Analysts believe big tech deal will lead to more, with high valuations

Getty Images

Is Twitter next?

Microsoft Corp.’s $26.2 billion all-cash deal

for LinkedIn Corp. might inspire other social-media acquisitions,

notably Twitter Inc., and could raise deal valuations, according to

analysts.

With Microsoft’s

MSFT, -0.62%

LinkedIn

LNKD, -0.30%

deal coming in as the sixth

largest tech-sector deal in history, according to Dealogic, some say it

might inspire other acquisitions in the industry. Saxo Bank’s head of

equity, Peter Garnry, is betting that Alphabet Inc.

GOOG, -0.01%GOOGL, +0.19%

will buy Twitter

TWTR, +5.57%

by the end of this year.

“It

is difficult long-term to see Twitter as a standalone company,” he

said. “We are betting more now that this will be an acquisition before

the year-end.”

Also see: Did Microsoft overpay for LinkedIn?

Google

might be interested in Twitter’s base of 300 million users to give it a

stronghold in the social media space after failing against Facebook

Inc.

FB, +0.87%

with Google Plus, Garnry said.

Shares

of Twitter have risen about 7% since the deal with LinkedIn was

announced Monday morning, though they’re still off 13% in the last three

months and 58% for the year.

While the LinkedIn deal isn’t likely a strict social media play by

Microsoft, according to Rob Enderle, principal analyst at tech

consulting company Enderle Group, it still might inspire other companies

already interested in social networks to make similar deals, possibly

at higher valuations, he said.

“Twitter is the next target and

this could be just a start for new tech boom,” said Naeem Aslam, chief

market analyst at Think Forex. Also See: 5 potential takeovers following Microsoft-LinkedIn deal

The

LinkedIn deal is the biggest technology acquisition so far this year in

what has otherwise been a slower year for tech M&A than 2015. So

far this year, 4,081 M&A deals have been struck, versus 4,456 at the

same time last year, according to Dealogic.

However, by

valuation, 2016 is so far tracking ahead of 2015, with LinkedIn’s $26

billion buyout leading the sector, according to Dealogic. Tech deal

values have reached $263.8 billion year-to-date, compared with $242.8

billion at this time last year, and some analysts say LinkedIn may bode

well for other potential takeout targets, such as Twitter, GrubHub Inc.

GRUB, -2.05%

, GoDaddy Inc.

GDDY, +0.89%

and Yelp Inc.

YELP, -0.41%

.

“We don’t

necessarily think transactions will increase materially, but rather help

create a better valuation floor,” Monness Crespi Hardt analyst James

Cakmak said.

An iconic Manhattan business will be closing its doors at the end of the month after 126 years in business.

In a letter to the Manhattan Mercury, the owner of Varney’s Book Store, Jon Levin, said all three stores will close on June 30th.

Levin told the Manhattan Mercury the store’s revenue has fallen 80

percent in the last few years after losing contracts with both the

K-State Student Union bookstore and K-State athletics.

Levin said increased online competition also hurt business.

The bookstore said it will have more information about unused gift cards and rewards points on its website.

It is with great sadness that we announce the closing of Varney’s

Book Store in Aggieville. At the same time we will close all of our

stores throughout Kansas. We will formally shut our doors for business

on June 30. Varney’s has served K-State and the community for a

wonderful 126 years as a locally owned family business.

We wish to thank all of our employees who through the years have helped

make us who we were. Many worked as part time student employees while

going to school at K-State. Others worked full time and dedicated many

years of their careers working with us. We truly appreciate each and

every one of you.

We also want to say thank you to the hundreds of thousands of

customers, who for over a century have come through our doors, shopped

through our catalogs, clicked through our websites, gathered with us at

many a bowl game, celebrated New Year’s, and watched a parade or two in

Aggieville. Many of you have followed us on Facebook and Twitter as

well. No matter how you came to us, it was a privilege serving each and

every one of you. CONTINUE READING

Student loan delinquencies skyrocket. Retail spending and home

improvement spending declines. Baltic Dry Index Falls declines again.

The Pension bubble has started to burst. Personal tax receipts and state

sales tax receipts decline showing the economy is failing. ECB begins

purchasing corporate debt. The people in the UK are pushing the idea to

exit the EU

by Simon Black

Apparently the biggest banks in the US didn’t learn their lesson the first time around…

Because a few days ago, Wells Fargo, Bank of America, and many of the

usual suspects made a stunning announcement that they would start

making crappy subprime loans once again!

I’m sure you remember how this all blew up back in 2008.

Banks spent years making the

most insane loans imaginable, giving no-money-down mortgages to people

with bad credit, and intentionally doing almost zero due diligence on

their borrowers.

With the infamous “stated income” loans, a borrower could qualify for

a loan by simply writing down his/her income on the loan application,

without having to show any proof whatsoever.

Fraud was rampant. If you wanted to qualify for a $500,000 mortgage,

all you had to do was tell your banker that you made $1 million per

year. Simple. They didn’t ask, and you didn’t have to prove it.

Fast forward eight years and the banks are dusting off the old playbook once again.

Here’s the skinny: through these special new loan programs, borrowers are able to obtain a mortgage with just 3% down.

Now, 3% isn’t as magical as 0% down, but just wait ‘til you hear the rest.

At Wells Fargo, borrowers who have almost no savings for a down

payment can actually qualify for a LOWER interest rate as long as you go

to some silly government-sponsored personal finance class.

I looked at the interest rates: today, Wells Fargo is offering the

exact same interest rate of 3.75% on a 30-year fixed rate, whether you

have bad credit and put down 3%, or have great credit and put down 30%.

But if you put down 3% and take the government’s personal finance

class, they’ll shave an eighth of a percent off the interest rate.

In other words, if you are a creditworthy borrower with ample savings

and a hefty down payment, you will actually end up getting penalized

with a HIGHER interest rate.

The banks have also drastically lowered their credit guidelines as

well… so if you have bad credit, or difficulty demonstrating any credit

at all, they’re now willing to accept documentation from “nontraditional

sources”.

In its heroic effort to lead this gaggle of madness, Bank of America’s subprime loan program actually requires you to prove that your income is below-average in order to qualify.

