Outsider styles would be borrowed by insiders and ultimately mainstreamed. Sociologist Philip Selznick popularized the word co-optation to describe this process when he wrote an analysis of the Tennessee Valley Authority’s relationship with community groups and elites in the 1930s. For Selznick and others, co-optation is the process by which a dominant group copies or steals another group’s ideas, style, or practices.

Republished from: AlterNet

The traditional duality between insider and outsider has, to some extent, broken down. Media renegades, for instance, tend to be people who in a previous era would have been marginalized from established newspaper and media culture; now they create separate spheres where their voices are often more popular than the output of traditional news organizations. But then the most popular of these once-outsider voices are seemingly inevitably swallowed up by the big media brands. Or take a look at formerly fringe stances such as “animal protection,” which has become so familiar that it’s appropriated by burger franchises.

So what constitutes rebellion, originality, and resistance in a culture of remix? What is rebellious thought? In fact, what does it mean to be an outsider in a contemporary culture where “selling out” has almost become an honorific?

The results vary, of course. Sometimes rebels’ attempts fail. Sometimes they succeed on their own terms. Whether these identity innovators fail or succeed, the outcomes can be attributed to the aggressively viral and short life span new ideas are now afforded in America. The line between the outsider and the establishment seems to shift by the day. Once upon a time, an established band or a musician disseminating music from her own small label was maverick or newsworthy; a few years later, that’s closer to the industry standard. Some of the cases in the book, such as the once-disruptive technologies I first reported on years ago and considered for inclusion in these pages, including Craigslist and Pandora, have since become part of a new establishment. Craigslist radicalized sales and publishing, but sooner rather than later its owner had been recast as a kindly philanthropist whose site the New York Times dubbed stodgy and reactionary.

This trajectory isn’t entirely surprising. In the last two generations, centrist culture in the United States has taken on and been enriched by novel, countercultural ideas, movements, and products, including civil rights, workplace safety laws, community antismoking campaigns, “green” architecture and cars, and the widening acceptance of gays (even in the military). And the digital has altered what’s inside the categories “outsider,” “indie culture,” and “niche market”: the Web has increased visibility at the margins because every rebel or amateur can publish or post his or her opinion. There is also a chance of anyone’s output going viral. That in itself changes what is considered outsider or marginal and how “fringe culture” operates: alternative or subcultures no longer assume their messages are for the few or the like-minded. The idea of a mainstream is, at the very least, a useful cliché. Yet it becomes less of a cliché when we recognize that all cultures—the establishment culture included—are dynamic.

While the Internet has enabled saboteurs, it has also created an ephemeral culture where alternatives to the mainstream arise only to crash almost instantly or be absorbed into the established order overnight. Instead of a broad-based participatory democracy, digital culture has given us millions of fragments; while some offer a respite from the endless churn of late capitalism, the escape provided is usually fleeting.

This is not the first era in which this has occurred. Throughout history, movements, aesthetics, and disruptive technologies would eventually be formalized, institutionalized, and capitalized. Outsider styles would be borrowed by insiders and ultimately mainstreamed. Sociologist Philip Selznick popularized the word co-optation to describe this process when he wrote an analysis of the Tennessee Valley Authority’s relationship with community groups and elites in the 1930s. For Selznick and others, co-optation is the process by which a dominant group copies or steals another group’s ideas, style, or practices.

Republished from: AlterNet

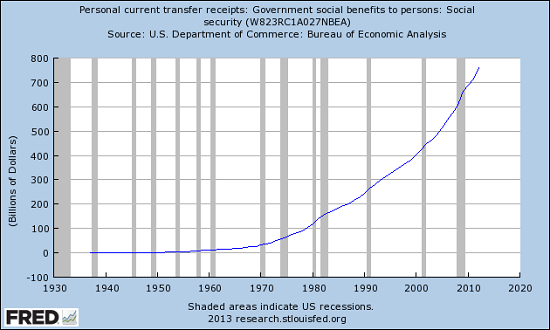

The Trends Few Dare Discuss: Social Security and the Decline in Full-Time Employment

by Charles Hugh-Smith

Believing official reassurances based on Fantasyland projections of ever-rising payroll taxes and employment does not magically make the Social Security system viable.

