Hobby Lobby doesn’t want to cover its employees’ birth control on

company insurance plans. In fact, they’re so outraged about women

having access to birth control that they’ve taken the issue all the

way to the Supreme Court.

I cannot believe that we live in a world where we would even consider letting

some big corporation deny the women who work for it access

to the basic medical tests , treatments or prescriptions that they

need based on vague moral objections. But here’s the scary thing: With the judges we ‘ve got on the Supreme Court, Hobby Lobby might actually win.

The current Supreme Court has headed in a very scary direction.

Recently, three well-respected legal scholars examined almost 20,000

Supreme Court cases from the last 65 years. They found that the five

conservative justices currently sitting on the Supreme Court are in the

top 10 most pro-corporate justices in more than half a century.

And Justices Samuel Alito and John Roberts? They were number one and number two.

Take a look at the win rate of the national Chamber of Commerce cases

before the Supreme Court. According to the Constitutional

Accountability Center, the Chamber was winning 43% of the cases in

participated in during the later years of the Burger Court, but that

shifted to a 56% win-rate under the Rehnquist Court, and then a 70%

win-rate with the Roberts Court. Follow these pro-corporate trends to their logical

conclusion, and pretty soon you’ll have a Supreme Court that is a wholly

owned subsidiary of big business.

Birth control is at risk in today’s case, but we also need to worry about a lot more.

In Citizens United , the Supreme Court unleashed a wave of

corporate spending to game the political system and drown the voices of

middle class families.

And right now, the Supreme Court is considering McCutcheon v. FEC ,

a case that could mean the end of campaign contribution limits —

allowing the big guys to buy even more influence in Washington.

Republicans may prefer a rigged court that gives their corporate

friends and their armies of lawyers and lobbyists every advantage. But

that’s not the job of judges. Judges don’t sit on the bench to hand out

favors to their political friends.

On days like today, it matters who is sitting on the Supreme Court.

It matters that we have a President who appoints fair and impartial

judges to our courts, and it matters that we have a Senate who

approves them.

We ‘re in this fight because we believe that we don’t run this country for corporations – we run it for people. Elizabeth Warren was assistant to the president and a special

adviser to the Treasury secretary on the Consumer Financial Protection

Bureau.

According to new government figures just released today, autism in

the U.S. has increased by a whopping 30%

in just two years. The new estimate is that one in every 68 kids

in America falls somewhere on the autism spectrum now.

Health officials claim that this is not because more kids are

autistic these days, but that it is recognized

more even in kids with fewer symptoms:

Much of the increase is believed to be from a cultural

and medical shift, with doctors diagnosing autism more frequently,

especially in children with milder problems.

While that may account for the increase over the last two years,

can that explanation really account for the overall autism increase

trending over the last two decades?

The prevalence rate for autism before 1990 was only three

children per 10,000. When the CDC began surveillance of the study

population above in 2000,

figures clocked in at one child in every 150. Since then, autism

diagnoses have been steadily increasing each year.

One trend that has remained the same is the five times higher

prevalence of autism in boys, at one in every 42, over girls, at one

in every 189.

Some have pointed to a wealth

of studies that show possible correlation and causation of the

continued rise in autism to the continued increase in vaccines. The

U.S. currently has the most aggressive vaccination schedule of any

country on the planet. New

vaccinations have been steadily added to the average American

child’s vaccine schedule each decade for several decades now:

In the early 1950s, there were four vaccines: diphtheria,

tetanus, pertussis and smallpox. Because three of these vaccines were

combined into a single shot (DTP), children received five shots by

the time they were 2 years old and not more than one shot at a single

visit.

By the mid-1980s, there were seven vaccines: diphtheria,

tetanus, pertussis, measles, mumps, rubella and polio. Because six of

these vaccines were combined into two shots (DTP and MMR), and one,

the polio vaccine, was given by mouth, children still received five

shots by the time they were 2 years old and not more than one shot at

a single visit.

Since the mid-1980s, many vaccines have been added to the

schedule. Now, children could receive as many as 24 shots by 2 years

of age and five shots in a single visit.

Vaccines contain a vast array of potentially dangerous

ingredients, including antibiotics, formaldehyde, monosodium

glutamate (MSG), bovine fetal tissue, polysorbate and heavy metals

like aluminum and the mercury-containing preservative thimerosal.

When these are shot into the bloodstream, they bypass the majority of

the body’s natural immune system which resides in the gut.

A new study recently released by Scientists from the University of

California has put forth evidence

that autism actually begins in utero during pregnancy and it not the

result of a child’s environmental and social factors (such as

childhood vaccines):

“Building a baby’s brain during pregnancy involves

creating a cortex that contains six layers,” said Eric Courchesne,

neurosciences professor and director of the Autism Center of

Excellence at UCSD, in a statement.

“We discovered focal patches of disrupted development of these

cortical layers in the majority of children with autism.”

While many media outlets are saying this proves conclusively that

vaccinations aren’t causing autism (the story quoted above was

titled, “Autism Awareness: Disorder Begins Before Brain Is Fully

Developed, Making Risks From Vaccinations Impossible”), that’s

more media spin than reality.

In fact, this particular story goes on to contradict its own

title.

As the story

itself says:

But these trends aren’t reflected in other parts of the

world. Asia, Europe, and other parts of North America display far

lower prevalence rates, sometimes as low as one percent, which

presents U.S. researchers with a curious challenge. There are no

blood tests to diagnose autism, and behavioral observation is by

nature imperfect. Some say we over-diagnose, especially on the

higher-functioning end. Some say America’s obsession with

vaccinations is to blame. So the question remains: How do stop

something if we don’t fully know what it is?

And then:

This doesn’t rule out maternal exposure during

gestation or earlier, but it does go a long way toward

quieting many of today’s critics. [emphasis added]

Did you catch that?

Pregnant mothers are consistently told they need to get all kinds

of vaccines in the U.S., including flu

shots, one of the vaccines known to still contain thimerosal. How

can something be “impossible” if it hasn’t entirely been ruled

out?

The debate, then, rages on.

Delivered by The

Daily Sheeple

Students at London University’s prestigious King’s College have delivered a blow to Israel by voting to endorse the boycott, divestment and sanctions movement (BDS) against the world’s only apartheid state.

The motion, adopted on 25 March, was passed by 348 to 252 votes.

It calls for a thorough research into the college’s “investments,

partnerships, and contracted companies, including subcontractors, that

may be implicated in violating Palestinian human rights as stated by the

BDS movement”.

It also calls for pressure to be put on the college to divest from

companies found to be “directly or indirectly supporting the Israeli

occupation and apartheid policies”.

It also resolves

To have a plaque in all KCLSU [King’s College London

Students Union] student centres acknowledging that KCLSU formally

supported the BDS call, as was done when KCLSU showed solidarity to our

sisters and brothers in their struggle against Apartheid South Africa

with the following text: “KCLSU officially endorses the 2005 Palestinian

call for Boycott, Divestment, and Sanctions of Israel until it abides

by international law and ends it illegal occupation of Palestine. KCLSU

is proud to follow the example of a similar call in the 1980’s, which

successfully led to the end of apartheid in South Africa.”

And it resolved to raise awareness of Israel’s apartheid policies and

its illegal occupation by “helping KCL Action Palestine Society with

printing materials and diffusion of important events such as the

international ‘Israeli Apartheid Week’ through the KCLSU website and

social media”.

Well done, King’s College students, for hammering another nail into the coffin of injustice and criminality.

David Lennox, Resources Analyst at Fat Prophets, says lingering issues of a budget deficit and a debt situation in the U.S. could lift gold prices higher

Are

you ready for some inspirational stories that will make your heart

jump for joy? These days, it is so easy to get down. Both

individually and as a nation, we have so many problems and it often

seems likethings

just keep getting worse. For example, this week we learned

that pending home sales in the United States just droppedby

the most in 3 years and that they have now been declining

for 8 months in a row. And without a doubt, incredibly

challenging times are on the horizon. In response, a lot of

people are going to choose to complain bitterly and curse the

darkness. Others are going to respond with fear and will try to

hide from the world as much as they can. But I don’t think

that either of those approaches is a good way to react to the

problems that we will be facing. Rather, I believe that the

right choice is to be a light in the darkness and to try to make a

difference. As you will see below, there are many ways that

this can be done. You don’t have to be famous, or run for

political office, or have a million dollars. All that it takes

is a willingness to reach out and love the one in front of you.