Think about that again: this bank is making home loans with just 3%

down (because, of course, housing prices always go up) to borrowers with

bad credit who MUST PROVE that their income is below average.

[As an aside, it’s amazing to see banks actively competing for

consumers with bad credit and minimal savings… apparently this market of

subprime borrowers is extremely large, another depressing sign of how

rapidly the American Middle Class is vanishing.]

Now, here’s the craziest part: the US government is in on the scam.

The federal housing agencies, specifically Fannie Mae, are all set up to buy these subprime loans from the banks.

Wells Fargo even puts this on its website: “Wells Fargo will service the loans, but Fannie Mae will buy them.” Hilarious.

They might as well say, “Wells Fargo will make the profit, but the taxpayer will assume the risk.”

Because that’s precisely what happens.

The banks rake in fees when they close the loan, then book another small profit when they flip the loan to the government.

This essentially takes the risk off the shoulders of the banks and

puts it right onto the shoulders of where it always ends up: you. The

consumer. The depositor. The TAXPAYER.

You would be forgiven for mistaking these loan programs as a sign of

dementia… because ALL the parties involved are wading right back into

the same gigantic, shark-infested ocean of risk that nearly brought down

the financial system in 2008.

Except last time around the US government ‘only’ had a debt level of

$9 trillion. Today it’s more than double that amount at $19.2 trillion,

well over 100% of GDP.

In 2008 the Federal Reserve actually had the capacity to rapidly expand its balance sheet and slash interest rates.

Today interest rates are barely above zero, and the Fed is technically insolvent.

Back in 2008 they were at least able to -just barely- prevent an all-out collapse.

This time around the government, central bank, and FDIC are all out

of ammunition to fight another crisis. The math is pretty simple.

Look, this isn’t any cause for alarm or panic. No one makes good decisions when they’re emotional.

But it is important to look at objective data and recognize that the colossal stupidity in the banking system never ends.

So ask yourself, rationally, is it worth tying up 100% of your

savings in a banking system that routinely gambles away your deposits

with such wanton irresponsibility…

… especially when they’re only paying you 0.1% interest anyhow. What’s the point?

There are so many other options available to store your wealth.

Physical cash. Precious metals. Conservative foreign banks located in

solvent jurisdictions with minimal debt.

You can generate safe returns through peer-to-peer arrangements, earning up as much as 12% on secured loans.

(In comparison, your savings account is nothing more than an

unsecured loan you make to your banker, for which you are paid 0.1%…)

There are even a number of cryptocurrency options.

Bottom line, it’s 2016. Banks no longer have a monopoly on your savings. You have options. You have the power to fix this.

Gun company shares soared on Monday as traders predicted that

Americans will react to the Orlando massacre by rushing out to arm

themselves with more guns.

Shares in the two biggest listed US gun manufacturers Smith &

Wesson and Sturm Ruger & Co rose by 11% and 10% in early trading and

ended the day up 6.8% and 8.5% respectively. Gun companies shares have risen strongly after every recent mass shooting incident as

investors speculate that the atrocities might lead to tougher gun

control measures. Fear that stricter gun laws might be enacted cause

more people to buy guns, especially semi-automatic assault rifles like

the AR-15 used by Orlando killer.

Smith & Wesson, which sold a record $627m worth of guns and

accessories last year, is expected to report even higher sales this year

when it releases its full-year results on Thursday.

In its most recent quarterly earnings, in March, the company said

sales were up 61.5%, which its British chief executive James Debney

credited to the “long-term trend toward personal protection”. Sales in

the quarter came in at $211m, and the company doubled its gross profit

to $87m.

S&W’s share price has already rise 39% in the last 12 years,

making it one of the best performing investments on the US stock

markets. Sturm Ruger’s shares have risen about 6%.

On Sunday Barack Obama said the Orlando attack – “an act of terror

and an act of hate” – once again showed that the nation needs to

introduce tougher gun control laws. “This massacre is therefore a

further reminder of how easy it is for someone to get their hands on a

weapon that lets them shoot people in a school, or in a house of

worship, or a movie theatre, or in a nightclub,” he said. CONTINUE READING

A young woman faints in the heat as hundreds fight for pasta,

screaming they are hungry. Slum-dwellers and armed gangs wait for

nightfall to hijack food trucks or ransack stores. A mother is shot dead

fleeing police after hundreds storm warehouses.

Food riots and violent looting have become a daily occurrence across

scarcity-struck Venezuela and a major problem for the struggling leftist

government of President Nicolas Maduro.

Despite hours in lines, Venezuelans increasingly find that coveted

supplies of subsidized flour and rice run out before they can buy them.

Many are skipping meals, getting by on mangoes stripped from trees – or

taking matters into their own hands.

On a recent morning in the rundown, garbage-strewn Caracas district

of El Valle, some 200 people pushed up against police guarding a

supermarket as they chanted, “We want food!” and “Loot it!” A few at the

front were allowed in for two bags of pasta each.

“We’re not eating. People are desperate for a looting,”

saidmother-of-three Miza Colmenares, 55, who had spent the night in line

and not eaten since the previous day when she had eggs for breakfast.

One young woman fainted in the heat, an elderly lady cried

uncontrollably on the sidewalk and the seething crowd chased away a

government supporter.

Supermarkets have become flashpoints across Venezuela, one of the world’s most violent countries.

More than 10 lootings occur every day now, according to the

Venezuelan Observatory of Violence, and are increasing in the usually

more insulated capital. CONTINUE READING

by: otterwood

The chart below shows the relation between the US dollar index and

speculative positioning in the USD futures. Speculative positions held

by individual investors, hedge funds, and large financial institutions

tend to lead changes in the USD, see the chart below.

The red arrows show peak positioning and eventual falls in the USD

while green arrows show troughs in positioning and subsequent increases

in the USD.

