Wednesday, November 13, 2013

The Big Lie: Lunch (and Debt) Are Free

Actions create consequences, and not

necessarily the consequences that were planned or expected.

A central tenet of propaganda is that the

Big Lie repeated often enough is accepted with greater ease than

small lies. Thus it is no surprise that the leadership and

propaganda organs of the Fed, Federal government and the Keynesian

cargo Cult of fellow travelers all repeat our era’s Big Lie: There

is a free lunch after all.

The common-sense saying that “there’s no

free lunch” has been refuted, according to the Fed and our

political “leadership” (if you call bought-and-paid-for toadies,

lackeys and apparatchiks for the monied classes “leaders”).

There are two free lunches, according to our

financial and political leaders: free money, in the form of money

created out of thin air by the Fed, and almost-free money borrowed

into existence by the Federal government.

With the Fed’s free lunch, trillions of

dollars are created and distributed to banks and those who can borrow

this free money for next to nothing.

In the Federal government’s almost free lunch

(it is almost free as a result of the Fed’s financial repression of

interest rates to zero, the infamous ZIRP – zero interest rate

policy), the central state borrows and blows essentially limitless

sums on favored cartels and constituencies: sickcare, global empire,

bridges to nowhere, etc.

We

are constantly reassured that the Fed can print (and distribute to

its banker buddies) $1 trillion a year with nothing but positive

consequences for the bottom 99.9%. On the fiscal side, the Federal

government borrowing and squandering $1+ trillion a year is heralded

as equally positive for everyone–especially the 49% of the populace

drawing a direct cash benefit from the Federal government: Census:

49% of Americans Get Gov’t Benefits; 82M in Households on Medicaid.

Possible blowback? None, or so we’re

told. If anything, the Keynesian parrots squawk, we need to

borrow and blow $2 trillion a year rather than a paltry $1+ trillion.

(We’re running out of cartels, quasi-monopolies, foreign wars, spy

agencies and other ratholes to pour trillions down; yikes, what a

problem for Krugman et al. Maybe the Martians can supply us with some

more rapacious cartels or a planetary war.)

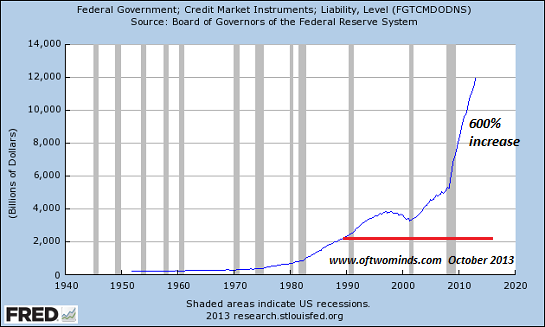

These two charts raise doubts about the

sustainability of the Fed and government’s free lunch. The

first is the monetary base, which just hit $3.5 trillion.

The

second one is Federal external debt, i.e. the Federal debt not

including “intergovernmental holdings,” what is “owed” to the

fictitious Social Security Trust Funds. Total national debt is $17

trillion, debt we actually have to roll over is $12 trillion and

rising by $1 trillion a year. Debt

to the Penny (U.S. Treasury site).

At the start of 2008, before the global

financial meltdown gathered momentum, debt owed to the public was

$5.1 trillion. Now it is $12.2 trillion, an increase of $7 trillion

in less than six years. According to the Big Lie, this is no

problem, and entirely sustainable: here’s your Free Lunch, America,

enjoy!

Big Lie, meet unintended consequences. The

problem with Big Lies is reality has not been disappeared; it still

exists. Actions create consequences, and not necessarily the

consequences that were planned or expected.

The Day The Bubble Became Official, And Everyone Was Happy

Wolf

Richter www.testosteronepit.com

www.amazon.com/author/wolfrichter

A

new era has dawned: there is now a consensus that

this is a stock market bubble. We’re back where we were during the

last bubble, or the one before it, though the jury is still out if

this is February 2000 or October 1999 or sometime in 2007. How do I

know it’s not just some intrepid souls on the bleeding edge who are

claiming this, but a consensus?

Bubble

data keep piling up relentlessly. IPOs so far this year amounted to

$51 billion, the highest for the period since bubble-bust year 2000,

the Wall

Street Journal reported. Of them, 62% were for companies

that have been losing money, the highest rate on record. Follow-on

offerings by companies that already had their IPO but dumped more

stock on the market amounted to $155 billion, the highest in

Dealogic’s book, going back to 1995. And throughout, the DOW and

the S&P 500 have been jumping from one new high to the next.

It’s even crazier in the land of bonds, where

issuers are dreading the arrival of higher interest rates – which

have already arrived. And they’re pushing everything possible out

the door while prices are still high. So far this year, $911 billion

in bonds were issued, also a Dealogic record. Emerging-market bond

issuance hit $802 billion, a notch below their all-time record last

year, but emerging-market bonds went into tailspin during the summer

taper-talk, which slowed things down temporarily.

These ominous clouds have been billowing up on

the horizon for a while, but nothing is a bubble until enough people

say it’s a bubble. And today, shortly before 10 a.m. Pacific Time,

it officially became one.

I

heard it on the last place where you normally hear this kind of

thing, on KQED Public Radio in San Francisco, on Forum,

a local show. Host Michael Krasny was chatting with New

York Times writer

Nick Bilton about Twitter as part of Bilton’s book tour. This isn’t

exactly Max Keiser’s whiplash-inducing

Keiser Report. This is soft-spoken public radio.

Twitter’s IPO shook up San Francisco. People

are waiting for the tsunami of money. Everyone talks about it. And

everyone talks about their gift to Twitter. Like all good corporate

citizens, Twitter got a huge tax break from San Francisco, and that

money is currently being extracted from everyone’s pockets.

In April 2011, the Board of Supervisors voted

to give Twitter and other companies that would relocate to Central

Market Street or the Tenderloin – not the most polished areas of

town – a six-year exemption from San Francisco’s 1.5% employment

tax. Twitter had threatened to leave and do whatever, if it didn’t

get it. Voilà. Corporate extortion works every time. Only new hires

would be impacted. At the time, the gift was estimated to be worth

$22 million.

