Monday, February 25, 2013

Michael Crichton: 'Al Gore Is Wrong About Global Warming'

'Al Gore has never looked at the data.'

The late Michael Crichton with Charlie Rose. Aired Aug. 27, 2007.

Outstanding Michael Crichton interview from a few years ago. It's a 5-star appearance. Crichton graduated Harvard Medical School, was a published scientist, and was a fellow at the Jonas Salk Institute before becoming a Hollywood writer/producer, so it's not really a fair fight.

UPDATE - Check Out This Climate Change Timeline 1895-2010

---

More from the same interview:

'Telling the truth about climate hysteria has made me a pariah.'

REPORT: Another Secret Bailout For Bank Of America

The NY Fed secretly bailed out Bank of America

last Summer, and it's just coming to light now.

last Summer, and it's just coming to light now.---

Don't Blink, Or You'll Miss Another Bailout

New York Times

By Gretchen Morgenson

Many people became rightfully upset about bailouts given to big banks during the mortgage crisis. But it turns out that they are still going on, if more quietly, through the back door.

The existence of one such secret deal, struck in July between the Federal Reserve Bank of New York and Bank of America, came to light just last week in court filings.

That the New York Fed would shower favors on a big financial institution may not surprise. It has long shielded large banks from assertive regulation and increased capital requirements.

Still, last week’s details of the undisclosed settlement between the New York Fed and Bank of America are remarkable. Not only do the filings show the New York Fed helping to thwart another institution’s fraud case against the bank, they also reveal that the New York Fed agreed to give away what may be billions of dollars in potential legal claims.

Here’s the skinny: Late last Wednesday, the New York Fed said in a court filing that in July it had released Bank of America from all legal claims arising from losses in some mortgage-backed securities the Fed received when the government bailed out the American International Group in 2008. One surprise in the filing, which was part of a case brought by A.I.G., was that the New York Fed let Bank of America off the hook even as A.I.G. was seeking to recover $7 billion in losses on those very mortgage securities.

Let’s recap: For zero compensation, the New York Fed released Bank of America from what may be sizable legal claims, knowing that A.I.G. was trying to recover on those claims.

It gets better.

What did the New York Fed get from Bank of America in this settlement?

Continue reading at the New York Times...

---

This wasn't the first time:

Bank Of America's Backdoor Bailout - Dumping Mortgage Trash Onto Taxpayers Via Fannie Mae

Photos by William Banzai7...

Looming Economic Crisis: 75% of Americans Cutting Back On Spending, Steep Spending Cuts Coming, Unfunded Federal Pension Liabilities Head Skyward, Fed Risks Losing Control Amid Budget Deficits

75% of Americans cutting back on spending, thanks to payroll tax hike

SPRINGFIELD, Mass. (WWLP) – The payroll tax hike that took effect as a result of the fiscal cliff is taking a toll on many Americans’ household budgets.That change in federal tax law means people are taking home smaller paychecks, and that’s forcing nearly 75% of Americans to cut back on spending, according to theNational Retail Federation .

FEDERAL SPENDING UP $822.90 PER PERSON SINCE OBAMA

Seib & Wessel: Sequester Cuts Likely to Kick In

The sequester: steep spending cuts comingWSJ’s Damian Paletta says the sequester cuts – including painful slashing of defense spending – now seem inevitable. The question now is how long they’ll last. WSJ’s David Wessel explains the hit to federal employees and when furloughs could kick in….

Economists Warn Fed Risks Losing Control Amid Budget Deficits

Four economists, including a former Federal Reserve governor who has co-written research with Chairman Ben S. Bernanke, warned that losses from the central bank’s more than $3 trillion balance sheet could lead to the Fed losing control of monetary policy.“The combination of a massively expanded central bank balance sheet and an unsustainable public debt trajectory is a mix that has the potential to substantially reduce the flexibility of monetary policy,” the economists write. “This mix could induce a bias toward slower exit or easier policy, and be seen as the first step toward fiscal dominance. It could thereby be the cause of longer-term inflation expectations and raise the risk of inflation overall.”

The conclusion from economists, including Frederic Mishkin, a governor at the central bank from 2006 to 2008 and an academic collaborator with Bernanke before that, will be presented at the U.S. Monetary Policy Forum in New York. Their paper serves as a high-profile warning to an audience including Boston Fed President Eric Rosengren, Fed Governor Jerome Powell and St. Louis Fed President James Bullard.

When The Fed Has To Print Money Just To Print Money

‘The second the Fed enters open deleveraging mode, everyone will sell everything they can to lock in the profits generated from the past 4+ years of Fed balance sheet expansion.Furthermore, at that moment, the market will begin pricing in the unwind of some or all of the $15 trillion in central bank liquidity which is the only reason the S&P is where it is today.

The result would be a market crash so epic it would make the market response to Lehman and AIG’s failure seem like a walk in the park by comparison.‘

Unfunded Federal Pension Liabilities Head Skyward

The unfunded liability of federal pensions have skyrocketed to more than $750 billion in the most recent accounting year available, according to an annual government report obtained by the Federal Times.The unfunded liability hit $761.5 billion in fiscal 2011 — an increase of $139 billion from the year before, The Times reported.

The Times extracted the information from the Office of Personnel Management (OPM)’s Civil Service Retirement and Disability Fund annual report for 2012, which it received upon request to the OPM.

