First American CoreLogic reported today that more than 11.3 million, or 24 percent, of all residential properties with mortgages were in negative equity at the end of the fourth quarter of 2009, up from 10.7 million and 23 percent at the end of the third quarter of 2009. An additional 2.3 million mortgages were approaching negative equity at the end of last year, meaning they had less than five percent equity. Together, negative equity and near-negative equity mortgages accounted for nearly 29 percent of all residential properties with a mortgage nationwide.

Negative equity, often referred to as “underwater” or “upside down,” means that borrowers owe more on their mortgage than their homes are worth. Negative equity can occur because of a decline in value, an increase in mortgage debt or a combination of both.

In Philadelphia, 7.7 percent, or 69,350, of all residential properties with a mortgage were in negative equity for Q4 2009. An additional 3.6 percent, or 32,150, were in near negative equity in Philadelphia.

National Data Highlights:

• Negative equity continues to be concentrated in five states: Nevada, which had the highest percentage negative equity with 70 percent of all of its mortgage properties underwater, followed by Arizona (51 percent), Florida (48 percent), Michigan (39 percent) and California (35 percent). Among the top five states, the average negative equity share was 42 percent, compared to 15 percent for the remaining states. In numerical terms, California (2.4 million) and Florida (2.2 million) had the largest number of negative equity mortgages accounting for 4.6 million, or 41 percent, of all negative equity loans.

• The net increase in the number of negative equity borrowers in Q4 2009 was 620,000, with the largest percentage increases occurring in Nevada, Georgia and Arizona. Among the states with the highest negative equity shares, California had the smallest increase in the negative equity share, which only rose 0.4 percent to 35.1 percent. In numerical terms, Florida had the largest increase in the number of negative equity borrowers rising by more than 141,000, followed by Georgia (65,000) and Illinois (55,000).

• The rise in negative equity is closely tied to increases in pre-foreclosure activity and is a major factor in changing homeowner default behavior. Once negative equity exceeds 25 percent, or the mortgage balance is $70,000 higher than the current property values, owners begin to default with the same propensity as investors.

• The aggregate dollar value of negative equity was $801 billion, up $55 billion from $746 billion in Q3 2009. The average equity for an underwater borrower in Q4 was -$70,700, up from -$69,700 in Q3 2009. The segment of borrowers that are 25 percent or more in negative equity account for over $660 billion in aggregate negative equity.

• Of the over 47 million homeowners with a mortgage, the average loan to value ratio (LTV) is 70 percent. More than 23 million, or 49 percent, of all homeowners with a mortgage have at least 25 percent equity in their home, and over 12 million have at least 50 percent equity in their home.

“Negative equity is a significant drag on both the housing market and on economic growth. It is driving foreclosures and decreasing mobility for millions of homeowners,” said Mark Fleming, chief economist with First American CoreLogic. “Since we expect home prices to slightly increase during 2010, negative equity will remain the dominant issue in the housing and mortgage markets for some time to come.”

Methodology — Only data for mortgaged residential properties that have an AVM value is presented. There are several states where the public record, AVM or mortgage coverage is thin. Although coverage is thin, these states account for fewer than 5 percent of the total population of the U.S.:

First American CoreLogic’s data includes 47 million properties with a mortgage, which accounts for over 85 percent of all mortgages in the U.S.* First American CoreLogic used its public record data as the source of the mortgage debt outstanding (MDO) and it includes 1st mortgage liens and junior mortgage liens and is adjusted for amortization and home equity utilization in order to capture the true level of mortgage debt outstanding for each property. The current value was estimated by using the First American CoreLogic Automated Valuation Models (AVM) for residential properties. The data was filtered to include only properties valued between $30,000 and $30 million because AVM accuracy tends to quickly worsen outside of this value range.

The amount of equity for each property was determined by subtracting the property’s estimated current value from the mortgage debt outstanding. If the mortgage debt was greater than the estimated value, then the property is in a negative equity position. The data was created at the property level and aggregated to higher levels of geography.

Tuesday, March 2, 2010

Administration Blames Bunning's 'Political Games' for Furlough of 2,000 Workers

Transportation Secretary Ray LaHood blasted Kentucky Sen. Jim Bunning Monday for blocking legislation to extend several federal programs, a move that triggered the furlough of 2,000 transportation workers without pay Monday.

Transportation Secretary Ray LaHood blasted Kentucky Sen. Jim Bunning Monday for blocking legislation to extend several federal programs, a move that triggered the furlough of 2,000 transportation workers Monday.

The legislation would have extended federal highway and transit programs, as well as unemployment benefits for about 400,000 Americans.

Bunning, a Republican, objected to the $10 billion measure, saying it would add to the budget deficit.

But the Department of Transportation issued a lengthy statement Monday detailing the numerous programs that would be temporarily sidelined as a result.

Workers will be furloughed, federal reimbursements to states for highway programs -- which total about $190 million a day -- will be halted, and construction workers will be sent home from job sites because federal inspectors will not be working.

"As American families are struggling in tough economic times, I am keenly disappointed that political games are putting a stop to important construction projects around the country," LaHood said.

The disruption may not last long.

Sen. Jon Kyl, R-Ariz., the No. 2 Republican in the Senate, told "Fox News Sunday" that the Senate will pass an unemployment benefits extension this week. But he praised Bunning, saying his decision to block the legislation was made to point out the hypocrisy in the Senate exempting the legislation from a just-passed bill requiring Congress to pay for legislation as it comes up, commonly referred to as PAYGO.

"All Senator Bunning was saying is that it should be paid for," Kyl said. "It will pass, though, because it's a temporary extension."

Furloughs will affect employees at the Federal Highway Administration, the Federal Motor Carrier Safety Administration, the National Highway Traffic Safety Administration and the Research and Innovative Technology Administration.

Among the construction sites where work will be halted: the $36 million replacement of the Humpback Bridge on the George Washington Parkway in Virginia; $15 million in bridge construction and stream rehabilitation in Coeur d'Alene, Idaho; and the $8 million resurfacing of the Natchez Trace Parkway in Mississippi.

The Associated Press contributed to this report.

Homeowners Say Banks Keep Them Underwater by Spurning Loan Program Rules

A slew of struggling homeowners are coming forward with complaints about the way banks are operating under a federal loan modification program announced last year by the Obama administration.

You qualify.

Those two words, from the mouth of a bank representative last October, triggered a wave of relief for Tracy Davis and her husband James. The couple had been in and out of work for three years and were struggling to pay their mortgage -- so when the Bank of America worker told them they qualified under a federal program to have their loan modified, they finally saw a path to keeping their house.

"We walked out thinking, great," Tracy Davis said.

But weeks went by, and nobody contacted them, and they weren't able to reach anyone -- other than representatives at a call center in India.

"To this day, we've not heard from someone," she said. "It's February. This goes back to October 30."

The Davises, who live in Cincinnati, are among a slew of struggling homeowners coming forward with complaints about the way banks are operating under a federal loan modification program announced last year by the Obama administration. The program, called the Home Affordable Modification Program, aims to keep 3 to 4 million people in their homes. Federal statistics show banks are making plenty of offers, but relatively few of those loan changes are being made permanent -- of the more than 1 million homeowners who have started the required three-month trial period, only 116,000 have had their new terms made permanent.

The complaints have a common tune. Homeowners say the banks are giving them the runaround -- either by pledging to modify loans and then not following through, as with the Davis family, or by signing them up for the trial period and then leaving them in limbo.

"This is an epidemic problem," said Stuart Rossman, director of litigation with the National Consumer Law Center.

Under the terms of the Treasury Department program, participating banks that offer new loan terms are supposed to put homeowners through a three-month trial period. If the homeowners make timely payments and meet other conditions, the terms are supposed to become permanent.

But a pair of lawsuits filed in U.S. District Court in Boston this past week claimed Bank of America and Wells Fargo were violating those rules.

