If you hang out much with thinking people, conversation eventually turns to the serious political and cultural questions of our times. Such as: How can the Americans remain so consistently brain-fucked? Much of the world, including plenty of Americans, asks that question as they watch U.S. culture go down like a thrashing mastodon giving itself up to some Pleistocene tar pit.

But a more reasonable explanation is that, (A) we don't even know we are doing it, and (B) we cling to institutions dedicated to making sure we never find out.

As William Edwards Deming famously demonstrated, no system can understand itself, and why it does what it does, including the American social system. Not knowing shit about why your society does what it makes for a pretty nasty case of existential unease. So we create institutions whose function is to pretend to know, which makes everyone feel better. Unfortunately, it also makes the savviest among us -- those elites who run the institutions -- very rich, or safe from the vicissitudes that buffet the rest of us.

Directly or indirectly, they understand that the real function of American social institutions is to justify, rationalize and hide the true purpose of cultural behavior from the lumpenproletariat, and to shape that behavior to the benefit of the institution's members. "Hey, they're a lump. Whaddya expect us to do?"

Doubting readers may consider America's health institutions, the insurance corporations, hospital chains, physicians' lobbies. Between them they have established a perfectly legal right to clip you and me for thousands of dollars at their own discretion. That we so rabidly defend their right to gouge us, given all the information available in the digital age, mystifies the world.

Two hundred years ago no one would have thought sheer volume of available facts in the digital information age would produce informed Americans. Founders of the republic, steeped in the Enlightenment as they were, and believers in an informed citizenry being vital to freedom and democracy, would be delirious with joy at the prospect. Imagine Jefferson and Franklin high on Google.

The fatal assumption was that Americans would choose to think and learn, instead of cherry picking the blogs and TV channels to reinforce their particular branded choice cultural ignorance, consumer, scientific or political, but especially political. Tom and Ben could never have guessed we would chase prepackaged spectacle, junk science, and titillating rumor such as death panels, Obama as a socialist Muslim and Biblical proof that Adam and Eve rode dinosaurs around Eden. In a nation that equates democracy with everyman's right to an opinion, no matter how ridiculous, this was probably inevitable. After all, dumb people choose dumb stuff. That's why they are called dumb.

But throw in sixty years of television's mind puddling effects, and you end up with 24 million Americans watching Bristol Palin thrashing around on Dancing with the Stars, then watch her being interviewed with all seriousness on the networks as major news. The inescapable conclusion of half of heartland America is that her mama must certainly be presidential material, even if Bristol cannot dance. It ain't a pretty picture out there in Chattanooga and Keokuk.

The other half, the liberal half, concludes that Bristol's bad dancing is part of her spawn-of-the-Devil mama's plan to take over the country, and make millions in the process, not to mention make Tina Fey and Jon Stewart richer than they already are. That's a tall order for a squirrel brained woman who recently asked a black president to "refutiate" the NAACP (though I kinda like refutiate, myself). Cultural stupidity accounts for virtually every aspect of Sarah Palin, both as a person and a political icon. Which, come to think of it, may be a pretty good reason not to "misunderstimate" her. After all, we're still talking about her in both political camps. And the woman OWNS the Huffington Post, fer Christsake. Not to mention a franchise on cultural ignorance.

Cultural stupidity might not be so bad, were it not self-reproducing and viral, and prone to place stupid people in charge. All of us have, at some point, looked at a boss and asked ourselves how such a numb-nuts could end up in charge of the joint.

In my own field, the book biz, the top hucksters in sales and marketing, car salesman with degrees, are put in charge of publishing the national literature. Similarly, ex-Pentagon generals segue from killing brown babies in Iraq into university presidents and CEOs. Conversely, business leaders such as Donald Rumsfeld who fancy themselves as battlefield commanders and imagine their employees as troops to be "deployed," find themselves happily farting behind Pentagon desks. On the strength of having mistaken Sun Tzu's The Art of War as a business text, they get selected by equally delusional national leaders to make actual war on behalf of the rest of us.