Fed unlikely to curtail stimulus despite rising doubts

Fed Officials Reject Warning Losses May Weaken FOMC Clout

E-Mails Imply JPMorgan Knew Some Mortgage Deals Were Bad

J. Scott Applewhite/Associated PressJamie Dimon, JPMorgan’s chief. The bank is being sued over mortgage-backed deals.

When an outside analysis uncovered serious flaws with thousands of home loans, JPMorgan Chase executives found an easy fix.

Rather than disclosing the full extent of problems like fraudulent home appraisals and overextended borrowers, the bank adjusted the critical reviews, according to documents filed early Tuesday in federal court in Manhattan. As a result, the mortgages, which JPMorgan bundled into complex securities, appeared healthier, making the deals more appealing to investors.

The trove of internal e-mails and employee interviews, filed as part of a lawsuit by one of the investors in the securities, offers a fresh glimpse into Wall Street’s mortgage machine, which churned out billions of dollars of securities that later imploded. The documents reveal that JPMorgan, as well as two firms the bank acquired during the credit crisis, Washington Mutual and Bear Stearns, flouted quality controls and ignored problems, sometimes hiding them entirely, in a quest for profit.

The lawsuit, which was filed by Dexia, a Belgian-French bank, is being closely watched on Wall Street. After suffering significant losses, Dexia sued JPMorgan and its affiliates in 2012, claiming it had been duped into buying $1.6 billion of troubled mortgage-backed securities. The latest documents could provide a window into a $200 billion case that looms over the entire industry. In that lawsuit, the Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, has accused 17 banks of selling dubious mortgage securities to the two housing giants. At least 20 of the securities are also highlighted in the Dexia case, according to an analysis of court records.

In court filings, JPMorgan has strongly denied wrongdoing and is contesting both cases in federal court. The bank declined to comment.

Dexia’s lawsuit is part of a broad assault on Wall Street for its role in the 2008 financial crisis, as prosecutors, regulators and private investors take aim at mortgage-related securities. New York’s attorney general, Eric T. Schneiderman, sued JPMorgan last year over investments created by Bear Stearns between 2005 and 2007.

Jamie Dimon, JPMorgan’s chief executive, has criticized prosecutors for attacking JPMorgan because of what Bear Stearns did. Speaking at the Council on Foreign Relations in October, Mr. Dimon said the bank did the federal government “a favor” by rescuing the flailing firm in 2008.

The legal onslaught has been costly. In November, JPMorgan, the nation’s largest bank, agreed to pay $296.9 million to settle claims by the Securities and Exchange Commission that Bear Stearns had misled mortgage investors by hiding some delinquent loans. JPMorgan did not admit or deny wrongdoing.

“The true price tag for the ongoing costs of the litigation is terrifying,” said Christopher Whalen, managing director at Carrington Investment Services.

The Dexia lawsuit centers on complex securities created by JPMorgan, Bear Stearns and Washington Mutual during the housing boom. As profits soared, the Wall Street firms scrambled to pump out more investments, even as questions emerged about their quality.

With a seemingly insatiable appetite, JPMorgan scooped up mortgages from lenders with troubled records, according to the court documents. In an internal “due diligence scorecard,” JPMorgan ranked large mortgage originators, assigning Washington Mutual and American Home Mortgage the lowest grade of “poor” for their documentation, the court filings show.

The loans were quickly sold to investors. Describing the investment assembly line, an executive at Bear Stearns told employees “we are a moving company not a storage company,” according to the court documents.

As they raced to produce mortgage-backed securities, Washington Mutual and Bear Stearns also scaled back their quality controls, the documents indicate.

In an initiative called Project Scarlett, Washington Mutual slashed its due diligence staff by 25 percent as part of an effort to bolster profit. Such steps “tore the heart out” of quality controls, according to a November 2007 e-mail from a Washington Mutual executive. Executives who pushed back endured “harassment” when they tried to “keep our discipline and controls in place,” the e-mail said.

Even when flaws were flagged, JPMorgan and the other firms sometimes overlooked the warnings.

JPMorgan routinely hired Clayton Holdings and other third-party firms to examine home loans before they were packed into investments. Combing through the mortgages, the firms searched for problems like borrowers who had vastly overstated their incomes or appraisals that inflated property values.

According to the court documents, an analysis for JPMorgan in September 2006 found that “nearly half of the sample pool” — or 214 loans — were “defective,” meaning they did not meet the underwriting standards. The borrowers’ incomes, the firms found, were dangerously low relative to the size of their mortgages. Another troubling report in 2006 discovered that thousands of borrowers had already fallen behind on their payments.

But JPMorgan at times dismissed the critical assessments or altered them, the documents show. Certain JPMorgan employees, including the bankers who assembled the mortgages and the due diligence managers, had the power to ignore or veto bad reviews.

In some instances, JPMorgan executives reduced the number of loans considered delinquent, the documents show. In others, the executives altered the assessments so that a smaller number of loans were considered “defective.”

In a 2007 e-mail, titled “Banking overrides,” a JPMorgan due diligence manager asks a banker: “How do you want to handle these loans?” At times, they whitewashed the findings, the documents indicate. In 2006, for example, a review of mortgages found that at least 1,154 loans were more than 30 days delinquent. The offering documents sent to investors showed only 25 loans as delinquent.

A person familiar with the bank’s portfolios said JPMorgan had reviewed the loans separately and determined that the number of delinquent loans was far less than the outside analysis had found.

At Bear Stearns and Washington Mutual, employees also had the power to sanitize bad assessments. Employees at Bear Stearns were told that they were responsible for “purging all of the older reports” that showed flaws, “leaving only the final reports,” according to the court documents.

