Wolf Richter

wolfstreet.com,

www.amazon.com/author/wolfrichter

How the government deceives us on inflation, as housing costs soar.

For inflation lovers, the headline numbers that the Bureau of Labor

Statistics reported today was benign: The Consumer Price Index for All

Urban Consumers (CPI-U) rose 0.2% in May, seasonally adjusted. Over the

last 12 months, not seasonally adjusted, the index rose 1.0%.

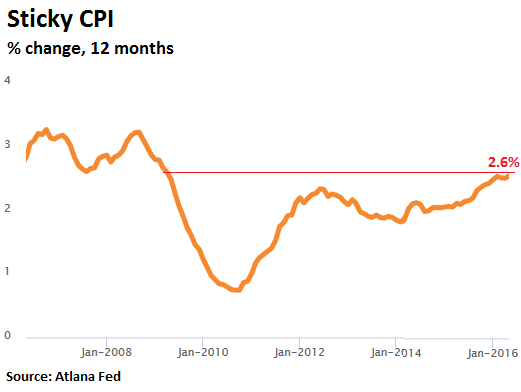

The Atlanta Fed’s “sticky-price” CPI – “a weighted basket of items

that change price relatively slowly,” as it says – wasn’t quite that

benign. It rose 2.6% for the 12-month period, the hottest increase since

April 2009!

So prices are rising. Not that

this is a surprise to anyone trying to make ends meet on a monthly

basis. But now even the official numbers are beginning to limp behind

reality.

The report by the BLS had a mix of rising and falling prices. Energy

got more expensive. The price of oil has jumped since February, and so

the price of gasoline rose 2.3% in May, seasonally adjusted, after

having soared 8.1% in April. Without seasonal adjustment, it jumped 6.6%

in May. Fuel oil jumped 6.2%, natural gas rose 1.7%, electricity edged

down 0.2%. But the energy index is still below last year with gasoline

down 16.9%. So yes, energy prices are rising, but they’re still down

from a year ago.

That cannot be said of rents.

The Consumer Price Index contains two housing components: “Owners’

equivalent rent of primary residence” (OER) and “rent of primary

residence” (Rent). They purport to measure the cost of “Shelter,” which

is the “consumption item” that a home provides and is thus included in

the CPI. The cost of the home itself and any improvements to the home

are considered an “investment,” not consumption, and therefore not part

of the CPI.

“Owners’ equivalent rent” accounts for 24.2% of total CPI. “Rent of

primary residence” accounts for 7.7% of CPI. Combined they account for

31.9% of CPI. “Shelter,” which adds those two and some other items,

accounts for 33.2%, by far the largest and most important component of

the CPI.

The data are obtained by survey. For “owners’ equivalent rent,”

homeowners are asked what they think they would have to pay if they were

renting the home. A measure of implicit rent. Would homeowners think

that rents of their types of homes are increasing? Nope. They’re not

renting. They have no idea. They can easily fool themselves.

Based on the surveys, the BLS figured the “owners’ equivalent rent”

rose 3.3% year over year. That measure accounts for 24.2% of CPI. It is

always ludicrously low. It’s the simplest way of hiding the impact of

soaring housing costs, and the simplest way of keeping CPI artificially

low.

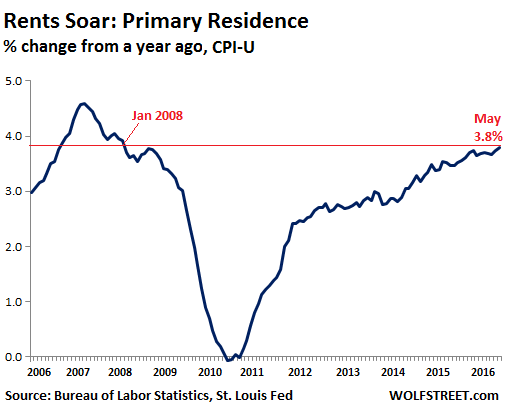

For the component “rent of primary residence,” renters are asked what

they’re currently paying in rent. Even if they’ve lived in a

rent-controlled apartment for 20 years and pay just a fraction of market

rent, it becomes part of the statistics, and not the rent that a new

renter pays. Market rent data is available everywhere. But no. So “rent

of primary residence” – however understated it may be – rose 0.4% from

April and 3.8% from a year ago, the biggest year-over-year increase

since January 2008:

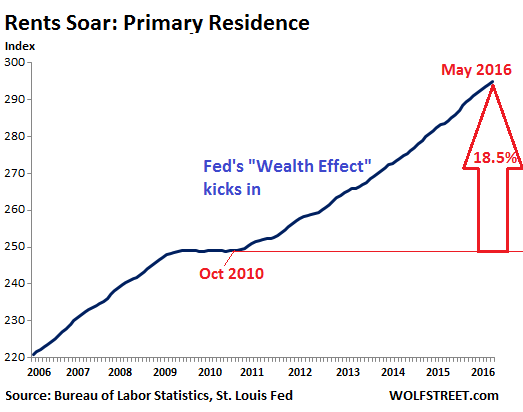

Over the longer term? In the five-and-a-half years since September

2010, the index for rent, understated as it is, has risen 18.5%:

Why are rents rising sharply when incomes, especially for the lower

80%, have languished? It’s not like renters have more money to blow on

rent and thus are driving up rents. On the contrary.