So Twitter moved into its new digs, and the

headcount jumped, and salaries went up, and there has been some

turnover, and now the gift has grown to $56 million – and continues

to grow. Twitter too has become a corporate welfare queen.

But

not everyone is happy, given the hoopla of the IPO, the billions

involved, and the soaring rents in San Francisco as newly hired

employees of startups with no revenues stand in line to rent whatever

is available, rent not being much of an issue with their inflated

salaries. Like Twitter, these companies are under no pressure to make

money. So evictions jumped 38% between March 2010 and February 2013,

the last period for which data is available; “Ellis

Act” evictions – named after the state law that allows

landlords to evict tenants when they want to sell their property –

jumped 170%. Housing has been booming!

And

people are being pushed out of the city. So on Thursday, as Twitter’s

valuation settled on $31.7 billion, residents of San Francisco, who

not only have to pay for Twitter’s gift, but are now facing

ballooning rents or eviction, demonstrated in

front of Twitter’s headquarters. “People over profit,” a sign

said. “No to evictions,” another said. Or “$56 million in tax

breaks – Are you Twittin’ me?”

This conflict too – between the fake money

that pushes up prices, and long-term residents who can no longer

afford to live here – is a sign of a bubble. San Francisco has been

there before: in the late 1990s. It popped spectacularly.

“Why is Twitter not a total fad perpetuated

by yet another financial bubble in speculative tech stocks?” a

caller asked Bilton toward the end of the radio show. This sent

Bilton off on a tangent, away from promoting his book. There were

“bubble companies” that made you wonder “how on earth” they

would be “worth so much,” he said.

Pinterest

in San Francisco, an internet message board for images with 50

million monthly users, got $225 million in a round of funding that

valued the company at $3.8 billion – though it has zero revenues.

That a big chunk of the funding came from mutual fund company

Fidelity, instead of venture capital funds, raised even more

eyebrows. Or messaging app developer Snapchat in LA is stewing over

an investment that would value it at $3.5 billion, and it doesn’t

have any revenues either.

“I absolutely”

– emphasis his – “believe that we’re in another bubble,”

Bilton explained. “And it is going to pop,”

Companies like Pinterest with sky-high

valuations and no business model or revenues – what are they going

to do? Well, they either would have to be sold, which you can’t do

easily at these valuations, he said, “or they’re gonna pop.”

That, on KQED, made it official.

I

remember very well: in late 1999, everyone knew it

was a bubble, and the word “bubble” had become a common term,

though strenuously denied by Chairman Greenspan and others at the

Fed, and by other official mouthpieces of Wall Street, but those in

the marketknew.

They were just riding the wave, and the wave was too magnificent to

get off. Money was being fabricated. IPOs were flying off the shelf,

doubling and redoubling. Everyone was planning to get off the wave in

the nick of time, ahead of the rest of them. And everyone was happy.

Well not everyone. Not the poor souls who were

driven out of San Francisco because they couldn’t afford to live

here anymore. Not the folks who lost fortunes when it all blew up.

Not the Fed that claimed afterwards that you can’t see bubbles when

they’re inflating – which made the Fed look really stupid.

But

this time it’s different. Money is being fabricated. Investors are

riding the magnificent wave for as long as possible. And

they’re all planning

to get off the wave in the nick of time, ahead of the rest of them.

After

five years of QE, and $3 trillion in new money floating around, risk

is no longer priced into anything. In fact, it has disappeared as a

factor. And the Fed is publicly fretting about it. Read….. Watching

The Fed Marinate In Its Own Artfully Concocted Pickle

Treasury Will Issue Its First Floaters On January 29, 2014

As was long predicted and foreshadowed (and analyzed here previously with the proposed FRN term sheet shown

half a year ago), after nearly two years of foreplay with the idea of

issuing inflation-friendly floating rate notes, moments ago as part of

its refunding announcement, the Treasury announced the first floater

issuance in history would take place on January 29, 2014, will have a 2

year tenor, and will amount to between $10 and $15 billion.

From the press release:

As posted previously, here is what the Treasury proposes for an indicative FRN term sheet:

Away from the topic of FRNs, the TSY also indicated it will offer $70 billion in new paper to refund $63.5 billion, for net new cash proceeds of $6.5 billion. Recall that a few days ago, the Treasury announced it would increase its cash build by a whopping $60 billion in the quarter, hoping to leave it with $140 billion in total cash by December 31. Which begs the question: is the Treasury, in order to keep net collateral roughly flat in light of no Fed monetizing, now simply issuing more gross debt to build up cash with the proceeds? If so, this would mean that the Treasury and the Fed which is monetizing the bulk of its issuance, have reached a level of synchronicity unseen before, all of it simply to preserve the upward ramp in stocks.

Finally, and as largely expected, the Treasury once again reminded Congress to fix itself promptly (i.e., ignore the enabling impact of the Fed), and to lift the debt ceiling ahead of February 7, 2014.

From the press release:

As the TSY further adds in its refunding presentation, in 2014 FRN issuance is expected to amount to $105 billion, or 14% of the total $730 billion in project net borrowings (this number will change), and 20% in 2015 before "tapering" subsequently. Why? Unclear - perhaps by then the expected inflation that was the reason for the arrival of FRNs will be gone...Floating Rate Notes (FRNs)

Treasury intends to announce the details of the initial Floating Rate Note (FRN) auction on Thursday, January 23, 2014, with the first auction occurring on Wednesday, January 29, 2014. Settlement of the security will occur on Friday, January 31, 2014.

The FRN is the first new product that Treasury has brought to market in 17 years. The FRN will have a maturity of two years and Treasury anticipates that the size of the first auction will be between $10 and $15 billion.

