“There are a bunch of folks who say that we’re wildly overspending, even though we aren’t.”

President Obama argued, “there are a bunch of folks

who say that we’re wildly overspending, even though we aren’t” and that

many things on the Internet and news broadcasts “are just factually

inaccurate” on Friday’s broadcast of “The Ellen DeGeneres Show.”

Obama: We’re Not ‘Wildly Overspending,’ A Lot of Stuff People Put On Internet and News Is ‘Factually Inaccurate’

“There are a bunch of folks who say that we’re wildly overspending, even though we aren’t.”

President Obama argued, “there are a bunch of folks

who say that we’re wildly overspending, even though we aren’t” and that

many things on the Internet and news broadcasts “are just factually

inaccurate” on Friday’s broadcast of “The Ellen DeGeneres Show.”

Obama said, “The amount of stuff that is just put out there on the

Internet, or on, sometimes news broadcasts that are just factually

inaccurate is surprising, and it’s really hard to catch up. Since I came

into office, we reduced the deficit by two-thirds. But if you ask the

average person, they’re sure that spending has shot up, and the reason

is because, there are a bunch of folks who say that we’re wildly

overspending, even though we aren’t. And that’s just one small example,

but it happens all the time, and that’s something that we have to fix,

partly by people paying more attention to what’s going on every single

day. And it’s hard. People are busy.”

Did you know that there are more than 1.8 trillion

dollars worth of junk bonds outstanding in the United States alone?

With interest rates at record lows all over the world in recent years,

investors that were starving for a decent return poured hundreds of

billions of dollars into high yield debt (also known as junk bonds).

This created a giant bubble, but at first everything seemed to be going

fine. Defaults were very low and most investors were seeing a nice

return. But then the price of oil started crashing and the global

economy began to slow down significantly. Energy company debt makes up

somewhere between 15 and 20 percent of the junk bond market, and the

credit rating downgrades for that sector are coming fast and furious.

But it isn’t just the energy industry that is seeing a massive wave of

defaults, debt restructurings and bankruptcy filings. Just like with

subprime mortgages in 2008, investors are starting to wake up and

realize that the paper that they are holding is not worth a whole lot.

So now investors are rushing for the exits and we are starting to see

panic on a level that we have not witnessed since the last financial

crisis.

Just look at what has been happening in recent days. Investors took

nearly 500 million dollars out of the largest junk bond ETF (iShares

HYG) last week alone. The following chart shows that HYG has now fallen

to the lowest level that it has been since the last financial crisis…

During the last financial crisis, junk bonds starting crashing well

before stocks did. In fact, many consider junk bonds to be a sort of

“early warning system” for stocks. For many analysts, when you see high

yield debt collapse that is a huge warning sign that you need to get

out of stocks as soon as possible.

And this makes perfect sense. When financial trouble erupts, it is going to hit more vulnerable companies first usually.

Blue chip companies are typically not in the high yield debt market.

Normally, high yield debt is only for companies that have more risk

associated with them. And it is risky companies that typically start to

crumble the quickest.

Another high yield ETF that I watch very closely is JNK. As you can see, the chart for JNK looks nearly identical to the chart for HYG…

What these charts are telling us is that a new financial crisis began

during the second half of last year and that it is now accelerating.

At this point, yields have reached levels that we have not seen since

the collapse of Lehman Brothers. The following bit of analysis comes from Wolf Richter…

The average yield of CCC or lower-rated junk bonds hit

the 20% mark a week ago. The last time yields had jumped to that level

was on September 20, 2008, in the panic after the Lehman bankruptcy, as we pointed out. Today, that average yield is nearly 22%!

Today even the average yield spread between those bonds and

US Treasuries has breached the 20% mark. Last time this happened was on

October 6, 2008, during the post-Lehman panic: At this cost of capital, companies can no longer borrow.

Since they’re cash-flow negative, they’ll run out of liquidity sooner or

later. When that happens, defaults jump, which blows out spreads even

further, which is what happened during the Financial Crisis. The market

seizes. Financial chaos ensues.

After junk bonds crashed in 2008, virtually every other kind of investment followed suit.

Just about the only thing that didn’t crash were precious metals.

Gold and silver soared, and that is what you would expect to happen

during a major financial crisis.

Another thing that I am watching closely is margin debt.

During past financial bubbles, we have seen lots of people borrow lots and lots of money to buy stocks.

If that sounds like a really bad idea, that is because it is a really bad idea.

Whenever margin debt peaks and then starts to decline precipitously,

that is a signal that a stock market crash could be imminent. The

following chart comes from James Stack…

After looking at that chart, I can’t understand how anyone couldn’t see the pattern.

We keep making the same mistakes, but we never seem to learn from history. In fact, the mainstream media keeps telling us that this new financial crisis “isn’t 2008? over and over again. Even though the exact same patterns are happening once again, they still believe that this time will somehow be different.

And to a certain extent that is actually true. This current crisis is

not going to be the same as the last one. Eventually, it is going to

prove to be even worse than the last one once everything is all said and

done.

So what should we all be doing? In a recent article entitled “70 Tips That Will Help You Survive What Is Going To Happen To America“,

I gave my readers some basic pieces of advice on how to get prepared

for what is coming. But not all of them will apply immediately. For

example, my wife and I don’t believe that we will need our emergency

food next month. But down the road we are absolutely convinced that we

will need it.