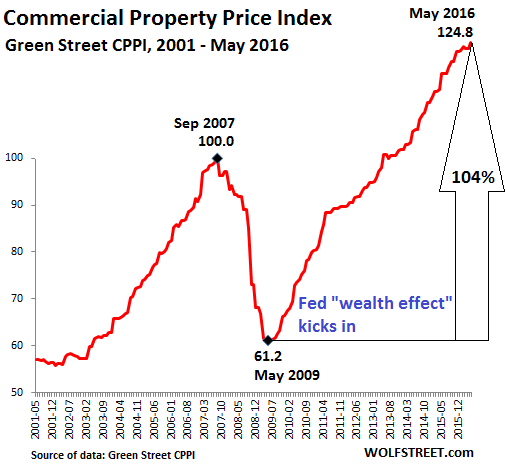

Since the Fed began its ZIRP and QE programs with the express goal of

inflating asset prices, stocks and bonds have soared, home prices have

soared, commercial real estate has soared, including apartments. Nearly

all asset prices have soared. According to the Green Street Commercial

Property Price Index (

CPPI), commercial real estate prices have

more than doubledsince May 2009, when the Fed’s “wealth effect” started to kick in:

People don’t have to live in stocks and bonds, and those asset

bubbles have little impact on the daily lives of regular folks. But they

do live in homes.

But when apartment prices, along with the rest of commercial real

estate, began to soar, landlords raised rents, on the essential logic of

cap rates and return on investment. It has to work out for the

investor, or else the whole over-leveraged house of cards comes tumbling

down again, as it did in 2008.

Housing costs is where the Fed’s “wealth effect” is eating the lunch

of regular folks. More than just their lunch. They’ve gotten

hammered

by the Fed’s policies. Just like savers, who’ve done the prudent thing

all their lives, only to watch their income streams get confiscated.

Rents started rising in late 2010, according to the BLS. The

commercial real estate boom had started 9 months earlier. The lag is

natural. And rent inflation, as figured by the BLS, hasn’t been nearly

as steep as commercial property price inflation, for two reasons: One,

because the BLS systematically understates rent inflation. And two,

because reality bites; renters can be squeezed only so far before

there’s nothing left to squeeze.

For many renters, it’s a zero-sum affair: every dollar spent on rent is a dollar

not

spent on other items. In this way, rent inflation is a transfer of

spending from healthcare, food, or electronic gadgets, to shelter. It’s

not helpful for the overall economy. And it’s devastating for the people

who have to struggle with it.

Sooner or later, with wages stagnant for many renters, market

resistance starts kicking in. And this may now be happening in the first

few cities, and a mega-landlord is preparing for a downturn. Read…

It Starts: Apartment Glut in San Francisco & New York City

Martin

Hill is a Catholic paleoconservative and civil rights advocate. His

work has been featured in the Los Angeles Daily News, San Gabriel Valley

Tribune, The Orange County Register, KNBC4 TV Los Angeles, The Press

Enterprise, LewRockwell.com, WhatReallyHappened.com, Infowars.com,

PrisonPlanet.com, Economic Policy Journal, TargetLiberty.com,

FreedomsPhoenix, Haaretz, TMZ, Veterans Today, Jonathan Turley blog, The

Dr. Katherine Albrecht Show, National Motorists Association,

AmericanFreePress.net, RomanCatholicReport.com, WorldNetDaily,

HenryMakow.com, OverdriveOnline.com, Educate-Yourself.org,

TexeMarrs.com, Dr. Kevin Barrett's Truth Jihad radio show,

Strike-The-Root.com, Pasadena Weekly, ActivistPost.com, Los Angeles

Catholic Lay Mission Newspaper, KFI AM 640, IamtheWitness.com, Redlands

Daily Facts, SaveTheMales.ca, BlackBoxVoting, The Michael Badnarik Show,

The Wayne Madsen Report, Devvy.com, Rense.com,

FromTheTrenchesWorldReport.com, BeforeItsNews.com, The Contra Costa

Times, Pasadena Star News, Silicon Valley Mercury News, Long Beach Press

Telegram, Inland Valley Daily Bulletin, L.A. Harbor Daily Breeze,

CopBlock.org, DavidIcke.com, Whittier Daily News, KCLA FM Hollywood, The

Fullerton Observer, Antiwar.com, From The Trenches World Report, and

many others. Archives can be found at

Martin

Hill is a Catholic paleoconservative and civil rights advocate. His

work has been featured in the Los Angeles Daily News, San Gabriel Valley

Tribune, The Orange County Register, KNBC4 TV Los Angeles, The Press

Enterprise, LewRockwell.com, WhatReallyHappened.com, Infowars.com,

PrisonPlanet.com, Economic Policy Journal, TargetLiberty.com,

FreedomsPhoenix, Haaretz, TMZ, Veterans Today, Jonathan Turley blog, The

Dr. Katherine Albrecht Show, National Motorists Association,

AmericanFreePress.net, RomanCatholicReport.com, WorldNetDaily,

HenryMakow.com, OverdriveOnline.com, Educate-Yourself.org,

TexeMarrs.com, Dr. Kevin Barrett's Truth Jihad radio show,

Strike-The-Root.com, Pasadena Weekly, ActivistPost.com, Los Angeles

Catholic Lay Mission Newspaper, KFI AM 640, IamtheWitness.com, Redlands

Daily Facts, SaveTheMales.ca, BlackBoxVoting, The Michael Badnarik Show,

The Wayne Madsen Report, Devvy.com, Rense.com,

FromTheTrenchesWorldReport.com, BeforeItsNews.com, The Contra Costa

Times, Pasadena Star News, Silicon Valley Mercury News, Long Beach Press

Telegram, Inland Valley Daily Bulletin, L.A. Harbor Daily Breeze,

CopBlock.org, DavidIcke.com, Whittier Daily News, KCLA FM Hollywood, The

Fullerton Observer, Antiwar.com, From The Trenches World Report, and

many others. Archives can be found at