Specific terms and conditions of each FRN issue, including the auction date, issue date, and public offering amount, will be announced prior to each auction. For more details about the new Treasury FRN product, including a term sheet, FRN auction rules, and Frequently Asked Question, please see:

http://www.treasurydirect.gov/instit/statreg/auctreg/auctreg.htm

In addition, a tentative auction calendar that includes Treasury FRNs can be found at:

http://www.treasury.gov/resource-center/data-chart-center/quarterly-refunding/Pages/default.aspx

As posted previously, here is what the Treasury proposes for an indicative FRN term sheet:

Away from the topic of FRNs, the TSY also indicated it will offer $70 billion in new paper to refund $63.5 billion, for net new cash proceeds of $6.5 billion. Recall that a few days ago, the Treasury announced it would increase its cash build by a whopping $60 billion in the quarter, hoping to leave it with $140 billion in total cash by December 31. Which begs the question: is the Treasury, in order to keep net collateral roughly flat in light of no Fed monetizing, now simply issuing more gross debt to build up cash with the proceeds? If so, this would mean that the Treasury and the Fed which is monetizing the bulk of its issuance, have reached a level of synchronicity unseen before, all of it simply to preserve the upward ramp in stocks.

Finally, and as largely expected, the Treasury once again reminded Congress to fix itself promptly (i.e., ignore the enabling impact of the Fed), and to lift the debt ceiling ahead of February 7, 2014.

Good luck with getting a functioning congress as long as the Fed is around.Debt Limit

The debt limit places a limitation on the total amount of money that the United States government is authorized to borrow to meet its existing legal obligations, including Social Security and Medicare benefits, military salaries, interest on the national debt, tax refunds, and other payments. Raising the debt limit does not authorize new spending commitments; it simply allows the government to finance existing legal obligations that Congresses and presidents of both parties have made in the past.

The Continuing Appropriations Act, 2014 suspended the debt limit through February 7, 2014. A new debt limit will be calculated on February 8, 2014 in the manner prescribed by the Act. At that time, Treasury will have extraordinary measures available, which will allow the government to continue to finance its obligations for a period of time.

During the recent debt limit impasse, concerns that the debt limit would not be increased before extraordinary measures were exhausted led to significant disruptions in the secondary market for short-dated Treasury securities and a measurable increase in borrowing costs for newly issued Treasury bills. As such, Treasury respectfully urges Congress to provide certainty and stability to the economy and financial markets by acting to raise the debt limit well before February 7, 2014.

Permanent Austerity In Front Of All Kinds Of Ridiculous Gold Things

REUTERS/Neil Hall

From HuffPo:

David Cameron

has suggested that public spending should continue to be squeezed in a

"fundamental culture change" that would leave the British public sector

"permanently" slimmed down.

Speaking at the Lord Mayor's Banquet in

the City of London, he said the best way to keep the cost of living down

was to take "difficult decisions on public spending" to leave "a state

we can afford".

What everyone is talking about though is the photo of Cameron making this call for lower spending.Among the items featured in the photo:

- A huge gold throne.

- A gold speech stand.

- Several expensive looking glasses and chalices filled with wine.

- A random silver horse.

- A huge necklace on the lady sitting on the throne.

- Tuxes with white ties.

REUTERS/Neil Hall

House Voted to Get Banksters Back in the Derivatives Business

Wholesale destruction of U.S. economy may now continue without interruption

Kurt Nimmo

In late October, the House passed a “bipartisan tweak” to the Dodd-Frank bill Congress earlier passed off as “reform” after the banksters nearly crashed the financial system in 2008.

H.R. 992, the Swaps Regulatory Improvement Act, authored primarily by Citibank lobbyists, will allow predatory Wall Street financial institutions to once again engage in high-risk derivatives trading. Losses will be socialized and paid for by the American taxpayer through the Federal Deposit Insurance Corporation or FDIC.

“Citigroup’s recommendations were reflected in more than 70 lines of the House committee’s 85-line bill,” Eric Lipton and Ben Protess wrote for the New York Times. “Two crucial paragraphs, prepared by Citigroup in conjunction with other Wall Street banks, were copied nearly word for word.”

Co-sponsors of the bill are on the Citibank payroll. They received

nearly 17 times more money from the bank than have members of the House

who have not signed on as co-sponsors, according to Forbes. “Citigroup

has given $503,150 to current members of the House of Representatives,”

writes Tom Groenfeldt.

“Representative Jim Himes, D-Conn., has received $66,450 from

Citigroup, more than any other member of the House of Representatives.

Himes is a co-sponsor of the bill.”

Wall Street lobbyists targeted House Democrats. 70 of them came out in support of the bill. Only two Republicans voted thumbs down. They were washed away by overwhelming support for bankster criminality.

According to the chairman of the House Financial Services Committee, Representative Jeb Hensarling, a Republican from Texas, the Dodd-Frank bill revamp will fix the economy. “America‘s economy remains stuck in the slowest, weakest nonrecovery recovery of all times,” he said on October 30. “Those who create jobs for America are drowning in a sea of red tape preventing them.”

Hensarling didn’t explain how allowing large banks to play high-stakes blackjack and then force a beleaguered American taxpayer pick up billions in losses will create jobs.

Left to their own devices, banksters will create new “unusual or exigent circumstances” Frank-Dodd was supposedly passed to address. Bank lobbyists have successfully rolled back sections of Frank-Dodd and are now working feverishly to institute a return of the heyday of unencumbered derivatives criminality.

Congress is a wholly owned subsidiary of the bankers and the global elite. The so-called Dodd–Frank Wall Street Reform and Consumer Protection Act signed into law by Obama in 2010 was largely devised as a propaganda device to placate Americans outraged by the “too big to fail” bail-out swindle.

Not surprisingly, Dodd-Frank has been left to twist in the wind. As of June, 175 of 279 passed Dodd-Frank deadlines have been missed. Government regulators have neglected 70.1 percent of rulemaking deadlines and 99.6 percent of 280 rules with specified deadlines, according to Bank Credit News.

Frank-Dodd was never a serious attempt to “reform” bankster financial institutions. Citibank and the money mobsters have paid off Congress. In turn Congress has given the Mafia dens up and down Wall Street a wink and a nod. No significant reform will be forthcoming.

Source: Infowars

Distributed by RINF Alternative News

Kurt Nimmo

In late October, the House passed a “bipartisan tweak” to the Dodd-Frank bill Congress earlier passed off as “reform” after the banksters nearly crashed the financial system in 2008.

H.R. 992, the Swaps Regulatory Improvement Act, authored primarily by Citibank lobbyists, will allow predatory Wall Street financial institutions to once again engage in high-risk derivatives trading. Losses will be socialized and paid for by the American taxpayer through the Federal Deposit Insurance Corporation or FDIC.

