Today’s AM fix was USD 1,611.50, EUR 1,246.62 and GBP 1,059.99 per ounce.

Yesterday’s AM fix was USD 1,608.75, EUR 1,246.42 and GBP 1,059.43 per ounce.

Silver is trading at $29.05/oz, €22.52/oz and £19.19/oz. Platinum is trading at $1,588.50/oz, palladium at $751.00/oz and rhodium at $1,250/oz.

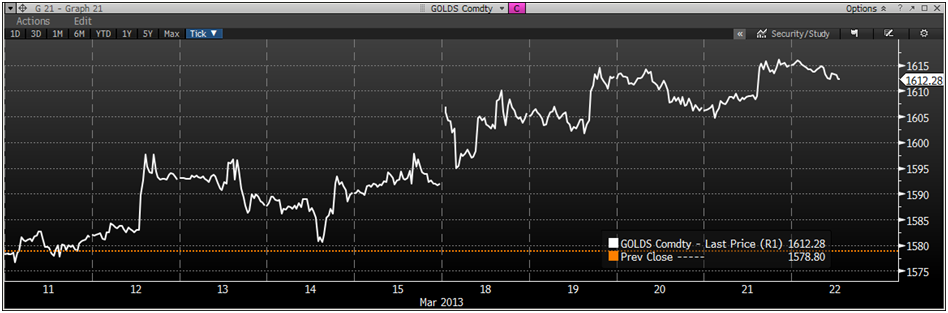

Gold climbed $8.70 or 0.43% and closed yesterday at $1,614.40/oz. Silver reached $29.31 and finished +1.29%.

Cross Currency Table – (Bloomberg)

Gold is slightly lower in all major currencies this morning but remains near a 4 week high, underpinned by safe haven demand due to concern of a financial meltdown in Cyprus and the risk of contagion in other European countries.

Gold bullion is headed for its second consecutive weekly rise and its biggest weekly rise in four months.

Gold is 1.4% higher in dollar terms and 2.5% higher in euro terms. In British pounds, gold has consolidated after the gains seen in sterling in recent weeks and is 0.8% higher for the week.

The clock is ticking for Cyprus to come up with a solution to clinch an international ‘bailout’, otherwise it could face the collapse of its financial system and exit from the euro zone.

There is a slow but creeping realisation that this crisis will almost certainly escalate. Financial contagion could ensue due to risks to payment systems and bank deposits which are often guaranteed by near insolvent governments.

Events in Cyprus look like that they could precipitate bank runs in Greece, Spain and Italy with obvious negative ramifications for the entire EU banking and financial system.

Senior euro zone officials acknowledged in a confidential conference call yesterday that they were “in a mess” and discussed imposing capital controls to insulate the currency area from a possible collapse of the Cypriot economy.

In Brussels, a senior European Union official told Reuters that an ECB withdrawal would mean forcing Cyprus to abandon the euro.

Gold In EUR, 10 Day – (Bloomberg)

The ECB has warned of the “great danger” of a bank run once banks reopen next week and has said that they may enforce capital controls overriding the government of Cyprus. Other draconian restrictions on people’s private property include an indefinite “freezing” of savings accounts, making bank or wire transfers dependent on central bank approval and lower ATM and bank deposit withdrawal limits.

While, the capital controls will be designed “so that citizens have access to sufficient cash to go about their lives”, they are likely to lead to a further collapse of consumer confidence in Cyprus and the collapse of commerce as businesses are greatly hampered in carrying out every day business activities.

This is not the first time this has happened in the EU and unfortunately, it will not be the last time.

Only last June, the Bank of Italy authorized the suspension of payments by Bank Network Investments Spa (BNI) without communicating anything to depositors. The BNI, a large Italian bank, suspended operations and clients with bank accounts could not write checks, pay bills, make mortgage payments, and use ATMs or debit and credit cards.

At the time, it was reported that not alone was the EU considering imposing a limit on the amount of money that can be withdrawn from ATMs but they were also considering imposing border checks and introducing currency controls to stop a flight of capital out of European countries.

