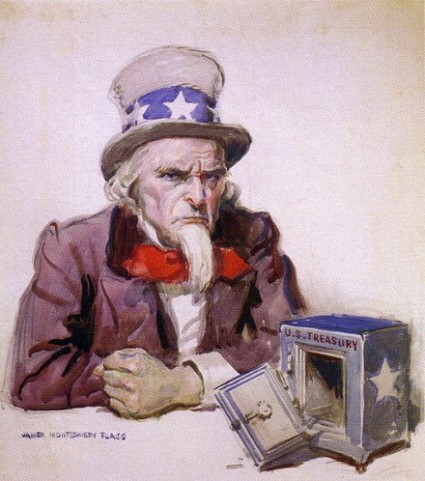

The Senate has severely scaled back the Stock Act, the law to stop members of Congress and their staff from trading on insider information, in an under-the-radar vote that has been sharply criticised by advocates of political transparency.Here is the FT article, here are other sources. Some officials suggested that transparency “could threaten national security,” more detail on that here. Here are some further interesting details.

The changes, if they become law, will exclude Congressional and White House staff members from having to post details of their shareholdings online. They will also make online filing optional for the president, vice-president, members of Congress and congressional candidates.

The House was expected to pass a similar bill on Friday.

Monday, April 15, 2013

The culture that is Washington

Solar panels could destroy U.S. utilities, according to U.S. utilities

That is not wild-eyed hippie talk. It is the assessment of the utilities themselves.

Back in January, the Edison Electric Institute — the (typically stodgy and backward-looking) trade group of U.S. investor-owned utilities — released a report [PDF] that, as far as I can tell, went almost entirely without notice in the press. That’s a shame. It is one of the most prescient and brutally frank things I’ve ever read about the power sector. It is a rare thing to hear an industry tell the tale of its own incipient obsolescence.

I’ve been thinking about how to convey to you, normal people with healthy social lives and no time to ponder the byzantine nature of the power industry, just what a big deal the coming changes are. They are nothing short of revolutionary … but rather difficult to explain without jargon.

So, just a bit of background. You probably know that electricity is provided by utilities. Some utilities both generate electricity at power plants and provide it to customers over power lines. They are “regulated monopolies,” which means they have sole responsibility for providing power in their service areas. Some utilities have gone through deregulation; in that case, power generation is split off into its own business, while the utility’s job is to purchase power on competitive markets and provide it to customers over the grid it manages.

This complexity makes it difficult to generalize about utilities … or to discuss them without putting people to sleep. But the main thing to know is that the utility business model relies on selling power. That’s how they make their money. Here’s how it works: A utility makes a case to a public utility commission (PUC), saying “we will need to satisfy this level of demand from consumers, which means we’ll need to generate (or purchase) this much power, which means we’ll need to charge these rates.” If the PUC finds the case persuasive, it approves the rates and guarantees the utility a reasonable return on its investments in power and grid upkeep.

Thrilling, I know. The thing to remember is that it is in a utility’s financial interest to generate (or buy) and deliver as much power as possible. The higher the demand, the higher the investments, the higher the utility shareholder profits. In short, all things being equal, utilities want to sell more power. (All things are occasionally not equal, but we’ll leave those complications aside for now.)

Now, into this cozy business model enters cheap distributed solar PV, which eats away at it like acid.

First, the power generated by solar panels on residential or commercial roofs is not utility-owned or utility-purchased. From the utility’s point of view, every kilowatt-hour of rooftop solar looks like a kilowatt-hour of reduced demand for the utility’s product. Not something any business enjoys. (This is the same reason utilities are instinctively hostile to energy efficiency and demand response programs, and why they must be compelled by regulations or subsidies to create them. Utilities don’t like reduced demand!)

It’s worse than that, though. Solar power peaks at midday, which means it is strongest close to the point of highest electricity use — “peak load.” Problem is, providing power to meet peak load is where utilities make a huge chunk of their money. Peak power is the most expensive power. So when solar panels provide peak power, they aren’t just reducing demand, they’re reducing demand for the utilities’ most valuable product.

But wait. Renewables are limited by the fact they are intermittent, right? “The sun doesn’t always shine,” etc. Customers will still have to rely on grid power for the most part. Right?

This is a widely held article of faith, but EEI (of all places!) puts it to rest. (In this and all quotes that follow, “DER” means distributed energy resources, which for the most part means solar PV.)

Due to the variable nature of renewable DER, there is a perception that customers will always need to remain on the grid. While we would expect customers to remain on the grid until a fully viable and economic distributed non-variable resource is available, one can imagine a day when battery storage technology or micro turbines could allow customers to be electric grid independent. To put this into perspective, who would have believed 10 years ago that traditional wire line telephone customers could economically “cut the cord?” [Emphasis mine.]Indeed! Just the other day, Duke Energy CEO Jim Rogers said, “If the cost of solar panels keeps coming down, installation costs come down and if they combine solar with battery technology and a power management system, then we have someone just using [the grid] for backup.” What happens if a whole bunch of customers start generating their own power and using the grid merely as backup? The EEI report warns of “irreparable damages to revenues and growth prospects” of utilities.

Utility investors are accustomed to large, long-term, reliable investments with a 30-year cost recovery — fossil fuel plants, basically. The cost of those investments, along with investments in grid maintenance and reliability, are spread by utilities across all ratepayers in a service area. What happens if a bunch of those ratepayers start reducing their demand or opting out of the grid entirely? Well, the same investments must now be spread over a smaller group of ratepayers. In other words: higher rates for those who haven’t switched to solar.

That’s how it starts. These two paragraphs from the EEI report are a remarkable description of the path to obsolescence faced by the industry:

The financial implications of these threats are fairly evident. Start with the increased cost of supporting a network capable of managing and integrating distributed generation sources. Next, under most rate structures, add the decline in revenues attributed to revenues lost from sales foregone. These forces lead to increased revenues required from remaining customers … and sought through rate increases. The result of higher electricity prices and competitive threats will encourage a higher rate of DER additions, or will promote greater use of efficiency or demand-side solutions.Did you follow that? As ratepayers opt for solar panels (and other distributed energy resources like micro-turbines, batteries, smart appliances, etc.), it raises costs on other ratepayers and hurts the utility’s credit rating. As rates rise on other ratepayers, the attractiveness of solar increases, so more opt for it. Thus costs on remaining ratepayers are even further increased, the utility’s credit even further damaged. It’s a vicious, self-reinforcing cycle:

Increased uncertainty and risk will not be welcomed by investors, who will seek a higher return on investment and force defensive-minded investors to reduce exposure to the sector. These competitive and financial risks would likely erode credit quality. The decline in credit quality will lead to a higher cost of capital, putting further pressure on customer rates. Ultimately, capital availability will be reduced, and this will affect future investment plans. The cycle of decline has been previously witnessed in technology-disrupted sectors (such as telecommunications) and other deregulated industries (airlines).

(“Despite all the talk about investors assessing the future in their investment evaluations,” the report notes dryly, “it is often not until revenue declines are reported that investors realize that the viability of the business is in question.” In other words, investors aren’t that smart and rational financial markets are a myth.)

Bloomberg Energy Finance forecasts 22 percent compound annual growth in all solar PV, which means that by 2020 distributed solar (which will account for about 15 percent of total PV) could reach up to 10 percent of load in certain areas. If that happens, well:

Assuming a decline in load, and possibly customers served, of 10 percent due to DER with full subsidization of DER participants, the average impact on base electricity prices for non-DER participants will be a 20 percent or more increase in rates, and the ongoing rate of growth in electricity prices will double for non-DER participants (before accounting for the impact of the increased cost of serving distributed resources).So rates would rise by 20 percent for those without solar panels. Can you imagine the political shitstorm that would create? (There are reasons to think EEI is exaggerating this effect, but we’ll get into that in the next post.)

If nothing is done to check these trends, the U.S. electric utility as we know it could be utterly upended. The report compares utilities’ possible future to the experience of the airlines during deregulation or to the big monopoly phone companies when faced with upstart cellular technologies. In case the point wasn’t made, the report also analogizes utilities to the U.S. Postal Service, Kodak, and RIM, the maker of Blackberry devices. These are not meant to be flattering comparisons.