As can be seen in the chart US

dollar positioning peaked in the beginning of 2015 and has been in a

down trend ever since. Considering all of the Fed’s flip flopping the

next major move in the USD may more likely be to the downside.

by Charles Hugh-Smith We need a new economic model that recognizes the value of useful work that isn’t necessarily profitable. All the media chatter about work disappearing due to automation

fails to draw the critical distinction between useful but unpaid work

and profitable work.Since value (and profits/wages) flow to what’s

scarce, what matters is not the decline of useful work–there’s plenty of

that even in a society that has automated production–but the supply of

paid work–work that is profitable and hence worthy of wages. Mark Jeftovik and I discuss work, profit and new models of paying for useful work(44:47) in a free-ranging podcast on my book A Radically Beneficial World.

The great fantasy that many are depending on to solve the decline of paid work is taxing the robots and software that ate all the jobs. These taxes are supposed to pay for the Universal Basic Income that everyone will enjoy once work is automated and jobs become scarce.

The problem with the fantasy is that profits only flow to what’s

scarce, and as the tools of automation are commoditized, they will no

longer be scarce. Once anyone can buy the same robots/software you

own, where is your competitive advantage? If anyone on the planet with

some capital can buy the same robots and software, where is the pricing

power that is essential to reaping big profits? Commoditization and globalization push profits down to near-zero.

In a world of ever-cheaper, ever more abundant commoditized tools and

software, it becomes much more difficult to generate increases in

productivity and profits. Those who dream of the the end of work forget that robots will only be purchased to perform profitable tasks.

Much of human life is not profitable. For example, maintaining

dedicated bikeways is useful work that serves the health and

transportation needs of the community and economy.

There is no way to make this work profitable unless you charge

bicyclists for using the bikeways, which defeats the purpose of the

bikeways.

The typical response is that governments will pay for robots to maintain bikeways. But that leads right back to the decline of profits and paid labor:

since government depends on profits and paid work for its revenues, as

those decline, where will government get the revenue to make good all

its vast promises for pensions, services, healthcare etc., and buy and

maintain robots to do unprofitable but useful work such as maintain

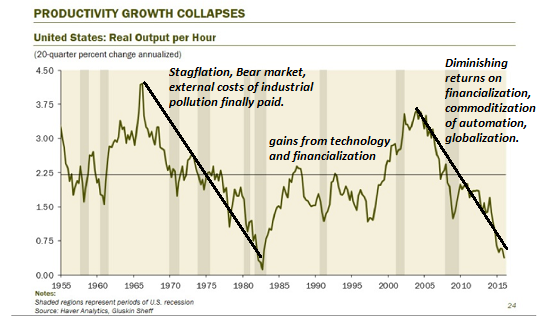

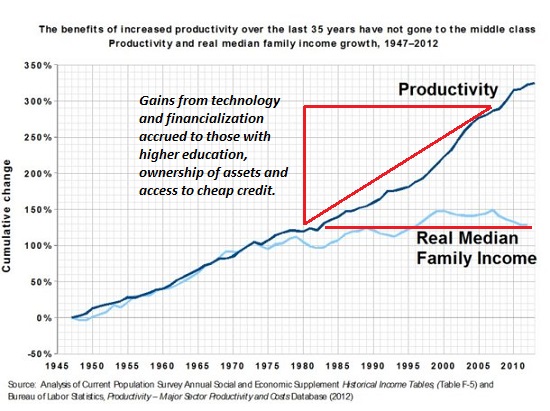

bikeways? Take a look at these charts of productivity and income.

Ultimately, increases in jobs, wages and profits flow from increases in

productivity, which typically rises as a result of investments in better

tools, training and processes.

Productivity struggles when investment stagnates, external costs

(such as paying to remediate industrial pollution) reduce the available

pool of capital/profits to invest, and new technologies are either

limited in scope or do not scale well.

All these factors played a role in the 15-year stagnation of productivity from 1966 to 1980.

As computer/digital technologies improved and dropped in price (i.e.

scaled up to impact the entire economy) and financialization (i.e.

abundant credit and leverage, and the commoditization of financial

assets) provided new sources of profits, productivity increased from

1981 to 2005.

Since then, growth of productivity has been in a freefall:

financialization has reached diminishing returns, the technologies of

automation have been commoditized, and globalization has opened up a

vast new labor force and new places to invest capital. In sum: what was once scarce is now abundant, and thus it no longer generates value or profits. When new productivity tools were scarce (unique to American

factories and workplaces) and required a growing labor force,

productivity growth translated into higher wages. But when

productivity growth relied on financial capital and processes and

higher-level technical/managerial skills, the gains flowed only to those

who owned these processes and skills: generally speaking, the wealthy

owners of productive capital and the highly educated

technocrat/managerial class (the top 5% and to a lesser degree, the top

20%.) All of which is to say the model of paying wages for profitable

work (or collecting taxes from profits and profitable work to pay

government workers) is broken: not slightly broken, but fundamentally broken. We need a new economic model that recognizes the value of useful work that isn’t necessarily profitable,

an economic system that creates money to pay those doing useful work at

the bottom of the pyramid rather that creating money only for banks,

corporations and financiers at the very top of the pyramid. There is plenty of work that is useful but not profitable. Work won’t disappear; it’s paid work and profits that will become increasingly scarce. We need a new system that enables an abundance of paid work. This is the topic of my book,which Mark Jeftovik and I Discuss in this podcast (44:47).

A vote to leave the EU could cost banks billions of dollars, if they lose their key ‘passporting’ rights

Bloomberg

London’s financial city could be hit hard by a Brexit

A U.K. exit from the European Union risks costing the City of London

billions of pounds, thousands of workers and its spot as the world’s top

financial center.

That’s the message from players in the

financial industry ahead of the highly contentious in/out referendum on

EU membership this month, and it all centers on one simple process

that’s complex to undo: passporting.

The mechanism allows

British-based financial institutions such as banks, fund managers and

insurers to seamlessly sell their services across the 28 EU nations

without having to get regulator approval or set up subsidiaries in each

member state.

So

what could happen in London’s financial sector, if the passporting

right goes down the drain? The Brexit “leave” and “remain” campaigns are

still hashing out the issue, but several voices across the City of

London are clear.

“It would kill it,” said Stuart Alexander, chief executive at Gemini Investment Management, which is using the mechanism.