Rossman, who is helping to represent the plaintiffs, said banks -- in Massachusetts and across the country -- are stringing homeowners along for months without sealing the deal.

"That, to us, is inexcusable and a breach of contract," he said. "They are living in limbo while they are at risk of losing their home."

In the Massachusetts cases, the lawsuits describe a Kafkaesque scenario in which the banks have been holding up the loan terms because of missing paperwork that they either won't identify or never required in the first place.

For instance, homeowners Odalid and Wilfredo Bosque, according to one suit, entered the trial period from October to December of last year, but after they "timely made each of the payments," Wells Fargo did not offer a final agreement. The Bosques were told that they did not submit their paperwork, but when they called the bank, agents purportedly told them "there is no paperwork missing." Meanwhile, they continued to receive calls from the collections agency.

Wells Fargo issued a statement saying the bank has "diligently" worked with homeowners to complete the loan modifications for customers who meet the guidelines.

"Unfortunately, not all customers who enter a HAMP trial ultimately qualify for the program. In these instances, we work to determine if another foreclosure prevention option is available to them," the written statement said.

Rossman said that his borrowers qualified.

In Ohio, the Davises were among 10 plaintiffs in a suit filed against Bank of America in early February in U.S. District Court. The homeowners all say they experienced the same problem. According to the suit, they went to a Treasury-sponsored "borrower outreach" event in Cincinnati at the end of October at which bank representatives offered them modified home loans and pledged to send them the paperwork "within weeks."

The documents never came, they say.

Tracy Davis said the representative she and her husband met with gave them her phone number and extension and said they would receive a packet within seven business days. When it never came, she tried the number, but she was not able to reach the extension. She said she was sent instead to a call center in India that could not help, and that numerous e-mails to the representative went unanswered.

"It's just not right," Davis said.

She said she and her husband had good-paying jobs until late 2006, when she was laid off from the title insurance company she worked for in the midst of the housing market collapse. After that, her husband lost his job. Then she got hired doing administrative work, but she was laid off nine weeks later. Finally, she got a job at a grocery store, where her husband also recently started working -- but their income, she said, is about one-third of what it used to be. With mortgage payments at above $1,000, she was hoping to reduce it to below $400 by stretching her mortgage from 15 to 30 years.

"It's been a rough three years," she said.

She received a package from Bank of America after she filed the suit, but she has turned that over to her attorney.

Bank of America could not be reached for comment.

The Treasury program, part of a $75 billion effort, has been billed as a way to keep millions in their homes by preventing foreclosure.

Under the program, banks get $1,000 for every modification, and then they can receive $1,000 a year for up to three years. Borrowers, too, can get $1,000 a year from the government under the plan, though the incentives don't kick in until after the three-month trial. The program is meant to reduce monthly mortgage payments to 31 percent of income.

Government statistics from January show Bank of America has offered the modifications to nearly 330,000 homeowners, but it made only 12,761 permanent. Wells Fargo has made 188,749 offers and made 17,652 permanent. There's a gap between those figures for most banks. J.P. Morgan Chase, for instance, made more than 222,000 offers, but sealed 11,581 of them.

Homeowners aren't just having a hard time winning modifications under the Home Affordable Modification Program. Personal accounts detail trouble getting loan modifications of any kind.

At least one plaintiff in the Ohio case was told she did not qualify under HAMP but could get an extension anyway. But the same thing that happened to Davis happened to her. She says nobody called her, and when she called the bank she was told Bank of America had none of the information she gave the representative at the October meeting.

She was told she qualified under a separate program and forced to re-start the process several times, according to the suit, until she was told in January that she did not qualify. Then she was told again that she qualified for a review, and she re-submitted her paperwork once more.

Bruce W. Gavin, who lives in Glen Burnie, Md., said he's been trying for years to get his home loan modified to no avail.

He said his monthly payment had been climbing continuously since he and his wife refinanced a decade ago -- it went from about $800 to $1,600, which was too much. Gavin said his son has autism, his wife has lupus and he's the only one who works. He lost his job five years ago, and his new job doesn't pay enough to be able to afford the higher mortgage -- which was pegged to an interest rate of 10.25 percent.

Gavin said he was rejected for one program, but was finally able to go under consideration for a loan modification program through Bank of America. His request? Lower the interest rate and turn the 20 years left on the loan into a 30-year plan.

During that period, he said he was told not to make mortgage payments.

Then came a bank letter last month, telling him he had until Jan. 26 to accept an agreement that was even worse or be foreclosed. The interest rate would stay at 10.25 percent and he'd be required to make up for the lost payments, pushing his monthly payment to more than $2,000.

He signed it, in part out of concern that moving would aggravate his son's autism.

"It's been a mess," Gavin said. "I don't even know what to do."

Mark Lawson, an attorney with the Legal Aid Society of Southwest Ohio representing the plaintiffs in the Ohio federal case, said loan modification problems are widespread.

"It's pretty much everywhere," he said.

Greece Now, U.K. Next as Scots Ready for Pound Plunge (Update2)

(Adds today’s decline in second, 12th paragraphs.)

By Rodney Jefferson

March 1 (Bloomberg) -- While the eyes of the world focus on Greece’s debt crisis, investors in Edinburgh are busy preparing for the U.K. to be next.

Turcan Connell, which caters to rich families, expects the pound to lose between 20 percent and 30 percent against the dollar once investors turn their sights on Britain as the government sells a record amount of debt. Sterling slid to a 10- month low versus the U.S. currency today.

“Alarm bells were ringing in Greece for a long time and when it happened, it happened very quickly,” Haig Bathgate, head of strategy at Turcan Connell, said at the company’s offices in the Scottish capital. “The U.K. is in a similar predicament. It could be hit very hard.”

Money managers in Edinburgh, where investment decisions have been made on behalf of insurers, pensioners and the wealthy for two centuries, are maneuvering to protect assets from the U.K. economy as it limps out of its worst recession on record.

Bruce Stout, whose Murray International Trust Plc in Edinburgh has doubled over the past five years, said the chance of a plummeting pound are “better than even” and his biggest holdings are in Asia and Latin America. He called sterling a “very vulnerable currency.”

U.K. fund managers at Aegon Asset Management and Scottish Widows Investment Partnership, together responsible for more than 30 billion pounds ($45 billion), said in January they are buying companies that do the bulk of their business abroad.

‘Very Dire’

“When there’s a fiscal crisis, the markets tend to punish that country very quickly,” said Bathgate, who is responsible for 560 million pounds. “I don’t think Britain is in nearly as bad a position as Greece. We’ve got a good taxation system, however the position of the economy is very dire.”

The U.K.’s budget deficit is roughly the same as Greece’s, both exceeding 12 percent of economic output. Moody’s Investors Service and Standard & Poor’s said last week they may cut Greece’s credit rating as the five-month-old government struggles to curb spending and control its debt.

Concern that Greece won’t be able to cut its deficit helped send the euro 5.6 percent lower against the dollar this year. The euro today strengthened to a three-month high against the pound, trading above 90 pence.

British Prime Minister Gordon Brown’s government in December increased its planned gilt sales for the financial year ending this month to a record 225.1 billion pounds from the 220 billion pounds announced in April. Moody’s Investors Service said in December the U.K. may “test the Aaa boundaries.”

Hung Parliament

Brown must call an election by June and some polls signal that no party will emerge with a clear majority.

The pound fell below $1.50 today for the first time since May last year, taking this year’s decline to 8 percent. A YouGov Plc poll published yesterday showed Brown’s Labour Party only two percentage points behind the opposition Conservatives, the narrowest margin for more than two years.

A so-called hung parliament or signs retail sales and economic growth aren’t recovering as expected might be the catalysts for the pound to accelerate declines, Bathgate said. The Office for National Statistics last week revised up the rate of economic growth for the fourth quarter to 0.3 percent from a previous estimate of 0.1 percent.

“There could be a number of triggers,” he said. “If there’s indecision about how you deal with a problem, that’s when things start to fall apart. We could be in the position where the spotlight turns to the U.K.”