Questioning the financial viability of the Social Security system is often taken as an attack on the program itself. Nothing could be further from reality. Anyone who truly wants Social Security to continue as is should take an active interest in structural trends rather than focusing all their energy on attacking those who question the official reassurances that the system is sound until 2033.

The two primary trends are obvious:

1. A structural decline in full-time employment

2. A historically unprecedented increase in Social Security benefits paid

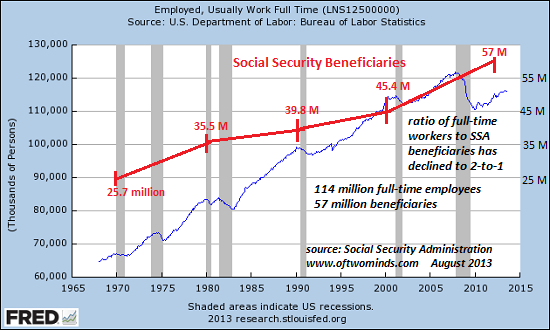

Take a look at this chart I prepared from St. Louis Federal Reserve and Social Security Administration (SSA) data: Social Security beneficiaries, by year

Notice that the ratio of full-time workers to SSA beneficiaries was comfortably higher than 2-to-1 for decades. Simply put, the number of full-time workers rose at roughly the same rate as the number of people drawing SSA benefits.

The full-time worker/beneficiary ratio was 2.56 in 1970 and 2.49 in 2000–basically the same ratio held for 30 years as full-time employment expanded along with the number of SSA beneficiaries.

But the trendlines are separating as the number of people drawing SSA benefits is soaring while the number of full-time jobs is stagnating. The increase in beneficiaries fro 1970 to 1980 was a steep 9.8 million, but full-time jobs increased by about 16 million despite the stagflationary economy.

The increases in beneficiaries in the next two decades was modest: 4.3 million more between 1980 and 1990, and 5.6 million more between 1990 and 2000. Meanwhile, the economy added roughly 30 million full-time jobs over those two decades.

The increase in beneficiaries between 2000 and 2010 was almost 10 million, while the number of full-time jobs in 2010 actually declined from 2000.

The ratio of full-time workers to SSA beneficiaries is now 2-to-1 and will fall below 2-to-1 as the number of beneficiaries rises.

The recession of 2008-9 revealed a deeply structural decline in full-time employment. Why focus on full-time employment? Only full-time workers pay enough payroll taxes to fund the system. Around 38 million workers make less than $10,000 a year, which means the SSA contributions they and their employers pay is on the order of $1,000 or so a year.

Workers paying in $1,000 or so a year (adjusted for inflation) will receive far more than their contributions in benefits, and so the system depends on higher-income workers.

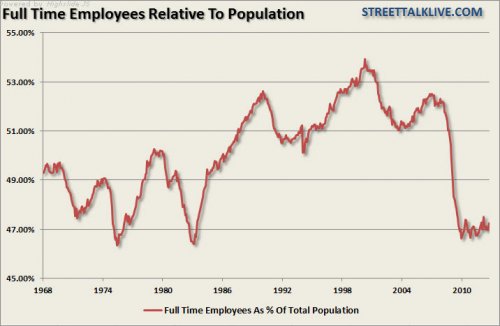

The problem is full-time work is in structural decline for a number of reasons that aren’t going away: globalization, robotics, advances in software, fast-rising cost of employee healthcare benefits and so on. We can clearly see this structural decline in these charts:

Here is full-time employees as a percentage of the population, courtesy of Lance Roberts:

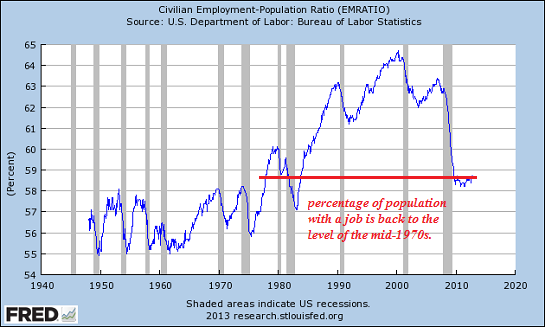

The same trend in a chart of civilian employment, which includes part-time jobs:

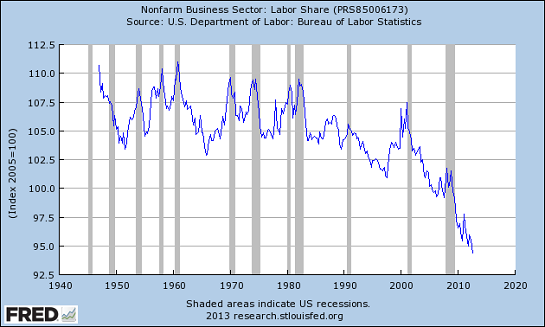

Labor’s share of the economy is in near-freefall:

Notice the trajectory of Social Security benefits: to the moon, while full-time employment has stagnated.