“You’d

have to go back to the old regime of a U.K. fund management company

going into Frankfurt and saying, ‘Please, Mr. Regulator, will you

authorize this fund for distribution in your country?’” he said.

Passporting has been

extremely popular. U.K. banks use it to expand its customer base in the

union. EU firms use it to tap into the international financial markets

via London, as a global financial hub.

Plus, non-U.K. and non-EU

banks use it as a financial springboard to do business with the entire

EU, with the benefit of only having to set up a base in one place. Swiss

and U.S. banks, for example, use London for easy access to the European

single market.

UBS

UBSG, -2.20%UBS, -1.29%

Goldman Sachs

GS, -1.64%

Russia’s Sberbank

SBRCY, -2.82%

J.P. Morgan

JPM, -1.88%

and China’s ICBC

1398, -0.48%

are among several international banks that use passports this way, according to the U.K.’s Financial Conduct Authority.

But

that right is likely to disappear if British voters choose a “Brexit” —

a departure from the EU — in the June 23 referendum. And given

“passporting is of vital importance,” then it will mean a shake-up for

the sector, says Nicky Edwards, director of policy and public affairs at

TheCityUK, a lobby group for London’s financial services industry.

“Brexit

would have a number of potential impacts,” Edwards said. “One is that

you have to expect the non-U.K. firms that currently are based here to

relocate some or all of their operations to within the single market.” Read:This stock-market sector will get hit hardest by a Brexit

Cost of a new passport

Totaling

up the cost to all those individual companies, the loss of a London

passport could mean billions of pounds of outlay on office relocations,

staff transfers, added paperwork and new capital requirements.

If

financial firms want to continue to do business in the EU after a

Brexit, they need to get regulator approval in another member state. To

do that, they will need to set up a subsidiary in the new country and

comply with local regulations there. Then they can “passport” their

services into the rest of the EU, just like they used to do from London.

This is an expensive process, as

the “new” regulator state requires a significant amount of cash or

assets on the institution’s balance sheet to be properly capitalized.

Under EU rules, the minimum share capital for banks and insurers is 5

million euros ($5.58 million), although most local regulators impose

much more, according to law firm Hogan Lovells. The EU-wide Basel III

rules require banks to keep a capital buffer — cash equivalent to 8% of

their total assets.

For funds, the capitalization cost varies.

For example, Luxembourg requires such firms to have at least €10 million

of capital on the their balance sheets, while Irish rules demand only

€300,000, according to Funds Partnership, a recruitment company for the

asset management industry.

And for the banks, fund management

companies and insurers affected, securing such new authorization from a

new regulator could take months, or possibly years.

“People have

to think about what their priorities are. Capitalizing banks is a very,

very expensive business. So you have to decide how big your presence

will be,” said Sharon Lewis, partner at Hogan Lovells.

“I think people will rethink their business,” she said.

“I think it will postpone investments. I think it will

cost jobs. I cannot really see anything positive about it”

There are

already signs that major financial players are considering ditching

London as their key European hub. Frankfurt and Paris have been

mentioned as the obvious choices for a replacement European financial

powerhouse, but Dublin has also been thrown into the mix, mainly because

it has the advantage of being another English-speaking capital.

The

potential loss of passporting rights is “absolutely massive” for Hogan

Lovells’s clients, Lewis said, with some already expressing concerns

about the “costly, time-consuming” process of dealing with it.

“I think it will postpone investments. I think it will cost jobs. I cannot really see anything positive about it,” Lewis said.

Stay or go?

At

Goldman Sachs, senior executives have warned publicly about the dangers

to the city of London of a Brexit. They said they’d considering

shifting the bank’s resources elsewhere in the EU if the exit becomes a reality.

“It

is imperative for the U.K. to keep the financial-services industry in

the U.K. [...] I don’t know what would replace that industry,” Goldman

Sachs’s president Gary Cohn said at the World Economic Forum meeting in

Davos in January, early to sound the alarm over Brexit risks.

The U.S. bank has donated £500,000, or about $700,000, to the “Britain Stronger in Europe” campaign. Morgan Stanley

MS, -2.61%

Citigroup

C, -2.78%

and JPMorgan Chase & Co.

JPM, -1.88%

have also handed over six-figure donations to the “remain” campaign, according to media reports.

Hit to financial services exports

While

it’s difficult to exactly quantify the economic benefits of

passporting, various organizations have taken a crack at estimating what

it would cost to lose the privilege.

“Without passporting

rights, it is conceivable that exports of financial services to the

European Union could fall by half, or about £10 billion ($14.51

billion),” said the authors of a research report by Capital Economics, commissioned by Woodford Investment Management.

Another report,

conducted by PricewaterhouseCoopers for TheCityUK, noted that the

U.K.’s status as a global and regional financial hot spot hinges on its

having access to the single European market.

It pointed out that

in 2014, more than 80% of foreign direct investment into the U.K.’s

financial sector came from countries outside the union, highlighting the

importance of non-EU investments. Read:These are the EU countries that would suffer after Brexit, says Fitch

“The

ability to access the Single Market is one of the factors in attracting

international banking institutions to establish their European

headquarters in the U.K.,” the report said.

Because of this, up

to 100,000 financial services jobs could be lost in the U.K. if a Brexit

goes ahead, according to the report.

GVA = Gross Value Added

Coming out stronger

Some

argue, however, that the Brexit fears are overblown. “Leave”

campaigners say that quitting the union would free London from the EU’s

regulatory restraints and allow the financial services industry to

become more competitive.

By leaving the union, the U.K. could,

for example, revert the cap on banking bonuses that was introduced after

the financial crisis against Britain’s will, said Melanie Debono, an

economist at Capital Economics. Removing that cap and letting bonuses

run high again could provide a lift to financial activity in London,

offsetting some of the negative impacts.

“Passporting rights are not the only thing that’s at stake for the financial services sector,” Debono said.

“We see that the financial services here in the City would flourish in

the long run. In the short term, it would be impacted — actually out of

all the sectors in the U.K., it’s probably the one that will be most

affected — but in the long term, we see it coming out strong,” she

added. Read:5 arguments in favor of a U.K. ‘Brexit’ from the EU — and 5 against

That view was echoed by more than 100 City executives — including Hargreaves Lansdown

HL., -2.76%

founder Peter Hargreaves and CMC Markets

CMCX, -1.27%

chief executive Peter Cruddas — who signed a letter backing a Brexit.

