New national poll from Bloomberg.

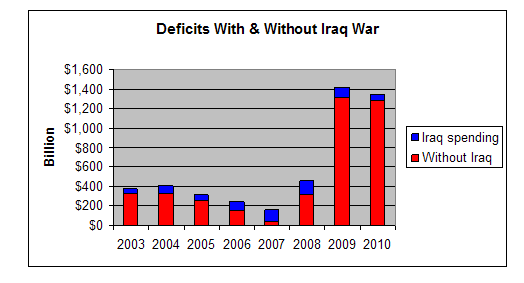

The answer is to cut defense. Here's an excerpt from a story on the Bush tax cuts.

I would have no objection to the 2-year extension had it been paid for - balanced by commensurate cuts in federal spending. The Pentagon would be a good place to start. But there were no spending cuts. Congress couldn't find the balls guts. So the tax cuts should have been allowed to expire.

The 2-year increase to the deficit because of the extension will be approximately $700 billion, about the price of TARP. The easy fix, that won't hurt anyone but the military, is to cut the Defense budget by 50% over the next 5 years.

---

Reprinted with permission.

Americans Want Deficit Cut, Entitlements Secured

Source - Bloomberg

Americans want Congress to bring down a federal budget deficit that many believe is “dangerously out of control,” only under two conditions: minimize the pain and make the rich pay.

The public wants Congress to keep its hands off entitlements such as Medicare, Medicaid and Social Security, a Bloomberg National Poll shows. They oppose cuts in most other major domestic programs and defense. They want to maintain subsidies for farmers and tax breaks like the mortgage-interest deduction. And they’re against an increase in the gasoline tax.

That aversion to sacrifice is at odds with a spate of recent studies, including one by President Barack Obama’s debt panel, that say reductions in Medicare, Social Security, military and other spending are necessary to curb a deficit that totaled $1.29 trillion in the fiscal year ended Sept. 30, or 9 percent of the gross domestic product.

“The idea that we can solve our structural-deficit problems merely by asking more of the well-off is totally unrealistic,” said David Walker, who was U.S. comptroller general from 1998 to 2008 and now leads a group advocating against deficits. “The math simply doesn’t work.”

According to the Dec. 4-7 poll, taken days after Obama’s commission sounded an alarm over the nation’s “unsustainable fiscal path,” the public still believes it’s more important to “minimize sacrifice” than to take “bold and fast” action to pare the $13.7 trillion national debt.

‘Deficit Cutting Hurts’

If anything, the poll shows that public concern over the deficit has ebbed: Forty-eight percent of Americans say the budget shortfall is “dangerously out of control,” down from 53 percent who said that in an October survey.

“The reality is deficit cutting hurts, and the American public is in no mood for further hurt than the slow economy and high unemployment is delivering,” J. Ann Selzer, president of Selzer & Co., a Des Moines, Iowa-based firm that conducted the nationwide survey.

Investors are worried about a widening of the budget gap. Treasuries tumbled for two days after Obama announced a plan to extend Bush-era tax cuts and reduce payroll taxes, stoking concern over more borrowing. The 10-year yield rose 35 basis points in its biggest back-to-back increase in more than two years. Treasuries rebounded yesterday on uncertainty over the prospects for the tax cuts. The 10-year Treasury yield slipped five basis points to 3.22 percent at 4 p.m. in New York.

Sacrificing the Rich

The one place Americans are willing to see sacrifice is in the wallets of the wealthy and Wall Street.

While they say they strongly support balancing the budget over the next 20 years, when offered a list of more than a dozen possible spending cuts or tax increases, majorities opposed every one of them except imposing a bigger burden on the rich.

A majority backs raising the cap on earnings covered by the tax on the Social Security retirement program above the current limit of $107,000. Two-thirds would means test Social Security and Medicare benefits. Six of 10 would end tax cuts for the highest-earning Americans. And 7 of 10 favor a tax on Wall Street profits.