As well as limiting cash withdrawals and imposing capital controls, the EU discussed suspending the Schengen Agreement, which allows for visa-free travel among 26 countries, including most of the EU, though not Britain and Ireland.

While EU officials may again manage to patch things up and not implement such extreme measures in the short term, unfortunately extreme measures seem quite likely in the long term given the scale of the crisis in the EU. There is also the risk of Japan, the UK and U.S. seeing their various debt crises deepening in the coming months and similar capital controls are more than possible.

These are risks that we have long warned of and it gives us no pleasure to see them come to pass.

Gold In USD, 10 Day – (Bloomberg)

However, people who own physical bullion in their possession and in safe storage internationally remain positioned and prepared for these threats.

These real risks have huge implications and ramifications that most have yet to fully consider and comprehend.

The silly debate as to whether gold is a safe haven or not, or a bubble or not, will be seen for what it is very soon.

Those, such as Paul Krugman, Nouriel Roubini and Warren Buffett, who have suggested gold is a barbaric relic, is a bubble and is not a safe haven, and have dissuaded investors from diversifying some of their wealth into gold, will be shown to have misled investors and savers and will lose credibility.

They will no doubt engage in some furious back pedalling and claim that “nobody saw this coming” when indeed there have been many financial and economic analysts warning about exactly these risks for years.

Rather than sitting nervously and passively and awaiting the coming financial dislocations and expropriations, investors and savers need to be prepared for the uncertain financial scenarios that seem increasingly likely.

One of the most published academics on gold in the world, Dr Brian Lucey of Trinity College Dublin (TCD) wrote yesterday that “the research evidence is that gold is usually a safe haven asset”.

Lucey pointed out how physical gold is financial insurance or a hedge against political uncertainty:

“Interestingly financial gold, such as ETFs etc are useful as safe havens against economic events and physical gold against political events. Both are in play in Cyprus and so the safe haven nature of gold should continue to provide comfort for purchasers.”

Gold In GBP, YTD – (Bloomberg)

Hoping for the best, but preparing for less benign scenarios remains prudent.

NEWS

Gold Seen Extending Rebound as Cyprus Revives Bulls – Bloomberg

Gold heads for biggest weekly rise in 4 months on Cyprus – Reuters

Gold futures pause after gains – Market Watch

Shanghai Bourse Mulls After-Hours Trade in Gold, Silver – Fox Business

COMMENTARY

Video: Gold Fundamentals “Absolutely Intact” – $1,800/oz By September – Business Week)

Getting Beyond the Fed – NY Sun

“It Is Only In Safe Hands If It Is Kept In Switzerland” – Zero Hedge

President Nixon: The Man Who Sold the World Fiat Money – CFA Institute

Could a “Cyprus-Like” Situation Happen in US? It Already Has – Sense on Cents

http://www.senseoncents.com/2013/03/could-a-cyprus-like-situation-happen-in-us-it-already-has/

Video: Texas May Start Hoarding Gold…Secession Next? – Yahoo

For breaking news and commentary on financial markets and gold, follow us on Twitter.

A

rightwing group has submitted more than 106,000 signatures to the

federal authorities, seeking a vote on stopping the sale of gold

reserves held by the Swiss National Bank (SNB). It also wants gold bars

stored in the US to be returned.

A

rightwing group has submitted more than 106,000 signatures to the

federal authorities, seeking a vote on stopping the sale of gold

reserves held by the Swiss National Bank (SNB). It also wants gold bars

stored in the US to be returned.

Huffington Post – by Mark Gongloff

Huffington Post – by Mark Gongloff The Telegraph – by Richard Spencer, Nicosia, Bruno Waterfield in Brussels, Tom Parfitt in Moscow and Alex Spillius

The Telegraph – by Richard Spencer, Nicosia, Bruno Waterfield in Brussels, Tom Parfitt in Moscow and Alex Spillius