They

argued EU membership is a threat to London’s prosperity, saying the

financial services industry “can thrive and grow” outside the union.

“A bit like a divorce”

What

the U.K.’s relationship with the EU would look like after an exit isn’t

clear. The process of renegotiating trade deals could take years, and

there’s no guarantee Britain’s financial institutions would keep their

easy access to the union. Read:The Swiss franc is your best bet for ‘Brexit’ protection

One

option is to strike a bilateral trade agreement with the EU, just as

Switzerland does. But there’s one flaw: Swiss banks don’t have

passporting rights, and for the most part they operate their European

businesses through subsidiaries in London.

According to the

Capital Economics report, that’s part of the reason Swiss financial

exports have been lower than Britain’s over the past 15 years, despite

Switzerland’s success in the financial sphere.

Another possibility is for

the U.K. to join the European Economic Area, as Norway has done. While

this could help the finance industry preserve its passport privileges,

there are still big risks, according to Hogan Lovell’s Lewis. The sector

could find itself worse off, vis-à-vis Europe.

“I think the EU will be less cooperative than the Brexit campaign thinks,” she said.

“It’s

a bit like a divorce. In some cases, divorces go very well, and there

are mutual interests — ‘children’ — involved on either side of the

Channel,” she added. “But for Europe, it feels a bit like taking a brick

out of a wall, in terms of the whole European Union.”

Gold set for 8.5% rally if Brits vote to leave the EU

So-called Brexit concerns already have significantly jolted financial

markets, but more could be in store if the fears become reality and the

U.K. votes to exit the European Union.

One of the biggest beneficiaries of disquiet that Briton’s could opt to leave the EU at its June 23 referendum, is gold.

Gold futures

GCQ6, +0.02%

are set to rise as much as 8.5%

from current levels, according to James Butterfill, head of research

and investment strategy at ETF Securities.

“Brexit

would be very beneficial for shorting sterling and we will probably see

a big pick up in gold. In that scenario we think gold could hit $1,400

[an ounce],” he said on the sidelines of the Inside ETFs Europe

conference in Amsterdam.

“We’ve looked at previous risk events

and for instance when Greece nearly left the Eurozone [in the summer of

2015] we saw really elevated futures positioning. We are making the

assumption that we would see net longs for quite an extended period of

time in gold in a Brexit scenario,” he said. He stressed, however, that a

U.K. exit from the EU, or Brexit, isn't what he thinks will mostly

likely occur.

Early polling suggests that the vote next week

will be close. Recent surveys show an increase in support for the

“leave” campaign. Meanwhile, the bookmakers are still pointing to a

narrow win for the “stay” camp. That uncertainty is fueling jitters in

the financial markets. The pound

GBPUSD, +0.3543%

for example, has shaved off

2.5% against the dollar in June so far, while the U.K. blue-chip

benchmark, the FTSE 100 index

UKX, -2.01%

is down 4.4%.

Gold, on

the other hand has been one of the best performing assets with a 5.9%

rise this month. Since the beginning of 2016, the metal has rallied a

whopping 22%. That compares with a lackluster 1.6% gain for the S&P

500

SPX, -0.18%

and 12% drop in the Stoxx Europe 600 index

SXXP, -1.92%

Butterfill said ETF

Securities has seen an inflow of $2.6 billion into gold this year,

boosting the metal’s share of the company’s asset under management to

14%.

“I think it has happened for various reasons. One is

Brexit, another is a non-establishment presidential candidate in the

U.S.,” he said, referring to the presumptive Republican presidential

nominee, Donald Trump. He said the other concern is the Federal

Reserve’s interest-rate policy, which appears to be on track to remain

unchanged for the near term, a fact that would be supportive to gold

prices.

“These are three quite significant risk events, so that’s why we are seeing popularity with gold,” Butterfill said.

That

also means a rally to $1,400 an ounce would have legs and not just

translate into a short-term shaven trade, Butterfill said.

“I

was actually surprised when [Fed Chairwoman Janet Yellen] mentioned

Brexit for the first time in her speech last Monday. It’s clear they are

thinking about how much instability it creates. The implications could

have a domino effect with other fringe parties around Europe pushing for

a referendum. It’s not a nice investment environment,” he said.

The August contract for gold traded around $1,290 on Tuesday, the highest it has been since early May.

Appetite for quality assets is pushing bond yields to record lows

Getty Images

Cash has not been this popular with investors in nearly 15 years.

The last time fund managers hoarded this much cash, the Arizona

Diamondbacks defeated the New York Yankees 4 to 3 to win the World

Series.

Today the Diamondbacks and the Yankees are struggling in

their respective divisions, and by the amount of cash investors are

stocking away, one might think that they fear the global markets are

melting down too.

Cash positions rose to 5.7% in June from 5.5%

in May, the highest level since November 2001, as fund managers have

become increasingly bearish, according to a Bank of America Merrill

Lynch survey published Tuesday.

Worries

about “‘summer of shocks” stemming from Brexit—the potential U.K. exit

from the European Union—and low expectations for a new “radical”

stimulus from central banks to revive the global economy are prompting

managers to stock pile cash despite record high corporate and U.S. stock

prices, according to Michael Hartnett, chief investment strategist at

Bank of America Merrill Lynch. What do you consider the biggest ‘tail risk’?

Bank of America Merrill Lynch

A recent poll

by market research firm TNS showed that 47% of voters backed leaving

the EU, compared with 40% who wish to remain. That contrasts with two

thirds of fund managers surveyed by Bank of America who believe that a

Brexit is “unlikely” or “not at all likely.” That disparity in so-called

Brexit outcomes highlights the shocks that some investors are bracing

against.

Brexit has emerged as the

single biggest risk ahead of the June 23 referendum to decide whether

the U.K. will remain a part of the EU. Global stock markets have swooned

as investors shy away from risk averse amid the uncertainty.