The Social Security system ran a $55 billion deficit in 2012, meaning that payroll tax receipts did not cover benefits paid. (Recall that SSA is “pay as you go,” meaning that current taxpayers fund the benefits paid to current beneficiaries.)

The fiction of the Trust Fund enables some intergovernmental sleight-of-hand, as the Treasury borrows money on the global bond market and pays the SSA interest on the fictional Trust Fund, but the bottom line is that the SSA deficit is funded by the Treasury borrowing money by selling Treasury bonds.

If the global economy slides into recession in the years ahead, as seems increasingly likely, full-time employment in the U.S. could slip to 100 million while the number of beneficiaries continues to soar by 10+ million a decade. All the official projections assume steady, strong increases in payroll taxes and full-time employment; the system’s deficits will explode higher if full-time employment sags while the number of beneficiaries increases from 57 million to 70 million and then on to 80 and 90 million.

Anyone who cares about the viability of Social Security had better wake up to the widening divergence of full-time employment and SSA beneficiaries.

Believing official reassurances based on Fantasyland projections of ever-rising payroll taxes and employment does not magically make the system viable.

Believing official reassurances based on Fantasyland projections of ever-rising payroll taxes and employment does not magically make the Social Security system viable.

Questioning the financial viability of the Social Security system is often taken as an attack on the program itself. Nothing could be further from reality. Anyone who truly wants Social Security to continue as is should take an active interest in structural trends rather than focusing all their energy on attacking those who question the official reassurances that the system is sound until 2033.

The two primary trends are obvious:

1. A structural decline in full-time employment

2. A historically unprecedented increase in Social Security benefits paid

Take a look at this chart I prepared from St. Louis Federal Reserve and Social Security Administration (SSA) data: Social Security beneficiaries, by year

Notice that the ratio of full-time workers to SSA beneficiaries was comfortably higher than 2-to-1 for decades. Simply put, the number of full-time workers rose at roughly the same rate as the number of people drawing SSA benefits.

The full-time worker/beneficiary ratio was 2.56 in 1970 and 2.49 in 2000–basically the same ratio held for 30 years as full-time employment expanded along with the number of SSA beneficiaries.

But the trendlines are separating as the number of people drawing SSA benefits is soaring while the number of full-time jobs is stagnating. The increase in beneficiaries fro 1970 to 1980 was a steep 9.8 million, but full-time jobs increased by about 16 million despite the stagflationary economy.

The increases in beneficiaries in the next two decades was modest: 4.3 million more between 1980 and 1990, and 5.6 million more between 1990 and 2000. Meanwhile, the economy added roughly 30 million full-time jobs over those two decades.

The increase in beneficiaries between 2000 and 2010 was almost 10 million, while the number of full-time jobs in 2010 actually declined from 2000.

The ratio of full-time workers to SSA beneficiaries is now 2-to-1 and will fall below 2-to-1 as the number of beneficiaries rises.

The recession of 2008-9 revealed a deeply structural decline in full-time employment. Why focus on full-time employment? Only full-time workers pay enough payroll taxes to fund the system. Around 38 million workers make less than $10,000 a year, which means the SSA contributions they and their employers pay is on the order of $1,000 or so a year.

Workers paying in $1,000 or so a year (adjusted for inflation) will receive far more than their contributions in benefits, and so the system depends on higher-income workers.

The problem is full-time work is in structural decline for a number of reasons that aren’t going away: globalization, robotics, advances in software, fast-rising cost of employee healthcare benefits and so on. We can clearly see this structural decline in these charts:

Here is full-time employees as a percentage of the population, courtesy of Lance Roberts:

The same trend in a chart of civilian employment, which includes part-time jobs:

Labor’s share of the economy is in near-freefall:

Notice the trajectory of Social Security benefits: to the moon, while full-time employment has stagnated.