Remember, too, that these utilities are not Google or Facebook. They are not accustomed to a state of constant market turmoil and reinvention. This is a venerable old boys network, working very comfortably within a business model that has been around, virtually unchanged, for a century. A friggin’ century, more or less without innovation, and now they’re supposed to scramble and be all hip and new-age? Unlikely.

So what’s to be done? You won’t be surprised to hear that EEI’s prescription is mainly focused on preserving utilities and their familiar business model. But is that the best thing for electricity consumers? Is that the best thing for the climate?

We’ll dig into those questions in my next post.

Something BIG is Collapsing Out of the Public’s Sight…

We are told by the MSM that the sale of $650 million worth of

Cypriot Gold has just caused a 3+% drop in the price of Gold (and more

than 5% in Silver). Is this credible?

The Fed is creating $85 billion per month or close to $3 billion per day, 24/7. The Cypriot Gold at is only 1/5th of what our Fed prints EVERY day! The U.S. Treasury borrows some $4 billion per day to keep our well oiled economic engine running, ALL of the Cypriot Gold is about 1/7th of what the U.S. borrows each and EVERY day. Last month, China imported from Hong Kong alone some 97 tons or roughly 7 times the amount of Cyprus’s total Gold holdings, the Cypriot Gold is a mere 4 days worth of imports. One other way to look at this is that 14 tons is about 6 tenths of 1 percent of the global production of Gold for 1 year…it is nothing. No, $650 million in today’s world is LESS THAN NOTHING!

By Bill Holter, Miles Franklin Ltd,:

I had not planned any commentary this weekend but with Gold “down” $65 per ounce I will put my 2 cents in. As you know, I called “bottom” about 5 weeks ago the first time we hit $1,550 then again about 2 weeks ago on the retest of those levels. They were broken decisively Friday. The “reason” for Wednesdays sell off of $25? And the reason given for today’s $65 by the CNBC know nothings? ……..Cyprus!

The Fed is creating $85 billion per month or close to $3 billion per day, 24/7. The Cypriot Gold at is only 1/5th of what our Fed prints EVERY day! The U.S. Treasury borrows some $4 billion per day to keep our well oiled economic engine running, ALL of the Cypriot Gold is about 1/7th of what the U.S. borrows each and EVERY day. Last month, China imported from Hong Kong alone some 97 tons or roughly 7 times the amount of Cyprus’s total Gold holdings, the Cypriot Gold is a mere 4 days worth of imports. One other way to look at this is that 14 tons is about 6 tenths of 1 percent of the global production of Gold for 1 year…it is nothing. No, $650 million in today’s world is LESS THAN NOTHING!

By Bill Holter, Miles Franklin Ltd,:

I had not planned any commentary this weekend but with Gold “down” $65 per ounce I will put my 2 cents in. As you know, I called “bottom” about 5 weeks ago the first time we hit $1,550 then again about 2 weeks ago on the retest of those levels. They were broken decisively Friday. The “reason” for Wednesdays sell off of $25? And the reason given for today’s $65 by the CNBC know nothings? ……..Cyprus!

Yep, Cyprus

may sell ALL of their Gold and swamp the market! This weeks price

action is merely “front running” these sales in order to get out before

the price is CRUSHED! But wait, Cyprus has less than 14 tons of

Gold…this is worth some $650 million (yes, with an “M”) yet they have an

updated shortfall of some $23 billion (with a “b”) so how does selling

their Gold fix their problems? Well obviously it does not even amount

to a drop in the bucket as it is only 3% or so of what capital they will

need to raise!

Let me put this into perspective

for you in a couple of different ways. The Fed is creating $85 billion

per month or close to $3 billion per day, 24/7. The Cypriot Gold is

only 1/5th of what our Fed prints EVERY day! The U.S. Treasury borrows

some $4 billion per day to keep our well oiled economic engine running,

ALL of the Cypriot Gold is about 1/7th of what the U.S. borrows each and

EVERY day. Last month, China imported from Hong Kong alone some 97

tons or roughly 7 times the amount of Cyprus’s total Gold holdings, the

Cypriot Gold is a mere 4 days worth of imports. One other way to look

at this is that 14 tons is about 6 tenths of 1 percent of the global

production of Gold for 1 year…it is nothing. No, $650 million in

today’s world is LESS THAN NOTHING!

So, we are told

that the sale of $650 million worth of Gold has just caused a 3+% drop

in the price of Gold (and more than 5% in Silver). Is this credible?

And if it had any credibility at all, this is Gold being sold, not

Silver so why would Silver, platinum, palladium and even copper be sold

off? I will leave you with a few questions that I won’t answer because

the answers are too obvious. Do you really believe that holders of

physical metal would part with their metal if they knew something bad

like a system wide banking failure was imminent? Or a (another)

sovereign was going to default? Or some whackos were going to start

lobbing nuclear weapons up in the air? Would physical holders sell (in

panic fashion no less) because a “treasure” was found or some new mine

opened that had 14 tons of Gold?

Do you see the

lack of logic here? Literally $ trillions in paper monies are being put

into the system and Gold is not only finite, it is scarce to begin

with. More physical has been purchased than produced over the last at

least 20 years so we know that “inventories” are shrinking.

Do you not think that the Chinese would like to take an extra 14 tons

into their hoard? How about the Indians? There are reports of

shortages of Gold in south India, wouldn’t they like this 14 tons to

alleviate the shortage?

Or, maybe I’m reading this

thing the wrong way. Maybe investors are selling their paper Gold

because they suddenly realized that it has no backing. Maybe they will

sell it all the way down to its intrinsic value…ZERO! All I can say is

that in the past whenever Gold was sold off in violent fashion, we soon

found out about another BIG problem that was brewing behind the scenes.

This is my bet, something big, REALLY BIG is collapsing out of sight of

the public’s eye and we will only learn of it after the fact.

By

the way, when the markets close there will be a period of time where no

one has a clue about what the “price of Gold” is. The only thing you

will know is whether you have it or not.

Regards, Bill H.

100 Years Old And Still Killing Us: America Was Much Better Off Before The Income Tax

by Michael

Did you know that the greatest period of economic growth in American history was during a time when there was absolutely no federal income tax? Between the end of the Civil War and 1913, there was an explosion of economic activity in the United States unlike anything ever seen before or since. Unfortunately, a federal income tax was instituted in 1913, and this year it turned 100 years old. But there was no fanfare, was there? There was no celebration because the federal income tax is universally hated. Sadly, most Americans just assume that there is no other option to an income tax. Most Americans just assume that it has always been with us and that it will always be with us. This year, the American people will shell out approximately $4.22 trillion in state and federal income taxes. That amount is equivalent to approximately 29.4 percent of all income that Americans will bring in this year, and that does not even take into account the dozens of other taxes that Americans pay each year. At this point, the U.S. tax code is about 13 miles long, and those that are honest and pay their taxes every year are being absolutely shredded by this system. But wouldn’t the federal government go broke if we didn’t have a federal income tax? No, actually the truth is that the federal government did just fine before there was an income tax. In fact, the U.S. national debt has gotten more than 5000 times larger since the federal income tax and the Federal Reserve were created by Congress back in 1913. As I have written about previously, the Federal Reserve system was actually designed to trap the United States in a debt spiral from which it could never possibly escape, and the federal income tax was needed to greatly expand the size of the federal government and to soak the American people of the funds necessary to service that debt. But it doesn’t have to be this way. America was once much better off before the income tax and the Federal Reserve were created, and we could easily go to such a system again.

What we desperately need to do is to teach the American people a little history lesson. The truth is that the greatest period of economic growth in U.S. history was between the Civil War and 1913 when there was no federal income tax at all. The following is from Wikipedia…

But you know what?

It worked. In fact, it worked fantastically well.

The period between the Civil War and 1913 propelled the United States to greatness. Just check out all of the good things that Wikipedia says happened for the U.S. economy during those years…

Well, early in the 20th century the “progressives” and the social planners started to take control in Washington.