For the moment, one of the key things is to build up an emergency

fund. In my opinion, everyone should have an emergency fund that can

cover at least six months of bills and expenses. And now is not the

time to go into debt. Instead of buying lots of shiny new toys, now is a

time to spend money on practical things that will be needed during the

hard times that are coming.

Unfortunately, most people believe what they want to believe, and

most people do not want to believe that hard times are coming. They

have an extraordinary amount of faith in the system, and they are

convinced that this time will be different somehow.

So I wish them the best, but as for me and my family, we are getting prepared.

What about you?

Are you getting prepared?

Please feel free to share your thoughts with the rest of us by posting a comment below…

In our column last week we were warning you about Deutsche Bank’s

problems and potential issues with its derivatives portfolio and its

capital structure. The story continued to unfold in the past week and

Deutsche Bank was pushed into a corner as more and more investors

started to lose confidence in the bank. A plan to buy back $5.4B in debt in

a desperate move to reassure the capital markets. In fact, Deutsche’s

move is so desperate it will even start buying back debt that was issued

less than six weeks ago.

Where did we see that before? Oh, yes, of course. Lehman Brothers.

When the shit was hitting the fan, Lehman continued to buy (back) assets

instead of keeping the cash in-house to have a financial buffer to

counter any potential liquidity issue.

Well, the financial world definitely wasn’t assured by Deutsche

Bank’s reassurances, and this effect was predominantly felt in the gold

market as the gold price jumped to a multi-year high at in excess of

$1264/oz. That’s very nice, but what’s even more interesting is the fact

the buying pressure actually started on Thursday, right at the moment

the Hong Kong Stock Exchange opened.

Source: kitco.com

This is very interesting as the Chinese buyers haven’t been willing

to shown their eagerness to get their hands on gold, and a strong gold

price appreciation during the Hong Kong trading hours was quite

remarkable. We’re looking forward to see how the gold price will behave

on Monday, as the US and Canadian exchanges will be closed. Will there be another coup coming from Asia?

Let’s have a look how strong the outbreak of the gold price was, and

how the Hong Kong trading day played a pivotal role on Thursday.

Source: stockcharts.com

The moment the gold price broke through the 200 day moving average,

all bets were off and several traders correctly recognized this could

potentially be a real game changed. And indeed. Just 4 trading days

after breaking through the 200MA, the gold price already touched the

$1200oz-level, where it stayed at for approximately 3 days without being

able to break through this symbolical level (yellow rectangle). Enter

the scene: Hong Kong traders (orange arrow). In just one move they

lifted the gold price above $1200/oz overnight, taking the Western

traders by surprise, who quickly had to unwind their short positions,

further strengthening the spike in the gold price to $1264/oz.

Source: Ibidem

Looking at the multi-year chart, it’s now pretty obvious the

downtrend has been broken, and gold is now swiftly moving higher. Not

only does this confirm the theoretical and technical pattern we saw

after the 200MA was captured, there also seems to be some more room to

run. The RSI, for instance, is still in the ‘safe’ zone, whilst the

Money Flow Index (the yellow circle below the chart) also hasn’t reached

alarming levels just yet.

Additionally, the gold/oil ratio has posted a new record as well. The

previous record of 41 barrels of oil per ounce of gold was in 1892,

but the eruption of the current crisis has now crushed that ‘record’.

This is also a very important sign to prove the volatility of the

markets is still exceptionally high. As gold and oil are moving in the

opposite directions, the markets are indicating they are expecting to

see more problems in the near future.

Source: Deutsche Bank via iii.co.uk

We remain unsure Janet Yellen and Mario Draghi are the right captains

to save us from this rollercoaster called the ‘world economy’, and we

hope you have started to protect yourself and your assets!

Credit derivatives trade volumes doubled over the past month

Barometers of risk rose to multi-year highs this week

As markets plunge globally, investors are seeking refuge in an all-but-forgotten place.

Trading volumes in the credit-default swaps market — where banks and

fund managers go to hedge against losses on corporate and government

debt — have surged. Transactions tied to individual entities doubled in

the four weeks ended Feb. 5 to a daily average of $12 billion, according

to a JPMorgan Chase & Co. analysis of trade repository data. The

volume of contracts on benchmark indexes in the market increased

two-fold during that period to an average of $87 billion a day.

The growth could represent a shift. The credit derivatives market has

contracted for almost a decade, after loose monetary policies triggered

a big rally in assets including corporate bonds, which made investors

less eager to protect against the worst. Regulators have also urged

banks to curb their risk taking, reducing the appetite for at least some

dealers to trade the instruments. Now, stock markets are selling off

and junk bond prices are plunging, increasing investor demand for

protection.

“The surge we’ve seen in trading is likely to stay with us for the

foreseeable future,” said Geraud Charpin, a portfolio manager at BlueBay

Asset Management in London, which oversees $58 billion and has traded

more credit-default swaps on individual credits in the past three

months. “The credit cycle has turned, so there’s more appetite to go

short and buy protection.”

Risk measures fell on Friday after soaring this week to the highest

levels since at least 2012 in the U.S., and 2013 in Europe. The cost of

insuring Deutsche Bank AG’s subordinated debt dropped from a record

after the German lender said it planned to buy back about $5.4 billion

of bonds to allay investor concerns about its finances. The bank’s

shares have lost about a third of their value this year. http://www.bloomberg.com/news/articles/2016-02-12/credit-default-swaps-are-back-as-investors-look-for-panic-button

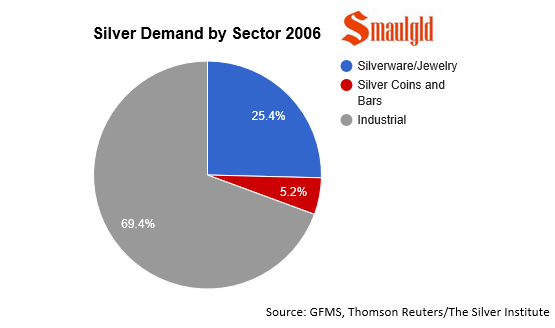

Silver Institute Reports show multi year supply demand silver deficits, as the price falls.