UBS Report

The pound may fall below parity with the euro and drop to the lowest level against the dollar since the mid-1980s should the U.K. cut spending too quickly, Mansoor Mohi-Uddin, chief currency strategist at UBS AG, said in a Feb. 24 report.

Sterling slid to a nine-month nadir against the dollar last week, trading at $1.52. Zurich-based UBS, the world’s second- biggest currency trader, predicted it could fall “quickly back” to $1.05 or below.

The pound may come under further pressure with the Bank of England resuming its quantitative-easing program, a process of injecting new money into the economy, within the next three to four months, Bathgate said. Policy maker Adam Posen said Feb. 24 the central bank may expand the 200 billion-pound asset-purchase plan should the economic recovery prove weaker than expected.

“If it comes back then we’re likely to be the only people doing that in the world at that time,” said Bathgate. “My strong view is the government is trying to create inflation and devalue the currency.”

Selling Bonds

Bathgate said he sold conventional U.K. government-bond investments at the end of 2008 and only holds index-linked securities because of concern inflation may accelerate.

The firm also has reduced holdings in corporate bonds because of the potential “knock-on impact” from a decline in government securities.

The yield on the benchmark 10-year gilt dropped 24 basis points to 4.03 percent last week. The yield on Greek 10-year bonds fell 6 points to 6.39 percent. German bunds, the region’s benchmark debt, declined 18 points to 3.10 percent.

Turcan Connell, whose clients typically have at least 5 million pounds to invest, was founded in 1998 and oversees about 1 billion pounds in total. Bathgate is responsible for allocating money to different funds, and half is currently in stocks portfolios with 30 percent in hedge funds and other so- called alternative investments.

--Editors: David Clarke, Tim Farrand

Senate leader predicts 'massive layoffs'

ATLANTA - Senate Majority Leader Chip Rogers announced Monday morning that “massive layoffs” will be one result in how the legislature copes with a roughly $1 billion shortfall in expected revenue for next year’s budget.

“I’m not going to sugarcoat the situation we’re in. Yeah, there will be massive layoffs,” said Rogers, a Woodstock Republican.

He wouldn’t say how many state workers could lose their jobs. One idea being investigated is offering an incentive for the 8,000 workers already eligible for retirement to give up their jobs.

Rogers met with reporters during his weekly press conference at the Capitol. Asked if last week’s round of hearings about the painful cuts possible for state agencies was a way to make tax increases politically palatable, Rogers said not from the Senate leadership’s point of view.

“We’re not looking at any tax increases at all,” he said. “We’re looking at cuts, cuts, cuts.”

Since the state is already among the lowest in government spending per citizen, there is little fluff to be cut from the budget, and the remaining cuts will be painful, he said.

Later in the day, the University System of Georgia was scheduled to release a list of cuts it would make if lawmakers trim another $300 million from funding for the 35 public colleges and universities. Rogers said if the Board of Regents lays off employees to meet those cuts, it will not be because lawmakers specified personnel reductions.

“(The regents) will have to make that decision for themselves,” he said.

Hawaii might halt junior kindergarten

Plan to move up kindergarten eligibility date would leave many kids waiting a year to start school

Lawmakers are considering a measure that would eliminate junior kindergarten in Hawai'i public schools and move up the date children are eligible to enter kindergarten, changes that would require thousands of late-born 5-year-olds to wait an additional year before they can start school.When the junior kindergarten program was implemented in 2006, it was hailed as a boost to early education in a state where four out of five students entering school lack basic skills.

However, lawmakers say junior kindergarten has not been effectively implemented at the school level, with junior-K students often mixed in with regular kindergarten classes.

"The effectiveness of junior kindergarten was called into question," said state Sen. Norman Sakamoto, (D-15th, Waima- lu, Airport, Salt Lake), chairman of the Senate Education and Housing Committee. "I personally would like to have a junior kindergarten. ... But if we're not going to effectively help the young ones, perhaps we should ask them to come the following year to school."

Educators respond that junior-K, first tried in 2004, was an unfunded mandate by the Legislature and that most schools could not afford to create separate junior-K classes. Acting Superintendent Kathryn Matayo-shi said the state Department of Education supports the proposed change in the kindergarten eligibility date, to Aug. 1 from the current Dec. 31.

The measure, SB 2068, still has half the legislative session to go, and Sakamoto said it is a work in progress. The bill passed out of the Senate Ways and Means Committee last week.

Despite junior-K's problems, educators, parents and early-education advocates say the program is helpful and that the proposed changes will create a burden for parents at a time when they can least afford it.

If the bill passes, it would not take effect until the 2011-12 school year.

Liz Chun, executive director of the Good Beginnings Alliance, said fewer parents can afford to pay for preschool because of the recession. As a result, changing the date children are eligible to enter kindergarten to Aug. 1 — currently kids must be 5 by Dec. 31 — is going to hit hard, particularly among low-income and at-risk students.

"My concern is as we essentially take out five months worth of students who will be able to start a kindergarten program, they will have to wait a whole year and parents' ability to pay for preschool seems to be slipping," Chun said.

For instance, about 63 percent of students entering Kalihi Elementary in 2008 as kindergarteners went to preschool. In 2009, that number was down to 33 percent, according to the Hawaii State Readiness Assessment compiled by Good Beginnings.

"This really amounts to not only a savings mechanism for the (state DOE), but truly another cut away at an opportunity for a young child to receive education prior to when they are 5 years old," Chun said.

Chun said many families, especially in "vulnerable communities," will not be able to afford to have their child in preschool for the year that they cannot be in kindergarten.

"Having them stay home without access to some kind of early learning will affect their readiness," Chun said.

Raedelle Van Fossen's son, now in first grade at 'Āina Haina Elementary, entered junior kindergarten last year. Van Fossen said junior-K offered her son the jump start he would not have received if he would have had to wait another year before entering school.

"He was at a point where I think preschool was too easy for him academically. He needed the challenge . If we kept him in preschool another year he would have been bored out of his mind. I think there is a need for it," she said.

two approaches

Less than 18 percent of children enter kindergarten with the literacy standards they need to succeed in school, according to a 2008 report by the state's early- learning education task force. That means the vast majority of children entering school are already behind, the report said.

Nearly 15,000 students are enrolled in kindergarten in Hawai'i public schools this year.

Christina Small, principal of Liholiho Elementary School, one of the schools that piloted junior kindergarten as a separate class back in 2004, said the program has merit.

"We found that some students that were late-born, after half a year they soared," Small said. "We find that socially they need more help, more play, more socialization."

Small said that if the school could no longer early-enroll children born in the latter part of the year, those children would be more likely to stay home without exposure to the skills they need to start classes.

"We would rather have them in school. The most development happens between birth and 5 years old, and they will miss that opportunity," Small said.

At Ala Wai Elementary, junior kindergartners are mixed in with general kindergarten classes.

Charlotte Unni, principal at Ala Wai Elementary, said junior kindergarten students often will enter school without some of the skills they need. They may be unable to sit still in a classroom, may need more social development, and sometimes may have never opened a book.

Often, those same children are ready to move on to first grade with the rest of their class by year's end. Sometimes, junior kindergartners are held back for another year before they advance.

"Some kids in class are two years in kindergarten. Some kids are one year in kindergarten. We found that the kids that are in the senior-K, they blossom. The first year they are a little slower. They aren't developmentally there. By the second year, they are shining," Unni said.

Funding crucial

Lisa Uyehara, administrative director for the Early Education Center in Downtown Honolulu, said if lawmakers were to change the entrance date for kindergarten, Hawai'i's public schools would be more in line with local private schools and districts across the country.

Currently, Hawai'i public school students must turn 5 by Dec. 31 to attend kindergarten. That's fairly late compared with private schools, Uyehara said.

"A lot of private schools have very specific cut-off dates. Boys have to be 5 by June, girls have to be 5 by August," she said.