And one of the things that “progressives” and social planners love is an income tax. In fact, the second plank of the Communist Manifesto is a “heavy progressive or graduated income tax”.

Of course they promised us that income tax rates would always remain low. And at first they were quite low. The following is from an articleby Adam Young…

And we have seen how things have worked out. Today, the American people are being taxed into oblivion.

In a previous article entitled “Show This To Anyone That Believes That Taxes Are Too Low“, I listed dozens of other taxes that the American people pay each year in addition to federal and state income taxes…

#1 Building Permit Taxes

#2 Capital Gains Taxes

#3 Cigarette Taxes

#4 Court Fines (indirect taxes)

#5 Dog License Taxes

#6 Drivers License Fees (another form of taxation)

#7 Federal Unemployment Taxes

#8 Fishing License Taxes

#9 Food License Taxes

#10 Gasoline Taxes

#11 Gift Taxes

#12 Hunting License Taxes

#13 Inheritance Taxes

#14 Inventory Taxes

#15 IRS Interest Charges (tax on top of tax)

#16 IRS Penalties (tax on top of tax)

#17 Liquor Taxes

#18 Luxury Taxes

#19 Marriage License Taxes

#20 Medicare Taxes

#21 Medicare Tax Surcharge On High Earning Americans Under Obamacare

#22 Obamacare Individual Mandate Excise Tax (if you don’t buy “qualifying” health insurance under Obamacare you will have to pay an additional tax)

#23 Obamacare Surtax On Investment Income (a new 3.8% surtax on investment income that goes into effect next year)

#24 Property Taxes

#25 Recreational Vehicle Taxes

#26 Toll Booth Taxes

#27 Sales Taxes

#28 Self-Employment Taxes

#29 School Taxes

#30 Septic Permit Taxes

#31 Service Charge Taxes

#32 Social Security Taxes

#33 State Unemployment Taxes (SUTA)

#34 Tanning Tax (a new Obamacare tax on tanning services)

#35 Telephone Federal Excise Taxes

#36 Telephone Federal Universal Service Fee Taxes

#37 Telephone Minimum Usage Surcharge Taxes

#38 Telephone State And Local Taxes

#39 Tire Taxes

#40 Tolls (another form of taxation)

#41 Traffic Fines (indirect taxation)

#42 Utility Taxes

#43 Vehicle Registration Taxes

#44 Workers Compensation Taxes

Yet even with all of these taxes, our local governments, our state governments and our federal government are all absolutely drowning in debt.

In another previous article entitled “24 Outrageous Facts About Taxes In The United States That Will Blow Your Mind“, I listed a number of reasons why our federal income tax system has become a complete and utter abomination that can never be fixed…

1 - The U.S. tax code is now 3.8 million words long. If you took all of William Shakespeare’s works and collected them together, the entire collection would only be about 900,000 words long.

2 - According to the National Taxpayers Union, U.S. taxpayers spendmore than 7.6 billion hours complying with federal tax requirements. Imagine what our society would look like if all that time was spent on more economically profitable activities.

3 - 75 years ago, the instructions for Form 1040 were two pages long. Today, they are 189 pages long.

4 - There have been 4,428 changes to the tax code over the last decade. It is incredibly costly to change tax software, tax manuals and tax instruction booklets for all of those changes.

5 - According to the National Taxpayers Union, the IRS currently has1,999 different publications, forms, and instruction sheets that you can download from the IRS website.

6 - Our tax system has become so complicated that it is almost impossible to file your taxes correctly. For example, back in 1998 Money Magazine had 46 different tax professionals complete a tax return for a hypothetical household. All 46 of them came up with a different result.

7 - In 2009, PC World had five of the most popular tax preparation software websites prepare a tax return for a hypothetical household. All five of them came up with a different result.

8 - The IRS spends $2.45 for every $100 that it collects in taxes.

9 - According to The Tax Foundation, the average American has to workuntil April 17th just to pay federal, state, and local taxes. Back in 1900, “Tax Freedom Day” came on January 22nd.

10 - When the U.S. government first implemented a personal income tax back in 1913, the vast majority of the population paid a rate of just 1 percent, and the highest marginal tax rate was just 7 percent.

11 - Residents of New Jersey pay $1.64 in taxes for every $1.00 of federal spending that they get back.

12 - The United States is the only nation on the planet that tries to tax citizens on what they earn in foreign countries.

13 - According to Forbes, the 400 highest earning Americans pay an average federal income tax rate of just 18 percent.

14 - Warren Buffett had an effective tax rate of just 17.4 percent for 2010.

15 - The top 20 percent of all income earners in the United States payapproximately 86 percent of all federal income taxes.

16 - Sadly, as Bill Whittle has shown, you could take every single penny that every American earns above $250,000 and it would only fund about 38 percent of the federal budget.

17 - The United States has the highest corporate tax rate in the world (35 percent). In Ireland, the corporate tax rate is only 12.5 percent. This is causing thousands of corporations to move operations out of the United States and into other countries.

18 - Some tax havens are doing a booming business in setting up sham headquarters for U.S. corporations. For example, the city of Zug, Switzerland only has a population of 26,000 people but it is the headquarters for 30,000 companies.

19 - In 1950, corporate taxes accounted for about 30 percent of all federal revenue. In 2012, corporate taxes will account for less than 7 percent of all federal revenue.

The wealthy have become absolute masters at avoiding taxes, and the poor are not able to pay much.

So who always gets squeezed?

The middle class does.

No matter what our politicians promise us, the hammer is always brought down on the middle class.

And now, according to The Huffington Post, the IRS says that it can even read our old emails without a warrant to make sure that we are paying all of the taxes that we should be…

Don’t the American people deserve better?

What do you think?

Should America go back to a system where there is no income tax and no Federal Reserve?

Please feel free to share what you think by leaving a comment below…

Did you know that the greatest period of economic growth in American history was during a time when there was absolutely no federal income tax? Between the end of the Civil War and 1913, there was an explosion of economic activity in the United States unlike anything ever seen before or since. Unfortunately, a federal income tax was instituted in 1913, and this year it turned 100 years old. But there was no fanfare, was there? There was no celebration because the federal income tax is universally hated. Sadly, most Americans just assume that there is no other option to an income tax. Most Americans just assume that it has always been with us and that it will always be with us. This year, the American people will shell out approximately $4.22 trillion in state and federal income taxes. That amount is equivalent to approximately 29.4 percent of all income that Americans will bring in this year, and that does not even take into account the dozens of other taxes that Americans pay each year. At this point, the U.S. tax code is about 13 miles long, and those that are honest and pay their taxes every year are being absolutely shredded by this system. But wouldn’t the federal government go broke if we didn’t have a federal income tax? No, actually the truth is that the federal government did just fine before there was an income tax. In fact, the U.S. national debt has gotten more than 5000 times larger since the federal income tax and the Federal Reserve were created by Congress back in 1913. As I have written about previously, the Federal Reserve system was actually designed to trap the United States in a debt spiral from which it could never possibly escape, and the federal income tax was needed to greatly expand the size of the federal government and to soak the American people of the funds necessary to service that debt. But it doesn’t have to be this way. America was once much better off before the income tax and the Federal Reserve were created, and we could easily go to such a system again.

What we desperately need to do is to teach the American people a little history lesson. The truth is that the greatest period of economic growth in U.S. history was between the Civil War and 1913 when there was no federal income tax at all. The following is from Wikipedia…

The Gilded Age saw the greatest period of economic growth in American history. After the short-lived panic of 1873, the economy recovered with the advent of hard money policies and industrialization. From 1869 to 1879, the US economy grew at a rate of 6.8% for real GDP and 4.5% for real GDP per capita, despite the panic of 1873. The economy repeated this period of growth in the 1880s, in which the wealth of the nation grew at an annual rate of 3.8%, while the GDP was also doubled.Sadly, most Americans cannot even conceive of an economy like that. Most Americans cannot even imagine having a nation without a massively bloated federal government and without an unelected central bank centrally planning our financial system.

But you know what?