If all of us decided to do what we could to truly make a difference

in the life of one other person, our nation would be a far better

place. The following are 5 people who made a conscious decision

to shine a light in the darkness…

Kelly

Nixon Mayr

It

takes a lot of love and compassion to adopt a child into your own

home. When that child has special needs, it can be especially

challenging. That is why the story of Kelly Nixon Mayr is so

inspiring. Along with her husband, she has made a lifestyle out

of helping children with special needs…

Kelly Nixon

Mayr of Colorado has birthed five children, adopted one troubled teen

and fostered several

special-needs infants. On Tuesday, she and husband Paul announced,

through their family blog,

that they had finalized their adoption of Angie, a 2-year-old who was

born drug-exposed and clubfooted, whom they had fostered on and off

since she was 1.

Now they are preparing for their next

adoption—of Rita, an 8-year-old Eastern European orphan with

arthrogryposis (a rare syndrome causing unbendable joints) and a case

of post-traumatic stress disorder.

But Nixon Mayr, 45, who speaks about her

close-knit brood with equal parts passion and humor, insists that she

and her husband are not extraordinary.

“I yell at my kids, and I think one might

have had Goldfish for breakfast the other day,” she tells Yahoo

Shine with a laugh. “The only thing we are is willing.”

It takes a lot of money to raise those

children. Kelly and her husband could have used that money on a

larger house, luxury cars and expensive vacations. But instead,

they willingly chose to live their lives in service to others.

Rahat

Younger

Americans are capable of feats of great compassion as well. For

example, a YouTube personality known as “Rahat” could have easily

ignored the homeless man that he would often see at the local

shopping mall. But instead, he

decided to do something about it…

On March 4, a YouTube magician and prankster

name Rahat set aside his mischievous pranks to do something really

kind for a homeless man he’d often seen hanging around his shopping

mall.

He heard that the man named Eric was a “nice

and respectable guy,” so he gave him a lottery ticket telling him

it was a winner and that he should come to the shop and claim his

prize. The store clerk was privy to the stunt and pretended the

ticket was indeed a winner and handed over $1,000 in cash to the

homeless gentleman.

Rahat, who had secretly given the clerk the

cash to give to Eric recorded a video of how excited Eric was to

“win” the money.

And

thanks to Rahat’s YouTube video and fundraising efforts, a total

of$42,000 has

been raised for that homeless man, and his future is looking bright

for the first time in a very long while.

Annie

Hart

Sometimes it is an animal that desperately

needs some love and compassion. In this economic environment,

there are a lot of people that are abandoning their pets, and there

are a lot of homeless dogs and cats that are in a tremendous amount

of pain right now.

That

is why what people like Annie Hart are doing is

so wonderful…

When Annie Hart rescued a sick, homeless pit

bull, not even she could have predicted the miraculous transformation

the animal would undergo.

Hart is the

executive director of the

Bill Foundationand is no stranger to rescuing animals.

She ended up naming the pit bull Gideon. The

dog was in such bad shape that he actually trembled at the sight of

humans.

Doctors also discovered that Gideon was

suffering from multiple severe bacterial and highly contagious fungal

infections. He was put in quarantine.

As

you watch the video of the transformation of this dog that

I have posted below, you might just find yourself getting choked

up over it…

Mark

A. Mayo

How many of you would be willing to give your

life so that someone else could live?

That

is precisely what Master-at-Arms 2nd Class Mark A. Mayo recently

did. It is this kind of heroism that America desperately

needs more of…

Master-at-Arms 2nd Class Mark A. Mayo, 24, was

killed during a shooting incident at Naval Station Norfolk Monday.

Mayo was assigned to Naval Security Forces, Naval Station Norfolk.

Norfolk Naval Base commander Robert Clark said

the young sailor sacrificed himself to save others.

“It was incredibly extraordinary,”

says Clark.

The shooting happened around 11:20pm Monday

night at Pier 1 onboard the USS Mahan.

Mark Mayo was protecting a sailor who first

confronted a civilian intruder. That man, a truck driver, tried to

board the destroyer Mahan. He disarmed the watch stander and then

turned the watch stander’s gun at Mayo.

“He jumped into the way between the gunman

and the petty officer of the watch. She fell to the ground. He

covered her and he basically gave his life for hers,” says Clark.

“Doing that, that’s something he would do,”

says Virgil Savage, a fellow sailor and close friend of Mayo. “He

always stood up for the little guy.”

You

can read more about Mayo’s incredible act of bravery right

here.

Dan

And Linda Catlin

It takes a very special individual to commit

your entire life to serving the homeless.

But that is exactly what Pastor Dan Catlin and

his wife Linda have been doing for many years.

The

following is an excerpt from a profile of the Messiah’s Branch

homeless ministry in Wichita, Kansas that was written by

Jessiqua Wittman…

Messiah’s

Branch is a family-owned homeless ministry. Since the year

2000, Dan and Linda Catlin have been traveling an hour, at least

twice a week, to help the homeless in the city of Wichita, Kansas.

When I was a teenager (before we were homeless

ourselves), my family had the privilege of working with this family.

We’d arrive at the mission building (a

renovated bar), around 12:30 on Tuesdays and Fridays. The homeless

people of the city, usually about 50 to 70 of them, would already be

trickling into the area. There are a lot more homeless people than

that in Wichita. Those were just the people from the surrounding area

that could walk there, and had no other ministry that they could go

for food. Most churches (besides Messiah’s Branch) require

identification before they feed people off the street, and oftentimes

homeless people have lost their identification long ago, whether

because of drugs, mugging, or police raids (many of the police in

Wichita are very hostile towards homeless people).

When you serve the homeless, there are no

vacations. It is just a relentless battle against human pain

and suffering. To do this year after year, you have got to be

driven by compassion…

Sister

Linda can hold a knife and cut a potato at the same time, in the same

hand! The

whole time seasoning her stew and chatting and laughing with a young

homeless couple that are hanging around the kitchen door, hungry for

more than just food.

And Pastor Dan? What does he do? He takes some

people to doctor’s appointments, some to the hospital. Sometimes he

buys shoes, or makes sure they find a coat that will fit just right.

The way I remember him most is being the resident jar-opener.

In the wintertime, when it reaches a certain

temperature, Pastor Dan and Sister Linda open up the building full

time. There are so many people that come, they lay them all

side-by-side in rows on the floor. For a week sometimes, it’s like

this.

I have personally talked to Pastor Dan and I

know how hard he has worked to help the homeless of Wichita for so

many years.

We are going to need a lot more people like the

ones you just read about above.

And you don’t have to do exactly what they

are doing. Find your own way to make a difference. We all

have different gifts, and together we can make this country a better

place.

So make a conscious decision to shine a light

in the darkness.

Charles and David Koch should not be blamed for having more wealth

than the bottom 40 percent of Americans put together. Nor should they be

condemned for their petrochemical empire. As far as I know, they’ve

played by the rules and obeyed the laws.

They’re also entitled to their own right-wing political views. It’s a free country.

But in using their vast wealth to change those rules and laws in

order to fit their political views, the Koch brothers are undermining

our democracy. That’s a betrayal of the most precious thing Americans

share.

The Kochs exemplify a new reality that strikes at the heart of America.

The vast wealth that has accumulated at the top of the American economy

is not itself the problem. The problem is that political power tends to

rise to where the money is. And this combination of great wealth with

political power leads to greater and greater accumulations and

concentrations of both — tilting the playing field in favor of the Kochs

and their ilk, and against the rest of us.

America is not yet an oligarchy, but that’s where the Koch’s and a few other billionaires are taking us.