But the most widespread damage is done at more mundane operational levels of the American empire, by clones of the over promoted asshole in the corner office where you work. At least one study demonstrated that random selection for corporate promotions offset the effect significantly. Research again confirms what is common knowledge around every workplace water cooler in the country.

Save my spot in the gulag, I'm off to Wal-Mart

Cultural ignorance of one sort or another is sustained and nurtured in all societies to some degree, because the majority gains material benefit from maintaining it. Americans, for example, reap huge on-the-ground benefits from cultural ignorance -- especially the middle class Babbitry -- from cultural ignorance generated by American hyper-capitalism in the form of junk affluence.

Purposeful ignorance allows us to enjoy cheaper commodities produced through slave labor, both foreign, and increasingly, domestic, and yet "thank god for his bounty" in the nation's churches without a trace of guilt or irony. It allows strong arm theft of weaker nations' resources and goods, to say nothing of the destructiveness of late stage capitalism -- using up exhausting every planetary resource that sustains human life.

The American defense, on those rare occasions when one is offered, runs roughly, "Well you commie bastard, I ain't ever seen a sweatshop and I got no Asian kids chained in the basement. So I've got what the guvment calls plausible deniability. Go fuck yerself!"

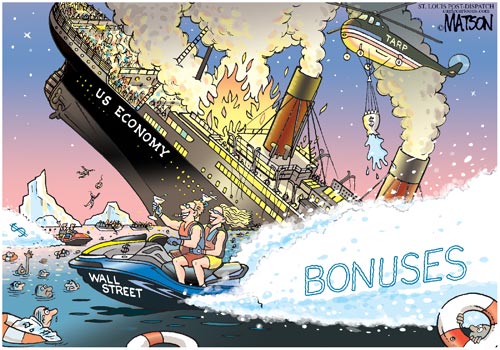

Uh, don't look now, but the banksters own your ass, your country has become a work gulag/police state and the most of the world hates you.

Such a thriving American intellectual climate enables capitalist elites to withhold and ration vital resources like health care simply by auctioning it off to the richest. Americans fail to grasp this because the most important fact (that a helluva lot of folks can't afford to bid, and therefore get to die early) never gets equal play with capitalist political propaganda, to wit, that if we give free medical attention to low income cleft palate babies, a wave of Leninism will seize the nation. That is cultural ignorance. We breathe the stuff every day of our lives.

But when Americans too poor to buy health care nevertheless vote to retain the corporate auction process, that is cultural stupidity.

(Let us now pause to clutch our hair in our fists and scream AAAAAAGGGGGHHHHH!)

Like the old song says, "Them that don't know don't know they don't know." I venture to say that even if they did, they would not know why. Primary truths elude us because of the junk affluence and propaganda. We get buried under a deluge of commodities that suggest we are all rich, or at least richer than most of the world. A mountain range of cheap shoes, cars, iPods, ridiculous amounts of available foodstuffs, and the entire spectacle of engorgement defines, and is enforced as, "quality of life" under materialistic commodities capitalism. The goods we have in our clutches trump the philosophical, or even the most practical considerations. "I may die early eating unidentified beef byproducts soaked in waste chemicals, but I'll die owning a 65-inch HDTV and a new five speed automatic Dodge Durango with a 5.7 L Hemi V8 under the hood!"

Even the threat of toasting planetary life is not enough to shake Americans loose from this disconnect. As Professor Emeritus of Natural Resources and Ecology & Evolutionary Biology Guy R. McPherson points out, "79.6% of respondents to a Scientific American poll are unwilling to forgo even a single penny to forestall the risk of catastrophic climate change. Scientific American readers undoubtedly are better informed than the general populace. And yet they won't pay a thing to avoid extinction of our species. Kinda makes you warm and fuzzy all over, doesn't it?"

Let us pray the next generation is a tad sharper.