Bank

of America’s “Risk & Liquidity Index” fell to 32 in June versus 34

last month, the lowest in four years, underscoring the weak demand for

risky assets such as stocks. BofAML Risk and Liquidity Index

Bank of America Merrill Lynch

This level of risk is

normally consistent with a recession, according to Hartnett. Even so,

expectations for global growth jumped to a six-month high in June with

23% of respondents projecting a stronger economy in the next 12 months,

he said.

Meanwhile, the most crowded trade at the moment is

investors gobbling up high-quality assets, according to 27% of fund

managers. The preference for comparatively less risky investments has

led to a rally in government bonds, pushing the yield on the 10-year

benchmark German bond

TMBMKDE-10Y, +2,000.00%

into negative territory for the first time ever. The yield on the U.S. benchmark 10-year Treasury note

TMUBMUSD10Y, +0.32%

also was under pressure,

sliding 1.5 basis points to 1.601%, its lowest since November 2012. What do you think is currently the most crowded trade?

Bank of America Merrill Lynch

Still, despite the gloomy

tone of the report, there is a reason to be optimistic, Hartnett notes,

citing the average cash level above 4.5%. That move tends to serve as a

contrarian buy signal for stocks whereas when it drops below 3.5%, it is

a contrarian sell sign, he said.

In 2006, western leaders decided that Gaddafi's

oil was more important than his human rights record and complicity in

terrorism and lifted sanctions against Libya, creating a massive pool of

cash for the country that it turned into a sovereign wealth fund whose

business was aggressively courted by Goldman Sachs.

Goldman's reps -- referred to by Libyan officials as the "bank of

mafiosa" -- allegedly procured prostitutes for Libyan officials, took

them on private jet rides, and billeted them in five-star hotels.

Goldman procured more than $1.2B worth of the country's money to

gamble with. The bankers executed nine trades with this fund in 2008,

and lost almost all of it. But the bank still pocketed $200m in

commissions from these trades.

One Goldman exec, Youseff Kabbaj, was later given $4.5m in bonuses,

allegedly to secure his silence about his doubts regarding the trades.

Goldman's internal docs frankly discussed the naivete of the Libyan

national bankers, calling their sophistication "zero-level" and laughing

about how they'd "delivered a pitch on structured leveraged loans to

someone who lives in the middle of the desert with his camels."

The Libyans, whose country has melted down into a failed, bankrupt

state that is in a chaotic civil war that includes terrorists operating

with impunity, are suing Goldman Sachs. Goldman says it did nothing

wrong.

Goldman agreed an internship for Haitem Zarti, the brother of Mustafa

Zarti, the LIA’s former deputy chief, which the LIA argues was intended

to influence decisions by the investment fund.

According to the skeleton argument presented to the court by the LIA:

“Mr Kabbaj took Haitem Zarti on holidays to Morocco on various

occasions. Mr Kabbaj also took him to Dubai for a conference, with the

business class flights and five-star accommodation being paid by Goldman

Sachs. Documents disclosed by Goldman Sachs show that during that drip

Mr Kabbaj went so far as to arrange for a pair of prostitutes to

entertain them both one evening.”

The LIA said the internship “has been and may still be the subject of

investigation” by the Securities and Exchange Commission in the US.

Right out of the gate, I want to thank everyone who took time out

of their busy schedules to tune in to our gold webcast last Wednesday. I

also want to thank Aram Shishmanian, CEO of the World Gold Council,

for joining me as our special guest. His deep insights into gold

investing were well articulated and highly appreciated. If you happened

to miss it live, I urge you to catch the replay, which we’ll be posting

on usfunds.com soon. Look for it!

If you’re a serious investor—and because you’re reading this, I have

to assume that you are—gold is looking more and more like a crucial

trade. Fewer than two weeks remain before United Kingdom voters decide

on whether the country will continue to be a member of the European

Union (EU) or become the first-ever to leave it. The “Brexit,” as it’s

come to be known, is arguably the most consequential political event of

2016—perhaps even more so than the U.S. presidential election in

November—with far-reaching implications.

Should the U.K. leave, it will certainly underline the question many

people have about the EU’s viability. And remember, this is a group of

countries that collectively has the world’s second largest gross

national product (GDP), followed by China.

But whatever happens, “the European Union is not going to remain the

same,” as Aram put it during the webcast. “The euro is still very

unstable, and I think we could easily see an environment in which trade

barriers will increase and currency wars will increase. Regrettably, we

could have a weaker global economy.”

With this as the threat, “gold’s role is one of wealth protection,” Aram said.

Taking Precautions Against an Unknowable Future

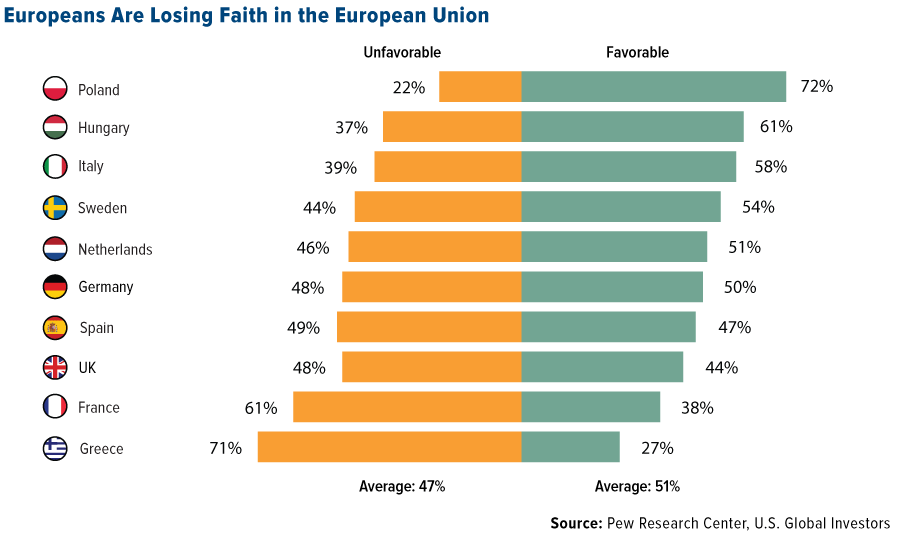

Even Europeans are beginning to lose confidence in the European

experiment. The Pew Research Center recently polled nearly 10,500

Europeans from 10 separate EU countries on their favorability of the

28-member bloc. Nearly half of all respondents—47 percent—held an

unfavorable view.