The Social Security system ran a $55 billion deficit in 2012, meaning that payroll tax receipts did not cover benefits paid. (Recall that SSA is “pay as you go,” meaning that current taxpayers fund the benefits paid to current beneficiaries.)

The fiction of the Trust Fund enables some intergovernmental sleight-of-hand, as the Treasury borrows money on the global bond market and pays the SSA interest on the fictional Trust Fund, but the bottom line is that the SSA deficit is funded by the Treasury borrowing money by selling Treasury bonds.

If the global economy slides into recession in the years ahead, as seems increasingly likely, full-time employment in the U.S. could slip to 100 million while the number of beneficiaries continues to soar by 10+ million a decade. All the official projections assume steady, strong increases in payroll taxes and full-time employment; the system’s deficits will explode higher if full-time employment sags while the number of beneficiaries increases from 57 million to 70 million and then on to 80 and 90 million.

Anyone who cares about the viability of Social Security had better wake up to the widening divergence of full-time employment and SSA beneficiaries.

Believing official reassurances based on Fantasyland projections of ever-rising payroll taxes and employment does not magically make the system viable.

NSA snooping could cost US tech companies up to $35bn over 3 years

The role of America’s intelligence boss on the panel reviewing government surveillance programmes is causing controversy. James Clapper was expected to lead the inquiry, which was promised to be independent – but now it looks like he’ll only have a limited part to play. And all this scrutiny of spying methods is costing big tech companies, big money.

Walmart sales expose collapsing economy

Walmart reported earnings of $1.24 a share Thursday on revenues of

$116.2 billion for the second quarter. Analysts had been expecting $1.25

on $118.5 billion. Sales in stores open more than a year declined 0.3%.

Walmart also guided lower for the full year citing a “challenging sales

and operating environment.” The stock is off sharply and at risk of

going negative for the last 52 weeks.

Those are the numbers, but not the whole story. Walmart is the thermometer of the American economy. Disregard the government data. Jobs and GDP and all the rest are at best inaccurate measures of the economy and at worst flat out corrupt. Walmart is capitalism writ large.

The entire organization is focused on nothing but selling goods and services to Americans. It may be an empire in decline, but Walmart sells more than $1 billion worth of merchandise per day in a bad quarter. When Walmart misses estimates, it can only mean one of two things: either Walmart or the American economy is weaker than anyone thought.

“Walmart is a terrific retail operator… They didn’t suddenly become stupid,” says Howard Davidowitz, one of the top retail minds in the country. “The economy is in collapse. That’s what’s going on.”

Davidowitz points out that Walmart isn’t just a store for the downtrodden. They have 150 million customers which collectively spent less in Walmart stores than in the same period last year. Davidowitz says another 50 million customers shop at Target, which he also expects to have negative comp stores sales when it reports next week.

Don’t forget that Macy’s also missed expectations yesterday. Three

makes a trend. The GDP data is positive and the employment data says

things are improving gradually. Either the best merchants in America

forgot how to sell, Americans stopped consuming beyond their means, or

the economy is turning south, not getting better.

“I don’t think we’re in a recession right now, but I think there’s a 50 percent chance we’ll be in one next year,” Davidowitz shouts, and there’s nothing the government is going to be able to do about it. “We’ve spent all the money, we’ve borrowed all the money, and we’re in the tank.”

AHT/DB

…read more

Republished from: Press TV

Those are the numbers, but not the whole story. Walmart is the thermometer of the American economy. Disregard the government data. Jobs and GDP and all the rest are at best inaccurate measures of the economy and at worst flat out corrupt. Walmart is capitalism writ large.

The entire organization is focused on nothing but selling goods and services to Americans. It may be an empire in decline, but Walmart sells more than $1 billion worth of merchandise per day in a bad quarter. When Walmart misses estimates, it can only mean one of two things: either Walmart or the American economy is weaker than anyone thought.

“Walmart is a terrific retail operator… They didn’t suddenly become stupid,” says Howard Davidowitz, one of the top retail minds in the country. “The economy is in collapse. That’s what’s going on.”

Davidowitz points out that Walmart isn’t just a store for the downtrodden. They have 150 million customers which collectively spent less in Walmart stores than in the same period last year. Davidowitz says another 50 million customers shop at Target, which he also expects to have negative comp stores sales when it reports next week.