Physical silver supply and demand numbers don’t add up.

Late last month, the Silver Institute, in conjunction with Thomson Reuters GFMS,released its “2016 Silver Market Trends” that tracks silver supply and demand trends. Also late last month, Thomson Reuters was involved in a masssive miscalcuation of the price of silver in conjuntion the CME Group.

Miscalculation of The Price of Silver

The price of silver is determined via COMEX futures silver trading

and the LBMA Silver Price. Both price discovery mechanisms involve

either Thomson Reuters and the CME Group, operator of the COMEX silver futures exchange.

The prices emanating from the Silver Price and COMEX have little to do

with the physical supply/demand dynamics of silver, at least not in

accordance with the supply and demand numbers that the Silver Institute

puts together with Thomson Reuters. COMEX

The price of silver is determined on the COMEX exchange, operated by

the CME Group, via the trading of silver futures and options contracts

of 5,000 ounces of silver (with a physical delivery option) and

mini-futures contracts of 1,000 ounces of silver (without a physical

delivery option). For an explanation ofhow COMEX operates, click here. The LBMA Silver Price

In August 2014, Thomson Reuters along with the CME Group, won the right to replace the “Silver Fixing Company” that was established in 1897. Thompson Reuters and the CME Group, together with the London Bullion Market Association (LBMA) launched the LBMA Silver Price, an electronic auction platform on which the price of silver is calculated.

On January 28, 2016, the Silver Price “broke” in that it produced a silver price far below the spot price of trading on the COMEX.

Such a large and glaring mismatch in the silver price between the COMEX and the LBMA Silver Price rattled the markets and shook investor confidence in the pricing mechanism of silver.

SGT bullion and David Morgan recap what happen to the LBMA Silver Price in this podcast. Ronan Manly of Bullion Star provides further details here.

Reuters reported after the Silver Price debacle that Thomson Reuters and the CME Group were working to create new silver benchmark.

Thomson Reuters’, miscalculation of the Silver Price, spurred us to

revisit the silver supply/demand numbers that they compile with the

Silver Institute for possible miscalculations.

Something is amiss.

Miscalculation of Silver Demand

The Silver Institute includes in its demand components: jewelry and

silverware, coins and bars and industrial fabrication. Determining

jewerly/silverware and industrial demand can only be done by

approximating demand. Silver coin demand, however, can be determined

with a decent level of accuracy as each of the large sovereign mints

like theAustrian, Canadian,Perth and United States Mints, publish their mintages.

Silver bar demand is more difficult to estimate as the numbers of

silver bars and rounds produced by private mints are less readily

available. Yet, an assumption might be made that if silver coin sales

are up significantly, silver bar and round sales might also be higher.

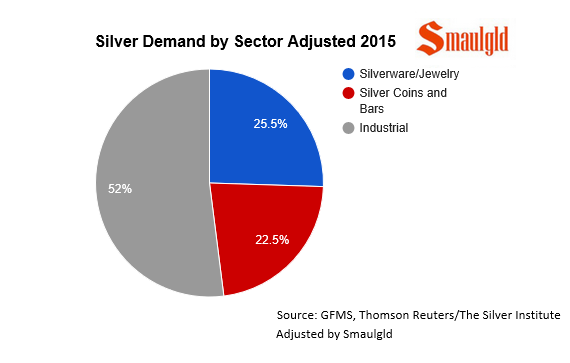

We would estimate that if government mint coin demand demand is up 21% in 2015, privately minted silver rounds and bars would be up by at least that much.

The Silver Institute noted that during 2015 there was a “largely

unexpected surge resulted in an unprecedented shortage of current year

silver bullion coins among the world’s largest sovereign mints”.

During the great silver coin shortage of 2015, sales privately minted silver bars and rounds were also surging. Demand for privately minted silver rounds and bars fell in 2015?

Yet, the Silver Institute 2015 projections do not include ANY

increase in demand for privately minted silver bars and rounds in 2015

and reflect a stunning 21% drop!

According to the Silver Institute, silver coin demand in 2014 was

approximately 107 million ounces of a total 203.5 million ounce demand

for silver coins and bars. This means that in 2014, demand for silver

products not produced by government mints was about 96.5 million ounces.

In 2015, the Silver Institute estimates that silver coin demand will

increase to 129.9 million ounces up from 107.5 million ounces in 2015,

but overall silver coin and bar demand will increase just 1.4% from

203.5 million ouces to 206.5 million ounces.

This means that, according to the Silver Institute, demand for silver

bars and rounds is projected to fall 21% from 96.5 million ounces in

2014 to 76.6 million ounces in 2015. We believe that if silver coin demand rose 21% in 2015, silver bar and round demand grew by at least the same amount.

In 2014, silver bars and rounds accounted 96.5 million ounces. A 21%

increase in 2015 from 2014 would mean demand for silver bars and rounds

would increase to 116.8 million ounces or a 40.2 million ounce

difference from the 76.6 million ounces the Silver Institute projects.