It worked. In fact, it worked fantastically well.

The period between the Civil War and 1913 propelled the United States to greatness. Just check out all of the good things that Wikipedia says happened for the U.S. economy during those years…

The rapid economic development following the Civil War laid the groundwork for the modern U.S. industrial economy. By 1890, the USA leaped ahead of Britain for first place in manufacturing output.But if we didn’t have an income tax, how did we fund the government? Well, we mostly did it with tariffs and excise taxes. The following is from a recent article by Thomas R. Eddlem…

An explosion of new discoveries and inventions took place, a process called the “Second Industrial Revolution.” Railroads greatly expanded the mileage and built stronger tracks and bridges that handled heavier cars and locomotives, carrying far more goods and people at lower rates. Refrigeration railroad cars came into use. The telephone, phonograph, typewriter and electric light were invented. By the dawn of the 20th century, cars had begun to replace horse-drawn carriages.

Parallel to these achievements was the development of the nation’s industrial infrastructure. Coal was found in abundance in the Appalachian Mountains from Pennsylvania south to Kentucky. Oil was discovered in western Pennsylvania; it was mainly used for lubricants and for kerosene for lamps. Large iron ore mines opened in the Lake Superior region of the upper Midwest. Steel mills thrived in places where these coal and iron ore could be brought together to produce steel. Large copper and silver mines opened, followed by lead mines and cement factories.

In 1913 Henry Ford introduced the assembly line, a step in the process that became known as mass-production.

Prior to ratification of the 16th (income tax) Amendment in February 1913, the federal government managed its few constitutional responsibilities without an income tax, except during the Civil War period. During peacetime, it did so largely — or even entirely — on import taxes called “tariffs.” Congress could afford to run the federal government on tariffs alone because federal responsibilities did not include welfare programs, agricultural subsidies, or social insurance programs like Social Security or Medicare. After the Civil War, tariff revenues sometimes suffered under a protectionist policy ushered in by the Republican Party that supplemented federal income via excises on alcohol, tobacco, and inheritances. But before the war, the need for tariff revenue to finance the federal government generally kept the tariff at reasonable levels. During wartime throughout early American history, the Founding Fathers were able to raise additional revenue employing a different method of direct taxation authorized by the U.S. Constitution prior to the 16th Amendment. These alternative taxing methods gave the young American nation embarrassing peacetime budget surpluses that several times came close to paying off the national debt.So why didn’t we stick with that system?

Well, early in the 20th century the “progressives” and the social planners started to take control in Washington.

And one of the things that “progressives” and social planners love is an income tax. In fact, the second plank of the Communist Manifesto is a “heavy progressive or graduated income tax”.

Of course they promised us that income tax rates would always remain low. And at first they were quite low. The following is from an articleby Adam Young…

The presidential election of 1912 was contested between three advocates of an income tax. The winner, Woodrow Wilson, after the ratification of the Sixteenth Amendment, called a special session of Congress in April 1913, which proceeded to pass an income tax of 1% on incomes above $3,000 and applied surcharges between 2% and 7% on income from $20,000 to $500,000.But once the “progressives” and the social planners get their feet in the door, they always want more.

And we have seen how things have worked out. Today, the American people are being taxed into oblivion.

In a previous article entitled “Show This To Anyone That Believes That Taxes Are Too Low“, I listed dozens of other taxes that the American people pay each year in addition to federal and state income taxes…

#1 Building Permit Taxes

#2 Capital Gains Taxes

#3 Cigarette Taxes

#4 Court Fines (indirect taxes)

#5 Dog License Taxes

#6 Drivers License Fees (another form of taxation)

#7 Federal Unemployment Taxes

#8 Fishing License Taxes

#9 Food License Taxes

#10 Gasoline Taxes

#11 Gift Taxes

#12 Hunting License Taxes

#13 Inheritance Taxes

#14 Inventory Taxes

#15 IRS Interest Charges (tax on top of tax)

#16 IRS Penalties (tax on top of tax)

#17 Liquor Taxes

#18 Luxury Taxes

#19 Marriage License Taxes

#20 Medicare Taxes

#21 Medicare Tax Surcharge On High Earning Americans Under Obamacare

#22 Obamacare Individual Mandate Excise Tax (if you don’t buy “qualifying” health insurance under Obamacare you will have to pay an additional tax)

#23 Obamacare Surtax On Investment Income (a new 3.8% surtax on investment income that goes into effect next year)

#24 Property Taxes

#25 Recreational Vehicle Taxes

#26 Toll Booth Taxes

#27 Sales Taxes

#28 Self-Employment Taxes

#29 School Taxes

#30 Septic Permit Taxes

#31 Service Charge Taxes

#32 Social Security Taxes

#33 State Unemployment Taxes (SUTA)

#34 Tanning Tax (a new Obamacare tax on tanning services)

#35 Telephone Federal Excise Taxes

#36 Telephone Federal Universal Service Fee Taxes

#37 Telephone Minimum Usage Surcharge Taxes

#38 Telephone State And Local Taxes

#39 Tire Taxes

#40 Tolls (another form of taxation)

#41 Traffic Fines (indirect taxation)

#42 Utility Taxes

#43 Vehicle Registration Taxes

#44 Workers Compensation Taxes

Yet even with all of these taxes, our local governments, our state governments and our federal government are all absolutely drowning in debt.

In another previous article entitled “24 Outrageous Facts About Taxes In The United States That Will Blow Your Mind“, I listed a number of reasons why our federal income tax system has become a complete and utter abomination that can never be fixed…

1 - The U.S. tax code is now 3.8 million words long. If you took all of William Shakespeare’s works and collected them together, the entire collection would only be about 900,000 words long.

2 - According to the National Taxpayers Union, U.S. taxpayers spendmore than 7.6 billion hours complying with federal tax requirements. Imagine what our society would look like if all that time was spent on more economically profitable activities.

3 - 75 years ago, the instructions for Form 1040 were two pages long. Today, they are 189 pages long.

4 - There have been 4,428 changes to the tax code over the last decade. It is incredibly costly to change tax software, tax manuals and tax instruction booklets for all of those changes.

5 - According to the National Taxpayers Union, the IRS currently has1,999 different publications, forms, and instruction sheets that you can download from the IRS website.

6 - Our tax system has become so complicated that it is almost impossible to file your taxes correctly. For example, back in 1998 Money Magazine had 46 different tax professionals complete a tax return for a hypothetical household. All 46 of them came up with a different result.

7 - In 2009, PC World had five of the most popular tax preparation software websites prepare a tax return for a hypothetical household. All five of them came up with a different result.

8 - The IRS spends $2.45 for every $100 that it collects in taxes.

9 - According to The Tax Foundation, the average American has to workuntil April 17th just to pay federal, state, and local taxes. Back in 1900, “Tax Freedom Day” came on January 22nd.

10 - When the U.S. government first implemented a personal income tax back in 1913, the vast majority of the population paid a rate of just 1 percent, and the highest marginal tax rate was just 7 percent.

11 - Residents of New Jersey pay $1.64 in taxes for every $1.00 of federal spending that they get back.

12 - The United States is the only nation on the planet that tries to tax citizens on what they earn in foreign countries.

13 - According to Forbes, the 400 highest earning Americans pay an average federal income tax rate of just 18 percent.

14 - Warren Buffett had an effective tax rate of just 17.4 percent for 2010.

15 - The top 20 percent of all income earners in the United States payapproximately 86 percent of all federal income taxes.

16 - Sadly, as Bill Whittle has shown, you could take every single penny that every American earns above $250,000 and it would only fund about 38 percent of the federal budget.

17 - The United States has the highest corporate tax rate in the world (35 percent). In Ireland, the corporate tax rate is only 12.5 percent. This is causing thousands of corporations to move operations out of the United States and into other countries.

18 - Some tax havens are doing a booming business in setting up sham headquarters for U.S. corporations. For example, the city of Zug, Switzerland only has a population of 26,000 people but it is the headquarters for 30,000 companies.

19 - In 1950, corporate taxes accounted for about 30 percent of all federal revenue. In 2012, corporate taxes will account for less than 7 percent of all federal revenue.