American democracy used to depend on political parties that more or

less represented most of us. Political scientists of the 1950s and 1960s

marveled at American “pluralism,” by which they meant the capacities of

parties and other membership groups to reflect the preferences of the

vast majority of citizens.

Then around a quarter century ago, as income and wealth began

concentrating at the top, the Republican and Democratic Parties started

to morph into mechanisms for extracting money, mostly from wealthy

people.

Finally, after the Supreme Court’s “Citizen’s United” decision in

2010, billionaires began creating their own political mechanisms,

separate from the political parties. They started providing big money

directly to political candidates of their choice, and creating their own

media campaigns to sway public opinion toward their own views.

So far in the 2014 election cycle, “Americans for Prosperity,” the

Koch brother’s political front group, has aired more than 17,000

broadcast TV commercials, compared with only 2,100 aired by Republican

Party groups.

“Americans for Prosperity” has also been outspending top Democratic

super PACs in nearly all of the Senate races Republicans are targeting

this year. In seven of the nine races the difference in total spending

is at least two-to-one and Democratic super PACs have had virtually no air presence in five of the nine states.

The Kochs have spawned several imitators. Through the end of

February, four of the top five contributors to 2014 super-PACs are now

giving money to political operations they themselves created, according

to the Center for Responsive Politics.

For example, billionaire TD Ameritrade founder Joe Ricketts and his

son, Todd, co-owner of the Chicago Cubs, have their own $25 million

political operation called “Ending Spending.” The group is now investing

heavily in TV ads against Republican Representative Walter Jones in a

North Carolina primary (they blame Jones for too often voting with Obama).

Their ad attacking Democratic New Hampshire Senator Jeanne Shaheen for supporting Obama’s

health-care law has become a template for similar ads funded by the

Koch’s “Americans for Prosperity” in Senate races across the country.

When billionaires supplant political parties, candidates are beholden

directly to the billionaires. And if and when those candidates win

election, the billionaires will be completely in charge.

At this very moment, Casino magnate Sheldon Adelson (worth an

estimated $37.9 billion) is busy interviewing potential Republican

candidates whom he might fund, in what’s being called the “Sheldon

Primary.”

“Certainly the ‘Sheldon Primary’ is an important primary for any Republican running for president,” says Ari Fleischer, former White House

press secretary under President George W. Bush. “It goes without saying

that anybody running for the Republican nomination would want to have

Sheldon at his side.”

The new billionaire political bosses aren’t limited to Republicans.

Democratic-leaning billionaires Tom Steyer, a former hedge-fund manager,

and former New York Mayor Michael Bloomberg, have also created their

own political groups. But even if the two sides were equal, billionaires

squaring off against each other isn’t remotely a democracy.

In his much-talked-about new book, “Capital in the Twenty-First

Century,” economist Thomas Piketty explains why the rich have become

steadily richer while the share of national income going to wages

continues to drop. He shows that when wealth is concentrated in

relatively few hands, and the income generated by that wealth grows more

rapidly than the overall economy – as has been the case in the United

States and many other advanced economies for years – the richest receive

almost all the income growth.

Logically, this leads to greater and greater concentrations of income

and wealth in the future – dynastic fortunes that are handed down from

generation to generation, as they were prior to the twentieth century in

much of the world.

The trend was reversed temporarily in the twentieth century by the

Great Depression, two terrible wars, the development of the modern

welfare state, and strong labor unions. But Piketty is justifiably

concerned about the future.

A new gilded age is starting to look a lot like the old one. The only

way to stop this is through concerted political action. Yet the only

large-scale political action we’re witnessing is that of Charles and

David Koch, and their billionaire imitators.

Robert B. Reich has served in three national administrations,

most recently as secretary of labor under President Bill Clinton. He

also served on President Obama‘s transition advisory board. His latest book is “Aftershock: The Next Economy and America‘s Future.” His homepage is www.robertreich.org.

Ann

Barnhardt, founder of Barnhardt Capital Management, exposes the real

and hidden risks lurking in almost all of the usual places you might be

tempted to stash your nestegg. Ann then describes ways to protect your

family and switch to a safer and sustainable course for your future.

Are Your Savings Safe in:

===================

Bank Savings Account?

Money Markey Fund?

FDIC/FSLIC Insurance?

Stocks or Bonds in a Brokerage Account?

Insurance?

Cash?

GLD or SLV Gold and Silver funds?

IRA?

401-K?

Social Security?

MyRA Account?

US Savings Bonds / Treasury Bonds?

BitCoin?

DISCLAIMER: The financial and

political opinions expressed in this interview are those of the guest

and not necessarily of “Finance and Liberty” or its staff.

Benihana restaurant founder Rocky Aoki was indicted by a federal

grand jury yesterday on charges he cooked up an insider trading scheme

that netted him $590,000.

Aoki, 59, resigned last month as chairman and chief executive of

Benihana, a 61-restaurant Japanese steakhouse chain based in Miami after

being informed he was the subject of a federal securities

investigation.

According to federal prosecutors, Aoki bought 200,000 shares of

Spectrum Information Technologies in September and October 1993 after

learning that the company was about to hire then Apple Computer chairman

John Sculley.

The colorful Aoki a former Olympic wrester and successful balloonist

paid between $4.

90 and $6.

60 per share.

He then sold his stock for $11 a share, earning a profit of $590,000,

after Sculley's appointment was announced soon after.

The stock rose 46% the day of the announcement.

Prosecutors said Aoki was tipped off about Sculley's negotations with

Spectrum from public relations consultant Donald Kessler.

Kessler, who was later paid $10,000 by Aoki, pleaded guilty last

December to participating in an insider trading scheme and is

cooperating with the government.

Kessler's guilty plea last Dec. 30 was part of a larger case of

securities fraud and tax evasion.

In the case, Kessler is described as a "self-employed stock promoter

who earned fees from companies primarily by arranging for them to be

mentioned publicly and in print by a prominent business journalist.

"

While the journalist was not identified in the indictment,

BusinessWeek had previously identified him as Dan Dorfman, a long-time

business columnist who made daily appearances on CNBC and wrote for

Money Magazine and USA Today. Citing health problems, Dorfman left CNBC.

Money fired him.

The restaurateur will be arraigned tomorrow. Indicted on one count of

conspiracy and six counts of insider trading, he faces up to five years

in prison and $250,000 in fines on each count.

"This indictment," said U.

S. Attorney Zachary Carter,

"demonstrates this office's zero tolerance for violations of the

securities laws and its commitment to protecting the investing public.

"

Aoki's attorney, Martin Auerbach, said his client intends to plead not guilty and "respond to the charges in court.

"

Aoki has long led a flamboyant life.

In 1981, he was part of a crew that became the first to fly a gas balloon across the Pacific Ocean.

Aoki is currently said to be working with Drezel Aqua Technologies to salvage a ship that sank off Ocean City, N.

J., in 1901.

Must be the weather... (though if you want to believe that, do not look at the regional breakdowns)... Pending home sales fell 10.2% YoY -

the worst in 3 years (notably worse than the 9% drop expected by the

meteorologists in the economics departments of the big banks). This is

the 8th month in a row of home sales drops (pre-weather).

Don;t worry though - a glimpse at the charts shows things are stabilizing as NAR's Larry Yun suggests..

Lawrence Yun, NAR chief economist, said the recent slowdown in home sales may be behind us, while home prices continue to rise. “Contract signings for the past three months have been little changed, implying the market appears to be stabilizing,” he said. “Moreover, buyer traffic information from our monthly Realtor® survey shows a modest turnaround, and some weather delayed transactions should close in the spring.”

Citigroup Inc.’s capital plan was among five that failed Federal Reserve stress tests, while Bank of America Corp. (BAC) won approval for its first dividend increase since the financial crisis.

Lenders

announced more than $60 billion of dividends and stock buybacks after

the Fed approved capital plans for 25 of the 30 banks in its annual

exam. Citigroup, as well as U.S. units of Royal Bank of Scotland Group

Plc, HSBC Holdings Plc and Banco Santander SA (SAN), failed because of concerns about the quality of their processes, the central bank said yesterday in a statement. Zions Bancorporation failed after its capital fell below Fed minimums in a simulation of a severe economic slump.