“Citigroup’s recommendations were reflected in more than 70 lines of the House committee’s 85-line bill,” Eric Lipton and Ben Protess wrote for the New York Times. “Two crucial paragraphs, prepared by Citigroup in conjunction with other Wall Street banks, were copied nearly word for word.”

Wall Street lobbyists targeted House Democrats. 70 of them came out in support of the bill. Only two Republicans voted thumbs down. They were washed away by overwhelming support for bankster criminality.

According to the chairman of the House Financial Services Committee, Representative Jeb Hensarling, a Republican from Texas, the Dodd-Frank bill revamp will fix the economy. “America‘s economy remains stuck in the slowest, weakest nonrecovery recovery of all times,” he said on October 30. “Those who create jobs for America are drowning in a sea of red tape preventing them.”

Hensarling didn’t explain how allowing large banks to play high-stakes blackjack and then force a beleaguered American taxpayer pick up billions in losses will create jobs.

Left to their own devices, banksters will create new “unusual or exigent circumstances” Frank-Dodd was supposedly passed to address. Bank lobbyists have successfully rolled back sections of Frank-Dodd and are now working feverishly to institute a return of the heyday of unencumbered derivatives criminality.

Congress is a wholly owned subsidiary of the bankers and the global elite. The so-called Dodd–Frank Wall Street Reform and Consumer Protection Act signed into law by Obama in 2010 was largely devised as a propaganda device to placate Americans outraged by the “too big to fail” bail-out swindle.

Not surprisingly, Dodd-Frank has been left to twist in the wind. As of June, 175 of 279 passed Dodd-Frank deadlines have been missed. Government regulators have neglected 70.1 percent of rulemaking deadlines and 99.6 percent of 280 rules with specified deadlines, according to Bank Credit News.

Frank-Dodd was never a serious attempt to “reform” bankster financial institutions. Citibank and the money mobsters have paid off Congress. In turn Congress has given the Mafia dens up and down Wall Street a wink and a nod. No significant reform will be forthcoming.

Source: Infowars

Distributed by RINF Alternative News

ALERT ODD NEWS Venezuela’s Military Seizes Electronics Stores, Slashes Prices Just Before Elections

Venezuela’s military seizes electronics chains, slashes prices

A month before municipal elections, some say the socialist government is trying to buy votes even as the economy spirals.

CARACAS, Venezuela — In his fight against the “economic war” he says the political opposition, in collusion with the United States, is waging against Venezuela, President Nicolas Maduro ordered the military occupation of electronics chains over the weekend and summoned the public to come shop at government-enforced “fair” prices.

The orders against Daka, KVG and Krash, which are basically Venezuelan equivalents of Best Buy, sparked chaos at the stores’ outlets. The authorities arrested five store managers and said they will be prosecuted for unjustifiably raising prices.

Jim Rickards on the Recession of 2014 and Greek Islands for Sale

Chat

room hours will be closed from 9-5, at least if you’re employed by

a big bank. That’s right, banks may start disabling electronic

chat-rooms following regulator scrutiny. We’ll tell you all about

it coming up.

And is there no where safe to keep your

bitcoins? Sadly, that might be the case. Some “bitcoin-bandits”

made off with over $1 million worth of electronic booty. We’ll tell

how they did it.

Finally, we have seen an unprecedented

expansion in the monetary base over the past decade. However this

phenomenon is not just limited to the US: Canada, South Africa, and

Japan have all facilitated extraordinary expansions of their monetary

bases, leading some to call this a competitive debasement of

currency. In 2010 Guido Mantega, Brazil’s finance minister,

famously proclaimed “We’re in the midst of an international

currency war, a general weakening of currency.” That was three

years ago, so where are we now? We talk to James Rickards, author of

of the bestselling book, “Currency Wars.”

Check

us out on Facebook

http://www.facebook.com/BoomBustRT

http://www.facebook.com/BoomBustRT

Follow

us @

http://twitter.com/ErinAde

http://twitter.com/ErinAde

7 Things No One Tells You About Being Homeless

#7. It Doesn't Take Much to Wind Up Homeless

Jupiterimages/Stockbyte/Getty Images

Jupiterimages/Stockbyte/Getty Images George Doyle/Stockbyte/Getty Images

George Doyle/Stockbyte/Getty Images"Of course we accept cigarette butts and burrito receipts as legal tender."

I had moved to Montana after finishing up my worthless liberal arts degree. I moved in with some cool folks my age and started a six-month contract job. It was an AmeriCorps position with weeklong shifts working in the wilderness, building hiking trails and whatnot, followed by a week off to spend in town. I was halfway through my contract when I found myself homeless. There are people with worse stories, of course -- many homeless are mentally ill, or maybe their parents kicked them out of the house for being gay when they were teenagers -- the point is, the line between where you are now and sleeping in your car is much, much thinner than you think.

Jupiterimages/liquidlibrary/Getty Images

Jupiterimages/liquidlibrary/Getty ImagesSometimes it isn't so much a "line" as "peeing in your boss's coffee."

#6. Having a Job Won't Save You

Comstock Images/Stockbyte/Getty Images

Comstock Images/Stockbyte/Getty Images Hemera Technologies/AbleStock.com

Hemera Technologies/AbleStock.com"Have you considered a Prius?"

First up: the ability to prepare food. I had to buy a camp stove and a mess kit, which will generally run you about $150 for stuff you can be reasonably sure won't break, plus you have to continuously pay for the fuel. I didn't want to get in trouble for sleeping in town, so I drove out into the woods to sleep, which meant I had to keep buying gasoline. Even people who work with their hands need to clean up and shower, so I spent the occasional night at a youth hostel or cheap motel ($25 to $50 a night) just to get access to running water and a mirror. Then there are all of the little complications that come from, for instance, not owning a refrigerator to store food in -- and every little thing costs you.

Jupiterimages/Photos.com/Getty Images

Jupiterimages/Photos.com/Getty ImagesBuying cheese by the wheel is a mistake I only made four or five times.