Appendix I: Silver and Industrial Metal Revisited

If the Silver Institute underestimated 2015 privately minted silver

round and bar demand, as we argue they did here, silver coin and bar

demand would rise from a projected 206.5 million ounces to 246.7 million

ounces and over all demand would rise from a projected 1,057.1 million

ounces to 1097.3 million ounces.

Assuming no further adjustments, this would lift the silver coin and bar demand to 22.5% and reduce industrial demand to 52%.

Silver coins and bars constituted just 5.2% of overall silver demand in 2006.

Silver coins and bars are projected to constitute nearly 20% of overall silver demand in 2015.

This chart is amended to assume that if silver coin demand

grew by 21% in 2015, silver round and bar demand also grew by the same

amount vs. the Silver Institute’s projection that silver round and bar

demand declined by 21% in 2015.

Miscalulation of the Silver Deficit

The Silver Institute noted that physical silver was in deficit for the third year in a row.They

projected a deficit for 2015 of 42.7 million ounces which was offset by

“net outflows from ETF holdings and derivatives exchange inventories”

to 21.3 million ounces.

If however, we add the 40.2 million ounces from silver bar and round demand unaccounted for by the Silver Institute, the silver supply demand deficit rises to 82.9 million ounces or 61.5 million ounces when factoring in outflows from ETFs and exchange inventories.

Silver Demand Calculation Does Not Include ETF Demand

The Silver Institute does NOT include demand for silver that backs

exchange traded funds (ETFs) in its demand equation. They show the

amount of silver demand for ETFs below their surplus/deficit

calculation. When silver ETF demand is included it makes the silver

defict larger.

In recent years massive amounts of silver supposedly went to back

silver ETFs. The Silver Institute estimates that from 2006 – 2014, 523.1 ounces of silver went to back ETFs.NONE of this silver is included in Silver Institute’s demand calculation.

Over 500 million ounces are held in silver ETFS but not included in the Silver Institute’s surplus deficit equation.

Miscalcualtion of Silver Solar Demand

According to the Silver Institute, demand for silver from the solar

industry is forecast to increase to 74.2 million ounces in 2015 or about

13% of industrial silver demand and about 7% of overall silver demand.

In our 2014 Silver Supply and Demand report we noted that the Silver Institute had projected 100 million ounces for use in the solar industry in 2015:

Last year the Silver Institute cited a 100 million ounce estimate for 2015 on their solar energy page. They have revised their solar energy page to read “close to 70 million ounces of silver are projected for use by solar energy by 2016.”

Click here to see the Silver Institute’s solar energy page as it appeared on July 9, 2014, projecting over 100 million ounces required for use in the solar energy industry in 2015.

The silver required for solar demand was slashed in the Silver Institue’s interim report at the end of 2015 to 74.2 million ounces and just two months later in their 2016 Silver Market Trends upped silver solar demand to more “than the previous peak of 75.8 Moz (million ounces) set in 2011.”

Miscalculation of Supply

The Silver Institute projects that silver supply will decline 5% in

2016. This is perhaps a reasonble projection based on current silver

mining output. Mining bankruptcies and production cuts, however, may

cause silver output to decline greater in 2016 than the Silver

Institute’s 2016 estimates. Silver In Deficit

The way the Silver Institute calculates supply and demand there will

be a deficit again in 2016. The Silver Institute states that “larger

deficit is expected to be driven by a contraction in supply” even though

their report says that they also expect demand to rise in 2016. The projected silver deficit in 2016, it would seem, would be driven by bothdecreased supply and increased demand.

The Silver Institute also projects that the 2016 deficit will be met from “drawing down from above ground stocks.”

Yet the Silver Institute also notes “Scrap supply, which has been on

the decline for several years, should further weaken in 2016.” Other than scrap silver, the only other known above ground

stocks of silver are the stockpiles held in the COMEX vaults (about 160

million ounces) and the silver ETFS (about 500 million ounces). Are we

to infer excess silver demand will be met from these sources?

Silver held in Comex eligible warehouses as of February 11, 2016, was 157.59 million ounces.

Silver Institute Conclusion on Price

The price of silver has fallen the past several years despite demand

outpacing demand. according to the Silver Institute. In the 2015 Interim

Silver Market Review, the Silver Institute commented on the deficits

and the price of silver: “While such deficits do not necessarily

influence prices in the near term, multiple years of annual deficits

can begin to apply upward pressure to prices in subsequent periods.”.

In 2016 Silver Market Trends the Silver Institute wrote: “The silver

price is expected to find solid ground this year. As of January 26th,

silver prices are up 3.7 percent from the end of last year. This price

appreciation is on the back of increased safe haven demand amid volatile

and weakening equity markets across the globe.” It seems inconceivable in any supply demand analysis for

there to be a significant and persistent shortfall in supply of an

underlying commodity while the price falls consistently. There is either

a miscalculation of the price of silver at the price setting mechanisms

at COMEX and the LBMA Silver Price and/or a miscalcuation of the

physical silver supply and demand dynamic.

Average cost of flight to United States has decreased 2% in two years

Jet fuel has gone down from $986.50 to just $300 per metric tonne

Some airlines still include fuel surcharges on passenger fares

Industry spokesman says number of factors involved in determining price

Airlines

have been accused of charging 'rip-off fares' to passengers on

transatlantic flights, despite the price of jet fuel falling a massive

70 per cent in the last two years.

By comparison, the average cost of a flight to the United States has dropped just two per cent over the same period.