The

results show lenders may still face obstacles to boosting dividends and

buybacks even as regulators say the firms have doubled their capital

since the first public stress test in 2009. The Fed is increasing

scrutiny of the industry’s controls and planning processes as concerns

about capital levels wane.

“Things are improving and the banking industry has turned a corner;

it just might not be as far along as the market would like,” said Joseph

Vitale, a partner at law firm Schulte Roth & Zabel LLP who

represents financial firms. “You’ve still got some time to go before the

regulators see things as business-as-usual again.”

Photographer: Craig Warga/Bloomberg

A customer uses an automated teller machine (ATM) inside of a Citibank bank branch on... Read More

Higher payouts may help bank stocks continue their recent rally. The KBW Bank Index (BKX) of 24 lenders advanced 4 percent this year through yesterday, compared with the 0.2 percent gain for the Standard & Poor’s 500 (SPX), and the KBW benchmark beat the broader measure in three of the past four years.

Bigger Payout

Banks

in this year’s test collectively received approval to pay out about 60

percent of their estimated net income during the next four quarters,

according to a Fed official. That ratio is closer to the 69 percent that

lenders were returning to shareholders in 2005 before the crisis,

according to data from Bloomberg Industries. Citigroup (C)

was denied in its attempt to quintuple its quarterly dividend to 5

cents and put in place a $6.4 billion buyback. Bank of America and

Goldman Sachs Group Inc. each had to cut their planned capital return to

gain approval.

Citigroup, which last year asked for the least

capital return among the five largest U.S. banks, would have passed this

year’s test on quantitative grounds alone. It had a 6.5 percent Tier 1

common ratio, above the Fed’s 5 percent minimum.

Multiple Defects

The

central bank found defects in Citigroup’s planning practices that

included areas the Fed flagged before. The regulator expressed concern

with the New York-based company’s ability to project losses in “material

parts of its global operations” and to reflect all business exposures

in its internal stress test.

“Taken in isolation, each of the

deficiencies would not have been deemed critical enough to warrant an

objection, but when viewed together, they raise sufficient concerns

regarding the overall reliability of Citigroup’s capital planning

process,” the Fed said of the third-largest U.S. bank. Michael Corbat,

the bank’s chief executive officer, said in a statement that Citigroup

is “deeply disappointed” by the rejection and will “work closely with

the Fed to better understand their concerns so that we can bring our

capital planning process in line with their expectations.” The timing of

any resubmission hasn’t been decided, he said.

Mexico Fraud

The

Fed made no mention of the bank’s discovery of a $400 million loan

fraud last month at its Mexico unit, which had stirred speculation that

regulators might fault Citigroup’s controls. Corbat has vowed that the

people involved will be held accountable.

Citigroup shares

fell the most in more than a year, sliding 5.7 percent to $47.28 at

12:22 p.m. in New York. Analysts from Stifel Financial Corp.’s KBW unit

and Sanford C. Bernstein & Co. downgraded the stock today, while

Mike Mayo at CLSA Ltd. said the company should increase its pace of

restructuring.

“The Federal Reserve’s surprise qualitative

rejection of Citigroup’s capital plan raises questions about the

company’s relationship with its regulators and the necessary next steps

and timing to restore confidence,” Bernstein’s John McDonald wrote in a note cutting his rating to market perform.

Rejected Again

It’s

the second time the Fed has failed one of Citigroup’s capital plans.

The last rejection came in 2012, when Vikram Pandit was the CEO, and the

defeat played a role in Pandit’s ouster later that year, a person with

knowledge of the board’s discussions said at the time.

“It came as a surprise,” said Michael Scanlon, managing director at Manulife Asset Management in Boston,

who helps oversee $3 billion, including shares of Citigroup. “It can be

a significant ding to confidence when these companies have failed in

the past. Sometimes it’s short-lived and they resolve the issues,

resubmit and move forward, and ultimately that is what Citigroup is

going to have to do.”

Two of the main gauges in the Fed’s test were the Tier 1 common ratio and the leverage ratio. The first measures a bank’s core equity, made up of common shares and retained earnings, divided by its total assets

adjusted for risk using global banking guidelines. The leverage ratio

makes no distinction among risks and is considered a stricter standard

by some regulators.

Second Chance

Bank of America

and Goldman Sachs each saw their Tier 1 leverage ratios drop to 3.9

percent in their original capital plans, below the required 4 percent.

Both firms lowered their requests and were approved, meaning they don’t

have to resubmit.

The two firms asked for too much in buybacks

and dividends after their own internal stress tests showed better

performance than in the central bank’s exam. New York-based Goldman

Sachs predicted its Tier 1 common ratio would be about 3.8 percentage

points stronger than the Fed estimated in a worst-case scenario. The gap

for Bank of America was 2.7 percentage points.

Bank of America,

ranked second by assets, raised its quarterly payout to 5 cents from 1

cent after the Fed’s decision and authorized a $4 billion stock buyback.

The increase is a victory for CEO Brian T. Moynihan, who has pressed to raise the payout from the token level that prevailed since the financial crisis.

The

Fed blocked plans in 2011 for an increase by the Charlotte, North

Carolina-based company, which didn’t ask for anything the following year

and won permission for a $5 billion stock buyback last year.

Loss Tally

Goldman

Sachs said yesterday that its capital plan “provides flexibility,”

without saying what it seeks to pay out to shareholders.

Projected

losses for the 30 banks under a scenario of deep recession would total

$366 billion over nine quarters, the Fed said last week. The aggregate

Tier 1 common capital ratio would fall from an actual 11.5 percent in

the third quarter of 2013 to a minimum of 7.6 percent, before accounting

for capital plans.

“The banking system is much better

capitalized at this point in time compared to where it was in 2009,”

Sameer Gokhale, an analyst at Janney Montgomery Scott LLC, said in a

Bloomberg Television interview with Carol Massar. “The risk that you see large-scale bank failures has diminished significantly.” JPMorgan Chase & Co. (JPM),

the biggest U.S. lender by assets, had its capital plan ratified as it

maintained a Tier 1 common ratio of 5.5 percent, a half a percentage

point above the minimum. Last year, approval for the New York-based bank

came with an order to resubmit the plan to fix qualitative weaknesses.

The quarterly dividend will rise to 40 cents a share from 38 cents, and

the company authorized a $6.5 billion stock buyback, according to a bank

statement.

Wells Fargo

The Tier 1 common ratio at Wells Fargo & Co., the biggest U.S. home lender, was 6.1 percent and Morgan Stanley (MS)’s

was 5.9 percent. Wells Fargo boosted its dividend 5 cents to 35 cents a

quarter. Morgan Stanley doubled its quarterly payout to 10 cents and announced a $1 billion buyback.

Zions,

the Salt Lake City-based bank that had a 4.4 percent Tier 1 common

ratio in the test, said before yesterday’s results were announced that

it planned to resubmit its capital plan.

The Fed broke new

ground on governance and transparency on this round of tests. For the

first time, the board held a vote on the qualitative objections that

resulted in a 4-0 approval, with Fed Governor Sarah Bloom Raskin

abstaining. Raskin was confirmed by the U.S. Senate as deputy Treasury secretary on March 12.

Detailed Objections

The

board’s descriptions of its qualitative objections were also more

detailed than before. In their remarks on Santander Holdings USA, for

example, they cited “specific deficiencies” including governance,

internal controls and risk management in capital planning.

The

central bank also faulted HSBC North America Holdings Inc. and RBS

Citizens Financial Group Inc. for estimates of revenue and losses in the

test. The rejection means the lenders won’t be able to increase

dividends to their European parent companies, freezing them at current

levels, according to a Fed official.

The dividend raises will

boost yields closer to the norms that prevailed before the financial

crisis, when the stocks were favored by income-oriented investors. The

average yield for the 24 companies in the KBW Bank Index stood at 4.9

percent at the end of 2007. It’s now under 2 percent.

Higher Yields

The $60 billion of payouts includes dividends that were already being paid in addition to increases and new repurchase plans.