Taser the tots

The "American Lifestyle," increasingly suspect as it is these days, is heavily soldiered and policed in the name of keeping we self-defined lotus eaters safe and secure from a jealous outside world. Which according to cultural consensus is a world that is at this very moment is stuffing its under drawers with explosives and buying plane tickets to Moline. Cultural ignorance dictates that the best way to stop foreign terrorists flying into the country is by humiliating American citizens flying out of the country. Go ahead, grope me, X-ray my dick and for god sake don't let anyone bring a large bottle of shampoo on board. In an obedient, authority worshipping police state, physical insult and surveillance are proof of safety.

It's profitable too, and not just for scanner manufacturers. The brouhaha over body scanners and crotch groping provide media with titillating fuel for ratings, thereby driving up TV advertising rates, which is passed on in the price of products we buy. So we pay to be insulted, have the hell scared out of us, and to unknowingly have our behavior shaped. Under American style capitalism, this mobius strip of cultural ignorance is called a win-win situation for everybody.

This also conveniently distracts us from the everyday human insult we practice on one another, as a result of state manufactured cultural misinformation -- fear. Ten years of orange alerts and post 9/11 fear mongering have led us to draw some paradoxical cultural conclusions.

Let us briefly careen off into one of these paradoxes. For instance, that we can taser our way to domestic security and tranquility. Yes, it's ugly business, but tasing the citizenry must be done. And besides, in these days of high unemployment, it's a paycheck for somebody -- usually, the guy who sat behind us in grade school happily eating chalk.

With taser packing police officers in thousands of schools, even grade schools (a weird enough cultural statement to begin with -- needless to say, the resulting deaths and injuries of school kids have personal injury lawyers shouting eureka and contemplating new recreational sail craft moored at Martha's Vineyard. Such are the rewards of righteous works through cult-ig.

In any case, the chance at a juicy lawsuit is accepted as a satisfactory offset to any screaming and writing in our school hallways. What are 50,000 volts and a little nerve damage, compared to a shot at paying off the credit cards, upgrading the family ride, and maybe remodeling the kitchen too?

But we gotta stick to the subject of cultural ignorance here, mainly because I wrote the title first and am determined to maintain some illusion of a theme here, or at least bullshit the reader into thinking that I have.

Soooo . . .

It can be safely said that cultural ignorance consists of the rational, sensible questions that never get asked. But it also includes the weird ones that are. For instance, one of the questions asked regarding tasering school kids is: What is the allowable weight range of a child to be tased? (Taser manufacturers say 60 pounds.) Somehow, by this geezer's prehistoric reasoning, that sounds like the wrong question, not to mention one that by its nature leads us away from the cultural truth.

The truth is that we live in a society which sanctions semi-electrocution of its own children on the grounds that it is not fatal, and therefore not true electrocution. It springs from the same streak of cultural cruelty that deems semi-drowning by water boarding not to be torture because it is seldom fatal.

This is not to be uncharitable to American communities willing to pony up tax money for school tasers. They've amply demonstrated their affectionate commitment to their children by bringing creationism and pizza-for-breakfast into the schools. But there remains the question, "What kind of community comes up with the idea of tasering its own children?"

The information racketeers

It is the job of our combined institutions to manage cultural information so as to deny the harmful aspects of the rackets they protect through legislation and promote through institutional research. That's why research shows that cell phone microwaves cause long term memory loss in rats, but do not harm people. Evidently, we are of different, more bullet proof mammalian material.

Our hyper capitalist system, through command of our research, media and political institutions, expands upon and disseminates only that information which generates money and transactions. It avoids, neglects or spins the hell out of information that does not. And if none of those work, the info is exiled to some corner of cyberspace such as Daily Kos, where it cannot change the status quo, yet can be ballyhooed as proof of our national freedom of expression. Here come the rotten eggs from the Internet liberals.

Cyberspace by nature feels very big from the inside, and its affinity groups, seeing themselves in aggregate and in mutual self reference, imagine their role bigger and more effective than it is. From within the highly directed, technologically administrated, marketed-to and propagandized rat cage called America, this is all but impossible to comprehend. Especially when corporate owned media tells us it is.