Such actions were designed to bolster profit. In a deposition, a Washington Mutual employee said revealing loan defects would undermine the lucrative business, and that the bank would suffer “a couple-point hit in price.”

Ratings agencies also did not necessarily get a complete picture of the investments, according to the court filings. An assessment of the loans in one security revealed that 24 percent of the sample was “materially defective,” the filings show. After exercising override power, a JPMorgan employee sent a report in May 2006 to a ratings agency that showed only 5.3 percent of the mortgages were defective.

Such investments eventually collapsed, spreading losses across the financial system.

Dexia, which has been bailed out twice since the financial crisis, lost $774 million on mortgage-backed securities, according to court records.

Mr. Schneiderman, the New York attorney general, said that overall losses from flawed mortgage-backed securities from 2005 and 2007 were $22.5 billion.

In a statement shortly after he sued JPMorgan Chase, Mr. Schneiderman said the lawsuit was a template “for future actions against issuers of residential mortgage-backed securities that defrauded investors and cost millions of Americans their homes.”

This post has been revised to reflect the following correction:

Correction: February 8, 2013

An article on Thursday about court documents indicating that JPMorgan Chase was aware of flawed loans in the mortgage-backed securities it was selling to clients included outdated information on the business affiliation of Christopher Whalen, who commented on the cost of continuing litigation in the case. He is managing director at Carrington Investment Services; he is no longer with Tangent Capital Partners.

A version of this article appeared in print on 02/07/2013, on page B1 of the NewYork edition with the headline: E-Mails Imply JPMorgan Knew Some Mortgage Deals Were Bad.

To Surge Against Pound, Europ, Yen And It Is Going To Hurt Corporate Profits. Andy Xie: A Strengthening Dollar Could Trigger New Financial Crisis

It Looks Like The Dollar Is About To Surge

Good perspective here from SocGen’s currency analyst Sebastien Galy. Between the Italian election uncertainty and the UK downgrade, it’s safe to expect another dollar pop:The combination of a UK downgrade and a uncertain Italian elections are the fuel for a run of stop losses on long GBPUSD and EURUSD at the opening of the markets in Asia. CFTC positioning had already shown another large scale profit taking on USD shorts and we are likely in the process of neutralizing these positions in favour of JPY shorts (see report for those that asked to be on the cftc mailing list). It is the stuff of a strange golden age of fx, under invested, over achieving for no great reason, a telltale of a greater instability in the global economy

.A confluence of uncertainty helps the greenback.

The Pound And The Yen Both Instantly Tank To Start The Week

The two most-hated currencies in the world.

U.K. credit downgrade will weigh on pound

SAN FRANCISCO (MarketWatch) — The British pound will face

continued pressure in the coming weeks as confidence erodes in the

United Kingdom’s recovery efforts following the loss of the country’s

triple-A rating, according to analysts.

The British pound GBPUSD -0.5980%

fell sharply to below $1.517 from around $1.525 late Friday following

Moody’s U.K. ratings downgrade to Aa1 from Aaa. The pound had surged

briefly past the $1.53 mark before the announcement on Friday from

$1.515 on Thursday after touching an intraday high of $1.55 on Tuesday.

Yen Plunges As Uber-Dove Kuroda Set To Head Bank Of Japan

In our prediction two weeks ago of who the next Bank of Japan governor was likely to be, we said that “the tussle lies between a slightly less dovish bureaucrat in Toshiro Muto (favored by the opposition) and a banker, Haruhiko Kuroda, who is a front-runner in Abe’s camp…. we suspect Abe will err on the side of uber-dovish to fight the currency wars alongside him.” Sure enough, the uber-dove Kuroda, not to be confused with the Yankees pitcher, is now set to become BOJ governor.From Reuters, “Japan’s government is likely to nominate Asian Development Bank President Haruhiko Kuroda, who has called for pumping more money into the economy, as its next central bank governor, the Nikkei newspaper reported on Monday. Kuroda, formerly Japan’s top currency diplomat, has already been offered the post unofficially by the government, which plans to submit its nominees for three BOJ leadership posts to parliament this week, the paper said. Kikuo Iwata, an academic known as one of the most vocal advocates of aggressive monetary expansion, is likely to be nominated as deputy BOJ governor, the Nikkei said without citing sources.”

The dollar is now corporate America’s worst enemy

Listen in to the earnings calls from multinationals this quarter and you’ll hear a common refrain: Fear the stronger dollar.FORTUNE – If there was a chorus to be sung this earnings season, CEOs would probably reference the mighty greenback in harmony. It’s one of the biggest threats to profits.

A stronger dollar isn’t always bad news for corporate America. But as the growth of earnings decelerates in the second quarter, CEOs from McDonald’s (MCD) to Colgate-Palmolive (CL) say that an appreciating dollar has been bad for business lately. Not only does it make products more expensive, but it also means sales made overseas aren’t worth as much when converted into a stronger greenback.

To be sure, most companies generally prepare for fluctuating exchange rates. They could raise prices, for instance. But the pace at which the dollar has strengthened in the three months ending in June has surprised most executives. During the second quarter, the dollar gained 5% against the euro. As Europe’s ongoing debt crisis took a turn for the worse, investors looking for a safer place to park their cash turned to the U.S. dollar. As of Wednesday morning, it stands at $1.2311 per euro in New York.