Ben Naki, program director of PACT Early Head Start/Head Start in Kuhio Park Terrace, said the change being contemplated by lawmakers would affect the most vulnerable families.

"More kids will be out there who will need our services, but ... it is not as if we can serve more kids than we are funded for," Naki said.

The Kuhio Park Terrace program has slots for about 200 children, but every year there is a long wait list, he said. He expects that wait list would grow if the kindergarten eligibility date changes.

He also said a number of the programs being pared as a result of the state's budget crisis are affecting children.

The state Department of Human Services is expected to decrease childcare subsidy rates beginning in February, Naki said. That will likely hit more than 1,600 low- to moderate-income families.

"A lot of the programs that are being looked at (for budget cuts) are the early- childhood programs," Naki said.

Israel shows China evidence of Iran bomb program

Delegation to Beijing offers Chinese 'the full intelligence picture available to Israel'.

An Israeli delegation that traveled to Beijing last week presented detailed intelligence on Iran's nuclear program in an attempt to persuade China that Tehran seeks atomic weapons, a senior diplomatic source told Haaretz.

The group, led by Strategic Affairs Minister Moshe Ya'alon and central bank chief Stanley Fischer, tried to persuade China to support sanctions on Iran by offering "the full intelligence picture available to Israel," the diplomat said.

The Israeli officials also told the Chinese that a nuclear Iran would push up oil prices - China depends on Iran for a significant proportion of its imported oil.

Israel is trying to recruit China's support for a fourth round of sanctions on Iran, and the UN Security Council is due to vote on the issue in the coming months. At the very least, Israel wants to ensure that China does not oppose the sanctions when they come to vote.

Israel also wants to make sure that China supports the report on Iran published by the new head of the International Atomic Energy Agency, Yukiya Amano. Unlike his predecessor Mohamed ElBaradei, Amano discussed in his report the possibility that Iran might secretively be developing nuclear weapons. The IAEA's annual conference is set to open in Vienna today.

The diplomat told Haaretz that the delegation's main aim was to present the Chinese with evidence that Iran is developing nuclear arms. China's official position is that Iran has a right to develop nuclear technology for peaceful, civilian purposes and that there is no proof Iran has a military nuclear program.

Most detailed overview in years

"The Chinese were given the full intelligence picture Israel has about the Iranian nuclear program, which clearly shows Iran is developing nuclear weapons," the source said.

"The delegation also stressed how concerned Israel was, and that all options must remain on the table," the source added.

The delegation that set out for Beijing in coordination with the U.S. administration also included senior officials in the Foreign Ministry, the National Security Council and the defense establishment.

It met with a number of Chinese officials, the most senior being State Councilor Dai Bingguo.

According to the source, the Israelis spent two hours presenting the Chinese with an overview of the intelligence information Israel has on Iran's nuclear program. This was the most detailed overview given by Israel to China in more than three years, since prime minister Ehud Olmert's visit in January 2007.

The Israeli delegation left with a positive feeling, the source said, with the Chinese saying they would seriously consider the information they received.

Talks were conducted in a friendly atmosphere, with Beijing stressing the importance of Chinese-Israeli relations and its desire to develop ties further, the source said.

Fischer detailed the implications a nuclear Iran would have for the world economy, stressing a dramatic rise in oil prices. Alternatives to importing oil from Iran were also discussed.

Earlier this year, Saudi Arabia and the United States proposed to China that it buy oil from Arab states at much lower prices than oil imported from Iran.

China is also concerned about possible sanctions because of its deals with Iran on developing railroads, tunnels and oil fields. These contracts are expected to be highly profitable, so the Chinese fear that sanctions would put them at risk.

An Israeli delegation that traveled to Beijing last week presented detailed intelligence on Iran's nuclear program in an attempt to persuade China that Tehran seeks atomic weapons, a senior diplomatic source told Haaretz.

The group, led by Strategic Affairs Minister Moshe Ya'alon and central bank chief Stanley Fischer, tried to persuade China to support sanctions on Iran by offering "the full intelligence picture available to Israel," the diplomat said.

The Israeli officials also told the Chinese that a nuclear Iran would push up oil prices - China depends on Iran for a significant proportion of its imported oil.

Israel is trying to recruit China's support for a fourth round of sanctions on Iran, and the UN Security Council is due to vote on the issue in the coming months. At the very least, Israel wants to ensure that China does not oppose the sanctions when they come to vote.

Israel also wants to make sure that China supports the report on Iran published by the new head of the International Atomic Energy Agency, Yukiya Amano. Unlike his predecessor Mohamed ElBaradei, Amano discussed in his report the possibility that Iran might secretively be developing nuclear weapons. The IAEA's annual conference is set to open in Vienna today.

The diplomat told Haaretz that the delegation's main aim was to present the Chinese with evidence that Iran is developing nuclear arms. China's official position is that Iran has a right to develop nuclear technology for peaceful, civilian purposes and that there is no proof Iran has a military nuclear program.

Most detailed overview in years

"The Chinese were given the full intelligence picture Israel has about the Iranian nuclear program, which clearly shows Iran is developing nuclear weapons," the source said.

"The delegation also stressed how concerned Israel was, and that all options must remain on the table," the source added.

The delegation that set out for Beijing in coordination with the U.S. administration also included senior officials in the Foreign Ministry, the National Security Council and the defense establishment.

It met with a number of Chinese officials, the most senior being State Councilor Dai Bingguo.

According to the source, the Israelis spent two hours presenting the Chinese with an overview of the intelligence information Israel has on Iran's nuclear program. This was the most detailed overview given by Israel to China in more than three years, since prime minister Ehud Olmert's visit in January 2007.

The Israeli delegation left with a positive feeling, the source said, with the Chinese saying they would seriously consider the information they received.

Talks were conducted in a friendly atmosphere, with Beijing stressing the importance of Chinese-Israeli relations and its desire to develop ties further, the source said.

Fischer detailed the implications a nuclear Iran would have for the world economy, stressing a dramatic rise in oil prices. Alternatives to importing oil from Iran were also discussed.

Earlier this year, Saudi Arabia and the United States proposed to China that it buy oil from Arab states at much lower prices than oil imported from Iran.

China is also concerned about possible sanctions because of its deals with Iran on developing railroads, tunnels and oil fields. These contracts are expected to be highly profitable, so the Chinese fear that sanctions would put them at risk.

A Country of Serfs Ruled By Oligarchs

The media has headlined good economic news: fourth quarter GDP growth of 5.7 percent ("the recession is over"), Jan. retail sales up, productivity up in 4th quarter, the dollar is gaining strength. Is any of it true? What does it mean?

The 5.7 percent growth figure is a guesstimate made in advance of the release of the U.S. trade deficit statistic. It assumed that the U.S. trade deficit would show an improvement. When the trade deficit was released a few days later, it showed a deterioration, knocking the 5.7 percent growth figure down to 4.6 percent. Much of the remaining GDP growth consists of inventory accumulation.

More than a fourth of the reported gain in Jan. retail sales is due to higher gasoline and food prices. Questionable seasonal adjustments account for the rest.

Productivity was up, because labor costs fell 4.4 percent in the fourth quarter, the fourth successive decline. Initial claims for jobless benefits rose. Productivity increases that do not translate into wage gains cannot drive the consumer economy.

Housing is still under pressure, and commercial real estate is about to become a big problem.

The dollar's gains are not due to inherent strengths. The dollar is gaining because government deficits in Greece and other EU countries are causing the dollar carry trade to unwind. America's low interest rates made it profitable for investors and speculators to borrow dollars and use them to buy overseas bonds paying higher interest, such as Greek, Spanish and Portuguese bonds denominated in euros. The deficit troubles in these countries have caused investors and speculators to sell the bonds and convert the euros back into dollars in order to pay off their dollar loans. This unwinding temporarily raises the demand for dollars and boosts the dollar's exchange value.