In

September last year, the United Federation of Travel Agents'

Associations (UFTAA) accused the industry of being 'shameless' for

including fuel surcharges within their prices.

+2

The airline industry has been accused of charging passengers 'rip-off fares' at a time when jet fuel is cheaper

These were originally introduced to compensate airlines when the price of fuel rose unexpectedly.

Now

consumer groups and MPs are calling on airlines to stop imposing fuel

surcharges and pass on the savings to its customers with cheaper

flights.

Graham Stringer, a Labour member of the Parliamentary transport select committee, told The Sunday Telegraph that passengers were exposed to 'rip-off air fares'.

Similarly,

Robert Flello, Labour MP for Stoke-on-Trent South, said: 'The price of

fuel in the UK is not far off rock bottom, but all the way through the

chain from oil producer to airline passenger or a person buying

something delivered by a haulage company, customers are being ripped off

pretty much at each level.'

Conservative

MP Martin Vickers, who sits on the Transport Committee, added: 'I

suspect that many transport companies are similar to energy companies

and rather reluctant to pass on the falls as quickly as they pass on the

increases.'

In

February 2014, aviation fuel cost $986.50 per metric tonne. Two years

on, that price has dropped to $300, giving an overall decline of 70 per

cent.

But air fares have not decreased at the same rate.

In 2013, an average flight to the United States cost £688. Two years later, the cost was £671.

At present, some airlines still also include a fuel surcharge or a 'carrier imposed charge'.

Virgin Atlantic, British Airways, American Airlines, and Delta fares all included an additional £143 for such charges.

+2

British Airways does not apply a fuel surcharge, but includes a £143 carrier imposed charge within its fares

European

destinations saw greater reductions in price over a two-year period,

varying from six per cent for flights to Portugal, to 25 per cent for

flights to Ireland.

But the average price of flights to Spain actually rose by 10 per cent over the same two years.

Chris

Goater, spokesman for IATA, the International Air Transport Association

(IATA) said there were a number of factors involved in the pricing of

air fares and was not singularly linked to the price of jet fuel.

Other factors include the fluctuating price of the dollar and operational expenses, including staff wages and equipment.

(Alex Kent)

Despite the country’s unemployment rate falling below 5% in January

for the first time since 2008, and the Federal Reserve’s decision to

raise interest rates for the first time since 2006, concerns about wage

growth — particularly among middle earners — remain. Since 2010, as the

country began to recover from the Great Recession, income of the top 20%

of households grew 3.7% from 2010 through 2014. During that time,

incomes of the middle 20% of households declined 0.7%.

Based on income earned before taxes by the third quintile — the

middle 20% of earners in each state — middle class incomes in Rhode

Island declined the most in the country. Incomes among middle class

Rhode Island households fell by 3.1% from 2010 to 2014, while income

among the state’s fifth quintile, the top 20% of state households, grew

by 4.5%. Based on an analysis of household incomes among America’s

middle class, these are the states where the middle class is suffering

the most.

Consumption is by far the largest component of GDP. Because middle

income families typically spend large shares of their income on goods

and services, America’s middle class is expected to drive up consumption

— and by extension, GDP. While high income households are able to spend

enormous sums of money, there is often only so much an individual can

spend, even on luxury goods.

These are the states where the middle class is dying.

States Where the Middle Class Is Dying

1. Rhode Island > Middle income growth 2010-2014: -3.1% > Fifth quintile income growth 2010-2014: 4.5% (18th highest) > Fifth quintile share of income: 51.2% (10th highest) > Middle class household income: $55,414 (19th highest)

Middle class households in Rhode Island are among the worst off

compared to the highest earning households in the state. From 2010

through 2014, middle class household incomes shrank 3.1% to $55,414 a

year. Over the same period, incomes of the top 20% of households grew by

4.5%, one of the largest income growth disparities between those

cohorts in the country. Consequently, the state’s Gini coefficient

increased nearly four times as fast as the nation’s comparable figure

from 2012 through 2014. Additionally, the state’s labor market is far

from healthy. Nearly 8% of the state’s workforce is unemployed, the

third highest unemployment rate in the country. And while the state’s

unemployment rate has fallen 3.5 percentage points since its peak in

2010, the decline is due largely to a 2.4% contraction in the state’s

labor force. 2. Georgia > Middle income growth 2010-2014: -2.7% > Fifth quintile income growth 2010-2014: 2.7% (22nd lowest) > Fifth quintile share of income: 51.3% (9th highest) > Middle class household income: $49,285 (18th lowest)

Household incomes of the top 20% of earners in Georgia grew by 2.7%

in the five years through 2014, slower than the 3.7% income growth among

that cohort nationally. While the income growth in the top quintile of

households was modest over that period, incomes of middle class

households declined dramatically. Income from Georgian households in the

third quintile fell by 2.7% over that period, more than 2.0 percentage

points faster than the 0.7% decline in middle class incomes nationwide.