Andy Xie: Next Global Crisis Might Be Caused by Strong Dollar

As the U.S. economy recovers, a strengthening dollar might cause the next financial crisis, warns Singapore-based economist Andy Xie.“The first dollar bull market in the 1980s triggered the Latin American debt crisis, the second the Asian Financial Crisis. Neither was a coincidence,” Xie writes for Caixin Online, a website specializing in China’s financial and business news.

When the dollar is in a bear market, liquidity flows into emerging markets, causing their currencies and asset prices to appreciate, which supports domestic demand.

“When the dollar changes direction, so does liquidity,” according to Xie, a former Morgan Stanley economist who predicted the economic bubbles like the 1997 Asian financial crisis and dot-com bubble.

“The virtuous cycle on the way up becomes a vicious one on the way down. The emerging economies already suffer inflation. The liquidity outflow leads to currency depreciation, which worsens inflation.”

SHOCKING: The World Is Running Out Of US Dollars!!

WRIST SLAP: Justice Dept Settles Robo-Signing Fraud Case

Criminal foreclosure costs LPS just $30 per fraud.

---

Reuters

Mortgage servicing company Lender Processing Services agreed to pay $35 million to resolve a federal criminal investigation into foreclosure fraud, the Justice Department said on Friday.

The settlement resolves allegations over the company’s involvement in what the government called a six-year scheme to prepare and file more than 1 million fraudulently signed and notarized mortgage documents in property recorders’ offices nationwide from 2003 to 2009. The practice became known as robo-signing.

Lorraine Brown, the former CEO of DocX LLC, was found guilty, November 20, 2012, for conspiracy to commit mail and wire fraud. Sentencing for Brown is scheduled April 23. She faces a possible sentence of a maximum of five years in prison and a $250,000 fine, or twice the gross gain or loss from the offense.

LPS entered into a two-year non-prosecution agreement that requires it to meet many conditions, including cooperating in federal probes, and alert the government to any abuses in mortgage or foreclosure documentation services at the company.

The $35 million payment includes criminal penalties and forfeiture and must be made within 10 days to the U.S. Marshals Service and the U.S. Treasury, the Justice Department said. The company said on Friday that it has a $223 million reserve that covers the Justice Department accord and prior settlements.

Continue reading...

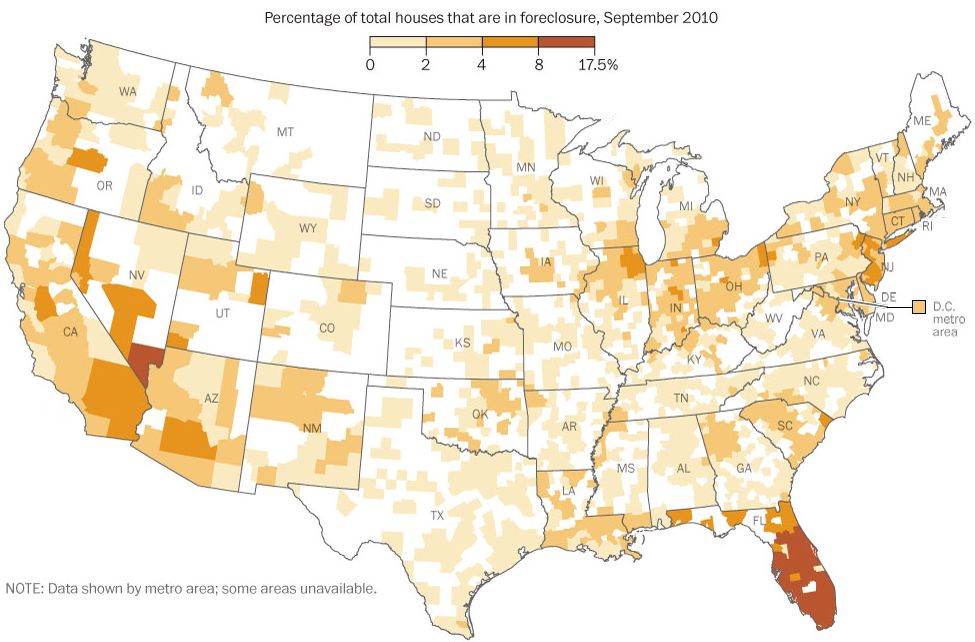

U.S. Foreclosure Map

Photos by William Banzai7...

127 corporations that want to “Fix the Debt” by gutting your retirement

Charleston Voice

Charleston VoiceWe’re grateful for author Gaius bringing mention of this to the fore. However, the major component is absent – the adhesive, the Super-Glu binding these frauds together under a cloak of “public service” is Peter G. Peterson, one of the grand masters of the Conspiracy: Chairman of the Council on Foreign Relations. We do not could him among America’s greatest allies or patriots. Certainly no friend of individual liberty!

Through this special report — and in partnership with The Nation magazine — the Center for Media and Democracy exposes the funding, the leaders, the partner groups, and phony state “chapters” of this $60 million “astroturf supergroup,” whose goal is to achieve a grand bargain on austerity by July 4, 2013.[1]

Through this special report — and in partnership with The Nation magazine — the Center for Media and Democracy exposes the funding, the leaders, the partner groups, and phony state “chapters” of this $60 million “astroturf supergroup,” whose goal is to achieve a grand bargain on austerity by July 4, 2013.[1]We urge you to see the beneficial interlocks that “Fix the Debt” has set up for their corporatist allies colluding with government at your expense. GO HERE

————————————

127 corporations that want to “Fix the Debt” by gutting your retirement

2/23/2013 10:00am by Gaius PubliusThe CEOs of the following corporations don’t think they have enough money — perhaps because they don’t have it all. So they got together a little group called “Fix the Debt” to cobble up some more. The source of their added wealth? Your government retirement and medical insurance programs. You know, Social Security and Medicare. ‘Cause all your money aren’t yet belong to them; you still have some left.