Take the world recent shaking WikiLeak's "revelations" of Washington's petty misery and drivel, which are scarcely revelations, just more extensive details about what we all already knew. Come on now, is it a revelation that Karzai and his entire government is a nest of fraudulent double-crossing thieves? Or that the US is duplicitous? Or that Angela Merkel is dull? The main revelation in the WikiLeaks affair was the U.S. government's response -- which was to bring US freedom of speech policy firmly in line with China's. Millions of us in cyber ghettoes saw it coming, but our alarm warnings were shouted inside a cyberspace vacuum bell jar.

Bear in mind that I am writing this from outside the US borders and media environment, where people watch the WikiLeaks story unfold more in amusement than anything else.

The WikiLeaks affair is surely seismic to those whose asses ride on the elite diplomatic intrigues. But in the big picture it will not change the way the top lizards in global politics, money and war have done business since the feudal age -- which is to say with arrogant disregard for the rest of us. Theirs is an ancient system of human dominance that only shifts names and methodologies over the centuries. Two years from now, little will have changed in the old, old story of the powerful few over the powerless many. In this overarching drama, Obama, Hillary and Julian Assange are passing players. Watching the sweaty, fetid machinations of our overlords with such passionate involvement only keeps us from seeing the big picture -- that they are the players and we are the pawns.

Still, I for one am in favor of giving Assange the Médaille militaire, the Noble Prize, 15 virgins in paradise and a billion in cash as a reward for his courage in doing damned well the only significant thing that can be done at this time -- momentarily fucking up government control of information. But "potentially stimulating a new age of U.S. government transparency," (BBC) it ain't."

Which brings us to back to the question of cultural ignorance. For ten points, why was Julian Assange forced to do what the world press was supposed to be doing in the first place?

Bulletin: PayPal has caved to government pressure to pull WikiLeak's PayPal account for contributions. However, the feds generously let PayPal keep its porn and prostitution clients.

The transparency scam

It is a form of cultural ignorance to believe that at some point or other, we were more in charge and that our government was somehow more transparent in the past. Societies declining into obsolescence understandably resist looking forward, and hang onto their past mythologies. Consequently, both liberals and conservatives in America feed on myths of political action which died in Vietnam. The results are ludicrous. Tea Partiers attempt to emulate the 1960s protest gatherings by staging rallies sponsored by the richest beneficiaries of the status quo. For the average TP participant, the goal, near as I can tell, is to "start a new American Revolution," by wearing foodstuffs, screaming, threatening, and voting for nitwits. Media pundits proclaim the Tea Party "a historic populist movement."

Neither populist, nor authentic movement, the Tea Party may yet prove historic, however, by seriously fucking things up more than they already are. Spun entirely from manufactured spectacle (and thus void of cohesive political philosophy or internal logic), the Tea Party lurches across the political landscape bellowing at the cameras and collecting the victims of cultural ignorance in sort of a medieval idiots crusade. But to the American public, seeing the Tea Party on television is proof enough of relevancy and significance. After all, stuff doesn't get on TV unless it's important.

Progressives also fancy a revolution, one in which they participate through the Internet petitions, and media events such as the risk free Jon Stewart Rally to Restore Sanity, where no one risked even missing an episode of Tremaine. Seeing people like themselves on television was proof fighting the good fight. The Stewart rally was nonetheless culturally historic; we will never see a larger public display of post modern irony congratulating itself.

In the historical view, cultural ignorance is more than the absence of knowledge. It is also the result of long term cultural and political struggle. Since the industrial revolution, the struggle has been between capital and workers. Capital won in America and spread its successful tactics worldwide. Now we watch global capitalism wreck the world and attempt to stay ahead of that wreckage clutching its profits. A subservient world kneels before it, praying that planet destroying jobs will fall their way. Will unrestrained global capitalism, with all the power and momentum on its side and motivated purely by machinelike harvesting of profits, reduce the faceless masses in its path to slavery? Does a duck shit in a pond?

Meanwhile, here we are, American riders on the short bus, barreling into the Grand Canyon. With typical American gunpoint optimism, we've convinced ourselves we're in an airplane. A few smarter kids in the back whisper about hijacking and turning the bus around. But the security cop riding shotgun just strokes his taser and smiles. Not that yours truly has the ass to take on the security surveillance state. Hell no. I jumped out the window when the bus shot past Mexico.