And I was fortunate because it was summertime -- winter camping in Montana would have made all of this far more complicated and much more expensive (it costs money to keep warm, no matter how you do it, and the odds of accidentally setting yourself on fire somehow rise exponentially). Still, I had to start buying rooms at the hostel or motel more frequently as fall set in and the weather got colder. I was working full time and taking care of no one other than myself, and I still couldn't afford to drag myself out of homelessness.

Digital Vision./Photodisc/Getty Images

Digital Vision./Photodisc/Getty ImagesForget making it rain -- I could barely make condensation.

#5. Government Benefits Aren't as Much Help as You Think

Spike Mafford/Photodisc/Getty Images

Spike Mafford/Photodisc/Getty Images

Ryan McVay/Photodisc/Getty Images

Ryan McVay/Photodisc/Getty ImagesNot pictured: a fucking Coleman stove.

But what about food stamps? Well, the problem with EBT -- the food stamps card -- is that, with little exception, you can only buy stuff that needs to be prepared at home, and if you're homeless, that means it's kind of like one of those cruelly ironic wishes granted by a genie. And unless you're in California, Arizona, Florida, or Michigan, you can't use food stamps to buy food at restaurants.

George Doyle/Stockbyte/Getty Images

George Doyle/Stockbyte/Getty Images

Sorry, kid. The Sizzler ain't for the likes of you.

So, I used the EBT to load up on food that I needed to cook, which meant I was using my cook stove more, which meant more money spent on fuel. Plus, you're not allowed to start fires in town, obviously, so cooking often meant yet another car trip, which meant more driving and more money spent on gas. In general, it just gave me an expensive commute every day. The food stamps were helpful, obviously, in that I have no idea how I would've survived without them. But like everything else, they were severely hindered by the realities of my situation.

Photodisc/Photodisc/Getty Images

Photodisc/Photodisc/Getty ImagesThere's much less smiling on the eighth night of this.

#4. Shelters Are a Band-Aid

Hemera Technologies/PhotoObjects.net

Hemera Technologies/PhotoObjects.net Medioimages/Photodisc/Photodisc/Getty Images

Medioimages/Photodisc/Photodisc/Getty ImagesThe lumbar support is unbelievable.

Many shelters are so overcrowded that people staying there have to arrive at 4:30 in the afternoon to even have a chance of getting a bed that night, which means cutting out of work early, which means risking losing your job, which exacerbates the problem you're trying to escape. There's also evidence that the stress of living in a homeless shelter makes you more prone to violence than living on the street.

BananaStock/BananaStock/Getty Images

BananaStock/BananaStock/Getty ImagesClose proximity to a Home Depot doesn't help.

Visions of America / UIG / Getty

Visions of America / UIG / GettyIf Los Angeles had seasons, this would be an even worse problem.

Meet One Of The Victims Of Obama’s “Economic Recovery”

Have you ever cried yourself to sleep because you had no idea how you

were going to pay the bills even though you were working as hard as you

possibly could? You are about to hear from a single mother that has

been there. Her name is Yolanda Vestal and she is another victim of Obama‘s “economic recovery”. Yes, things have never been better

for the top 0.01 percent of ultra-wealthy Americans that have got

millions of dollars invested in the stock market. But for most of the

rest of the country, things are very hard right now. At this point, more than 102 million working age Americans do not have a job, and 40 percent

of those that are actually working earn less than $20,000 a year in

wages. If we actually are experiencing an “economic recovery”, then why

is the federal government spending nearly a trillion dollars a year

on welfare? And that does not even include entitlement programs such as

Social Security and Medicare. We live in a nation where poverty is exploding

and the middle class is shrinking with each passing day. But nothing is

ever going to get fixed if we all stick our heads in the sand and

pretend that everything is “just fine”.

What you are about to read is an open letter to Barack Obama that has gone absolutely viral on the Internet in recent days. It is a letter that a single mother named Yolanda Vestal posted on her Facebook page, and it has really struck a nerve because countless other young parents can clearly identify with what she is going through. The following is the text of her letter…

And now that food stamps are being cut back, more of them than ever are going to be forced to turn to food banks for help. The following is what the head of a large food bank in Casper, Wyoming told one local newspaper about the increase in demand that he is witnessing in his area…

That is a lot of people.

And while Barack Obama may trot out a few vets on national holidays and promise that “we will never forget” them, the truth is that most of the time the federal government treats our military veterans like human garbage. If you doubt this, please see my previous article entitled “25 Signs That Military Veterans Are Being Treated Like Absolute Trash Under The Obama Administration“.

Meanwhile, anger and frustration with the economy are starting to rise to very dangerous levels in this nation.

In a previous article, I noted that violent crime in America rose by 15 percent last year. One of the primary reasons for this is the economic despair that we see in our streets.

As the economy gets even worse, people will become even more desperate. We will start to see even more flash mob crimes like we saw in Chicago recently. Posted below is a video news report that shows footage of a flash mob in Chicago dragging entire racks of merchandise out of a Sports Authority store…

When you watch stuff like this, it helps to explain why demand for armored vehicles among the ultra-wealthy in America is skyrocketing.

Unfortunately, most Americans cannot afford armored vehicles and walled vacation homes in the middle of nowhere.

Most Americans are going to have to live right in the middle of all of this as it happens.

A volcano of anger, frustration and despair is simmering just below the surface in America.

When that volcano finally erupts, it is going to be a very frightening thing to behold.

Distributed by RINF Alternative News

What you are about to read is an open letter to Barack Obama that has gone absolutely viral on the Internet in recent days. It is a letter that a single mother named Yolanda Vestal posted on her Facebook page, and it has really struck a nerve because countless other young parents can clearly identify with what she is going through. The following is the text of her letter…

Dear President Obama,These are the kinds of emotions that millions of American parents are wrestling with on a daily basis. Many of them are working as hard as they possibly can and yet still find themselves unable to adequately provide for their families.

I wanted to take a moment to say thank you for all you have done and are doing. You see I am a single Mom located in the very small town of Palmer, Texas. I live in a small rental house with my two children. I drive an older car that I pray daily runs just a little longer. I work at a mediocre job bringing home a much lower paycheck than you or your wife could even imagine living on. I have a lot of concerns about the new “Obamacare” along with the taxes being forced on us Americans and debts you are adding to our country. I have a few questions for you Mr. President.