“I don’t think we’re in a recession right now, but I think there’s a 50 percent chance we’ll be in one next year,” Davidowitz shouts, and there’s nothing the government is going to be able to do about it. “We’ve spent all the money, we’ve borrowed all the money, and we’re in the tank.”

AHT/DB

…read more

Republished from: Press TV

Upper West Side condo has separate entrances for rich and poor

The poor will use a separate door under plans for a new Upper West Side luxury tower — where affordable housing will be segregated from ritzy waterfront condos despite being in the same building.

Manhattan developer Extell is seeking millions in air rights and tax breaks for building 55 low-income units at 40 Riverside Boulevard, but the company is sequestering the cash-poor tenants who make the lucrative incentives possible.

Five floors of affordable housing will face away from the Hudson River and have a separate entrance, elevator and maintenance company, while 219 market-rate condominiums will overlook the waterfront.

Extell broke ground on the building between West 61st and West 62nd streets last year as part of the 15-tower Riverside South residential complex stretching to West 72nd Street.

Now the company is applying for the city’s Inclusionary Housing Program, which gives developers more floor area in exchange for building on- or off-site affordable housing.

But instead of building a larger condo, Extell plans to sell the bonus floor area to another building within a half-mile of the site. Real-estate attorneys say such a sale could be worth millions.

Extell is also seeking a controversial 421a exemption — a tax break given to developers who include affordable housing in their market-rate buildings.

In October, The Post reported that five of the luxury firm’s towers cost the city $21.8 million in tax revenue in their first year alone.

Together, the buildings paid just $567,337 in annual taxes. Without the 421a program, they would have paid the city $22 million, according to appraisal firm Miller Samuel Inc.

Extell declined to comment.

A spokesman for the Department of Housing Preservation and Development said Extell’s application is still under review.

Assemblywoman Linda Rosenthal, a Democrat who represents the Upper West Side, told The Post that Extell’s plans “smack of classism,” and feared they could set a dangerous precedent for other developers.

“It’s a blatant attempt to segregate people,” fumed Rosenthal, who is demanding that HPD deny Extell’s request for tax breaks. “It’s just not a good thing for the city of New York to be supporting.”“I hate the visual of market-rate tenants going in one door and affordable tenants going in another, but that’s a visceral reaction,” Diller said.

Community Board Chair Mark Diller sent a letter to HPD last month asking for safeguards to protect low-income residents, who are relegated to floors two to six.

Under Extell’s plans for the low-income units, a studio will go for $845 a month, a one-bedroom for $908, and two-bedrooms for $1,099.

Households with incomes below 60 percent of the city’s area median income qualify for the units.

A family of four, for example, would need to make less than $51,540; an individual would need to earn less than $36,120.

Fat cats living in the condos will pay more than $1,000 per square foot. At The Aldyn, Extell’s 40-story luxury building next door, one-bedrooms sell for a whopping $1.3 million. A six-bedroom, eight-bath pad goes for $15.9 million.

Is The Wealth Effect In The US Already Tapering?

In his latest video update, Peter Schiff discussed three important

evolutions of this week. It gives an insight about the wealth effect,

particularly in the US. The wealth effect is undoubtedly very high on

the agenda of central planners.

Peter Schiff interprets this as a bad evolution. He thinks people are using debt to pay for necessities at grocery stores and gasoline stations, ending up with less purchasing power in total.

Moreover, the latest data show that 60% of home buyers are paying all cash. It can only be investors or speculators buying new homes; the average American can’t afford buying a new property by paying cash.

Data clearly point to a phony housing recovery. Peter Schiff concludes that the housing market is already tapering before Fed is tapering. The reasonable question to ask is what will happen when the speculators are going to unwind if the Fed starts the real taper? Who will be left buying when investors and speculators start selling?

Now the remarkable thing is that the Fed has only been talking about a slight easing of their asset purchases. They are not even talking about a significant taper or even about unwounding previous purchases.

1. Weak retail sales, increased credit card usage

Two retail chains (Macy’s and Walmart) came with lower than expected earnings. Those results came right after credit card companies announced better than expected earnings.Peter Schiff interprets this as a bad evolution. He thinks people are using debt to pay for necessities at grocery stores and gasoline stations, ending up with less purchasing power in total.