The problems of the American economy are too great to be reached by traditional policies. Large numbers of middle class American jobs have been moved offshore: manufacturing, industrial and professional service jobs. When the jobs are moved offshore, consumer incomes and U.S. GDP go with them. So many jobs have been moved abroad that there has been no growth in U.S. real incomes in the 21st century, except for the incomes of the super rich who collect multi-million dollar bonuses for moving U.S. jobs offshore.

Without growth in consumer incomes, the economy can go nowhere. Washington policymakers substituted debt growth for income growth. Instead of growing richer, consumers grew more indebted. Federal Reserve chairman Alan Greenspan accomplished this with his low interest rate policy, which drove up housing prices, producing home equity that consumers could tap and spend by refinancing their homes.

Unable to maintain their accustomed living standards with income alone, Americans spent their equity in their homes and ran up credit card debts, maxing out credit cards in anticipation that rising asset prices would cover the debts. When the bubble burst, the debts strangled consumer demand, and the economy died.

As I write about the economic hardships created for Americans by Wall Street and corporate greed and by indifferent and bribed political representatives, I get many letters from former middle class families who are being driven into penury. Here is one recently arrived:

"Thank you for your continued truthful commentary on the 'New Economy.' My husband and I could be it's poster children. Nine years ago when we married, we were both working good paying, secure jobs in the semiconductor manufacturing sector. Our combined income topped $100,000 a year. We were living the dream. Then the nightmare began. I lost my job in the great tech bubble of 2003, and decided to leave the labor force to care for our infant son.

Fine, we tightened the belt. Then we started getting squeezed. Expenses rose, we downsized, yet my husband's job stagnated. After several years of no pay raises, he finally lost his job a year and a half ago. But he didn't just lose a job, he lost a career. The semiconductor industry is virtually gone here in Arizona. Three months later, my husband, with a technical degree and 20-plus years of solid work experience, received one job offer for an entry level corrections officer. He had to take it, at an almost 40 percent reduction in pay. Bankruptcy followed when our savings were depleted. We lost our house, a car, and any assets we had left. His salary last year, less than $40,000, to support a family of four. A year and a half later, we are still struggling to get by. I can't find a job that would cover the cost of daycare. We are stuck. Every jump in gas and food prices hits us hard. Without help from my family, we wouldn't have made it. So, I could tell you just how that 'New Economy' has worked for us, but I'd really rather not use that kind of language."Policymakers who are banking on stimulus programs are thinking in terms of an economy that no longer exists. Post-war U.S. recessions and recoveries followed Federal Reserve policy. When the economy heated up and inflation became a problem, the Federal Reserve would raise interest rates and reduce the growth of money and credit. Sales would fall. Inventories would build up. Companies would lay off workers.

Inflation cooled, and unemployment became the problem. Then the Federal Reserve would reverse course. Interest rates would fall, and money and credit would expand. As the jobs were still there, the work force would be called back, and the process would continue.

It is a different situation today. Layoffs result from the jobs being moved offshore and from corporations replacing their domestic work forces with foreigners brought in on H-1B, L-1 and other work visas. The U.S. labor force is being separated from the incomes associated with the goods and services that it consumes. With the rise of offshoring, layoffs are not only due to restrictive monetary policy and inventory buildup. They are also the result of the substitution of cheaper foreign labor for U.S. labor by American corporations. Americans cannot be called back to work to jobs that have been moved abroad. In the New Economy, layoffs can continue despite low interest rates and government stimulus programs.

To the extent that monetary and fiscal policy can stimulate U.S. consumer demand, much of the demand flows to the goods and services that are produced offshore for U.S. markets. China, for example, benefits from the stimulation of U.S. consumer demand. The rise in China's GDP is financed by a rise in the U.S. public debt burden.

Another barrier to the success of stimulus programs is the high debt levels of Americans. The banks are being criticized for a failure to lend, but much of the problem is that there are no consumers to whom to lend. Most Americans already have more debt than they can handle.

Hapless Americans, unrepresented and betrayed, are in store for a greater crisis to come. President Bush's war deficits were financed by America's trade deficit. China, Japan, and OPEC, with whom the U.S. runs trade deficits, used their trade surpluses to purchase U.S. Treasury debt, thus financing the U.S. government budget deficit.

The problem now is that the U.S. budget deficits have suddenly grown immensely from wars, bankster bailouts, jobs stimulus programs, and lower tax revenues as a result of the serious recession. Budget deficits are now three times the size of the trade deficit. Thus, the surpluses of China, Japan, and OPEC are insufficient to take the newly issued U.S. government debt off the market.

If the Treasury's bonds can't be sold to investors, pension funds, banks, and foreign governments, the Federal Reserve will have to purchase them by creating new money. When the rest of the world realizes the inflationary implications, the US dollar will lose its reserve currency role. When that happens Americans will experience a large economic shock as their living standards take another big hit.

America is on its way to becoming a country of serfs ruled by oligarchs.

To find out more about Paul Craig Roberts, and read features by other Creators Syndicate writers and cartoonists, visit the Creators Syndicate web page at www.creators.com.

COPYRIGHT 2010 CREATORS.COM

The Saddest Story

One of the most unusual books and far-and-away the saddest I have ever read is James Douglass's "JFK and the Unspeakable: Why He Died and Why It Matters." This is the best documented account ever produced of why and how the CIA assassinated John F. Kennedy. That the CIA did this is beyond dispute, and that the first President Bush was involved is well established by Russ Baker's book "Family of Secrets." What separates Douglass's book from the pack is his account of how Kennedy lived his final months, the actions he took that turned the CIA against him but saved the world from a nuclear holocaust and -- had he lived -- would probably have avoided the Vietnam War and brought the Cold War to a swift and peaceful conclusion.

Kennedy was a cold warrior who turned away from orthodoxy and became a heretic to those within the military industrial spook complex. He defied the demands of the Joint Chiefs of Staff and the CIA on the Bay of Pigs and the Cuban Missile Crisis, on Laos and Congo, on Berlin and Indonesia and -- above all -- on Vietnam, in opening up a dialogue with Khrushchev and with Castro, by creating a nuclear test ban treaty with the Soviet Union, by taking on the steel corporations, by firing the director of the CIA and other top officials, by planting a false story that his military advisors opposed escalation in Vietnam, by ordering a withdrawal from Vietnam, by selling wheat to the Soviet Union, by publicly and privately setting an agenda for peace and complete disarmament and world law, and by making plans to visit the Kremlin and declare the Cold War over.

This is not the Kennedy we think we know. It is certainly not the Kennedy the History Channel claims to document. But this is a Kennedy thoroughly researched and documented by the author. And if the History Channel's portrait of a sex-obsessed president has any relevance to how Kennedy acted on the large issues of war and peace, then we have an absolute moral duty to get President Obama some girlfriends fast!

Douglass has been a religious writer on the topic of religion, and that background shows up in this book, especially in the opening pages, but this atheist did not find that framing of the story distracting or troubling in the least. This is a history text and a dramatic tale by a talented researcher and summarizer of facts and their broader import.

Kennedy was the president of a nation that had already -- long before the Bush-Cheney age -- transferred tremendous power from the legislative branch to the president. This was not government of the people, but government of the person. But it was a person under the threat of death if he stepped too far out of line, a person unable to control his own military and CIA, a person able to make progress toward world peace only once Khrushchev and Castro understood that Kennedy's greatest impediment was his own bureaucracy.

Douglass shows us that Kennedy knew he was risking assassination but chose to take that risk, and that Johnson and later presidents knew what had transpired and chose not to put their necks on the line. The fear that presidents, congress members, and millions of other Americans have lived with -- allowed themselves to live with, CHOSEN to live with -- since the Kennedy assassination is the unspeakable weight dragging our republic and the world back to the abyss that Kennedy so narrowly avoided during the missile crisis, and which the powers behind the US throne would have plunged the world into could they have had their way.