The wealthy have become absolute masters at avoiding taxes, and the poor are not able to pay much.

So who always gets squeezed?

The middle class does.

No matter what our politicians promise us, the hammer is always brought down on the middle class.

And now, according to The Huffington Post, the IRS says that it can even read our old emails without a warrant to make sure that we are paying all of the taxes that we should be…

The IRS apparently interprets that authority very broadly, the documents show: as long as you’ve stored your email in a cloud service like Google Mail, and as long as those emails haven’t been deleted after a few months, the agency thinks it doesn’t need a warrant to read them.It should be noted that the IRS is claiming that it does not use emails “to target” specific taxpayers, but notice that they are not promising not to use old emails against taxpayers once they are officially being audited or investigated…

The idea of IRS agents poking through your email account might sound at the very least creepy, and maybe unconstitutional. But the IRS does have a legal leg to stand on: the Electronic Communications Privacy Act of 1986 allows government agencies to in many cases obtain emails older than 180 days without a warrant.

That’s why an internal 2009 IRS document claimedthat “the government may obtain the contents of electronic communication that has been in storage for more than 180 days” without a warrant.

“Contrary to some suggestions, the IRS does not use emails to target taxpayers. Any suggestion to the contrary is wrong.”In any event, the truth is that we have one of the most complicated and one of the most intrusive tax systems in the history of the world.

Don’t the American people deserve better?

What do you think?

Should America go back to a system where there is no income tax and no Federal Reserve?

Please feel free to share what you think by leaving a comment below…

SLAMMED AGAIN. Silver Now Below $25.00

Paper silver is slicing through $25.00 on the Globex tonight. Given

the fundamentals, this would be a near impossibility in a freely traded,

HONEST market. $25.00 marks firm support for silver which has held time

and time again for more than three years. Gold has also fallen off a

cliff, now down $35 or so.

These criminals will steal everything in sight, from savings in Cyprus to Social Security to pensions and all points in between. And by issuing billions of ounces of paper metal, they can steal the physical cheaply. The criminal Cartel will offer us no harbor from their crimes.

Smart money is buying tonight. Although if we don’t get a very hard bounce higher tomorrow, next real support is at $20 – 21.

SILVER: The Achilles’ Heel

These criminals will steal everything in sight, from savings in Cyprus to Social Security to pensions and all points in between. And by issuing billions of ounces of paper metal, they can steal the physical cheaply. The criminal Cartel will offer us no harbor from their crimes.

Smart money is buying tonight. Although if we don’t get a very hard bounce higher tomorrow, next real support is at $20 – 21.

SILVER: The Achilles’ Heel

How The Criminal Banking Cartel Is Destroying America

Part Two: How Obama Surrendered Sovereignty to the Criminal Banking Cartel

By John Titus

---

Summary of Part One:

The U.S. government openly conceded that its sovereign authority to enforce its own laws is gone when Attorney General Eric Holder testified that the Justice Department’s failure to prosecute any big banks is based on anonymous “expert” opinions that prosecutions would destabilize the financial system.

This notion of “systemic importance” has been thoroughly discredited. According to Tim Geithner, it’s an intellectually bankrupt phrase. What’s more, it’s been debunked both legally and empirically, which is likely one reason the DOJ’s “experts” wish to remain anonymous.

If it turns out that these “experts” are in fact agents of the big banks whose crimes are being immunized by the very entities whose discredited opinions the DOJ is relying on, then those “opinions” are nothing more than assertions of criminal sovereign immunity—a privilege that is legally limited to the President of the United States.

Since “the King can do no wrong”—the legal foundation of sovereign immunity—the real King here is the criminally immune cartel of banks, not the President, since real sovereigns don’t surrender the right to enforce their laws. And following the long series of unprosecuted crimes by the cartel, in which the President’s own constituents are the undisputed victims, “surrender” is the most charitable description of the Obama’s acts before the banking cartel.

--

Part Two: Inside The Criminal Banking Cartel

There are two very big and related clues as to the identity of the anonymous experts behind whose opinions U.S. Attorney General Eric Holder hides whenever explaining away his failure to prosecute big banks on the basis of their “systemic importance.”

The first, noted in an article last week by Golem XIV, is a list of international banks that parade under the rather obvious label of “Globally Systemically Important Financial Institutions,” or G-SIFIs. There are 28 banks in total, 9 of them headquartered in the U.S.:

Citigroup

Deustsche Bank

HSBC

JP Morgan Chase

Barclays

BNP Paribas

Bank of America

Bank of New York Mellon

Credit Suisse

Goldman Sachs

Mitsubishi UFJ FG

Morgan Stanley

Royal Bank of Scotland

UBS

Bank of China

BBVA

Group BPCE

Group Credit Agricole

ING Bank

Mizuho FG

Nordea

Santander

Societe Generale

Standard Chartered

State Street

Sumitomo Mitsui FG

Unicredit Group

Wells Fargo

This list of cartel members is updated annually by the Financial Stability Board, a collection of international organizations. The FSB is a global meta-body of bankers.

But the formal edifice, whether called the FSB or the NWO (hat tip Alex), really doesn’t matter, because, as Golem XIV states: “Guess which institutions provide the membership for all of the above international bodies? Yes, you got it—the big banks.”

These are the banks that are above the law in the U.S. In Part One, we mentioned four banks—Citigroup, Wells Fargo, HSBC, and UBS—whose massive crimes had been taxed at a de minimis rate by the Department of Justice rather than prosecuted. All four are on the list of G-SIFIs above.

So what, you may ask, that’s just a list compiled by some international convention of cokehead bankers, how do they make sure a rogue federal prosecutor doesn’t break ranks and haul a cartel member or two off to criminal trial?

Enter clue no. 2: Covington & Burling, the law firm from which both the head of the DOJ (Eric Holder) and the DOJ’s head of criminal enforcement (Lanny Breuer) were recruited. Actually, Breuer is no longer with the DOJ. Following a four-year stint in which “the enforcer” failed to prosecute a single big bank, Breuer has returned to Covington & Burling, where he will earn be rewarded with $4 million in annual compensation.

The significance of Covington & Burling lies in its list of current clients, which looks remarkably like the list of criminally immune cartel members above (particularly the more recognizable names): Citigroup, Deutsche Bank, JP Morgan Chase, Bank of America, Goldman Sachs, Morgan Stanley, UBS, Wells Fargo, and ING Bank.

Not to put too fine a point on it, but Eric Holder and Lanny Breuer have the financial motivation not to prosecute their firm’s clients. In Breuer’s case, it turned out to be $4 million of motivation. Per year.

Under any functioning system of law, of course, both Holder and Breuer would submit to screening procedures at the DOJ to insulate them from prosecutorial decisions involving their former clients. We're sure they did the same thing under our impotent system as well. But so what? When laws against crimes are a dead letter, who in his right mind would put any trust in a conflict screen?

As Cheyenne told Jill in Once Upon a Time in the West, “when you’ve killed four, it’s easy to make it five.”

Now commentators are starting to point out where the slippery slope of sovereign immunity for criminal banks will lead. Jim Chanos, who detected the fraud at Enron well before it destroyed the company and its shareholders, notes that not only are criminal cartel members now motivated to continue cheating and stealing, they have a fiduciary duty to do so. (Speaking of the Enron-ization of the U.S., Eric Holder is working to release CEO Jeff Skilling from prison early in yet another act of prostrate submission before his real masters, the criminal banks.)

As Golem XIV points out, immunity extends not only to criminal behavior, but to assets that a cartel member bank acquires through crime: “if by doing those illegal things [the bank] makes out-sized profits for its shareholders and staff, that money, those profits are also above the law.”

--

Cyprus Vs. MF Global: The Rule Of Law Is Dead

Thus, anyone who thinks account confiscation a la Cyprus can’t happen in the U.S. is dreaming of a bygone republic. Not only is account seizure possible in the U.S., or even likely, it is guaranteed. Just ask MF Global’s segregated account holders or GM senior bondholders if you have any doubts.