I wrote about Fix the Debt earlier, the truly bipartisan group that wants Obama to do what he also wants to do, reduce the safety net. The following is a list of corporations who are driven by their millionaire and billionaire CEOs to help him get ‘er done.

The source is the amazing group SourceWatch. Also amazing — the list itself. Take a gander:

http://chasvoice.blogspot.com/2013/02/127-corporations-that-want-to-fix-debt.html

If the Masses Lose Confidence in the Currency…

At a recent meeting of the American Economic Association a vote was

held about whether or not the United States should back its currency

with gold. Not surprisingly, 100% of mainstream economists educated by

our most prestigious universities were against such a measure.

From the top down, there is a cult-like belief that our paper monetary system is absolute and infallible.

Yet, as we have seen throughout history, and especially in the last decade, currencies backed by nothing are always debased, eventually being worth even less than the paper they’re printed on.

If you’re one of those contrarians who happens to believe, like investment guru Jay Taylor, that market manipulation is rampant and the only reason why our ‘best and brightest’ continue to promote the legitimacy of paper currencies is to maintain a perception of stability in a crumbling monetary system, then the following interview from the Sound Money Campaign is a must watch.

Taylor discusses his thoughts on the importance of hard assets, the meaning of real value, investment strategies, and international diversification to avoid a government whose aim is to punish those who will survive and thrive when things turn sour.

Moreover, Taylor delves into the real reason for why the Federal Reserve

and leading mainstream economists continue to push policies that led to

the financial meltdown of 2008 and why those policies will eventually

lead to something much, much worse :

From the top down, there is a cult-like belief that our paper monetary system is absolute and infallible.

Yet, as we have seen throughout history, and especially in the last decade, currencies backed by nothing are always debased, eventually being worth even less than the paper they’re printed on.

If you’re one of those contrarians who happens to believe, like investment guru Jay Taylor, that market manipulation is rampant and the only reason why our ‘best and brightest’ continue to promote the legitimacy of paper currencies is to maintain a perception of stability in a crumbling monetary system, then the following interview from the Sound Money Campaign is a must watch.

Taylor discusses his thoughts on the importance of hard assets, the meaning of real value, investment strategies, and international diversification to avoid a government whose aim is to punish those who will survive and thrive when things turn sour.

Moreover, Taylor delves into the real reason for why the Federal Reserve

and leading mainstream economists continue to push policies that led to

the financial meltdown of 2008 and why those policies will eventually

lead to something much, much worse :I think more than that is the talk that comes out of the Fed and the establishment… I think that, in part, is to keep people believing in the integrity of a system that doesn’t have much else going for it other than talk.

Because the debasing of currency is relentless.

The Federal Reserve is expanding its balance sheets, it’s creating money out of nothing, it’s devaluing the savings of individuals through the debasement of the currency and through zero interest policies.

They’re just trying to keep people off balance so they don’t bet in one direction in favor of inflation hedges.

They want to keep people believing [inflation] is not going to be a problem. they need to do that in order to keep people believing in the dollar, which they create out of nothing.

So, it’s a giant con game.

In the end, Pinocchio’s nose will be exposed and [free] markets win out.

The Banks Show No Mercy: 10 Foreclosure Horror Stories That Will Blow Your Mind

by Michael

During the last housing crash, the big banks begged the federal government

for help and they received it, but when average Americans ask the big

banks for help most of the time the banks show no mercy whatsoever. If

you fall behind on your mortgage payments, the big banks have shown that

they are willing to be absolutely ruthless. They will change locks in

the middle of the night, they will toss disabled veterans and families

with children out into the street in the middle of winter, and sometimes

once the foreclosure process has begun they will not even allow someone

to come forward and offer to pay off the loan if they think that they

can make more money by selling the home. The big banks will often

string homeowners along for months or even years with loan modification

promises, only to drop the hammer on them at the most inopportune time.

Over the past several years there has been case after case where

mortgage documents have “disappeared”, where big banks have

“manufactured” missing documents out of thin air and there have even

been cases where big banks have tried to foreclose on homes that do not

even have a mortgage. Once in a while, the big banks get a small slap

on the wrist, but nobody ever really gets into much trouble for any of

this. In fact, the big banks just continue to gain even more market

share and even more power. Hopefully when some of these foreclosure

horror stories start to become publicized more widely we will start to

see some real changes in the marketplace.

The following are 10 foreclosure horror stories that will blow your mind…

#1 If you get behind on your mortgage, your family might be tossed into the street at gunpoint in the middle of the night…

. The following is from a recent Bloomberg article…

So what do you think about all of this?

Do you have a foreclosure horror story to share?

Please feel free to post a comment with your thoughts below…

During the last housing crash, the big banks begged the federal government

for help and they received it, but when average Americans ask the big

banks for help most of the time the banks show no mercy whatsoever. If

you fall behind on your mortgage payments, the big banks have shown that

they are willing to be absolutely ruthless. They will change locks in

the middle of the night, they will toss disabled veterans and families

with children out into the street in the middle of winter, and sometimes

once the foreclosure process has begun they will not even allow someone

to come forward and offer to pay off the loan if they think that they

can make more money by selling the home. The big banks will often

string homeowners along for months or even years with loan modification

promises, only to drop the hammer on them at the most inopportune time.