JPMorgan’s

increase boosted its yield to about 2.7 percent annually based on

yesterday’s close. Its payout ratio -- dividends plus buybacks -- equals

about 56 percent of earnings over the next four quarters, according to

figures from the banks and KBW estimates. That’s up from 48 percent in

the last four quarters, said KBW, which made its estimates before

stress-test results were announced.

Bank of America’s payout

ratio climbed to about 39 percent from 34 percent, bringing the dividend

yield to 1.2 percent. U.S. Bancorp’s payout jumped to about 70 percent

from 59 percent, and the yield would be 2.3 percent.

SunTrust

Banks Inc. doubled its dividend yield to 2 percent, according to data

compiled by Bloomberg. Discover Financial Services boosted its yield to

1.7 percent from 1.4 percent and American Express Co.’s climbed to 1.2

percent from 1 percent.

The leaders of the U.S. Senate Banking Committee, Sen. Tim Johnson

(D., S.D.) and Sen. Mike Crapo (R., Idaho), released a draft bill on

Sunday that would provide explicit government guarantees on

mortgage-backed securities (MBS) generated by privately-owned banks and

financial institutions. The gigantic giveaway to Wall Street would put

US taxpayers on the hook for 90 percent of the losses on toxic MBS the

likes of which crashed the financial system in 2008 plunging the economy

into the deepest slump since the Great Depression. Proponents of the

bill say that new rules by the Consumer Financial Protection Bureau

(CFPB) –which set standards for a “qualified mortgage” (QM)– assure that

borrowers will be able to repay their loans thus reducing the chances

of a similar meltdown in the future. However, those QE rules were

largely shaped by lobbyists and attorneys from the banking industry who

eviscerated strict underwriting requirements– like high FICO scores and

20 percent down payments– in order to lend freely to borrowers who may

be less able to repay their loans. Additionally, a particularly lethal

clause has been inserted into the bill that would provide blanket

coverage for all MBS (whether they met the CFPB’s QE standard or not)

in the event of another financial crisis. Here’s the paragraph:

“Sec.305. Authority to protect taxpayers in unusual and exigent market conditions….

If the Corporation, the Chairman of the Federal Reserve Board of

Governors and the Secretary of the Treasury, in consultation with the

Secretary of Housing and Urban Development, determine that unusual and

exigent circumstances threaten mortgage credit availability within the

U.S. housing market, FMIC may provide insurance on covered securities

that do not meet the requirements under section 302 including those for

first loss position of private market holders.” (“Freddie And Fannie

Reform – The Monster Has Arrived”, Zero Hedge)

In other words, if the bill passes, US taxpayers will be

responsible for any and all bailouts deemed necessary by the regulators

mentioned above. And, since all of those regulators are in Wall

Street’s hip-pocket, there’s no question what they’ll do when the time

comes. They’ll bailout they’re fatcat buddies and dump the losses on

John Q. Public.

If you can’t believe what you are reading or if you think that the

system is so thoroughly corrupt it can’t be fixed; you’re not alone.

This latest outrage just confirms that the Congress, the executive and

all the chief regulators are mere marionettes performing whatever task

is asked of them by their Wall Street paymasters.

The stated goal of the Johnson-Crapo bill is to “overhaul” mortgage

giants Fannie Mae and Freddie Mac so that “private capital can play the

central role in home finance.” (That’s how Barack Obama summed it up.)

Of course, that’s not really the purpose at all. The real objective is

to hand over the profit-generating mechanism to the private banks

(Fannie and Freddie have been raking in the dough for the last three

years) while the red ink is passed on to the public. That’s what’s

really going on.

According to the Wall Street Journal, the bill will

“construct an elaborate new platform by which a number of

private-sector entities, together with a privately held but federally

regulated utility, would replace key roles long played by Fannie and

Freddie….”

“The legislation replaces the mortgage-finance giants with a new

system in which the government would continue to play a potentially

significant role insuring U.S. home loans.” (“Plan for Mortgage Giants

Takes Shape”, Wall Street Journal)

“Significant role”? What significant role? (Here’s where it gets interesting.)

The WSJ:

“The Senate bill would repurpose the firms’ existing

regulator as a new “Federal Mortgage Insurance Corp.” and charge the

agency with approving new firms to pool loans into securities. Those

firms could then purchase federal insurance to guarantee payments to

investors in those bonds. The FMIC would insure mortgage bonds much the

way the Federal Deposit Insurance Corp. provides bank-deposit

insurance.”

Unbelievable. So they want to turn F and F into an insurance company

that backs up the garbage mortgages created by the same banks that just

ripped us all off for trillions of dollars on the same freaking swindle?

You can’t be serious?

More from the WSJ: “Mortgage guarantors would be required to

maintain a 10% capital buffer against losses and to have that capital

extinguished before the federal insurance would be triggered.” 10 percent? What the hell difference does 10 percent make;

that’s a drop in the bucket. If the banks are going to issue mortgages

to people who can’t repay the debt, then they need to cover the damn

losses themselves, otherwise they shouldn’t be in the banking biz to

begin with, right?

This is such an outrageous, in-your-face ripoff, it shouldn’t even

require a response. These jokers should be laughed out of the senate.

All the same, the bill is moving forward, and President Twoface has

thrown his weigh behind it. Is there sort of illicit, under-the-table,

villainous activity this man won’t support?

Not when it comes to his big bank buddies, there isn’t. Now check out

this clip from an article by economist Dean Baker. Baker refers to the

Corker-Warner bill, but the Crapo-Johnson fiasco is roughly the same

deal. Here’s Baker:

“The Corker-Warner bill does much more than just

eliminate Fannie and Freddie. In their place, it would establish a

system whereby private financial institutions could issue

mortgage-backed securities (MBS) that carry a government guarantee. In

the event that a large number of mortgages in the MBS went bad, the

investors would be on the hook for losses up to 10 percent of its value,

after that point the government gets the tab.

If you think that sounds like a reasonable system, then

you must not have been around during the housing crash and ensuing

financial crisis. At the peak of the crisis in 2008-2009 the worst

subprime MBS were selling at 30-40 cents on the dollar. This means the

government would have been picking up a large tab under the

Corker-Warner system, even if investors had been forced to eat a loss

equal to 10 percent of the MBS price.

The pre-crisis financial structure gave banks an enormous incentive

to package low quality and even fraudulent mortgages into MBS. The

system laid out in the Corker-Warner bill would make these incentives

even larger. The biggest difference is that now the banks can tell

investors that their MBS come with a government guarantee, so that they

most they stand to lose is 10 percent of the purchase price.” (“The

disastrous idea for privatizing Fannie and Freddie”, Dean Baker, Al

Jazeera)

Just ponder that last part for a minute: “The bill would make these incentives even larger.”

Do you really think we should create bigger incentives for these

dirtbags to rip us off? Does that make sense to you? Here’s more from

Baker:

“The changes in financial regulation are also unlikely to

provide much protection. In the immediate wake of the crisis there were

demands securitizers keep a substantial stake in the mortgages they put

into their pools, to ensure that they had an incentive to only

securitize good mortgages. Some reformers were demanding as much as a 20

percent stake in every mortgage.

Over the course of the debate on the Dodd-Frank bill and subsequent

rules writing this stake got ever smaller. Instead of being 20 percent,

it was decided that securitizers only had to keep a 5 percent stake. And

for mortgages meeting certain standards they wouldn’t have to keep any

stake at all.

Originally only mortgages in which the homeowner had a down payment

of 20 percent or more passed this good mortgage standard. That cutoff

got lowered to 10 percent and then was lowered further to 5 percent.

Even though mortgages with just 5 percent down are four times as likely

to default as mortgages with 20 percent or more down, securitizers will

not be required to keep any stake in them when they put them into a

MBS.”

Hold on there, Dean. You mean Dodd Frank didn’t ”put things right”?

What the heck? I thought that “tough new regulations” assured us that

the banks wouldn’t blow up the system again in five years or so. Was

that all baloney?