In the MF Global case, Jon Corzine "brazenly took liquid assets like Treasuries and warehouse receipts, but not cash which would have been more quickly missed, from customer accounts to post as illegal collateral for emergency funding with a lender who must have known that they were receiving stolen goods." The lender, of course, turned out to be JP Morgan--a prominent international cartel member. Jon Corzine was of course one of Obama's top fundraisers and an alumnus of Goldman Sachs--a cartel member.

In the GM bankruptcy, the age-old pecking order of creditor priority was turned upside down, literally "rewriting law," when senior unsubordinated secured creditors' claims were trumped by payouts to junior unsecured creditors in a patently political sop to Obama's perceived union supporters.

In both cases, the black letter law that's supposed to gird markets with trust and predictablity was trampled in favor of Obama's political allies. Now that Obama has altogether surrendered the DOJ's law enforcement functionality to the criminal international banking cartel, those dangerous precedents turn out to have been short-sighted in the extreme: there is nothing left to stop the plunder of customer accounts in Cyprus from crashing like a tidal wave across U.S. shores. The timing depends only on the restraint that the banking cartel elects to show.

There is no remedy in sight, only more financial crime as Americans are robbed deeper into serfdom. The Executive Branch is merely an agent of the criminal banking cartel for the reasons given. That fact, in turn, has cut the Judiciary out of the equation altogether: a court cannot try criminals who are never brought before it to face charges.

That leaves Congress, which in theory could initiate impeachment proceedings. But how likely is success when the Senate, which would try any impeachment cases, couldn’t even obtain the names of the DOJ’s so-called experts in the first place?

As noted in Part One, Senator Grassley asked the DOJ for the experts’ names in a letter on January 29, 2013. Eric Holder testified on March 6, more than a month later. The issue of the experts’ identities was thus as ripe as could be, but rather than obtaining the names, the ranking member of the Judiciary Committee put on a clinic in how to conduct an incompetent examination:

Q. On

January 29, Senator Sherrod Brown and I requested details on who these

so-called 'experts' are. So far we have not received any information.

Maybe you're going to but why have we not yet been provided the names of

experts the DOJ consults as we requested on January 29? We continue to find out why we aren't having these high-profile cases.

A: We will endeavor to answer your letter, Senator. We did not, as I understand it, endeavor to obtain experts outside of the government in making determinations with regard to HSBC.

Just putting that aside for a minute though, the concern that you have raised is one that I, frankly, share. I'm not talking

about HSBC here, that would be inappropriate. But I am concerned that

the size of some of these institutions becomes so large that it does

become difficult for us to prosecute them when we are hit with

indications that if we do prosecute — if we do bring a criminal charge —

it will have a negative impact on the national economy, perhaps even

the world economy. I think that is a function of the fact that some of

these institutions have become too large.

Again, I'm not talking about HSBC, this

is more of a general comment. I think it has an inhibiting influence,

impact on our ability to bring resolutions that I think would be more

appropriate. I think that's something that we — you all [Congress] —

need to consider. The concern that you raised is actually one that I

share.

Note that Senator Grassley asked one question: why haven’t you

answered our letter? Holder doesn’t answer it. Instead, he promises to

supply the names later. At that point, Grassley should have put two

questions to Holder. First, answer my question by explaining why you

ignored our letter. Second, when will you supply the names of the

“so-called experts”?A mediocre first-year litigation associate would’ve gotten this information within seconds. But not Senator Grassley, who earned his masters degree during the Eisenhower Administration. Here is his completely irrelevant follow-up question:

Q: Do you believe that the investment

bankers that were repackaging bad mortgages that were AAA-rated are

guilty of fraud or is it a case of just not being aggressive or

effective enough to prove that they did something fraudulent and

criminal?

Huh? Not surprisingly, Eric Holder has been in no hurry to disclose

the names of the “experts” retained by Covington & Burling’s clients

since dancing around Grassley like a cigar store Indian. Holder has

completely blown off the Senate, which has done nothing to follow up the

issue.Frankly this disgusting charade has surprised no one who’s paying any attention, coming, as it does, from the same august body that exempted itself from insider trading laws and has failed to pass any meaningful reform legislation since the 2008 meltdown, an even worse repeat of which is on its way.

On the contrary, both Congress and the Executive Branch are now just tools of fraud used by the criminal international banking cartel against the people, who for their part are drooling iDope dreams oblivious to their own last act, proving Edward Murrow right, a nation of sheep having begotten a government of wolves.

***

Postscript: for an altogether different analysis that reaches the same conclusion (it's open season for international bankers on U.S. bank accounts), please see what Jesse has to say.

Dollar Collapse In Process: Four Big Nations Have Signed A Currency Deal With China IN LESS THEN 2 MONTHS!! Yuan Reaches Record High Against The US Dollar!!

4 BIG NATIONS that have signed a currency deal with China IN LESS THEN 2 MONTHS!!

- UK

- Brazil

- Australia

- France

American power was necessary during the Cold War. Now that capital moves freely around the globe, capitalists do not require a specific national entity for any particular role. In other words, the American working class will have to pay their way in future. There are no more freebies.

“One more domino in the dollar reserve supremacy regime falls. Following the announcement two weeks ago that “Australia And China will Enable Direct Currency Convertibility“, which in turn was the culmination of two years of Yuan internationalization efforts as summarized by the following: “World’s Second (China) And Third Largest (Japan) Economies To Bypass Dollar, Engage In Direct Currency Trade“, “China, Russia Drop Dollar In Bilateral Trade“, “China And Iran To Bypass Dollar, Plan Oil Barter System“, “India and Japan sign new $15bn currency swap agreement“, “Iran, Russia Replace Dollar With Rial, Ruble in Trade, Fars Says“, “India Joins Asian Dollar Exclusion Zone, Will Transact With Iran In Rupees“, and “The USD Trap Is Closing: Dollar Exclusion Zone Crosses The Pacific As Brazil Signs China Currency Swap“, China has now launched yet another feeler to see what the apetite toward its currency is, this time in the heart of the Eurozone: Paris. According to China Daily, as reported by Reuters, “France intends to set up a currency swap line with China to make Paris a major offshore yuan trading hub in Europe, competing against London.” As a reminder the BOE and the PBOC announced a currency swap line back in February, in effect linking up the CNY to the GBP. Now it is the EUR’s turn.”

Trade between Australia and China just got a little easier.

The Australian dollar is set to become only the third currency to trade directly with the Chinese yuan — a move that will help internationalize China’s currency and smooth transactions between the major trading partners.

Australian Prime Minister Julia Gillard announced the deal Monday during a trip to Shanghai.

“Australia’s banks, superannuation funds and financial houses will be even better placed to help in the growth of China’s service economy,” Gillard said. “This is good news for the Chinese economy and good news for the Australian economy.”

Officials said this will ensure smooth bilateral trade, regardless of global financial conditions.

Along with being the world’s second-largest economy, China is also Brazil’s biggest trading partner.

“If there were shocks to the global financial market, with credit running short, we’d have credit from our biggest international partner, so there would be no interruption of trade,” said Guido Mantega, Brazil’s economy minister.

The Bank of England is in negotiations with its Chinese counterpart on a deal likely to boost trade between the UK and China in the yuan.

The Bank and the People’s Bank of China are close to signing a three-year currency swap arrangement, governor Sir Mervyn King said.

The UK is looking to become a centre for the Chinese currency, also known as the renminbi.

Chancellor George Osborne welcomed the agreement as an “important step”.

Such agreements allow central banks to swap currencies and can be used by firms to settle trade in local currencies rather than in US dollars, as happens now, since China’s currency is not fully convertible to other currencies.

Mr Osborne added that it “cements London as the Western hub for the fast-growing renminbi market”.

- UK

- Brazil

- Australia

- France

American power was necessary during the Cold War. Now that capital moves freely around the globe, capitalists do not require a specific national entity for any particular role. In other words, the American working class will have to pay their way in future. There are no more freebies.