Have you ever struggled to pay your bills? I have.

Have you ever sat and watched your children eat and you eat what was left on their plates when they were done, because there wasn’t enough for you to eat to? I have.

Have you ever had to rob Peter to pay Paul, and it still not be enough? I have.

Have you ever been so sick that you needed to see a doctor and get medicine, but had no health insurance because it was too expensive? I have.

Have you ever had to tell your children no, when they asked for something they needed? I have.

Have you ever patched holes in pants, glued shoes, replaced zippers, because it was cheaper than buying new? I have.

Have you ever had to put an item or two back at the grocery store, because you didn’t have enough money? I have.

Have you ever cried yourself to sleep, because you had no clue how you were going to make ends meet? I have.

My questions could go on and on. I don’t believe you have a clue what Americans are actually going through and honestly, I don’t believe you care. Not everyone lives extravagantly. While your family takes expensive trips that cost more than most of us make in two-four years, there are so many of us that suffer. Yet, you are doing all you can to add to the suffering. I think you are a very selfish and cold hearted man, who does not care what is best for the people he was elected by (not by me) to represent, but more so out for the glory of your name attached to history. So thank you Mr. President, thank you for pushing those of us that are barely staying afloat completely under water and driving America into the ground. You have made your mark in history, as the absolute worst and most hated president of the United States. God have mercy on your soul!

Sincerely,

Yolanda Vestal

Average American

And now that food stamps are being cut back, more of them than ever are going to be forced to turn to food banks for help. The following is what the head of a large food bank in Casper, Wyoming told one local newspaper about the increase in demand that he is witnessing in his area…

Across the state, food banks and other related programs aiming to feed the needy are worried the supply to meet the uptick in need during the holiday season won’t meet the growing demand for food caused by the expiration of SNAP benefits.And of course this is not just happening in rural areas either. Margarette Purvis, the head of the largest food bank organization in New York City, says that she is anticipating a huge surge in demand and thatveterans are being hit particularly hard…

“People are scared to death of the lack of food availability,” Martin said.

Martin called Joshua’s Storehouse a reliable barometer for measuring the rate of need in Casper. The number of people using the food bank skyrocketed before the reduction in SNAP, he said.

Fewer than 2,000 people used the food bank in October 2012. Last month 2,500 people went there for help.

“On this Veterans Day, when we’re waving our flags — I need every New Yorker to know — 40 percent of New York City veterans are relying on soup kitchens and pantries.”Purvis says that there are 95,000 vets relying on food banks in New York City alone.

That is a lot of people.

And while Barack Obama may trot out a few vets on national holidays and promise that “we will never forget” them, the truth is that most of the time the federal government treats our military veterans like human garbage. If you doubt this, please see my previous article entitled “25 Signs That Military Veterans Are Being Treated Like Absolute Trash Under The Obama Administration“.

Meanwhile, anger and frustration with the economy are starting to rise to very dangerous levels in this nation.

In a previous article, I noted that violent crime in America rose by 15 percent last year. One of the primary reasons for this is the economic despair that we see in our streets.

As the economy gets even worse, people will become even more desperate. We will start to see even more flash mob crimes like we saw in Chicago recently. Posted below is a video news report that shows footage of a flash mob in Chicago dragging entire racks of merchandise out of a Sports Authority store…

When you watch stuff like this, it helps to explain why demand for armored vehicles among the ultra-wealthy in America is skyrocketing.

Unfortunately, most Americans cannot afford armored vehicles and walled vacation homes in the middle of nowhere.

Most Americans are going to have to live right in the middle of all of this as it happens.

A volcano of anger, frustration and despair is simmering just below the surface in America.

When that volcano finally erupts, it is going to be a very frightening thing to behold.

Distributed by RINF Alternative News

Mike Maloney: Expect First Real Deflation, Then Hyperinflation

In this video, Mike Maloney is being asked

where he sees the economy going in terms of inflation vs deflation.

To answer that question, he refers to the book he wrote about a

decade ago, in which he wrote the following:

“First

the threat of deflation, followed by a helicopter drop, followed by

big inflation, followed by real deflation, and then followed by

hyperinflation.”

Why does Maloney think so? Because the gigantic

expansion of base money (which is the monetary base as created by the

US Fed and visible on its balance sheet) is being offset by a

collapse of the other monetary aggregates, a trend started in 2008.

Furthermore, the deflation could be much, much

worse than the ones the world experienced in the 30ies. Why? Because

of the scale of the ongoing emergency measures. This scale is not

clear to most people. These are truly emergency measures … for 4

years in a row. For the Chairman Mr. Bernanke coming out not willing

to taper is an admission that the whole system is ready to crash

again and that there is no recovery.

“This

type of monetary measures cannot come without economic consequence.”

The Poverty of Capitalism and the struggle for another world.

The

current global economic crisis has been covered extensively within

academic literature and the wider (social) media alike. Few, however,

have tackled the topic with the ambition of questioning capitalism

itself. John Hilary’s book The Poverty of Capitalism: Economic Meltdown and the Struggle for What Comes Next(Pluto

Press, 2013) is a welcome exception here. In this blog post, I will

provide a critical engagement with this excellent analysis of capitalist

crisis and moves towards alternatives.

The power of transnational capital

The

global garments industry is closely controlled by brand names and

retailers, who relentlessly squeeze suppliers in producing more cheaply.

Unsurprisingly, working conditions in this sector are characterised by

super-exploitation with a disregard for issues such as health and

safety. The recent collapse of

the Rana Plaza factory in Bangladesh, when more than 1000 people were

killed is only one of the most extreme examples of the consequences of

poor working conditions in this sector. In relation to food production,

‘as with the garments sector, the production, distribution and

consumption of food are already dominated by a small number of giant

transnational corporations who seek to determine what is grown and what

is eaten in all corners of the globe. As with the extractive sector,

capital has become increasingly aggressive in its attempts to

appropriate the natural resources necessary for its further expansion:

land, seeds, water and

the genetic building blocks of life itself’ (P.118). In short, global

capitalism has intensified exploitation across borders with the peoples

of the Global South bearing yet again the brunt of the onslaught.