Over the past several years there has been case after case where

mortgage documents have “disappeared”, where big banks have

“manufactured” missing documents out of thin air and there have even

been cases where big banks have tried to foreclose on homes that do not

even have a mortgage. Once in a while, the big banks get a small slap

on the wrist, but nobody ever really gets into much trouble for any of

this. In fact, the big banks just continue to gain even more market

share and even more power. Hopefully when some of these foreclosure

horror stories start to become publicized more widely we will start to

see some real changes in the marketplace.The following are 10 foreclosure horror stories that will blow your mind…

#1 If you get behind on your mortgage, your family might be tossed into the street at gunpoint in the middle of the night…

This week, Christine Frazer and her family were thrown out of the Atlanta home they’d lived in for 18 years, at gunpoint in the dead of night.#2 Time after time we have seen authorities show absolutely no mercy when conducting these evictions…

They were not set upon by robbers, but by the Dekalb County Sheriff’s department, which evicted the family at the request of Investors One Corporation. As Steven Rosenfeld reported for AlterNet, it was the fourth company to buy the family’s mortgage in eight months.

It was bad enough when 62-year-old disabled veteran Ramsey Harris was evicted from a foreclosed house on Jamaica Lane where the former owner had been letting him live.#3 Sometimes financial institutions will promise you a loan modification for many months and then turn around and foreclose on you anyway…

Then it started to rain as all his worldly possessions sat in a heap by the side of the road and Harris noticed some of his valuables were missing.

“It was just ugly,” Harris said Friday. “I was just broken-hearted. I couldn’t believe what was happening to me. I ended up standing, watching all my life’s work go down the tubes.”

When the economy crashed and his business slowed down, Wells Fargo offered to modify Steve Bailey’s loan to lower his payments. After making a series of trial payments, Wells Fargo notified Steve that his modification was on the way.#4 Other homeowners have found themselves trapped in loan modification hell for years…

A few days later he received a letter stating that his modification had been denied. The Wells Fargo representative he spoke with reassured him that they had made a mistake and that he should keep making the payments, which he did for seven months.

Steve then started to receive foreclosure notices. Again, the bank representative assured him that the notices had been sent in error.

Then Steve checked his credit. Wells Fargo had reported him delinquent on his mortgage for the last six months. The reduced payments that Steve had agreed to pay for the previous months had been put into a separate trust by Wells Fargo, and they had not gone towards his mortgage.

Steve took the case to court but lost despite mountains of evidence in his favor. He lost his home and his business.

I am self-employed, have been all my life and have owned a home for 30 years. When I started my Loan Modification process in August of 09 I WAS NOT behind on any payments. I sent full documentation, over 150 pages, with the things they needed to verify my income. I am now 2 payments behind and I am getting nowhere. They keep flipping me between Loss Mitigation and Imminent Default, back and fourth month end month out. I made a habit of calling every week, then every two weeks just to be sure all was moving forward. From the middle of November I was told my file was with the underwriter and it would only be 30-60 days. I began automatically updating my income verification, verification that I still resided at the property and an updated 4506-T every month. In the middle of April a rep finally told me I was not in the loan modification process. In fact, that I had been denied on March 2. Keep in mind, I’m talking to these people every 2 weeks. She did a financial interview and sent me a new packet so that I could start all over, resubmitting all the documentation yet again. She told me she was my Account Manager. I completed the packet, called with a question (2 weeks later – over a week to receive the packet and another few days to complete it and gather all my documents again) and learned that my “Account Manager” was on maternity leave and I now didn’t have an account manager. Also, I was told that I had received the incorrect packet…it was the old version rather than the updated version. She asked me to fax four or five pieces of information in the hopes it would, quote, “jump start my file back into the process” and said she we send me another packet. That was mid April. Here we sit, 2-1/2 months later, I have still not received anything in writing about my rejection. And, though I’ve now had people tell me on three separate occasions that I would receive a new packet, it has yet to show up on my door step. I asked several times why my application was denied and the answer I finally got last week was that it was because I was DELIQUENT in my payments. Call me crazy but I thought that was the whole point??!! I almost hired a third party but am so hesitant to take that step. Every time I get on the phone with them it takes an hour out of my day and I am usually so upset I find it difficult to work, so I just don’t call. I’m going to sit back and regroup and decide what I need to do next.#5 Sometimes a big bank will kick someone out of their home and then never actually take possession of the house. As a result, many former homeowners now find themselves stuck with thousands of dollars of unpaid bills. For example, a recent CNN article told the story of Rose Nathan, a 37-year-old office manager…

Nathan lost her South Bend, Ind., home in January 2009, after working out a deal with CitiMortgage to voluntarily walk away in a “deed in lieu of foreclosure.”These unpaid taxes that she didn’t even know about have absolutely destroyed Nathan’s finances…

“On Christmas Eve, the bank called and told me a sheriff’s sale was coming and I had to move out right away,” she said. “So that’s what I did — seven days after New Year’s.”

She sold her belongings and moved to Hawaii. Nearly two years later, she received a property tax bill from the City of South Bend for $5,000. The bank had never taken possession of the house.

Meanwhile, the unpaid debt has crushed Nathan’s credit score. The deed-in-lieu alone lowered her score by 80 to 120 points, but the unpaid debt meant her credit kept taking a hit. Eventually her credit card companies cut her off, even though she said she was making her payments.#6 Sometimes a big bank will decide to foreclose on you even when you have been making all of your payments. Just check out what real estate agent Mark Conca went through with one major bank…

Her auto loan now carries a 25% rate. Her car insurance premiums have skyrocketed. She can only afford a one-bedroom apartment where she lives with her three kids. And forget about buying another home. “Nobody will give me a mortgage,” she said.