Yuan reaches record high against the US dollar

Apr 13, 2013

Further appreciation predicted, which would fuel inflation on the mainland and in Hong Kong

The yuan reached a record high yesterday as the central bank fixed its midpoint against the US dollar at the strongest level ever.

That sparked anticipation of further appreciation this year and stoked inflationary pressure on the mainland and Hong Kong.

The People’s Bank of China set the midpoint at 6.2506 yuan per US dollar – up from the fixing of 6.2578 on Thursday – ahead of a visit by US Secretary of State John Kerry to Asia. The yuan jumped to 79.775 Hong Kong dollars per 100 yuan, just near the record of 79.729 on Wednesday.

The yuan reached a record high yesterday as the central bank fixed its midpoint against the US dollar at the strongest level ever.

That sparked anticipation of further appreciation this year and stoked inflationary pressure on the mainland and Hong Kong.

The People’s Bank of China set the midpoint at 6.2506 yuan per US dollar – up from the fixing of 6.2578 on Thursday – ahead of a visit by US Secretary of State John Kerry to Asia. The yuan jumped to 79.775 Hong Kong dollars per 100 yuan, just near the record of 79.729 on Wednesday.

China Takes Another Stab At The Dollar, Launches Currency Swap Line With France

04/13/2013“One more domino in the dollar reserve supremacy regime falls. Following the announcement two weeks ago that “Australia And China will Enable Direct Currency Convertibility“, which in turn was the culmination of two years of Yuan internationalization efforts as summarized by the following: “World’s Second (China) And Third Largest (Japan) Economies To Bypass Dollar, Engage In Direct Currency Trade“, “China, Russia Drop Dollar In Bilateral Trade“, “China And Iran To Bypass Dollar, Plan Oil Barter System“, “India and Japan sign new $15bn currency swap agreement“, “Iran, Russia Replace Dollar With Rial, Ruble in Trade, Fars Says“, “India Joins Asian Dollar Exclusion Zone, Will Transact With Iran In Rupees“, and “The USD Trap Is Closing: Dollar Exclusion Zone Crosses The Pacific As Brazil Signs China Currency Swap“, China has now launched yet another feeler to see what the apetite toward its currency is, this time in the heart of the Eurozone: Paris. According to China Daily, as reported by Reuters, “France intends to set up a currency swap line with China to make Paris a major offshore yuan trading hub in Europe, competing against London.” As a reminder the BOE and the PBOC announced a currency swap line back in February, in effect linking up the CNY to the GBP. Now it is the EUR’s turn.”

Australia, China strike deal on currency

April 8, 2013Trade between Australia and China just got a little easier.

The Australian dollar is set to become only the third currency to trade directly with the Chinese yuan — a move that will help internationalize China’s currency and smooth transactions between the major trading partners.

Australian Prime Minister Julia Gillard announced the deal Monday during a trip to Shanghai.

“Australia’s banks, superannuation funds and financial houses will be even better placed to help in the growth of China’s service economy,” Gillard said. “This is good news for the Chinese economy and good news for the Australian economy.”

China and Brazil sign $30bn currency swap agreement

26 March 2013

China and Brazil have signed a currency swap deal, designed to safeguard against future global financial crises.

The pact, first announced last year, will allow their central banks

to swap local currencies worth up to 190bn yuan or 60bn reais ($30bn;

£20bn).Officials said this will ensure smooth bilateral trade, regardless of global financial conditions.

Along with being the world’s second-largest economy, China is also Brazil’s biggest trading partner.

“If there were shocks to the global financial market, with credit running short, we’d have credit from our biggest international partner, so there would be no interruption of trade,” said Guido Mantega, Brazil’s economy minister.

UK and China poised for currency swap deal

22 February 2013The Bank of England is in negotiations with its Chinese counterpart on a deal likely to boost trade between the UK and China in the yuan.

The Bank and the People’s Bank of China are close to signing a three-year currency swap arrangement, governor Sir Mervyn King said.

The UK is looking to become a centre for the Chinese currency, also known as the renminbi.

Chancellor George Osborne welcomed the agreement as an “important step”.

Such agreements allow central banks to swap currencies and can be used by firms to settle trade in local currencies rather than in US dollars, as happens now, since China’s currency is not fully convertible to other currencies.

Mr Osborne added that it “cements London as the Western hub for the fast-growing renminbi market”.

Wall Street Hides from Regulators in “Dark Pools”

Source: All Gov.

While the federal government has pushed Wall Street to make itself more transparent with trading, many high-rolling investors are avoiding more visible venues like the New York Stock Exchange (NYSE) and instead spending their money in so-called “dark pools.”

Established in the 1980s, dark pools are electronic Alternative Trading Systems, often run by big banks, which function similarly to the NYSE, except that traders buy and sell without knowing the bids of others involved.

Participants aren’t the only ones left wondering what exactly transpires in dark pools. Federal regulators have had a tough time knowing if these deals are proper or in the best interests of the market.

A few years ago dark pools made up only a small percentage of all trading. But, recently, there have been days when these shadowy transactions comprised nearly 40% of all deals, up from 16% in 2008. In January, daily dark pool trading actually surpassed the New York Stock Exchange with 920 million trades to 900 million for the NYSE.

So far the Securities and Exchange Commission has refused to adopt new rules regulating dark pools. Some foreign governments, like those in Australia and Canada, have taken a more hands-on approach to limit off-exchange trading.

-Noel Brinkerhoff

DoD Issues Instructions on Military Support of Civilian Law Enforcement

Source: Public Intelligence

Soldiers from the 3rd Battalion, 321st Field

Artillery Regiment, XVIII Fires Brigade train last December to “respond

to an escalating civil-disturbance situation caused by unhappy simulated

hurricane victims.” According to an article produced by the 82nd

Combat Aviation Brigade, the training was designed to prepare the

soldiers “for their upcoming assignment as a quick reaction and rapid

response force for U.S. Army North Command in support of emergencies in

the United States.”

The Department of Defense has issued an instruction clarifying the rules for the involvement of military forces in civilian law enforcement. The instruction establishes “DoD policy, assigns responsibilities, and provides procedures for DoD support to Federal, State, tribal, and local civilian law enforcement agencies, including responses to civil disturbances within the United States.”

The new instruction titled “Defense Support of Civilian Law Enforcement Agencies” was released at the end of February, replacing several older directives on military assistance to civilian law enforcement and civil disturbances. The instruction requires that senior DoD officials develop “procedures and issue appropriate direction as necessary for defense support of civilian law enforcement agencies in coordination with the General Counsel of the Department of Defense, and in consultation with the Attorney General of the United States”, including “tasking the DoD Components to plan for and to commit DoD resources in response to requests from civil authorities for [civil disturbance operations].” Military officials are to coordinate with “civilian law enforcement agencies on policies to further DoD cooperation with civilian law enforcement agencies” and the heads of the combatant commands are instructed to issue procedures for “establishing local contact points in subordinate commands for purposes of coordination with Federal, State, tribal, and local civilian law enforcement officials.”

In addition to defining responsibilities for military coordination with local law enforcement, the instruction describes circumstances in which direct participation in civilian law enforcement is permissible. Under the Posse Comitatus Act of 1878, U.S military personnel are generally prohibited from assisting in civilian law enforcement functions such as search and seizure, interdiction of vehicles, arrest and interrogation, surveillance or using force except for in self-defense. Though the Posse Comitatus Act originally referred only to the Army, it was extended in 1956 to include the Air Force. Subsequent DoD regulations prevent the use of the Marine Corps or Navy for civilian law enforcement functions. In 1981, this principle was further codified in 10 USC § 375 which directs the Secretary of Defense to ensure that military activities do “not include or permit direct participation by a member of the Army, Navy, Air Force, or Marine Corps in a search, seizure, arrest, or other similar activity unless participation in such activity by such member is otherwise authorized by law.”