“We give billions of dollars to these corporations, and in my eyes they pretty much just put it in their pocket,” said Donald Froemming, a 57-year-old independent voter and unemployed diesel gas mechanic from Moose Lake, Minnesota.

Divided on Taxes

While Republican congressional leaders have opposed increases in taxes paid by high-income families, sentiment among the party’s rank and file is mixed. Republicans are divided on eliminating the tax cuts for the wealthy, with 50 percent opposing and 47 percent supporting. An increase in the cap on earnings subject to Social Security taxes splits Republicans almost evenly.

The poll shows there’s little appetite across all parties and demographic groups for changes to entitlements.

Eighty-two percent of respondents opposed benefit cuts to the Medicare health-insurance system for the elderly, with about half of Republicans wanting to see both the current Medicare and Social Security systems preserved. Just 35 percent of all respondents back a system in which government vouchers would help people pay for their own health insurance.

“Nobody wants to fail to take care of children who need medicine or the elderly,” said Tea Party supporter Randy Thorman, 45, a high school social studies teacher in Pryor, Oklahoma. “We don’t want to throw people out without some type of help.”

Backing Social Security

Support for keeping the current structure of the Social Security program is strong, at 55 percent. Lower-earning Americans are especially averse to any big changes.

Cathy Freeman, a 64-year-old Republican and retired bookkeeper from Waco, Texas, said the deficit should be addressed by ending tax breaks for the wealthy and corporations, not slashing the entitlement programs her family relies on.

“We need to look at that before you start hurting the little guys,” Freeman said. “Let’s look at some things that aren’t fair in our system.”

A majority of 72 percent also opposes reducing benefits for the Medicaid health program for the poor. This is true even of Tea Party supporters who have built a movement around smaller government, with 66 percent against reducing Medicaid benefits. Seventy-two percent of those earning $100,000 or more also are opposed.

Raise the Cap

In Social Security, the only areas for change that have support are raising the cap on wages subject to the payroll tax and reducing benefits for the wealthy. The wealthy themselves are willing to sacrifice. Those making $100,000 or more are most supportive of raising the cap, at 59 percent. That compares with 45 percent of those making $25,000 or less.

Overall, 67 percent of Americans want means-testing and 51 percent think the payroll tax cap should be raised. Just 31 percent want to see cost-of-living increases trimmed and 37 percent say the government should gradually raise the age of Social Security eligibility to 69.

Partisan differences over the deficit are strong, with Republicans more than twice as likely as Democrats to see the fiscal situation as imperiled. Still, the shortfall is also a potential source of conflict within each party’s coalitions.

Tea Party supporters, who played a key role in Republican victories in the midterm elections, are more likely to back strong action than are rank-and-file Republicans; a 49 percent plurality favors a dramatic overhaul of Social Security, compared with 41 percent of Republicans. Tea Party backers want a Medicare overhaul by 52 percent to 43 percent, while Republicans narrowly prefer to keep the current system.

Splitting the Coalition

The deficit also divides the coalition Obama assembled to win the 2008 election. Political independents, whom he carried then, consider the deficit a more immediate threat than do Obama’s fellow Democrats. Fifty percent of independents said the deficit is “dangerously out of control” versus 29 percent of Democrats.

The poll suggests a possible opening for a new sales tax. Americans are split on a 6.5 percent national sales tax to bring down the deficit, with 46 percent in favor and 49 percent opposed.

Still, three-quarters of the country opposes a 15-cent gasoline tax across party lines. Even among those who want bold action, 7 out of 10 oppose a higher gas tax.

A freeze on nondefense discretionary spending, which some Republican congressional leaders have proposed, is opposed by 53 percent against 43 percent in favor. Cuts in defense spending are opposed by 51 percent versus 45 percent in favor.

The Bloomberg National survey of 1,000 U.S. adults has a margin of error of plus or minus 3.1 percentage points.

---