The rise of the BRICS and CSR as hopes for alternatives?

John

Hilary dismisses hopes that the rise of the BRICS, Brazil, Russia,

India, China and South Africa, will result in a dramatic change in

global capitalism. Yes, the balance of power in the global economy is

changing, but capitalism itself has not been undermined. ‘Instead of the

traditional division between the capital-exporting countries of the

North and the capital-importing countries of the South, the increasing

accumulation of capital in the semiperiphery has generated a new wave of

imperialism from the emerging economies themselves’ (P.34). At the same

time inequality across the globe is increasing between countries, but

also within countries and the BRICS are no exception here. ‘In the

emerging economies of India and China, similar increases in inequality

have taken place against the backdrop of hundreds of millions living in

absolute poverty (P.18). Interestingly, the position of transnational

capital has actually been strengthened rather than weakened as a result

of the rise of the BRICS. ‘The G20’s decision to resurrect the failed

institutions of twentieth-century globalization

in the interests of transnational capital represents the greatest

structural continuity between the new world order and the old’ (P.29).

What alternatives beyond capitalism?

|

| Photo by seven-resist |

As

important as all these examples of change are, it is this aspect of the

book where I find myself in slight disagreement with John Hilary. I am

not convinced that the majority of the ‘global justice movement’ has

declared itself opposed to capitalism as such rather than criticising

the most negative outgrowths of neo-liberalism. Nor does the

re-emergence of the state as an important actor of development in Latin America

point towards a future beyond capitalism. As John Hilary acknowledges

himself, at the national level ‘several of the “pink” governments have

actually augmented the power of capital both nationally and

internationally, maintaining their socially progressive credentials

through pro-poor welfare programmes, but at the expense of any

structural change’ (P.146). Capitalism as such is not challenged. Is

John Hilary slightly too optimistic when assessing the current potential

for moves beyond capitalism? Perhaps, but then there are many studies

simply re-asserting the dominance of capitalism. In a way, it is

refreshing that The Poverty of Capitalism goes into the opposite direction.

|

| Photo by Sterneck |

The

struggle over the future world order is open ended. It is these

struggles, which can function as vehicles, ‘by which to develop an

international class consciousness over and against the very real

challenges posed by globalization

to transnational solidarity’ (P.116). Solidarity is always the result

of concrete struggles, and it is in this respect, that John Hilary’s

positive assessment of the current situation may be justified. Hence, to

conclude with his words, ‘the struggle for alternatives beyond

capitalism is what makes another world possible. Even in the midst of

crisis, that world is already coming into view’ (P.161).

An impressive book, a must read for all those interested in transformative change beyond capitalism!

The official Andreas Bieler blog can be found here.

Prof. Andreas Bieler

Professor of Political Economy

University of Nottingham/UK

Personal website: http://andreasbieler.net

12 November 2013Distributed by RINF Alternative News

Coming Pension Meltdown: The 10 Most Troubled City Systems

Monday, 11 Nov 2013 04:21 PM

Voters in Cincinnati last week soundly defeated a ballot initiative which would have overhauled the pension system for public workers, leaving the city without a plan to deal with $872 million in unfunded liabilities.

Cincinnati is not alone.

Across the nation, cities and states are finding funding for basic services being crowded out of their budgets by the rising cost of retirees' pensions and healthcare.

The Cincinnati initiative would have turned the public pension system into a 401(k) style-plan and require the city to pay off its unfunded liabilities in 10 years.

Urgent: Do You Approve Or Disapprove of President Obama's Job Performance? Vote Now in Urgent Poll

It failed 78 percent to 22 percent, an example of the opposition that cities face when trying to tackle the politically sensitive issue of funding retirees' benefits.

More and more cities, counties, and even some states will face the harsh reality of having to fix their pension systems or deal with a Detroit-style bankruptcy.

"This is happening in too many cities and towns across America, where social services, because they can be cut, are cut. Because pensions and bonds constitutionally cannot be cut, they're the protected class," Wall Street financial analyst Meredith Whitney told CNBC.

"I think you're going to see a real issue of neighbor against neighbor on these very issues," said Whitney, who recently co-founded Kenbelle Capital LP, a New York hedge fund.

Whitney argues in her recently released book, "Fate of the States: The New Geography of American Prosperity," that cities and states which delay addressing the crisis will witness a continued decline in growth.

A study by the Pew Center earlier this year looked at 61 cities — those with populations over 500,000 plus the largest city in each state — and found a total gap of $217 billion between pension and retiree healthcare obligations and the funding saved to pay those costs.

According to Pew, those cities had a total pension liability of $385 billion, with 74 percent funded, leaving a $99 billion shortfall.

The situation regarding retiree healthcare benefits in those cities is far worse, with a total of $126.2 billion of liabilities that are only 6 percent funded.

But here’s the real rub: experts are warning that many pension systems, those claiming they are well funded and those who say they aren’t, have all been using rosy projections about future investment returns.

In a recent editorial in Barron’s, Thomas Donlan writes that pension funds have “hidden the results with dubious financial reporting.”

He cites as just one example Detroit, which claimed as late as 2011 that their pension funds were 80 percent fully funded. New auditors found a $3.5 billion shortfall, a hole that pushed the city into bankruptcy.

Detroit, he says, was using the standard 8 percent return on assets, widely used by other funds. Donlan argues that is foolhardy to claim an 8 percent rate of return.

Consider that since January 1, 2001, the Dow Jones has appreciated, on average, a paltry 2.2 percent, with the S&P growing just 1.36 percent.

Instead, Donlan suggests pension funds use a 4 percent rate, the blended rate for no-risk Treasuries or a 5.5 percent rate, consistent with current corporate bond payouts. But if pension funds were to be honest and use such numbers, real unfunded liabilities would jump by a third or more.

| City | Total Liability | % Funded |

| Charleston, W. Va. | $270 million | 24 |

| Omaha, Neb. | $1.43 billion | 43 |

| Portland, Ore. | $5.46 billion | 50 |

| Chicago, Ill. | 24.97 billion | 52 |

| Little Rock, Ark. | $498 million | 59 |

| Wilmington, Del. | $364 million | 59 |

| Boston, Mass. | $2.54 billion | 60 |

| Atlanta, Ga. | $3.17 billion | 60 |

| Manchester, N.H. | $436 million | 60 |

| New Orleans, La. | $1.99 billion | 61 |

The Pew Charitable Trusts study further identified nine cities that underperformed on two pension indicators, levels of funding along with the annual contribution percentage: Charleston; Chicago; Fargo, N.D.; Jackson, Miss.; Little Rock; New Orleans; Omaha; Philadelphia, and Portland.