He decided to approach his lender, Bank of America, to see if he’d qualify for a modification. After he applied, many months passed and Conca heard nothing from the bank. Knowing lenders had huge backups in modification requests, he remained patient.#7 Sadly, the customer service at many of these large financial institutions is almost non-existent. In fact, sometimes representatives from these companies will literally tell you that they won’t lift a finger to help you…

Conca, 41, continued to make the full payment on the mortgage for his Caldwell home, on time, every month.

But that’s not what Bank of America said when it sent Conca a letter about its intent to foreclose.

“I would have been better going to a loan shark and borrowing all that money,” Conca said. “At least with the street mafia, you know where you stand.”

After a car accident Kathryn Nava wound up on disability and had trouble making her mortgage payments. She had a friend who was willing to help her make her back payments, but that friend wanted to see a payment history before giving her the money. Nava called her mortgage lender to request that history—and was told it would cost her $50 per hour, and take 90 days to receive it.#8 Sometimes the big banks will try to foreclose even when you paid cash for your house and you don’t even have a mortgage…

So she tried again, calling the president of the company. She got a voicemail response that shocked her so much she recorded it and saved it.

“Let me enlighten you, Kathy. First of all, there’s nothing in your contract with us says we owe you any history, now, next year, five years from now or the next time…I’ve begun foreclosure today. I bet you’re sorry now that you made that phone call. I don’t need to put up with your crap, OK?…Bottom line, I’m doing nothing for you now.”

Indeed, she did end up losing her home.

Charlie and Maria Cardoso are among the millions of Americans who have experienced the misery and embarrassment that come with home foreclosure.#9 Dealing with these big banks is so incredibly frustrating that some homeowners have completely snapped. For example, one very frustrated homeowner in Ohio decided to crash his SUV into his own home…

Just one problem: The Massachusetts couple paid for their future retirement home in Spring Hill with cash in 2005, five years before agents for Bank of America seized the house, removed belongings and changed the locks on the doors, according to a lawsuit the couple have filed in federal court.

30-year-old Steve Doak told deputies he was recently served with foreclosure papers and wanted to destroy the house rather than turn it over to the bank. The sheriff’s office says Doak drove the vehicle into fencing and then into the rear of the house#10 Another very frustrated homeowner literally bulldozed his own home…

“The average homeowner that can’t afford an attorney or can fight as long as we have, they don’t stand a chance,” he said.Meanwhile, the big banks that are doing all of this continue to receive billions of dollars in assistance from the federal government

Hoskins said he’d gotten a $170,000 offer from someone to pay off the house, but the bank refused, saying they could get more from selling it in foreclosure.

Hoskins told News 5?s Courtis Fuller that he issued the bank an ultimatum.

“I’ll tear it down before I let you take it,” Hoskins told them.

And that’s exactly what Hoskins did.

. The following is from a recent Bloomberg article…When JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon testifies in the U.S. House today, he will present himself as a champion of free-market capitalism in opposition to an overweening government. His position would be more convincing if his bank weren’t such a beneficiary of corporate welfare.Sadly, when the next wave of the economic crisis strikes, we are probably going to see millions more foreclosures and thousands upon thousands of more stories just like these.

To be precise, JPMorgan receives a government subsidy worth about $14 billion a year, according to research published by the International Monetary Fund and our own analysis of bank balance sheets. The money helps the bank pay big salaries and bonuses. More important, it distorts markets, fueling crises such as the recent subprime-lending disaster and the sovereign-debt debacle that is now threatening to destroy the euro and sink the global economy.

So what do you think about all of this?

Do you have a foreclosure horror story to share?

Please feel free to post a comment with your thoughts below…

Thrones, gold seat buckles and a concert hall: Inside the gloriously opulent private jets of the world's richest including a prince's 'flying palace' and Trump's $100m plane

For most people, flying is a boring

and uncomfortable experience. But in the customized private jets that

belong to the ultrarich the possibilities are endless, and it's

astounding to look at.

These incredible aircraft include cinemas, marble baths, aquariums, Rolls Royce garages, glass floors, concert halls, wellbeing rooms, thrones, chef's kitchens and gold seat buckles.

Each unique jet can be personally designed down to the tiniest luxurious detail for work or play.

Photographer Nick Gleis specializes in picturing such planes. But many of the owners wish to remain anonymous, so around 90 percent of Gleis’s work is never seen by the public.

Well-known names who feature in the photos below include Jackie Chan, Saudi Prince Al-Waleed bin Talal and Donald Trump.

Chan's plush jet has his name and intertwining dragons emblazoned on the side. Al-Waleed's has several planes and his 'flying palace' includes a concert hall complete with a grand piano. And Donald Trump's chosen transport has 18 IMAX-level speakers in the cinema room.

These incredible aircraft include cinemas, marble baths, aquariums, Rolls Royce garages, glass floors, concert halls, wellbeing rooms, thrones, chef's kitchens and gold seat buckles.

Each unique jet can be personally designed down to the tiniest luxurious detail for work or play.

Photographer Nick Gleis specializes in picturing such planes. But many of the owners wish to remain anonymous, so around 90 percent of Gleis’s work is never seen by the public.