2. Phony housing recovery

The housing numbers came out a bit better than anticipated. But Peter Schiff points to the data “under the hood” which reveal a worse situation. It appears that the demand for rental units has increased which goes with a decrease in new mortgages. No coincidence that housing stocks have been among the weakest lately.Moreover, the latest data show that 60% of home buyers are paying all cash. It can only be investors or speculators buying new homes; the average American can’t afford buying a new property by paying cash.

Data clearly point to a phony housing recovery. Peter Schiff concludes that the housing market is already tapering before Fed is tapering. The reasonable question to ask is what will happen when the speculators are going to unwind if the Fed starts the real taper? Who will be left buying when investors and speculators start selling?

3. Consumer confidence is down

The latest consumer confidence figures from the Michigan University have dropped compared to the previous month. Consumers appear to be less confident. The most likely explanation is that they have only been hearing about an economic recovery, but they have not experienced it. At one point in time, the experience takes over expectations.The wealth effect already tapering

The above data show that the wealth effect is working in reverse already. Peter Schiff compares it with a “house of cards recovery” which is already collapsing before the real taper starts.Now the remarkable thing is that the Fed has only been talking about a slight easing of their asset purchases. They are not even talking about a significant taper or even about unwounding previous purchases.

The gold price rising

There was a lot of speculation by market watchers about the recent gold price rally. The real predicament, according to Schiff, is related to the failure of the latest bond auction. In fact, the bond auction saw its weakest demand since March 2009. On top of that, private investors from abroad (China, Singapore, etc) have been selling treasuries, according to recent data. So with less demand for bonds by the Fed and private investors abroad, it means that interest in the dollar is going down as well. That is what shapes the prospects for gold and explains recent price action.UK food bank inquiries up by 78%

UK food bank inquiries show a shocking rise of 78 percent in the last six months.

Republished from: Press TV

There has been an “alarming” 78 percent increase in the number of

food bank inquiries in Britain over the last six months, a charity says.

According to figures released by Citizens Advice, more Britons are asking for emergency food aid as poverty rises throughout the country.

The charity also warned that people in employment are seeking assistance with obtaining food for the first time.

Citizens Advice Chief executive Gillian Guy said the data showed that millions of British families were struggling with financial problems.

“The combined impact of welfare upheaval, cuts to public spending,

low wages and the high cost of living are putting unbearable pressure on

many households, forcing them to seek emergency help putting food on

the table,” Guy added.

The charity also identified the West Midlands as the worst affected area, with a 142 percent rise in food bank inquiries since February.

Earlier in April, the Trussell Trust, the largest food bank provider in the UK, said over 350,000 hungry Britons have turned to food banks last year, almost triple the number who has received food aid in 2011, due to the government’s welfare reforms

SSM/HE

…read more

According to figures released by Citizens Advice, more Britons are asking for emergency food aid as poverty rises throughout the country.

The charity also warned that people in employment are seeking assistance with obtaining food for the first time.

Citizens Advice Chief executive Gillian Guy said the data showed that millions of British families were struggling with financial problems.

The charity also identified the West Midlands as the worst affected area, with a 142 percent rise in food bank inquiries since February.

Earlier in April, the Trussell Trust, the largest food bank provider in the UK, said over 350,000 hungry Britons have turned to food banks last year, almost triple the number who has received food aid in 2011, due to the government’s welfare reforms

SSM/HE

Republished from: Press TV

Detroit: Government Chooses Big Banks Over the American People Once Again

Government Sides with the Big Banks Every Time

Ellen Brown noted recently that Detroit is yet another example of the government choosing big banks over the American people:The argument for the super-priority of derivative claims [background] is that nonpayment on these bets represents a “systemic risk” to the financial scheme. Derivative bets are cross-collateralized and are so inextricably entwined in a $600-plus trillion house of cards that the whole financial scheme could go down if the betting scheme were to collapse. Instead of banning or regulating this very risky casino, Congress has been persuaded by the masterminds of Wall Street that it needs to be preserved at all costs.The New York Times Editorial Board writes:

The same tortured logic has been used to justify the fact that the federal government deigned to bail out Wall Street but not Detroit. Supposedly, the mega-banks pose a systemic risk and Detroit doesn’t. On July 29th, former Obama administration economist Jared Bernstein pursued this line of reasoning on his blog, writing:

[T]he correct motivation for federal bailouts — meaning some combination of managing a bankruptcy, paying off creditors (though often with a haircut), or providing liquidity in cases where that’s the issue as opposed to insolvency – is systemic risk. The failure of large, major banks, two out of the big three auto companies, the secondary market for housing – all of these pose unacceptably large risks to global financial markets, and thus the global economy, to a major industry, including its upstream and downstream suppliers, and to the national housing sector. Because a) there’s not much of a case that Detroit is systemically connected in those ways, and b) Chapter 9 of the bankruptcy code appears to provide an adequate way for it to deal with its insolvency, I don’t think anything like a large scale bailout is forthcoming.