Equally startling, Pew found numerous cities were woefully unprepared to finance healthcare benefit obligations.

"Only Los Angeles, Calif., and Denver, Colo., had even half of the money needed to fulfill their promises to employees. Thirty-three cities had set aside nothing to pay for this bill coming due," the research noted. Cincinnati was not among the cities ranked.

Many localities are seeing their operating budgets squeezed to pay for pension and healthcare retirement benefits.

The country's 250 largest cities saw spending for pensions increase to 10 percent of their general budgets in 2012, an increase of 7.75 percent since 2007, according to The Wall Street Journal.

The situation is no better for the states, which are also facing high burdens associated with worker's retirement costs.

The Chicago Sun-Times reported that an analysis of pension reform scenarios under consideration by the Illinois legislature "make clear that no matter what legislators do, including major pension cutting, a significant portion of the state's budget for the next 20 to 25 years will go toward paying pension bills, consuming 16 to 24 percent of the state’s general revenue fund annually."

Reform: No Easy Solutions

Steven Stanek of the Heartland Institute says there are no easy solutions when you get into situations that are as bad as states like Illinois, which has saved just 43 cents to cover every dollar of what it needs to pay 350,000 retirees and 500,000 current workers who are counting on pension checks.

"Enacting reform is made even harder because all policy is politics ultimately," Stanek tells Newsmax.

Stanek said that while rankings may differ depending on who is doing the number crunching and which data they survey, some states are present on all rankings.

"I would say from what I have seen the worst are Illinois, California, West Virginia, Oklahoma, New Hampshire, Louisiana, Alaska, Connecticut — all make the list," said Stanek.

A September report by the think tank State Budget Solutions said that state public employee retirement promises are underfunded by $4.1 trillion nationally. In addition, the report concluded that when combined, state public pension plans are just 39 percent funded.

The study found the five most poorly funded states are Illinois (24%), Connecticut (25%), Kentucky (27%), and Kansas (29%), along with Mississippi, New Hampshire, and Alaska tied at 30% funded.

State Budget Solution's Cory Eucalitto said in the report that for years the methodology used to rate public pension systems in the states has been too generous, allowing states to spin a rosier picture than reality truly reflected.

The generosity of the standards resulted in decisions this year by the Governmental Accounting Standards Board and by Moody's Investors Services to change the way they calculate state burdens.

"GASB and Moody's have joined a chorus of financial economists and other observers warning that pension funding practices are dangerous for both taxpayers and public employees alike," he writes.

Pension reform not only is causing a strain on local governments, but also on long-held political alliances.

California: The Future Has Arrived

Reform efforts advocated by Democratic mayors in Chicago and Detroit have both been vocally opposed by teacher and labor unions. The fissures have also arisen in San Francisco, where pension reform was one of several issues which resulted in Bay Area Transit Authority (BART) workers striking.

San Jose Mayor Chuck Reed announced in early October he would support a ballot measure for November 2014 that would amend California's Constitution to allow local governments to reduce pension expenses associated with their current employees. The proposal would not affect retiree benefits, but could allow modifications to future beneficiary plans.

With other cities in the state laboring under the weighty costs of pension obligations and retiree benefits, San Bernardino Mayor Pat Morris and Santa Ana Mayor Miguel Pulido joined Reed in submitting the ballot initiative to the state Attorney General.

"Typically, reform is being led by Democratic mayors. It's being resisted by leaders of public employee unions, who are also Democrats. California state legislators tend to side with the unions over the mayors, preferring the status quo — and the campaign contributions from unions — to an intramural fight," says Carl Cannon of RealClearPolitics.

Richard Dreyfuss, senior fellow at the Manhattan Institute, suggests several reforms are needed to avoid going off the fiscal cliff, including prohibiting issuing new bonds to refinance existing liabilities.

Dreyfuss also advocates for comprehensive reform that will combine a transition to defined-contribution plans, such as a 401(k), with reforms to how pensions are funded. He believes the new pension plans should be funded as they are earned, to avoid burdening future employees and beneficiaries.

Dreyfuss is clear in stating that any reform is going to be politically unpalatable.

"The necessity for real reform is problematic for policymakers, who must deal with a workforce resistant to the loss of guaranteed monthly pension benefits; and for political constituencies, including government workers and their allies, whose support for defined-benefit pensions in the public sector stems as much from ideology as from financial self-interest," he wrote.

Related Stories:

© 2013 Newsmax. All rights reserved.

Europe's Scariest Chart Leaves 1 in 4 Young People Unemployed

While near record low sovereign bond spreads and

near record high equity prices have been taken as vindication by the

European elites that all is well and 'we just need a little less fauxsterity' to be done with this crisis; the data, as it so often does, says the exact opposite. European unemployment just broke above 12% for the first time ever and European youth unemployment remains miserably above 24%. And while 1-in-4 under-25s unemployed is a bad enough statistic in terms of likely emergence of social unrest,

the individual countries are in general deteriorating once again at a

faster rate. French youth unemployment has risen for 13 months in a row

to a record 26.5%; Spain (at 57.2% of under-25s unemployed) is catching

up fast to Greece's stunning 59.1%; but perhaps the most concerning for

the broader economies is the fact that Italy's youth unemployment has now topped that of Portugal at 38.4%.

The only nation to see a drop in its youth unemployment was Ireland -

which fell back modestly to January levels. Not a rosy picture, but then

again, it doesn't matter...

Ugly...

and even worse for the youth...

but does it matter?

Charts: Bloomberg

Ugly...

and even worse for the youth...

but does it matter?

Charts: Bloomberg

Subscribe to:

Posts (Atom)