Last year, Congressman Barney Frank, whose every utterance is usually televised, held a press conference to propose cutting 25% from the military budget. Not a single reporter came. This is also the story of President Kennedy's greatest and least known speech, a commencement address he gave at American University on June 10, 1963 -- a thing of beauty that no politician in Washington, outside of Dennis Kucinich, would ever come close to uttering today. Kennedy spoke of complete disarmament and world government, and announced the unilateral cessation of nuclear testing. He was urging the public toward peace, reversing the relationship the public has had with politicians ever since. In private Kennedy wrote:

"Things cannot be forced from the top. The international relinquishing of sovereignty would have to spring from the people -- it would have to be so strong that the elected delegates would be turned out of office if they failed to do it. . . . War will exist until that distant day when the conscientious objector enjoys the same reputation and prestige that the warrior does today."

Kennedy, like any president or member of Congress, knew that decisions he made risked many other people's lives, including those of soldiers in the U.S. military. He found the courage to risk his own life in order to save those of many others. We must demand that our elected officials today, in an era of greatly expanded power for the CIA, act on the same courage. To do so, we must find that courage ourselves.

Sometimes a sad story can be a beautiful guide forward.

Prudential's billions will not pay off AIG's bailout debt

A $35bn deal with Prudential will not be enough to pay off the insurer's debt to the US taxpayer

Prudential's billions will still leave AIG with a huge bailout debt to the US taxpayer. Photograph: Mark Lennihan/AP

A few billion pounds from the man from the Pru will help. But even after offloading its Asian business, AIA, to Britain's Prudential for $35.5bn (£23bn), the US insurer AIG faces an epic struggle to pay back the vast amount of money it received in a contentious bailout from American taxpayers.

In three separate emergency injections of funding at the height of the credit crunch, AIG was handed $180bn by US authorities to avert a collapse considered likely to create a knock-on panic at the heart of the financial system. As a result, the US public owns 80% of the once-mighty insurer.

"I don't think it's responsible to say yet with certainty that the US taxpayer will or won't take a bath on AIG," said Bill Bergman, an insurance analyst at Chicago-based research firm Morningstar.

AIG is beginning to show signs of improvement in revenue as customers, once scared by the possibility of bankruptcy, return to the insurer. But liabilities keep mounting in the company's core casualty business, which indemnifies individuals and companies against damage to themselves and their properties.

"They appear to have stopped the bleeding on incoming premiums," said Bergman. "But they're pretty highly leveraged to the housing market and the credit market. Any further deterioration there is going to be a problem."

At the core of AIG's original implosion was its financial products arm, largely run out of a Mayfair office in London, which wrote billions of dollars of credit default swaps protecting financial institutions against default by trading partners. Once considered low-risk, these blew up spectacularly when the US mortgage market collapsed. In Britain, the Serious Fraud Office is probing the division, once characterised by the Federal Reserve boss Ben Bernanke as a "hedge fund … attached to a large and stable insurance company".

AIG's financial products arm is being wound down and other businesses are on the auction block to pay back bailout funds, although the continuing recession has made it difficult to get decent prices. AIG has sold its US car insurance business, its Tokyo headquarters building, and a reinsurance division for a total of nearly $6bn. It has struck a deal to sell a Taiwanese operation and is negotiating to sell a foreign life insurance arm for a possible $15bn to MetLife.

The company lost $10.9bn in 2009 – a hefty sum, but a significant improvement on its $99bn deficit in 2008. New boss Robert Benmosche, who became chief executive in August and condemned criticism of the company from "lynch mobs with pitchforks", is widely credited with steering AIG towards calmer waters.

To avoid the stigma of government support, the name AIG has been dropped from many businesses. The company's property and casualty business in the US is now known as Chartis. AIG's life and retirement insurances businesses in the US still have $240bn of assets, 16m customers and 300,000 staff – but the company is unlikely ever to reclaim the global dominance it once enjoyed.

When Debt-Junkies Go Broke, So Do Mercantilist Pushers

This Week's Theme: "I've got a bad feeling about this..."

Mercantilist nations with competitive advantages due to currency manipulations are the pushers/lenders; the consumer nations are the junkies.

This week's theme will be familiar to anyone who has seen the original Star Wars films in which Luke, Leia or Hans Solo utter the ominous words "I've got a bad feeling about this..." just before a crisis strikes.

I've got a bad feeling about the Eurozone and here's why: when debt-junkie consumerist nations go broke, so do their merchantilist pushers.

China, Japan and Germany are the mercantilist "pushers," the nations which are structurally dependent on exports for their growth and profits.

The U.S., the U.K., and the "PIIG" countries (Portugal, Ireland, Italy and Greece) are debt-junkies, endlessly borrowing vast sums to enable their addiction to public "Savior State" spending and private consumption.

Like any good drug pusher, the mercantilist nations lower the price of their goods via currency manipulations to hook the addict nations on their goods, and then feed the debt-junkies' consumerist "habit" with low-interest loans drawn from the immense profits reaped by selling to the junkies.

This arrangement is enhanced by a global environment of low-cost, abundant credit pumped out by central banks and governments everywhere.

The "trade" (heh) of goods paid for with money borrowed from the pusher continues to be a "good deal" for both pusher and junkie until the debt-addicted nations can no longer borrow enough to feed their "habit" and pay the interest on their fast-rising debts.

This occurs because it takes more and more debt to create a GDP "high" (the euphoria of endlessly rising consumption and resultant "growth" in GDP), just as the heroin addict finds it takes more and more "junk" to produce the desperately desired euphoria.

Mercantilist China's manipulation of currencies to create an unbeatable competitive advantage is very straightforward: it pegs the renminbi to the U.S. dollar. This is manipulation by fiat: it's more less the equivalent of strong-arm tactics to "introduce" the potential addicts to the exceedingly affordable pleasures of the "junk" (smack).

Germany pursued a much more subtle and pernicious strategy: the euro. In a poorly understood but brilliantly mercantilist move, highly efficient Germany roped the potential debt-junkie nations into the eurozone, in which all nations would become more efficient by sharing the common currency.

This sounded good to the consumerist nations, but they didn't understand that the euro gave Germany a stupendous structural competitive advantage: in effect, the euro raised the costs of less-efficient labor and capital in the PIIG nations, locking them into a currency which made German goods cheaper than domestically produced goods.

In the pre-euro era, when overconsumption and over-borrowing began crippling a PIIG economy, the imbalance could be corrected via currency depreciation. That is, the Greek drachma would fall in value versus the German mark, effectively raising the cost of German goods to Greeks, who would then buy less German products. Over time, the currency devaluation would restore the supply-demand and credit/debt balances between mercantilist and consumer nations.

Mercantilist nations' exports falter when consumer nations reduce consumption, so the merchantilists either peg their currency or manipulate it via other means (the euro) to keep the cost of their goods low. In the initial addiction phase, everyone is delighted with the arrangement; the mercantilist pusher-nations rapidly increase exports and profits (German exports rose by an astonishing 65% between 2000 and 2008), and the debt-junkie nations find they can borrow immense sums of money at low interest rates to support their consumerist habit.

Please see this BusinessWeek article for more on this topic: Angela Merkel, the EU's most powerful leader, has to save Europe from itself.

But eventually the "honeymoon" ends as the costs of servicing the stupendous debts incurred start rising, trimming consumption and imports as the debt-junkie nations have to divert more money to paying interest on past debt.

This makes global lenders nervous, as it becomes increasingly obvious that the rate of borrowing is completely unsustainable; the cliff of default is visible just ahead.

As noted above, this looming default is exacerbated by the pernicious need for ever-larger amounts of borrowed money to sustain feeble GDP "growth" (is it really growth if it's all based on borrowed money?). Borrowing rises astronomically, and as the risks become painfully obvious, interest rates rise, too, boosting the costs of servicing the debt accumulated in the "honeymoon" phase.

Now the mercantilist pusher-nations (China and Germany) are getting angry with their hapless junkies. They foolishly assumed the junkies would be able to borrow endless sums from someone other than the pusher-mercantilists themselves.