Trust in the European Central Bank (ECB) continues to falter as well. In a blistering note titled “The ECB must change course,”

Deutsche Bank called out the central bank for “threatening the European

project as a whole for the sake of short-term financial stability.” The

ECB’s actions have “allowed politicians to sit on their hands with

regard to growth-enhancing reforms.” The longer the bank persists with a

negative interest rate policy, the more damage it will inflict upon

Europe, Deutsche added.

Meanwhile, Frankfurt-based Commerzbank is considering stashing

physical cash in pricey vaults instead of keeping it with the ECB, whose

policies are cutting into bank profitability.

Speaking to the World Gold Council’s Gold Investor newsletter this month, former Governor of the Bank of England Mervyn King

criticized the ECB’s negative rate policy, saying: “If you repeatedly

bring down interest rates to try and persuade people to spend today

rather than tomorrow, it works for a while. But they become increasingly

resistant to being asked to spend their resources now rather than save

for the future.”

Like Aram and others, Governor King sees gold as a likely solution.

“There is clearly a need to take some precautions against an unknowable

future,” he said, which is the same argument for having health

insurance.

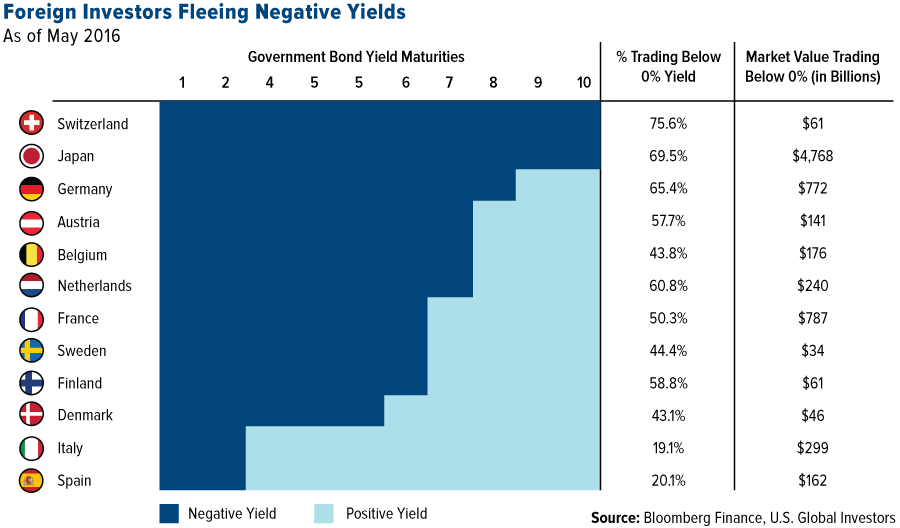

Negative rate policies are having a huge effect on bond yields, as

you can see below. Over $10 trillion worth of government debt across the

globe carried a negative yield as of the end of April. (In a tweet last

week, legendary bond guru Bill Gross

called it “a supernova that will explode one day.”) In Switzerland,

three quarters of all government bonds right now actually charge

investors interest. Real harm is being done to retirees, who have had to

pick up part-time work at Walmart or become Uber drivers to offset lost

interest on their savings and pensions.

This is prompting investors to look elsewhere, including the U.S.

municipal bond market, which has attracted $632 billion in assets this

year alone as of June 1. Of that amount, more than $22 billion has

flowed into muni mutual funds,

the best start to a year since 2009. Between that year and the end of

2015, the amount of U.S. municipal debt held by foreign investors

climbed 44 percent, validating its appeal as an investment with a

history of little to no drama, even during times of economic turmoil and

periods of rising and lowering interest rates.

$1,400 Gold this Summer?

Joining Aram in seeing the Brexit as further proof of impeding

economic troubles is billionaire investor George Soros. After a hiatus

of conducting any personal trading, the 85-year-old is back in the

game—this time with some bearish investments. In the first quarter, he

purchased a $264 million stake in Barrick Gold,

the world’s largest gold producer, and a million shares in precious

metals streaming company Silver Wheaton. It appears he’s added to both

positions, indicating a bet against the broader equity market.

Now, with a Federal Reserve rate hike looking more and more unlikely

this month, gold is expected to resume its bull run, according to

Australia and New Zealand Bank Group (ANZ) commodity strategist Daniel

Hynes. This, along with a possible Brexit, could push the yellow metal

to $1,400, a price we haven’t seen in three years this month.

Paradigm Capital also sees the rally picking up where it left off in

May, noting that gold’s trajectory so far this year resembles the one it

took in 2002, the first full year of the last bull market, which

carried the metal to $1,900 in 2011. “The resemblance is rather

striking,” Paradigm writes.

The investment dealer forecasts gold to reach nearly $1,400 by

year-end after a dip in October. It also maintains its position that

this particular bull run will peak at $1,800 sometime during the next

three to four years.

Whether or not this turns out to be the case is beside the point.

Savvy investors—not to mention central banks and governments—recognize

gold’s historical role in minimizing the impact of inflation, negative

rates and currency depreciation. This is what I call the Fear Trade, and

I always advocate up to a 10 percent weighting in gold that includes gold stocks as well as bullion, coins and jewelry.