What we do have a problem with is shared sacrifice that does not seem to apply to the big banks that abetted Detroit’s descent into bankruptcy.Reuters adds some details:

Last month, just days before its bankruptcy filing, Detroit reached its first settlement with creditors. The settlement was with UBS and Bank of America, and though the precise terms will not be nailed down until the bankruptcy judge weighs in, Detroit is set to pay an estimated $250 million to terminate a soured derivatives transaction from 2005.

The derivatives, known as interest-rate swaps, were supposed to protect Detroit from rising interest payments on a chunk of its variable rate debt. The banks would pay Detroit if interest rates rose, and Detroit would pay the banks if rates fell. By 2009, both interest rates and the city’s credit rating were falling, forcing Detroit to pay the banks some $50 million a year and to pledge roughly $11 million a month in casino-tax revenue as additional collateral. [Background on how the big banks suckered Detroit]

***

But the haircut doesn’t mean that the banks will suffer. They have already made money on the swaps; the true extent of any discount will not be known until the deal is finalized.

This much is clear:

■ The banks’ 25 percent hit is nothing compared with the city’s suggested 90 percent cut to the pensions’ unfunded liability — which will result in benefit cuts that would be disastrous in both human and political terms and that the State of Michigan must prevent from happening.

■ Municipal officials are prey for Wall Street. The Dodd-Frank financial reform law called on regulators to establish “enhanced protection” for municipalities and other clients in their dealings with Wall Street, but the Securities and Exchange Commission has not yet completed rules, while the Commodity Futures Trading Commission’s rules are so weak as to virtually invite the banks to exploit municipalities.

■ The special treatment banks receive when debtors are in or near bankruptcy is unfair and economically destabilizing. Detroit’s agreement with the two banks requires court approval, but, in general, swap deals by banks are not subject to the constraints that normally apply in bankruptcy cases; in effect, the banks are paid first, even before other secured creditors and certainly before pensioners. That privilege, dating to the heyday of derivatives deregulation in the 1990s and 2000s, is destabilizing because the assurance of repayment fosters recklessness.

Detroit’s problems are a reminder of broader challenges, identified but still unmet: protecting pensions; protecting municipalities from Wall Street; and, at long last, revoking the obscene privileges of banks that allow them to prosper on the failings of others

The city is paying its swap counterparties a fixed interest rate of approximately 6 percent and receiving payments back of approximately 0.57 percent (current three month Libor ~0.27 percent + 0.30 percent = 0.57 percent for the floating rate). The city’s swap counterparties cannot take haircuts if bankruptcy is filed, according to a creditor attorney that I spoke to. In fact, they move to the head of the creditor line. The same part of the bankruptcy code that was used in the Lehman bankruptcy (Chapter 11) applies to Detroit (Chapter 9). Swaps are settled (netted and paid) when the entity enters the bankruptcy process. From the Stanford Law Review:The bigger pictures is that the government always chooses the big banks over the little guy:

Under the Bankruptcy Code, creditors of a failed entity are stayed or prohibited from seizing that entity’s assets. Since 1978, however, Congress has exempted derivatives counterparties from the automatic stay and permitted the termination of the derivatives contracts.Clearly Detroit’s derivative counterparties will siphon precious cash away from the insolvent city if it were to enter bankruptcy. This cash payment to swap counterparties could likely be in the $400 million range.

All of the top independent economists and financial experts (and many bankers) say that we’ve got to break up the big banks to save the economy.…read more

Instead, the government has thrown trillions at the big banks to artificially make them appear profitable.

The bailouts are continuing non-stop … to this very day (and see this).

Indeed, the government chose the big banks over Main Street, the average American … or the economy as a whole. And see this and this.