Yep, sure was. 100% baloney. Once the banks unleashed their army of

attorneys and lobbyists on Capital Hill, new regulations didn’t stand a

chance. They turned Dodd Frank into mincemeat and now we’re back to

square one.

And don’t expect the ratings agencies to help out either because

they’re in the same shape they were before the crash. No changes at all.

They still get paid by the guys who issue the mortgage-backed

securities (MBS) which is about the same as if you paid the salary of

the guy who grades your midterm exam. Do you think that might cloud his

judgment a bit? You’re damn right, it would; just like paying the

ratings agencies guarantees you’ll get the rating you want. The whole

system sucks.

And as far as the new Consumer Financial Protection Bureau, well, you

guessed it. The banks played a role in drafting the new “Qualified

Mortgage” standard too, which is really no standard at all, since no

self-respecting lender would ever use the same criteria for issuing a

loan or mortgage. For example, no banker is going to say, “Heck, Josh,

we don’t need your credit scores. We don’t need a down-payment. We’re

all friends here, right? So, how much do you need for that mortgage old

buddy, $300,000, $400,000, $500,000. You name it. The sky’s the limit.”

No down payment? No credit scores? And they have the audacity to call this a qualified mortgage?

Qualified for what? Qualified for sticking it to the taxpayers? The

real purpose of the qualified mortgage is to protect the banks from

their own shifty deals. That’s what it’s all about. It provides them

with “safe harbor” in the event that the borrower defaults. What does

that mean?

It means that the government can’t get its money back if the loan

blows up. The qualified mortgage actually protects the banks, not the

consumer. That’s why it’s such a farce, just like Dodd Frank is a

farce. Nothing has changed. Nothing. In fact, it’s gotten worse. Now

we’re on the hook for whatever losses the banks run up peddling mortgage

credit to anyone who can fog a mirror.

We’ll leave the last word for Dean Baker, since he seems like the

only guy in America who has figured out what the hell is going on:

“In short, the Corker-Warner plan to privatize Fannie and

Freddie is essentially a proposal to reinstitute the structure of

incentives that gave us the housing bubble and the financial crisis, but

this time with the added fuel of an explicit government guarantee on

the subprime MBS. If that doesn’t sound like a great idea to you then

you haven’t spent enough time around powerful people in Washington.”

The Johnson-Crapo bill doesn’t have anything to do with “winding

down” Fannie and Freddie or “overhauling” the mortgage finance industry.

It’s a bald-face ripoff engineered by two chiseling senators who are

putting the country at risk to beef up Wall Street’s bottom line.

It’s the scam of the century.

Billionaire Oprah Winfrey is planning a tour to help you with your life.

The Oprah Winfrey experience is coming to an arena near you.

Starting in September, Winfrey will set out on an eight-city Oprah’s

The Life You Want Weekend tour. The plan: pack 18,000-seat arenas for a

two-day experience featuring a keynote by Winfrey, who will share her

personal story and advice on Friday night, and group activities and

speakers picked by her on Saturday. Among those signed to participate:

Eat Pray Love author Elizabeth Gilbert, pastor Rob Bell, OWN star Iyanla

Vanzant and, in certain cities, guru Deepak Chopra.

It’s all about helping you live the life you want:

Winfrey tells THR a domestic tour has been atop her

“bucket list” since she finished a speaking circuit in Canada in early

2013. Although Life You Want will be much larger in scale, her message

remains the same. “It’s about living the life you want, because a great

percentage of the population is living a life that their mother wanted,

that their husband wanted, that they thought or heard they wanted,” says

Winfrey, adding that she will use the platform to push themes of

“empowerment, resilience and authenticity.”

Tickets begin at $99 and a VIP “Meet and Greet” will cost you $999.

Oprah says that this has been on her “bucket list” for some time, but it

appears to represent one more avenue to extract capital from her

addle-brained fans.

Life You Want is being staged in partnership with Harpo

Studios, O, The Oprah Magazine, cable network OWN and her agency, WME,

which recently launched a live events division. (The latter, a way to

capitalize on another potential revenue stream in a fractured media

environment, also is behind other events, including Arianna Huffington

and Mika Brzezinski’s Thrive: A Third Metric Live and Cosmopolitan

Magazine’s Fun Fearless Career Weekend.) Toyota and Olay will serve as

sponsors. Although the different Winfrey media outlets likely will use

tour content, fellow OWN president Erik Logan says they haven’t yet

determined how.

This is precisely what makes liberals, especially wealthy liberals,

so loathsome. A billionaire does not need any more money. A billionaire

can afford to offer you advice for free. What Winfrey is doing is so

typical of hypocritical liberals. This is all about helping you- for a

chunk of change. Where’s the “spreading it around” that liberals and her

buddy Obama are always blathering about? The bottom line is always the

same. It’s about spreading YOUR money around and not theirs.

If you have $1000 to squander on meeting Oprah, then you already have the life you want.

Thai satellite images have shown 300 floating objects in the

southern Indian Ocean during a search for the missing Malaysian

airliner, an official said Thursday.

The objects, ranging from two

to 15 metres (6.5 to 50 feet) in size, were scattered over an area

about 2,700 kilometres (1,680 miles) southwest of Perth, according to

the Geo-Informatics and Space Technology Development Agency.

"But

we cannot -- dare not -- confirm they are debris from the plane," the

agency's executive director, Anond Snidvongs, told AFP.

He said the information had been given to Malaysia.

The

pictures were taken by Thailand's only earth observation satellite on

Monday but needed several days to process, Anond added.

He said

the objects were spotted about 200 kilometres away from an area where

French satellite images earlier showed potential objects in the search

for the Boeing 777 which vanished on March 8 with 239 people aboard.

Thailand

faced criticism after announcing more than a week after the jet's

disappearance that its radar had picked up an "unknown aircraft" minutes

after flight MH370 last transmitted its location.

The Thai air force said it did not report the findings earlier as the plane was not considered a threat.

The

Malaysia Airlines plane is presumed to have crashed in the Indian Ocean

after mysteriously diverting from its Kuala Lumpur-Beijing path and

apparently flying for hours in the opposite direction.

Thunderstorms and gale-force winds grounded the international air search for wreckage on Thursday.

Japanese satellite images have shown around 10 floating objects off

Australia, possibly from missing Malaysia Airlines flight 370, media

reports quoted the government as saying today.

The objects were spotted in waters roughly 2,500 kilometres southwest of Perth, Kyodo and Jiji news agencies said.

Japan's Cabinet Satellite Intelligence Center's study showed objects up

to eight metres (26.4 feet) in length and four metres wide in images

captured by a satellite between 8 am and 2 pm (0000 GMT and 0600 GMT)

Wednesday, Kyodo said.

A government source said they could be wreckage of the missing plane

since they were found in an area overlapping the sites where debris had

previously been spotted, according to the agency.

Jiji quoted a government official as saying the floating objects were "highly likely" to be part of the plane.

Japan had handed the information to Malaysia, the reports said. – AFP, March 28, 2014.

The disappearance of flight MH370 has triggered painful memories for

families of another Malaysia Airlines tragedy who have been waiting for

answers even longer – 37 years, to be exact, reported CNN today.

In 1977, flight MH653 was hijacked en route from Penang to Kuala

Lumpur. The Boeing 737-200 crashed into a mangrove swamp as it

descended, killing all 100 on board.

It was the deadliest incident in Malaysian aviation history prior to MH370.

"Thirty-seven years down the line, we still don't really know the

truth," Ruth Parr, who was 19 when her father, Thomas, died in the

crash, told CNN.

The hijacker or hijackers of MH653 have never been identified, despite

cockpit voice recordings that captured everything from the breach of the

cockpit to the sound of gunshots that killed both pilots.

A report by the Malaysian Civil Aviation Department said the aircraft was hijacked as it approached Kuala Lumpur.

Apparently, there was confusion over whether it should land there and the aircraft then proceeded towards Singapore.

As it descended, the crew was shot and the aircraft "carried out some

unusual pitch up and pitch down terminal manoeuvres before finally

crashing into swampy ground at some 450 knots".

The report, quoted by CNN, concluded that the crash was caused by the

crew being fatally incapacitated, leaving the aircraft "professionally

uncontrolled".