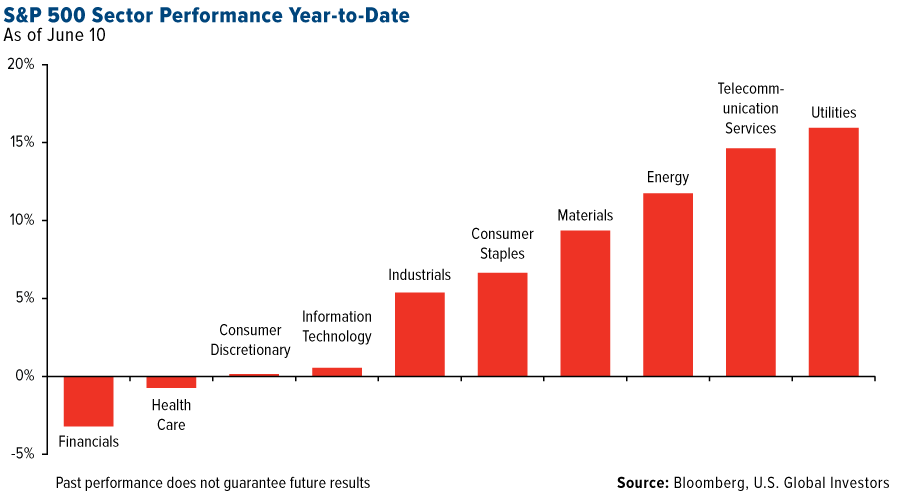

Catching Up with Sectors and Industries

Because we’re near the halfway mark of 2016, I thought you’d be

interested to see what the top performing sectors and industries were

for the year so far.

As for sectors, utilities is on top, delivering more than 15 percent

so far. Jittery investors, worried about slow global growth and

geopolitical threats, have moved into defensive stocks such as water and

electricity providers and telecommunications companies, many of which

offer steady dividends in a low-yield world. Financials, as you might

imagine, have been hurt by interest rate uncertainty.

Below I’ve highlighted the 10 best performing industries for the

year, and interestingly enough, metals and mining companies,

particularly those involved in the gold space, lead all others. Spot

gold is up 20 percent so far, but amazingly gold miners have doubled

investors’ money. Metals and mining companies have rallied more than 53

percent.

Many of the top-performing companies this year had some of the

biggest declines last year because of impaired balance sheets. To

maintain their performance long-term, they will need to show earnings.

June 11, 2016 – Following an evaluation of credit card

transaction fees in Canada and the rest of the world, we have concluded

the fees applied to Visa credit card purchases remain unacceptably high.

Walmart’s purpose is to save customers money so they can live better.

We are committed first and foremost to this purpose, which requires us

to keep costs as low as possible.

To ensure we are taking care of our customers’ best interests and

delivering on our promise of saving customers money, we constantly work

to reduce our operating costs, including credit card fees.

Unfortunately, Visa and Walmart have been unable to agree on an

acceptable fee for Visa transactions. As a result we will no longer

accept Visa in our stores across Canada, starting with our stores in

Thunder Bay, on July 18, 2016. This change will then be rolled out in

phases across the country. To keep prices low we continuously assess opportunities to

lower our operating expenses. Walmart Canada pays over $100 million in

fees to accept credit cards each and every year. Lowering costs such as

these is necessary for us to be able to keep our prices low and continue

saving our customers money.

Customers will continue to be able to use other forms of payment

including cash, Interac debit, MasterCard, Discover, and American

Express.

We sincerely regret any impact this will have on our customers who

use Visa and remain optimistic that we will reach an agreement with

Visa.

The price of rock-solid German government bonds has rocketed over fears of a possible Brexit.

Interest rates have fallen to record lows meaning investors are looking for safe havens to park their cash.

As investors flock to place money in German government 10-year bonds their price has risen

The

bonds, which are considered a benchmark of financial security, known as

Bunds, are now not paying any money back because demand is too high.

Today the Bund yielded minus 0.028 percent - meaning it was costing anyone who held the investment.

+1

As investors flock to place money in German government 10-year bonds their price has risen (German parliament pictured)

Ditching

any hope of a return on their investment now seems a reasonable price

to pay to escape the uncertainties of falling stock markets or volatile

commodities and currencies.

The

factors driving the current rally in Bund prices are concerns about the

global economy, rock-bottom inflation in the Eurozone and fears about a

possible Brexit.

Polling

for weeks has placed the Leave campaign ahead of the Remain side with

the British referendum now little more than a week away.

DeKaBank

economist Ulrich Kater said: 'A huge driving factor behind the current

price trend is the heightened uncertainty over a possible Brexit, which

is driving investors into the safe haven of German sovereign bonds.'

Interest

rates on sovereign debt have been low for some time as central banks

snap up government bonds from investors in an effort to boost economic

growth.

Be

it in Japan, the United States, Switzerland or Britain, the rate of

return for sovereign bonds of most major industrialised nations are

striking new record lows in day-to-day trading.

German chancellor Angela Merkel

'The

drop in yields below the zero mark once again shows the immense

challenges currently facing global financial markets,' Kater said.

'Weak

growth is pulling down inflation expectations even further. Central

banks are trying to counter falling inflation expectations using

aggressive monetary policy,' he said.

The

European Central Bank has slashed its key interest rates to zero and

launched a massive bond-buying programme known as quantitative easing

(QE) in a bid to get the eurozone economy back on its feet and push

inflation higher.

LBBW

analyst Werner Bader said: 'Fears that Britain will quit the EU has

killed off any willingness to take risks in European capital markets.'

'Risk aversion and scarcity remain the key driving forces for market activities and valuations.'

Germany's

own finances have benefitted from its safe-haven status in recent

years, because with investors favouring national sovereign debt,

borrowing rates in Europe's biggest economy have come down.

The

government has seen its annual interest payments fall from more than 40

billion euros ($45 billion) per year in 2008 to 21 billion euros in

2015.

The

reduced debt servicing costs enabled Germany to balance its budget in

2014 for the first time since 1969 and a year ahead of target.

The finance ministry declined to comment on the drop in Bund yields today.

A

spokesman for the German national financial agency said the drop to

negative yields should not be seen in terms of either good or bad.

'The

government's debt management is done on a long-term perspective. The

current level of yields is of secondary importance,' he said.

'The main aim is to reach a sustainable balance between costs and reliability of planning.'

But

from the taxpayers' point of view, 'negative yields are certainly

pleasing because they reduce interest payments in the federal budget.'

Getty Images

Getty Images

Bank of America Merrill Lynch

Bank of America Merrill Lynch

Bank of America Merrill Lynch

Bank of America Merrill Lynch

Bank of America Merrill Lynch

Bank of America Merrill Lynch