Union membership, which can help strengthen a state’s middle class,

is low in the state with just 4.3% of workers belonging to a union,

considerably less than the 11.1% of the American workforce with a union

membership

3. Maine

> Middle income growth 2010-2014: -2.2% > Fifth quintile income growth 2010-2014: 6.0% (11th highest) > Fifth quintile share of income: 49.3% (20th lowest) > Middle class household income: $49,250 (16th lowest)

Unlike most states where the middle class is falling behind, income

in Maine is relatively well distributed. However, the income gap in

Maine is widening faster than in the nation as a whole. Average incomes

among the wealthiest 20% of households in the state grew by 6.0% between

2010 and 2014, one of the faster growth rates and much faster than the

comparable national figure of 3.7%. Incomes earned by middle class

households, on the other hand, declined 2.2% over that time. While more

income has been shifting faster to the state’s wealthiest residents,

both Maine’s unemployment and poverty rates have been lower than the

respective national rates. 4. North Carolina

> Middle income growth 2010-2014: -1.8% > Fifth quintile income growth 2010-2014: 3.3% (25th highest) > Fifth quintile share of income: 51.0% (11th highest) > Middle class household income: $46,677 (11th lowest)

North Carolina’s unemployment rate dropped 4.8 percentage points from

2010 to 6.1% in 2014, just below the national unemployment rate of 6.2%

that year. Despite the improvement, however, income inequality has been

getting worse in the state. The highest earning 20% of North Carolina

households have an average income of more than $166,000, up 3.3% since

2010. Meanwhile, the income of a typical middle class North Carolina

household fell by 1.8%, more than twice the comparable national income

decline of 0.7%.

Union membership, which is often associated with middle class health,

fell 1.3 percentage points to 1.9% in 2014, the lowest share in the

country. Low union membership can often make it more difficult for

workers to organize and advocate for themselves. North Carolina has

resisted workers’ demands to raise the minimum wage above the federal

minimum of $7.25 per hour, which many argue would help mitigate income

inequality. 5. Tennessee > Middle income growth 2010-2014: -1.8% > Fifth quintile income growth 2010-2014: 3.8% (22nd highest) > Fifth quintile share of income: 51.5% (7th highest) > Middle class household income: $44,635 (6th lowest)

In 2010, middle class households in Tennessee earned 14.7% of all

income in the state, a slightly higher share than that earned by middle

class households nationwide. By 2014, that share had dropped to 14.2%,

nearly twice the comparable decline across the country. In fact, the

share of income controlled by the bottom 95% of Tennessee households

contracted between 2010 and 2014, with all income gains going to the top

5%. Those gains contributed to a 7.1% increase in incomes among the top

5% of households, larger than the 6.1% growth for that cohort

nationwide.

At 7.0%, Tennessee’s sales tax is among the highest in the country

and may contribute to declining middle class incomes. A sales tax causes

poorer residents — roughly 18.3% of Tennesseans live in poverty — to

pay a larger share of their income in taxes compared to wealthier

residents. Methodology

To determine the states where the middle class is suffering the most,

24/7 Wall St. used data on the average pre-tax income earned by each

income quintile from theU.S. Census Bureau’s 2014 American Community

Survey (ACS). We defined middle class as the third quintile, or the

middle 20% of earners. We examined the growth in average incomes in the

third and fifth quintiles between 2010 and 2014 to identify income

trends in the middle and upper class. The final list is composed of

states where middle class incomes fell by more than 0.8% and fifth

quintile incomes rose by more than 2.5%. Because ACS income data reflect

pre-tax levels, they may overstate the degree of income inequality in

the poorer quintiles. However, it is unlikely that the tax burden of the

third quintile is significant enough to skew the data.

We also looked at data on the share of aggregate income by quintile

from the ACS, and how that share changed between 2010 and 2014. Also

from the ACS, we reviewed poverty rates and the Gini coefficients. The

Gini coefficient indicates the degree to which incomes in an area

deviate from a perfectly equal income distribution. Scaled between 0 and

1, a coefficient of 0 represents perfectly equal incomes among all

people. All data are from 2010 to 2014. From the Bureau of Labor

Statistics (BLS), we looked at annual unemployment rates from 2010

through 2014. The percentage of non-agricultural employees who identify

as members of a union came from Unionstats.org. Tax data came from the

Tax Foundation, and reflect sales tax rates as of January 1, 2016. More on states where the middle class is dying:

Despite being essential to economic growth, middle class incomes have

suffered from wage stagnation. According to the Economic Policy

Institute, an economic and social policy think tank, one reason that

middle class incomes have remained flat for decades is the divergence of

productivity and wage growth. Just after World War II — a time many

have called America’s golden age — productivity and wages both increased

more than 90%. Since 1973, productivity has continued to climb,

increasing 74.4%. Meanwhile, however, wages have increased by less than

10%. This means owners and investors, many of whom comprise the

wealthiest 20% of households, have by and large reaped the benefits of

the greater productivity. The workers, on the other hand, have not seen

comparable wage increases.

Wealthier households have also benefited from the strong stock market

performance in recent years. Despite weak returns in 2015, all three

major U.S. indices hit all-time highs during the year, allowing those

with money invested to earn even more. With the rich holding a

disproportionately large share of money in the stock market, their

incomes have recovered to their pre-recession levels much faster than

those of middle class workers.

In all 10 of the states where the middle class is suffering, the

share of total income earned by the bottom 80% of households fell from

2010 through 2014 and was redistributed to the highest quintile. The top

20% of U.S. households held more than half of total income in 2014, up

1.08 percentage points from 2010. Even among top earners, income was not

evenly distributed. During that five-year period, the top 5% of

households accounted for more than 85% of income gains for the top 20%

of earners.

Declining union membership may also have contributed to the suffering

of the middle class. In 1979, 24.1% of American workers belonged to a

union. Today, just 11.1% of Americans are unionized. The decline of

union membership has largely mirrored the shrinking of middle class

incomes.