However, some eyewitnesses at the time reported seeing the aircraft in

flames before it hit the ground, while others reported hearing an

explosion before the crash although there was no evidence to support

these allegations.

As the search for MH370 enters the 21st day, for the family members of

victims of flight MH653 contacted by CNN, MH370 tiggered painful

memories although they have learned to cope with their grief.

"You have to carry that with you all the time," Tom Sherrington, whose father, Richard, was on MH653, told CNN.

He said talking about their memories of his father, whom he described

as a "fun guy" and "big adventurer," helped his family to cope.

The family also visits the memorial, built near the crash site in the

coastal town of Tanjung Kupang, Johor, and Sherrington said this enabled

his family to have a tangible place to reflect on their loss.

Sherrington told CNN that families of those on board MH370 should focus

on remembering their loved ones and not become obsess with assigning

blame for the tragedy.

"The one thing I would say is not for them to get too obsessed with the

detail and the recriminations and all that," he said, adding that he

hoped the families would stick together and find comfort in each other.

Both Parr and Sherrington said everyone processed his or her grief in

different ways and there was no shortcut.

"It gets a little easier over time but you can never forget the date," Parr told CNN.

"You will forever think you see that person out and about, a glance in

the car's rearview mirror or crossing the road. It could be anywhere, a

voice that sounds like him will have you spinning around only to find

it's someone else."

Anguished families of passengers on board MH370 have been clamouring

for proof that the Boeing 777-200ER (9M-MRO) had indeed ended its flight

in the Indian Ocean as announced by Prime Minister Datuk Seri Najib

Razak on Monday night.

Ch’ng’s Khai Cheak, whose sister Ch’ng Mei Ling was on the flight, said

such an announcement should only have been made when there was physical

evidence or bodies to show that the plane had indeed crashed in the

ocean.

“What do I tell my mother back home? She saw the news but she cannot

accept the fact that my sister is dead. She keeps asking how did she

die?” said a visibly angry Khai Cheak, the eldest of five children.

“I don’t know what to tell her because there is no proof to show that Mei Ling is dead.”

Families in China, too, have criticised the Malaysian authorities and

had lambasted senior officials at briefings held for them.

Scores of angry relatives of the Chinese passengers aboard MH370 had

marched to the Malaysian embassy in Beijing to demand more answers about

the fate of the plane and its passengers.

Around 200 family members, some in tears, linked arms and shouted

slogans, including "the Malaysian government are murderers" and "we want

our relatives back".

Some families have also approached a Chicago-based law firm to help

them file a suit against the 777 aircraft manufacturer Boeing Co and

Malaysia Airlines as they believe the plane had crashed because of

mechanical failure. – March 28, 2014.

That any schoolkid could predict eliminating

feedback and consequences will lead to a series of disastrously poor

choices by speculators and imprudent borrowers doesn’t register

with the Keynesian Cargo Cult.

The Keynesian Cargo Cult’s ability to

print and squander money is insignificant next to the power of

Diminishing Returns. By now we all know two things about the

Keynesian Cargo Cult’s religion:

1. It has failed to conjure up the recovery its

sadly devoted believers insist is “just around the corner if we

only borrow and squander more money” because…

2. Its main tenet–that the problem is “lack

of aggregate demand,” i.e. people will buy more stuff made in China

and corporations will open more stores to sell the stuff made in

China–if only it was dirt-cheap to borrow more money–is

completely, utterly, painfully false.

The central premise of the Keynesian Cargo

Cult is that this mechanism of making it cheap and easy to borrow

money will work a kind of magic that can only be manifested by

dancing around a fire at night waving dead chickens and chanting

“humba-humba.” The Keynesian cargo Cult calls this magic

“animal spirits.”

Unfortunately, waving dead chickens while

dancing around a fire doesn’t do anything in the real world, and

neither does making it cheap and easy to borrow more money.It

turns out that prudent people have no interest in borrowing more

money, even at low rates of interest, and imprudent people are happy

to do so but will stop paying the loan as soon as something untoward

occurs in their finances. The cheap, easy-to-get loans default and

either the banks who made the loans collapse or the taxpayers have to

bail out the banks who foolishly lent money to imprudent borrowers at

super-low rates of interest.

Corporations, meanwhile, look at the real risks

of expanding business in a debt-saturated economy distorted by

Keynesian Cargo Cult policies and realize that gambling capital on

the possibility that waving dead chickens and chanting “humba-humba”

will actually increase profits is a truly stupid bet, so they borrow

the nearly-free money and invest it in various carry trades overseas

that return a virtually risk-free return, thanks to the nearly-free

cost of borrowing mountains of money from the Cargo Cult.

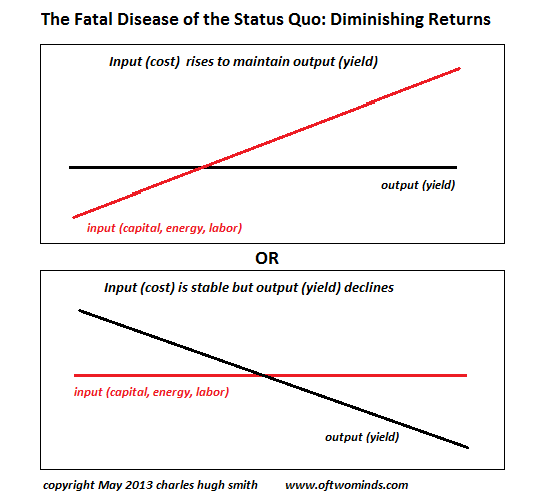

The Keynesian Cargo Cult is stubbornly blind

to the two key dynamics of the real-world economy: diminishing

returns and the S-Curve. Diminishing returns result when a

system’s ability to produce an economically valuable output

declines.

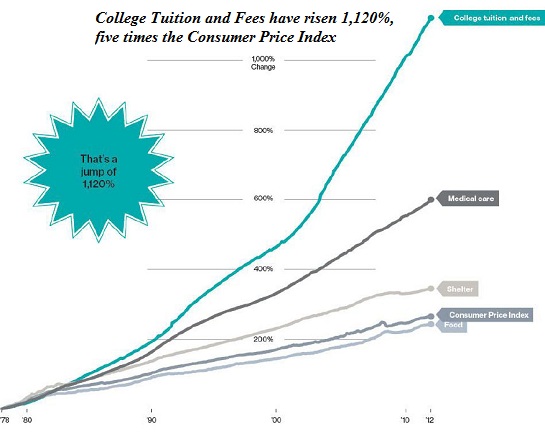

Higher

education is a good example: tuition has soared $1,100% while the

output (value of a college degree) has declined precipitously. A

recent major study,Academically

Adrift: Limited Learning on College Campuses, concluded that

“American higher education is characterized by limited or no

learning for a large proportion of students.”

Meanwhile, student loans exceed $1 trillion,

only 37% of freshmen at four-year colleges graduate in four years

(58% finally graduate in six years), and 53% of recent college

graduates under the age of 25 are unemployed or doing work they could

have done without going to college–retail clerks, waiting tables,

etc.

The Keynesian Cargo Cult solution to the

diminishing returns is to provide more debt to students, making them

into debt-serfs for life. The cruel stupidity and immorality

of the Keynesian Cargo Cult knows no bounds because they refuse to

accept the reality that diminishing returns cannot be fixed by more

debt and more squandering of good money after bad.

The

truth is the failed cartel of higher education has to be leapfrogged

and left in the dustbin of history: here’s a model that lowers

costs by 90% and aligns the output with the real economy: The

Nearly Free University and The Emerging Economy.

The Keynesian Cargo Cult’s solution allows

no feedback from the real world, and allows no mechanism to

discipline the imprudent borrower/speculator. If imprudent

borrowers take on too much debt, the Keynesian Cargo Cult’s

solution is to offer them more credit at rates they can

afford–near-0% if necessary.

If a speculator borrows money and loses it in a

high-risk gamble, the Keynesian Cargo Cult’s solution is to force

the taxpayer to make good the gambler’s losses and then give the

speculator more nearly-free money to continue gambling.