Though the Posse Comitatus Act is the primary restriction on direct DoD involvement in law enforcement functions, it does not prevent military personnel from participating in circumstances “authorized by the Constitution or Act of Congress.” This includes circumstances involving “insurrection, domestic violence, or conspiracy that hinders the execution of State or Federal law” as well as actions “taken under express statutory authority.” The DoD’s instruction includes a list of more than a dozen “laws that permit direct DoD participation in civilian law enforcement” including many obscure statutes that are more than a hundred years old. For example, a law passed in 1882 and codified under 16 USC § 593 allows for the President to use land and naval forces to “prevent the felling, cutting down, or other destruction of the timber of the United States in Florida.” Likewise, the Guano Islands Act of 1856 enables the President to use land and naval forces to protect the rights of a discoverer of an island covered by the Act.

Military commanders also have “emergency authority” to use military forces in civilian law enforcement functions “in extraordinary emergency circumstances where prior authorization by the President is impossible and duly constituted local authorities are unable to control the situation, to engage temporarily in activities that are necessary to quell large-scale, unexpected civil disturbances”. This authority is limited to actions “necessary to prevent significant loss of life or wanton destruction of property and are necessary to restore governmental function and public order” and “provide adequate protection for Federal property or Federal governmental functions.” In fact, an enclosure to the DoD instruction describing requirements for support of civil disturbance operations states that military commanders “shall not take charge of any function of civil government unless absolutely necessary under conditions of extreme emergency.” According to the instruction, any “commander who is directed, or undertakes, to control such functions shall strictly limit DoD actions to emergency needs and shall facilitate the reestablishment of civil responsibility at the earliest time possible.”

Lloyd Blankfein’s $21m haul makes him the world’s best paid banker

12 Apr 2013 Goldman Sachs paid its chief executive, Lloyd Blankfein,

$21m last year — and granted him a further $5m in bonus shares in

January. The Wall Street bank handed Blankfein $13.3m (£8.7m) in

restricted shares and a $5.7m cash bonus on top of his $2m annual salary

last year. His total 2012 pay was $9m more than in 2011, and the

highest since the $68m he received in 2007, before the financial crisis

struck. The payout, disclosed in a filing with the US regulator the Securities and Exchange Commission (SEC), makes Blankfein, 58, the world’s best paid banker.

Helios orphans fall victim to haircut

ON AUGUST 14, 2005, 33 children were orphaned overnight, their lives irrevocably changed.

These children are the living victims of the fateful Helios Airways crash that killed all 121 passengers onboard the Boeing 737 aircraft, including their parents and, in many cases, their siblings.

On March 16, 2013, the majority of these same children became victims once again. This time, instead of being robbed of their parents, they stand to lose the compensation awarded to them following their parents’ death as part of the brutal haircut on bank deposits.

George Nicolaou and his wife are both 60 years old. For the past seven and a half years they have been the sole carers of their nine-year-old grandson, George, who lost both his parents and sister, in the crash.

Nicolaou has been unemployed for two years. His wife stopped working when their grandson was born, to help look after him, because the couple’s son and daughter-in-law worked full time. Although the couple don’t have much money, they have managed to get by. They have also felt secure in the knowledge that they had around €1 million in a fixed deposit account with the Bank of Cyprus.

“This was the compensation he got for losing his mother and father and sister,” said Nicolaou.

The figure is in fact the total sum of money that Nicolaou, his wife, their grandson and other family members all received as compensation for their loss. Instead of keeping their portion of compensation money themselves, however, the grandparents and other family members preferred to give it all to the orphaned boy.

Today, given the terms of the bailout, his grandson might lose up to 60 per cent of that money and there was nothing Nicolaou could do to stop it.

The bitter irony is that he had tried desperately to keep his grandson’s money out of the clutches of the EU and IMF lenders but was prevented from doing so by red tape.

“In the first few weeks of March I wanted to move his money. I felt things weren’t right with the Bank of Cyprus (BoC). I contacted a lawyer and he told me that because the money was in my grandson’s name I had to file an application with the court to take over the management of the child’s money. He said this process would take at least three months.”

Nicolaou said he feared his grandson could also lose the remainder of his money given the present state of affairs at the BoC.

“I want to move it to another bank or to split the money up into four accounts. I don’t know what to do. I just know that I need to protect what is left so that when he’s 18 he’ll have at least something to help him have a start in life,” he said.

“We have nothing to give him. If something happens, there’s no one to help him,” he added.

The grandfather said he and his wife didn’t know how long they would live and they worried what would come of the boy. Although he had aunts and uncles, they had children of their own to provide for, and they had all been comforted in the knowledge that at least the child had some money to give him an education.

“We knew when he was 18 he would have some money to study. Now....,” said Nicolaou, his voice trailing off.

Continuing in a hollow voice, he added: “I feel anxious. Anxious about his future. A lot, a lot of anxiety.”

Nicolaou said had the first bailout package been agreed, his grandson would have lost only 10 per cent of the compensation money.

“That would not have been a problem. It [10 per cent haircut] would have been the interest he’d collected so far. He would have just had to start over again. Now though, he’s lost so much. It’s just so unjust. You hear about so many bigwigs getting tipped off and moving their money. It’s so unfair. Other people make mistakes and other people pay,” he said.

In the meantime, the 60-year-old said he’d hired a lawyer to try to help him get access to the money to move it. He only hoped that he managed to do it before his grandson lost everything.

“The way the BoC is going I don’t know if anything will be left,” he said.

The government spokesman said yesterday that while George Nicolaou and the other orphans could not escape the haircut on their compensation, the government would do its best to reimburse them.

But the spokesman, Christos Stylianides, conceded there was no guarantee when this might happen or how much the children might receive towards covering their losses.

“Each individual case will be examined. They could be [reimbursed] the total amount [lost]. This issue will be the responsibility of the Labour Minister... The government feels very compassionate [about this issue] and there is the political will,” he told the Sunday Mail.

Despite the government’s assurances, the orphans’ relatives have understandable doubts to what extent its promise will stand.

Neoclis Neocleous is another broken man. You can hear it in his voice when he speaks to you.

“What do you want me to say? What can I do? It’s a mess.” The desolation the 61-year-old feels is almost tangible.

Neocleous is the guardian of his two granddaughters aged 11 and 9. His daughter, the girls’ mother, and son-in-law, their father, was killed in the Helios crash. When the girls received compensation in the region of €1 million each for their parents’ death, he put all the money in Laiki bank for safekeeping. This sum was the total compensation received by all the relatives of the girls’ parents. The relatives kept none of the money themselves, preferring instead to give it to the orphaned girls. Some of the money was put in high-yield securities and the other in fixed-term deposits. Like any grandparent, Neocleous was looking out for his grandchildren’s future. Today, that future looks extremely bleak.

“These are minors under the state’s protection until they are 18. How can they come and take their money?” he asked.

Like Nicolaou, Neocleous had tried to move his granddaughters’ money but his hands had been tied due to the lengthy court procedure to get access to it. Now, he doesn’t know if the two girls will see a penny of it.

The pensioner said he and his wife used to receive €270 a month for both girls from the social services but that last August the attorney-general (AG) had ruled that the children were not really orphans and that they should be exempt from receiving state aid. Nicolaou said he had also stopped receiving the same aid for his grandson on the same grounds.

“The AG ruled they aren’t really orphans because they are living with me and I am now their father. As if that’s even possible! Me? Their father? How does that even make sense? How is it possible? And this ruling comes from an AG who covered for his son. Do you see what goes on in this country?” he said.

Neocleous was referring to last week’s confirmed reports that the AG had suspended prosecution for his son’s driving violations.

Neocleous could not seem to get his head round the fact that his two granddaughters, two little girls who have suffered from the day they lost their parents, could be subjected to this from a state under whose care they were.

“They are protected by the state, by the court, how could this happen?” he said.

The 61-year-old pensioner said he had no intention of taking this lying down and that he would fight this to the end, including going to the European Courts.

“They don’t need the money for at least another six or seven years but I will get it for them,” he said.

Asked to describe how he felt since March 16, the grandfather said “despair”.

“The children (his daughter and son-in-law) are being killed for a second time. This is Helios all over again. It is opening old wounds. These are two minors. Where is the justice now? This money is their parents’ lives. The pain of losing a child is indescribable. It is the ultimate pain. Everyone says they feel for you, but the reality is so much worse,” he said.