A state’s tax environment can also sometimes exacerbate income

inequality. A 2015 report by researchers at the Federal Reserve Board of

Governors found that federal taxes tend to minimize inequality. States

taxes on gas and goods, however, can have the opposite effect. And since

these are consumed by rich and poor alike, poorer households tend to

pay greater shares of their income on these taxes. In all but one of the

states where the middle class is suffering, consumers are required to

pay sales tax.

World faces a crunch that could see a collapse in London property prices

Despite 2008 crisis being caused by debt, the levels have since risen

Overall debt has gone from 200% of global GDP in 2007 to 250% now

The world

is facing a new crisis caused by an explosion in debt. So warns William

White, the central banker who famously predicted the crisis of 2008.

As

financial markets reeled last week and fears of a fresh recession or

even banking crisis sparked panic, White was more than willing to issue

yet another prophecy of doom.

The

world is now facing a crunch that could see a collapse in property

prices, including those in London; a new global banking crisis; waves of

cheap commodities savaging Western industrial centres; and the need for

debts to be written off on a grand scale.

+5

Predictions: The world is facing a new

crisis caused by an explosion in debt. So warns William White, the

central banker who famously predicted the crisis of 2008

Rather than being better placed to survive, the world is actually worse off than it was in 2008, he argues.

‘At each stage what’s been happening is the imbalances in the global economy have been getting worse and worse.’

White issued

his first warning to central bankers in 2003 at their regular meeting

at America’s Jackson Hole. At the time White was economic adviser to the

Swiss-based Bank of International Settlements – often dubbed ‘the

central bankers’ central bank’.

White

now works part-time at the equally prestigious Organisation for

Economic Co-operation and Development, but Britain has played a

significant role in his life.

Although Canadian-born, he attended the University of Manchester and his first job was as an economist at the Bank of England.

And

the 72-year-old has particular warnings for the UK, notably on its

property market and the risk to British industries such as steel. But

the picture he paints is of a fresh global crisis.

Cheap

money has led to an explosion in debt, taken on by governments,

households and companies – and despite the 2008 crisis being caused by

too much debt, the levels have risen since, he says.

+5

Pressure: White says China’s overcapacity in steel is deflationary

‘Overall

debt has gone from 200 per cent of global GDP in 2007 to 250 per cent

now. The deleveraging hasn’t happened,’ he said, by which he means

companies, households and governments have not paid back enough debt to

be ready for the next crisis.

Britain – and London in particular – could be vulnerable in relation to house prices.

‘Property prices particularly in some bigger places like London, Sydney and Paris would be deemed on the rich side.’

His own son, he says, has just moved from Vancouver in Canada to Victoria because he can no longer afford the property prices.

‘I would consider all of these financial and real assets where they have risen to historically high levels, to be vulnerable.’

At the very least he expects the world to ‘hunker down’.

‘The

banks are going to say the whole world has got very risky. They will be

biased against lending to anyone who isn’t a number one credit.

Consumers are going to say I may have a job today, but maybe not

tomorrow and they will focus on repaying debt. Everybody tries to save

at the same time,’ he warns.

He worries too about a wave of deflation from China, arguing the world is facing an oversupply of things it does not need.

We're

in a new reality, and unless we get to work making it into a reality we

actually want to live in we're going to be in a lot of trouble.

February 13 2016, By James Corbett

Toto, I have a feeling we're not in Kansas anymore. Heck, we're not even on the map.

In case you haven't noticed, things are starting to get crazy out

there. Not just economically (with another global contraction already

well under way) or financially (with teetering European banks leading

global stocks into volatile territory) or monetarily (with the global

currency war reaching a rate-slashing crescendo) or geopolitically (with

new Iranian/Iraqi/Russian cooperation in Syria throwing the NATO powers

off balance), but even socially (with a sea change taking place in the

American electorate, not to mention Europe, Latin America and

elsewhere).

Let's take a look at three stories that show clearly that this craziness

isn't just a bit of turbulence, but a sign that we're moving into a new

paradigm altogether.

1) Negative interest rates This week

Sweden's Riksbank became the latest central bank to surprise people

with a negative interest rate slash. But this time, they weren't going

from a positive rate to a negative rate, but from a negative rate

(-0.35%) to an EVEN MORE negative rate (-0.5%). Welcome to the

new normal, where banks have to pay money to park their reserves at the

central bank. And where Japan can assure the world that they have no

plans to go negative...right before going negative. And where a Spanish

bank which had pegged its mortgages to the (now negative) Swiss Libor

had to pay customers for borrowing from them. Or where the Fed insists

they're not planning to go negative...even while secretly stress testing

banks for the possibility and confronting the (il)legality of such a

move.

For those still trying to wrap their heads around this

idea, here's the skinny: central banks lower rates to encourage people

to borrow (and money to circulate) when the economy is stagnating or

contracting. So what do you do when you've been at or near zero percent

interest for years (or, in Japan's case, decades) and you're still

stagnating? Well there's only one way to go: negative! Or at

least that's the official line. But as you might have guessed there is a

deeper agenda at work here, and you don't have to dig very hard to find

it.