But alas, nobody except the oil-exporting nations is raking in the massive profits from exports which can be lent to the debt-junkies. The mercantilist pusher-nations are now the "last lender standing": there is no one else willing to lend to the obviously doomed debt-junkie nations except the pushers themselves.

The mercantilist pusher-nations are now in a bind. If they stop lending more money to the consumerist junkie-nations, then their exports and profits will dry up, triggering domestic turmoil. But if they continue bailing out the junkie-nations so they can keep buying the mercantilists' exports, then the mercantilists will become dangerously exposed to the inevitable default of the debt-junkie consumer nations as they attempt to overcome the growing imbalances by borrowing ever-greater sums of money.

China has attempted to bypass the mercantilist dilemma by squandering trillions of yuan in domestic stimulus which has mostly ended up in malinvestments like real estate speculation. China's real estate bubble is now so gigantic that its collapse is inevitable. The losses will be as spectacular as the crash.

Please see my article on AOL Daily Finance for why this is predictable: Why China Can't Cool Its Overheated Real Estate Boom

Germany is harrumphing and whining, but they face the same bleak choice as China: either bail out the debt-junkie nations so they can continue to buy more goods from export-dependent Germany, or let them collapse in default or withdraw from the eurozone, at which point they will no longer be able to afford German goods.

The unhealthy pusher-junkie relationship always ends badly; the junkie runs out of the ability to borrow more money to feed his habit, and the pusher has to abandon him to the gutter to either expire or suffer the agonies of debt-withdrawal.

The debt-junkie nations are already moaning in pain, and the mercantilist pusher-nations are annoyed and impatient. But it's the pushers who manipulated the currencies to create unbeatable competitive advantages, and so they have no one to blame but themselves.

They are now kicking the hapless debt-junkie nations in the ribs, demanding that they borrow the money needed to support their consumerist habits from somewhere, anywhere. But the lenders willing to extend cheap abundant credit have vanished. Now there is only increasingly costly credit available to the doomed junkie-nations, and even that will dry up soon enough as the end-game of default becomes ever more inevitable.

The biggest debt-junkie, the U.S., is blissfully high on the illusion that it can borrow money at near-zero-interest forever. It will soon be kicked in the ribs by reality and the delusionary high will turn into agonizing pain.

The mercantilists have supported the U.S. debt-junkie for years, enabling it to add trillions of dollars in debt every year. Now doubts are creeping in as it is becoming obvious to everyone that even the U.S. cannot borrow $1.6 trillion a year forever. Interest rates are about to notch higher, and at some point they will explode higher, dooming the debt-junkies, the U.S. included, to default or ever-higher interest rates.

What few seem to realize is that once the profits and reserves of capital dry up, then the well of cheap, abundant credit will be dry, too.

When the junkies go broke, so do the pushers.

State mulls unpaid leave

State agency heads are readying plans to furlough employees or reduce staff if necessary as revenues continue to decline and lawmakers remain at loggerheads over a plan to help agencies through the remaining months of the fiscal year.

At February's meeting, the Personnel Board also approved Auditor Stacey Pickering's request to reduce his staff by two, Mosley said.

House and Senate budget negotiators traded jabs Friday morning and left the Capitol for the weekend without an agreement to offset cuts to the 2010 budget.

Last week, the State Personnel Board signed off on a request from the Department of Human Services to furlough employees for up to four days in the remaining four months of the fiscal year, said Deanne Mosley, the board's chief of staff.

Julia Bryan, spokeswoman for DHS, said the request was put in as a "just-in-case." The department employs about 3,200.

"We have no plans at this time to furlough employees," Bryan said. "It's strictly strategy or pre-planning in the event that more budget cuts come down. That's the last thing we would want to do is have our employees off work."

The State Tax Commission said preliminary revenue collections for February are down $33 million, or 12.4 percent. Those numbers could shift somewhat as fee collections and other investments are added.

Regardless, February closes as the 18th consecutive month with revenues falling short of expectations. Gov. Haley Barbour said more cuts may be needed beyond the $458.5 million he has already trimmed.

The personnel board's February's actions were the first related to furloughs and layoffs since the worst of the recession hit state coffers. More are expected to follow.

"All the agencies are asking the State Personnel Board about what actions we may take if that's necessary," said Department of Mental Health Director Ed LeGrand.

About 32,000 state employees are under the purview of the personnel board, which must sign off on furlough and layoff plans before they can be carried out. The board does not have jurisdiction over employees at public schools, colleges and universities.

LeGrand said he can make it to June 30 without layoffs and furloughs so long as his budget is not cut again. Barbour has slashed $458.5 million from the state budget in four separate rounds of cuts to account for declining revenues.

Barbour asked the Legislature to remove employees out from under the Personnel Board for a two-year window to give agency heads staffing flexibility. The Senate signed off on legislation to do that, but the House isn't likely to go along. Tuesday is the committee deadline for nonrevenue bill action.At February's meeting, the Personnel Board also approved Auditor Stacey Pickering's request to reduce his staff by two, Mosley said.

The Department of Education also has announced plans for a staff reduction. And Department of Corrections Commissioner Chris Epps said he plans to hold back two weeks pay from his employees in June, and then move workers from a monthly to a bimonthly pay schedule.

Epps said employees will get their two weeks pay when they leave the department, whether via retirement, termination or resignation.

Agencies are anxiously awaiting a fiscal 2010 budget resolution, but negotiations are moving slowly. House and Senate leaders began negotiating Thursday on Senate Bill 2495, which would draw down state savings to restore some of the governor's cuts.

Talks began after the Senate voted Thursday to sustain Barbour's veto of a similar bill, but the negotiations are hung up over a disagreement on prison spending.

Senate Appropriations Committee Chairman Alan Nunnelee, R-Tupelo, offered to keep the House's numbers for public schools, but said Republican Senate leaders aren't budging from their position that the Legislature needs to give $16 million to MDOC.

The Mississippi Adequate Education program that funds K-12 schools would get around $34 million.

"We made significant movement, and we're hoping the House will respond in a similar fashion," Nunnelee said. MDOC has taken a $29.4 million cut.

The House leaders offered $10 million for MDOC, up from their original offer to repair $1 million to the agency. Both chambers would still have to sign off on any agreement that's reached among the half dozen budget negotiators.

House Appropriations Committee Chairman Johnny Stinger, D-Montrose, scoffed at Nunnelee's suggestion that Senate leaders were making a significant gesture of good faith.

"Let's don't play games with the people," Stringer said.What Are Banks Doing with Their Depositors' Money?

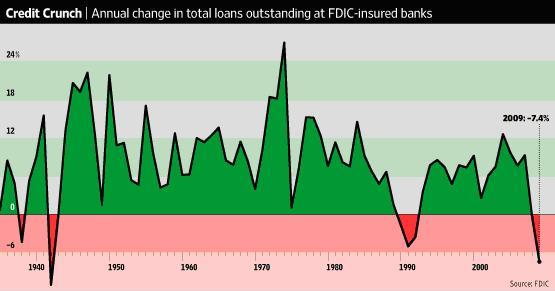

February 26, 2010 – There have been numerous reports about the sharp decline in bank lending since the beginning of the financial crisis. The Wall Street Journal, for example, on Wednesday reported in an article entitled “Lending Falls at Epic Pace” that last year’s decline in lending is the biggest since 1942. It also provided the following chart to clearly make its point.

So if the banks are not making loans, what are they doing with depositor money?

Well, they are still lending, but not to businesses and consumers. They are lending to the federal government.

Banks don’t lend directly to the federal government of course, but buying US government paper accomplishes the same thing in the end. Depositor money is sent to the federal government, ether directly when banks purchase newly issued government paper or indirectly when they purchase US government paper from others, who in turn have used their dollars to purchase this paper.

If we mark the beginning of the financial crisis with the collapse of Bear Stearns in March 2008, data from the Federal Reserve show that since then bank lending has declined by $220 billion. During this same period, banks increased the amount of US government paper they hold by $337 billion.