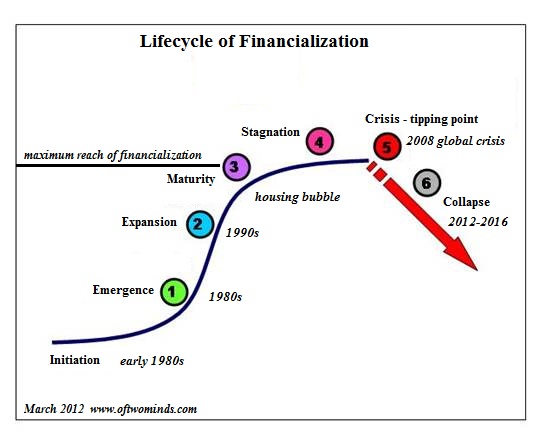

This “solution” works the first time

around, less well the second time around, and triggers a collapse the

third time around. This lifecycle is called the S-Curve:

The Keynesian Cargo Cult inflated one credit

bubble in the 1990s, another in the 2000s, and by an extraordinary

expansion of credit and lowering interest rates to near-zero has

managed to Beat the Devil and inflate a third credit bubble in the

2010s.

That any schoolkid could predict waving dead

chickens and eliminating feedback and consequences will lead to a

series of disastrously poor choices by speculators and imprudent

borrowers doesn’t register with the Keynesian Cargo Cult. But

since the Keynesian Cargo Cult is headed by a Nobel Prize academic

economist, the Cargo Cult members effusively praise the Emperor’s

fine (and nonexistent) robe.

You poor, dumb, deluded fools. You’ve

destroyed our economy, our values and our ability to deal with

reality. Your faith is as boundless and disconnected from

the real world as your policies.

A fresh round of food stamp cuts at the state level are underway, on

top of federal food stamp reductions that hit millions of Americans

twice since November. In some states, policymakers have imposed

additional cuts that jeopardize benefits for hundreds of thousands.

The impact of the reductions is just beginning to take hold, or soon will.

"They're

getting cut off and seeking help," said Debi Kreutzman of the Kansas

Food Bank, which is dealing with changes that could affect 20,000

Kansans. "We're starting to see that come into play now, and I'm afraid

it's only going to get worse."

The state cuts target a relatively

small portion of the food stamp population: low-income able-bodied

adults, without children, 18 to 50 years old -- estimated to be about

10% of the more than 47 million in the program. In some states,

recipients are losing benefits because of reinstated work requirements

as a condition of qualifying for food stamps.

These cuts come on top of an across-the-board 5% reduction of benefits to all food stamp recipients' benefits last November.

As part of the farm bill earlier this year, Congress also closed a

loophole and cut benefits for 850,000 households, although many states

affected are moving to block the cuts for now.

The

federal food stamp program (formally known as the Supplemental

Nutrition Assistance Program) limits how long low-income childless,

able-bodied adults can receive food stamps to three months in a

three-year period, unless they are working or participating in a

training or workfare program for at least 20 hours a week. Other food

stamp recipients face less stringent work requirements, and there are

exemptions for those with children or other caregivers.

The 2009

stimulus bill suspended these requirements through 2010, and after that

states were allowed to waive them if they met certain conditions based

on their economies and job markets. Most every state has waived the

requirements since 2011. RETHINKING WAIVERS

In recent years, though, some states — many controlled by Republicans — began to rethink the waivers,

which were part of the 1996 welfare reforms and designed to give states

flexibility in times of high unemployment. With the start of the new

federal fiscal year last October, eight went back to enforcing the

requirements, and 10 waived them only in part of their state or for part

of this year. The changes are just beginning to be felt in some of

those states.

In Delaware, officials insist a waiver is

unnecessary because the state's work-training and placement program has

been able to manage the growing ranks of the jobless. But the Food Bank

of Delaware said some recipients have hit the three-month cutoff unable

to find work. The state might soon reconsider the requirements.

"The

case load is growing pretty dramatically," said Elaine Archangelo,

director of the Division of Social Services for Delaware. "So we have

been considering if there are areas where we could, should request a

waiver."

Of states without waivers, Iowa, Nebraska and Wyoming

were no longer eligible, because their economies and job markets had

improved, as measured by the eight factors

considered by the federal government when determining waiver

eligibility. Others, such as Delaware, Kansas, Oklahoma, Utah and

Virginia, are going without them despite being eligible for at least

partial waivers.

Ohio, Colorado, New York, Texas and Wisconsin are

all waiving the work requirements for only part of the year or in

certain areas, even though they were eligible for full coverage.

Minnesota, New Hampshire, North Dakota, South Dakota and Vermont were

eligible only for partial waivers. For a full list of each state's

status for this year, click here. JOB TRAINING

Ohio

chose to go without a waiver for most of the state. Only 16 out of 88

counties are exempt — mainly rural, Appalachian regions where the

average unemployment rate was 10.2% or higher in 2011 through 2012. The

situation left food banks and food stamp outreach workers in Ohio

scrambling, facing a shortage of jobs and training opportunities.

"It's

a lack of jobs, not a lack of willingness to work," said Lisa

Hamler-Fugitt of the Ohio Association of Food Banks. "In an environment

where we have college graduates that are now competing for low-wage

jobs, for folks with multiple barriers to employment, it's going to be

difficult for them to find work."

Exact figures on the effect in

Ohio are hard to come by. Of the nearly 141,000 people in the affected

category receiving food stamps before, 98,000 were still receiving them

in January, but it's impossible to know exactly why people left the

program. According to the Ohio Department of Job and Family Services, in

January more than 16,000 were suspended or kicked off the program due

to the work requirements.

Ben Johnson of the Ohio Department of

Job and Family Services disagreed with Hamler-Fugitt's assertion that

jobs aren't available. "Our only goal was to provide benefits and job

training where appropriate," he said. "We've worked very hard, and our

county partners have worked especially hard, to notify individuals and

bring them in and find appropriate training and employment activities."

Passed

by the Republican-controlled legislature, Wisconsin will re-impose the

work requirements this year as part of a job-growth pitch from

Republican Gov. Scott Walker. The changes — which were part of a jobs

package that also included $35 million for job training — will phase in

starting in July and cover the entire state by next January. About

63,000 could be affected. APPLYING PRESSURE

In some

states, the decision to reinstate work requirements was part of an

effort to push people off food stamps and back to the workforce, as in

Kansas, where officials said jobs, not public welfare, was the cure for poverty.

In Oklahoma, Republican House Speaker T.W. Shannon, who's now running for U.S. Senate, pushed

the change as welfare reform. As many as 233,000 were put under review ,

according to the Regional Food Bank of Oklahoma, many more than

originally expected.

"Unfortunately, some believe compassion is

measured by how many people you can keep on a government aid program,"

Shannon said in a statement when fellow Republican Gov. Mary Fallin

signed his bill. "Through personal responsibility, hard work and a drive

to better one's situation, people can establish their independence and

begin down the road of prosperity."

Food banks and other advocates

see things differently. They say the economy hasn't recovered enough to

support reinstating the work requirements. Many affected are very poor,

often uneducated, sometimes homeless who would have difficulty meeting

the requirements anyway.

"Certainly a lot of people max out with

that three-month period," said Matt Talley, who works on outreach for

the Food Bank of Delaware, which includes helping those who lack

transportation or have other barriers to meeting requirements. "It's

just a matter of trying to help them find work, or help them find an

opportunity to participate in a job training program."

The changes

in states are coming as part of a broader effort in Congress to trim

food stamps, after spending hit a record high of $82 billion in fiscal

year 2013.

The work requirements have been a popular subject in

that debate. House Republicans in Congress proposed reinstating the

requirements nationwide last year, citing a recovering economy and

warning about the cost of suspending the requirements for too long. But

Democrats rejected that, leaving states to enact the changes themselves.

"In

general, having a work requirement is good policy," said Rachel

Sheffield of the conservative Heritage Foundation. "It serves as a

gatekeeper to ensure that those who need assistance are able to get it,