As such, the government has sucked trillions out of the real economy by pushing policies which destroy jobs (sorry … Obama doesn’t care), redistributed wealth upwards from the broad economy to a handful of the very richest (which trashes the economy .. and Obama is even worse than Bush), and destroyed savers and Main Street.

In other words, we have thrown many trillions of dollars at the banks, and then sucked trillions more out of the real economy.

As we noted recently:

The central banks’ central bank – the Bank for International Settlements- warned in 2008 that bailouts of the big banks would create sovereign debt crises … which could bankrupt nations.Given the above – and the fact that we no longer prosecute the big white collar criminals – we no longer have a free market economy … we have fascism, communist style socialism, kleptocracy, oligarchy or banana republic style corruption. As such, the machinery of capitalism – which could generate enough prosperity to dig us out of this budget deficit – has been broken.

That is exactly what has happened.

The big banks went bust, and so did the debtors. But the government chose to save the big banks instead of the little guy, thus allowing the banks to continue to try to wring every penny of debt out of debtors.

Treasury Secretary Paulson shoved bailouts down Congress’ throat by threatening martial law if the bailouts weren’t passed. And the bailouts are now perpetual.

Moreover:

The bailout money is just going to line the pockets of the wealthy, instead of helping to stabilize the economy or even the companies receiving the bailouts:Moreover, a large percentage of the bailouts went to foreign banks (and see this). And so did a huge portion of the money from quantitative easing. Indeed, the Fed bailed out Gaddafi’s Bank of Libya, hedge fund billionaires, and big companies, but turned its back on the little guy.

- A lot of the bailout money is going to the failing companies’ shareholders

- Indeed, a leading progressive economist says that the true purpose of the bank rescue plans is “a massive redistribution of wealth to the bank shareholders and their top executives”

And as the New York Times notes, “Tens of billions of [bailout] dollars have merely passed through A.I.G. to its derivatives trading partners”.

- The Treasury Department encouraged banks to use the bailout money to buy their competitors, and pushed through an amendment to the tax laws which rewards mergers in the banking industry (this has caused a lot of companies to bite off more than they can chew, destabilizing the acquiring companies)

***

In other words, through a little game-playing by the Fed, taxpayer money is going straight into the pockets of investors in AIG’s credit default swaps and is not even really stabilizing AIG.

A study of 124 banking crises by the International Monetary Fund found that propping up banks which are only pretending to be solvent often leads to austerity:

Existing empirical research has shown that providing assistance to banks and their borrowers can be counterproductive, resulting in increased losses to banks, which often abuse forbearance to take unproductive risks at government expense. The typical result of forbearance is a deeper hole in the net worth of banks, crippling tax burdens to finance bank bailouts, and even more severe credit supply contraction and economic decline than would have occurred in the absence of forbearance.

Cross-country analysis to date also shows that accommodative policy measures (such as substantial liquidity support, explicit government guarantee on financial institutions’ liabilities and forbearance from prudential regulations) tend to be fiscally costly and that these particular policies do not necessarily accelerate the speed of economic recovery.

***

All too often, central banks privilege stability over cost in the heat of the containment phase: if so, they may too liberally extend loans to an illiquid bank which is almost certain to prove insolvent anyway. Also, closure of a nonviable bank is often delayed for too long, even when there are clear signs of insolvency (Lindgren, 2003). Since bank closures face many obstacles, there is a tendency to rely instead on blanket government guarantees which, if the government’s fiscal and political position makes them credible, can work albeit at the cost of placing the burden on the budget, typically squeezing future provision of needed public services.In other words, the “stimulus” to the banks blows up the budget, “squeezing” public services through austerity.

Numerous top economists say that the bank bailouts are the largest robbery and redistribution of wealth in history.

Why was this illegal? Well, the top white collar fraud expert in the country says that the Bush and Obama administrations broke the law by failing to break up insolvent banks … instead of propping them up by bailing them out.

And the Special Inspector General of the Tarp bailout program said that the Treasury Secretary lied to Congress regarding some fundamental aspects of Tarp – like pretending that the banks were healthy, when they were totally insolvent. The Secretary also falsely told Congress that the bailouts would be used to dispose of toxic assets … but then used the money for something else entirely. Making false statements to a federal official is illegal, pursuant to 18 United States Code Section 1001.

Republished from: Global Research

Subscribe to:

Posts (Atom)