Well-known names who feature in the photos below include Jackie Chan, Saudi Prince Al-Waleed bin Talal and Donald Trump.

Chan's plush jet has his name and intertwining dragons emblazoned on the side. Al-Waleed's has several planes and his 'flying palace' includes a concert hall complete with a grand piano. And Donald Trump's chosen transport has 18 IMAX-level speakers in the cinema room.

Plush: The dining facilities on board Saudi

Prince Al-Waleed bin Talal's private Boeing 747. The prince owns several

planes, one of which includes a concert hall complete with a grand

piano

Gold: A comfortable throne sits in the middle of Prince Al-Waleed's Boeing 747

Collection: The prince has several planes including the smaller A Hawker jet, left, and the Boeing 747.

Tranquil: The interior of Jackie Chan's Embraer

SA Legacy 650 jet is designed to be relaxing. The plane transports up to

14 people

Thumbs up: Jackie Chan's plane is emblazoned with his name and personal logo

Anonymous: The owners of most private jets like to keep their luxurious travel arrangements out of the public eye

Detail: Every part of a private plane can be customized to the final detail, like this exquisite sink

Gleaming: The detail on these doors resemble a luxury home rather than a means of transportation

Snacktime: This kitchen could produce a gourmet meal to wile away the hours on a long flight

Luxury: The curving lines of this jet disguise the fact you are inside an aircraft

Freshen up? Even large bathrooms are elegantly designed to make a big impression

Looking after the staff: On this jet, even the pilots travel in sheepskin luxury

Bespoke: Donald Trump bought his private jet

from Microsoft executive Paul Allen for $100 million in 2010 and then he

customized it. It includes a cinema room and little extras like gold

faucets and seat buckles

Emblazoned: There's no mistaking that this plane belongs to Donald Trump from the outside

Multi-purpose: Each plane can be configured for work, play or both

Dine in style: Panels and screens section off different areas of the impressive jets

On the agenda: Why waste time in the air when you can have a boardroom meeting?

Traveling in style: These private jets provide huge levels of comfort

Futuristic: In this plane the mirrored ceiling creates the illusion of a bigger space

Gas Prices Set to Spike in the United States reports Baltimore News Journal

San Francisco, CA — Gas prices are set to take one of the largest jumps in decades. At a rate expected to be $4 a gallon, the average drive is likely considering just how important many of the possibly weekly trips to stores and banks are necessary.

2013 is likely on track to being one of the most expensive years for someone to fill up their automobile. Prices in Maryland are up 16 cents overall within the past month. According to AAA, the 17 cents that the price has risen on average is just the start.

“The way prices have been increasing over the past few weeks we wouldn’t be surprised to see prices approach near $4 a gallon here in Maryland,” said Christine Delise, AAA.

Drivers certainly are not happy about it, and many can recall a time when prices were considerably cheaper. “I remember when I went to college it was 95 cents a gallon,” a man said.

United States oil production is at its highest point in years, but experts note that there are simply not enough producing refineries. That, mixed with growing demand for oil from China make up the bulk of factors which cause the prices to rise at home.

“The price spike we’re seeing at the pump is a result of crude prices that are trading around the $95-to-$97 barrel range. That’s about 10% a barrel more than mid-December,” Delise said.

Many people admit that the recent rise, and consideration of future rises is a wakeup call. “The more expensive gas is the more interested people are in finding a way to not use as much,” a man said.

The average American household is likely to spend nearly $3,000 on gasoline this year. That is considered nearly 4% of their income.

http://emailwire.com/release/114817-Gas-Prices-Set-to-Spike-in-the-United-States-reports-Baltimore-News-Journal.html

Global Finance Crisis – The Crisis of Credit Visualized

This short animation might help you to understand one of the core problems of modern capitalism.

The term financial crisis is applied broadly to a variety of situations in which some financial institutions or assets suddenly lose a large part of their value. In the 19th and early 20th centuries, many financial crises were associated with banking panics, and many recessions coincided with these panics. Other situations that are often called financial crises include stock market crashes and the bursting of other financial bubbles, currency crises, and sovereign defaults. Financial crises directly result in a loss of paper wealth; they do not directly result in changes in the real economy unless a recession or depression follows.

The term financial crisis is applied broadly to a variety of situations in which some financial institutions or assets suddenly lose a large part of their value. In the 19th and early 20th centuries, many financial crises were associated with banking panics, and many recessions coincided with these panics. Other situations that are often called financial crises include stock market crashes and the bursting of other financial bubbles, currency crises, and sovereign defaults. Financial crises directly result in a loss of paper wealth; they do not directly result in changes in the real economy unless a recession or depression follows.

VIDEO: Topless Women Protest As Berlusconi Casts Ballot

Safe to watch. Femen makes its point.

(Reuters) - A group of topless women were dragged away by police on Sunday when they protested against former Prime Minister Silvio Berlusconi as he voted in Italy's election. The protesters, from the Ukrainian women's rights group Femen, shouted "Basta (Enough) Berlusconi", as the media tycoon was voting in a polling station in a Milan school.

The same words were painted on their bodies.

The 76-year-old billionaire, who was pushed out of power in November 2011 as Italy faced a grave financial crisis

,

enrages feminists who accuse him of exploiting scantily-clad showgirls

on his television shows and degrading women with off-colour jokes.---

Another angle:

Italian broadcast.

---

Don't skip this:

Exactly at 10 seconds.

Italian Prime Minister in 2010 - Silvio Berlusconi shows his love for Italy.

Subscribe to:

Posts (Atom)