The change is even more dramatic when viewed from the peak of bank lending that occurred in the aftermath of the Lehman Brothers collapse. Companies cut off from the commercial paper market in the financial turmoil then prevailing turned to the banks for liquidity. By drawing down their credit lines, they caused bank loans to surge. Bank loans have now declined $646 billion from their October 2008 peak, as illustrated in the following chart.

This significant shift in bank assets has implications for the economy and the US dollar.

Instead of depositor money being used to stimulate economic activity in the private sector by lending to businesses and consumers, the banks are helping to fund the growing federal deficits. This re-allocation of resources has a negative long-term impact on the economy. Depositor money is not being used for productive purposes like building manufacturing plants and making other investments that will create jobs and grow the economy. It is being spent by the government, which consumes in the present and does not invest for the future.

This shift in bank assets also has negative implications for the dollar. As the realization grows that the financial condition of the federal government is not much different from Greece and the dozens of other over-indebted countries, the value of US government paper declines as a consequence of the US government’s deteriorating creditworthiness. Given that the quality of bank assets perforce determines the quality of the dollar, deterioration, i.e., debasement, of the dollar is inevitable as banks funnel depositor money into US government paper instead of making loans.

Lastly, the reduction in bank loans does not mean the money supply is shrinking. Rather, it is simply changing. More and more dollars (i.e., the liabilities on bank balance sheets) are being backed (i.e., the assets on bank balance sheets) by US government debt instead of loans to the private sector.

Gold, the IMF, and Dirty Jokes

How many IMF officials does it take to change a light bulb?

As you probably read, the International Monetary Fund announced they would proceed with selling the remaining 191.3 tonnes of gold from the 403.3 tonnes planned. The money is to be used for lending to poor countries. Lending implies the money will be repaid, which, in the case of the IMF, is a joke that isn’t funny. But that’s a topic for another day.

The IMF stated that sales will be conducted in the open market, which is interesting because until now, gold has only been made available to central banks. While the IMF remains open to central banks buying some of the gold, sales will be conducted “in a phased manner over time” to avoid disruptions to the open market.

So, will IMF sales depress the gold price? Well, remember the price rose with the first sale, when it was announced India was buying 200 tonnes of the 212 for sale. But that was an offtake deal, not an open market sale, so the question is legitimate.

One way to look at it is this: global mine production was 80.9 million ounces in 2009, so the IMF’s 6.7 million ounces could be a market-jolting 8.2% addition if dumped all at once. And an 8.2% load would indeed upset a market if we were talking about strawberries or anything else that people buy only for the purpose of consuming.

But most gold isn’t bought for the purpose of using it up. It’s bought for the purpose of holding it. So the relevant comparison for the IMF’s 6.7 million ounces isn’t annual mine production. Instead, we should compare it to the world’s existing stockpile of gold, which is roughly 2 billion ounces. The IMF sale would add just 0.3% to global inventory – hardly a market trasher.

Further, we’ve been down this road before with the IMF. When they sold gold in the 1970s, the price dropped upon the announcement of the sale, but then rose when actual sales took place.

And the dirty joke is this: when the IMF sold gold in the 1970s, it marked a bottom in the price. The late Jerome Smith advised always betting against the government: “When they’re unloading an asset, it’s time to buy.”

The IMF provides some very cushy jobs for the right people, along with a perpetual series of exquisitely catered conferences for the politically connected and politically correct. These people are not exactly known for being the brightest economic decision-makers. However noble their cause, the fact that they’re selling at all in the current environment, given the enormity of the monetary crisis that will only worsen as time goes on, tells me I want to be doing the opposite.

And that’s why the answers to my light bulb joke are as follows:

How many IMF officials does it take to change a light bulb?

None. Doesn’t gold glow in the dark?

One, but only if the ladder is padded.

Two. One to screw it in and one to screw it up.

Three, but nobody can find them.

Four, to form a panel to discuss which way to turn the bulb.

Five. One to change the bulb and four to buy the wine to celebrate.

Nine, to provide a quorum to vote on incandescent vs. fluorescent.

Eleven. One to hold the bulb, and ten to turn the house.

All of them. But only after dinner at L’Arpège (the most expensive restaurant in Paris).

While we’re convinced gold is headed much higher, is the recent correction over, signaling its time to jump in? Get our answer in the new issue of Casey’s Gold & Resource Report, which you can try risk-free here…

Snow-cialism

There is a silver lining to every snowstorm – getting to know your neighbors both good and bad. With forty inches on my block this week, I’ve learned a lot about my neighbors and, strangely enough, socialism.

My corner of Baltimore seems like a good place to ride out a storm. After all, innumerable cars are plastered with Obama bumper stickers, and windows display signs like “Universal Healthcare Now.” In essence, it’s a very liberal neighborhood in an extremely liberal state. What better neighborhood to be in times of need, right?

The architecture ranges from early 19th to early 20th century row homes, which as a result demands parallel parking. This isn’t a great inconvenience most of the time, but with the snow, it’s an absolute nightmare. First the clouds drop forty inches. Then the city snow plow piles another mountain from the street onto your car.

Successfully liberating the vehicle from its icy prison can take hours. After leaving the spot, anyone can take the laboriously freed space. Restoring regular parking conditions quickly requires everyone chipping in for the common good.

During this street clearing process, my neighbors sorted themselves into four groups:

- The Saint (1% of the neighborhood) – Every couple of blocks resides a truly amazing human being living to serve others. He’s shoveling out his neighbors’ cars, dumping bags of rock salt down the whole street, and passing out shovels like he owns a hardware store.

- The Good Citizen (15% of the neighborhood) – A caring person doesn’t just shovel enough snow to drive away. He carves out the front and back. After leaving his spot, someone else can parallel park without digging. If everyone did this, normal parking would resume in a day – if not less.

- The Self-Interested Person (70% of the neighborhood) – This guy doesn’t really care about helping anyone. He carves just enough in the front to get out. The next person must dig before parking.

- The Malicious Creep (14% of the neighborhood) – Instead of shoveling snow to the curb, the creep stacks snow onto his neighbor’s car. This saves the creep approximately fifteen minutes while adding an hour to his neighbor’s work.

While my neighbors love Obama and universal healthcare, they obviously aren’t such good socialists on their own block. This is no surprise; everyone on earth is an armchair Mother Theresa. We all have noble thoughts at the coffee shop or over beers. But when the snow shovel has to come out, so does the truth.

So let’s face it. Universal healthcare supporters are much like the folks on my street. There are a couple of saints, a few good people, and a large chunk who are either self-interested or just plain selfish. Most support it either because they will benefit directly, or they think the tax burden will not be placed on them.

Just look at this Gallup poll: only 34 percent believe that healthcare reform will personally increase their costs. Gallup also points out that most don’t think healthcare reform will benefit them personally – hence they are supposedly altruistic. But it’s not altruism when only 34 percent believe that they will do the shoveling.

You don’t think this is true? Just look at the Republican Party’s anti-universal healthcare campaign. The GOP hasn’t appealed to morality or fairness, but instead to selfish elements among universal healthcare supporters. The message is that the plan will cost more for everyone and your healthcare will get worse. So far the campaign has worked.

One can speak sweet nothings while pleasantly sitting around a warm fireplace. But in the end, a snowy day and a shovel will always reveal the selfish nature of a socialist underneath.

If you want to stay in the loop on what the Obama administration is planning and how to protect yourself – even profit from – the ramifications, give The Casey Report a risk-free try. Never get hoodwinked again because you will see the big trends coming long before they get here. Click here to find out more.

CNN host places Hawaii off the coast of South America

CNN host Rick Sanchez may have been trying to overdramatize this weekend's earthquake in Chile by placing Hawaii off the coast of Ecuador for his more geographically-challenged viewers.

Or maybe he just doesn't know where the Pacific island state is located.