What America needs is some balls

GOP honcho Mitch O'Connell says what America needs is for Republicans to finish beating the snot out of Obama, and strengthen the already rich by eliminating taxes for them and shifting the burden onto us. Obama says America needs to find bipartisan cooperation with the party of ruthlessness. Elton John says that America needs more compassion (Thanks, we never noticed).

What America really needs is a wall-to-wall people's insurrection, preferably based on force and fear of force, the only thing oligarchs understand. And even then the odds are not good. The oligarchs have all the legal power, police, jails and prisons, surveillance and firepower. Not to mention a docile populace.

Shy of open insurrection, a nationwide refusal to pay income taxes would certainly shake things up. But broader America is happy in the sense they know happiness as an undisturbed regimen of toil, stress and commodity consumption. Despite the way it looks in the news, most Americans remain untouched by foreclosure, bankruptcy and unemployment. So risking loss of their work-buy-sleep cycle in an insurrection looks to be sheer lunacy to them. Like cows, they are kept comfortable in the pure animal sense to be milked for profit. Animal comfort kills all thoughts of revolution. Hell, half of mankind would be thrilled with the average American's present material situation.

And besides, revolutionary history does not exist for Americans. The 20th Century's successful revolutions in Russia, Germany, Mexico, China, and Cuba are wired into our minds as history's evil failures, because all but one were Marxist. (The only successful non-Marxist revolution of the 20th Century was Fidel Castro's Cuban Revolution).

So if we are talking change through revolt, we're necessarily talking about deconditioning because the thing we fear already has a life deep in our own consciousness. Deconditioning from cultural ignorance is at the heart of any insurrectionary politics.

Deconditioning also involves risk and suffering. But it is transformative, freeing the self from helplessness and fear. It unleashes the fifth freedom, the right to an autonomous consciousness. That makes deconditioning about as individual and personal act as is possible. Maybe the only genuine individual act.

Once unencumbered by self-induced and manufactured cultural ignorance, it becomes clear that politics worldwide is entirely about money, power and national mythology, with or without some degree of human rights. America still has all of the above to one degree or another. Yet for all practical purposes, such as advancing the freedom and the well being of its own people, the American republic has collapsed.

Of course, there is still money to be made by the already rich. So the million or so people who own the country and the government use their control to convince us that there is no collapse, just economic and political problems that need to be solved. Naturally, they are willing to do that for us. Consequently, the economy is discussed in political terms, because the government is the only body with the power to legislate, and therefore render the will of the owning class into law.

But politics and money are never going to fill what is essentially a public vacuum that is moral, philosophical and spiritual. (The latter was instantly recognized by fundamentalist Christians, disfigured by cultural ignorance, as they may be.) Not many ordinary Americans talk about this vacuum. The required spiritual and philosophical language has been successfully purged by newspeak, popular culture, a human regimentation process masquerading as a national educational system, and the ruthlessness of everyday competition, which leaves no time to contemplate anything.

Still, the void, the meaninglessness of ordinary work and the emptiness of daily life scares thinking citizens shitless, with its many unspeakables, spy cams, security state pronouncements, citizens being economically disappeared, and general back-of-the-mind unease. Capitalism's faceless machinery has colonized our very souls. If the political was not personal to begin with, it's personal now.

Some Americans believe we can collectively triumph over the monolith we presently fear and worship. Others believe the best we can do is to find the personal strength to endure and go forward on lonely inner plains of the self.

Doing either will take inner moral, spiritual and intellectual liberation. It all depends on where you choose to fight your battle. Or if you even choose to fight it. But one thing is certain. The only way out is in.

For governments, crises are opportunities, a fact well known among analysts of government. This fact is one reason why governments postpone taking actions to remedy what appear to the rest of us to be bad situations.

For governments, crises are opportunities, a fact well known among analysts of government. This fact is one reason why governments postpone taking actions to remedy what appear to the rest of us to be bad situations.