As Washington's Blog recently pointed out, Richard

Werner, the economist who coined the term and the concept of

quantitative easing, argues that negative rates are about driving small

banks out of business and eliminating cash:

As readers know,

we have been arguing that the ECB has been waging war on the ‘good’

banks in the eurozone, the several thousand small community banks,

mainly in Germany, which are operated not for profit, but for

co-operative members or the public good (such as the Sparkassen public

savings banks or the Volksbank people’s banks). The ECB and the EU have

significantly increased regulatory reporting burdens, thus personnel

costs, so that many community banks are forced to merge, while having to

close down many branches. This has been coupled with the ECB’s policy

of flattening the yield curve (lowering short rates and also pushing

down long rates via so-called ‘quantitative easing’). As a result banks

that mainly engage in traditional banking, i.e. lending to firms for

investment, have come under major pressure, while this type of ‘QE’ has

produced profits for those large financial institutions engaged mainly

in financial speculation and its funding.

The policy of

negative interest rates is thus consistent with the agenda to drive

small banks out of business and consolidate banking sectors in

industrialised countries, increasing concentration and control in the

banking sector.

It also serves to provide a (false) further justification for abolishing cash. Conspiracy theory? Nope, just conspiracy fact. As Zerohedge notes, Morgan Stanley' s

head of EMEA equity, Huw van Steenis, recently gave a presentation

which contained the following quotation attributed to an unnamed

"policy-maker" at Davos this year:

"We should move quickly to a cashless society so that we could introduce negative rates well below 1%."

Cripple the banksters' competition and stop the difficult-to-track and

hard-to-control cash economy all in one step? You betcha. Hence we have

central bank after central bank turning rates negative or about to turn

them negative for the first time in history. But wait, there's more...

2) End of the petrodollar

I've been talking about the breakdown of the petrodollar system for

some time at The Corbett Report, both in the pages of this column and in

my various interviews and radio appearances. But it's one thing to hear

it from me, it's another to hear it from the (Rothschilds') horse's

mouth: the revered Financial Times.

"The petrodollar age is

no more but with it go old certainties" blares the dramatic headline

over top of a no less dramatic op-ed from Philip Stephens, associate

editor and chief political commentator for the City of London's favorite

salmon pink news rag. In it, Stephens points out that not only has

conventional wisdom about the economic boon of falling oil prices and

turmoil in the Middle East propping up prices been upended in the

current downturn, but a third rule (that prices may fluctuate but will

always trend upwards) is also being broken:

The accumulating

evidence points to a structural shift that will keep prices relatively

low. During the century before the great price shock of the early 1970s

the real cost of a barrel of oil was between $10 to $40. Economists at

Llewellyn Consulting in London make a convincing case that this trading

range offers a rough template for the future.

What is

happening with this current oil price plunge, many argue, is no mere

blip on the radar, but a fundamental shift that is taking place in the

oil markets now. And as we've talked about before, that's not merely

significant for the oil companies but the entire monetary system, which

for the last few decades has been propping up the international monetary

order via the "petrodollar." With America moving from a net importer to

a net producer of oil and the Saudi-American axis in the Middle East

showing signs of strain, it is entirely possible that we are about to

see a severing of the Saudi petrodollar recycling system that has helped

to undergird the US dollar since Nixon took the country off the gold

standard.

So what does this mean, exactly? No one

knows...yet. But given the machinations that Kissinger undertook (at the

behest of his boss, David Rockefeller) to create the petrodollar system

in the first place, it would be naive to think that some new system

isn't being devised right now. It would also be naive to think that

whatever system comes along to take its place will be founded on peace,

harmony and happiness.

So the average Joe Sixpack and Jane

Soccermom may have no idea what's going on in the international oil

markets or its relation to geopolitics, but they do know something's

wrong, which means...

3) The old political order is collapsing

That we are heading into a new political order should not be

surprising to followers of this column. Heck, it's becoming difficult

for even the most brainwashed of the brainwashed to deny that a

fundamental sea change is taking place in American politics, or European

politics, or Latin American politics, or East Asian politics, or...

But once again it's one thing to hear about this change from James

Corbett of The Corbett Report, it's quite another to hear it straight

from the horse's mouth. Or the horse's pollsters, as it were.

Last week The Huffington Post published a remarkable piece by Patrick

Caddell, a top Democratic pollster and strategist, and Bob Perkins, a

top Republican strategist. The subject of their post? The results of the

Iowa caucuses.

You might be able to guess that old

establishment party hacks would be a bit confused, perhaps even

perturbed by the rise of populist forces in this election cycle and the

dead-on-the-vine nature of "presumed nominees" Jeb "cold tuna sandwich"

Bush and Hillary "exciting as a glass of warm water" Clinton, but that

doesn't even begin to explain the tone of this piece. They start by

quoting an exchange between Louis XVI and one of his ministers where the

king asks if the storming of the Bastile is a revolt and the minister

replies it is a revolution. Things only get gloomier from there.

"Gloomy" from the perspective of the two-party duopolists, that is:

"The upheaval and the explosion of discontent that have provided a

launch-pad for outsider candidates from Donald Trump and Ted Cruz to

Bernie Sanders are not, as so many establishment pundits suggest, just

another episode in the long history of ad-hoc populist moments of

discontent sure to fade away. Our survey data shows that the United

States is in the midst of an evolving political revolution of historic

proportions. In fact, this election could mark the beginning of the end

of two-party duopoly in the United States."

They then go on

to back up that assertion with a series of data from a half dozen

surveys that have taken place over the last three years. The result of

those surveys a nothing short of startling:

84% of Americans believe political leaders are more interested in protecting their power and privilege than doing what is right 75%

believe that powerful interests, from Wall Street to unions to interest

groups, have used campaign and lobbying money to rig the system for

themselves. 72% blame the stagnation of the American economy on corruption and crony capitalism in Washington 67% hold that the US government is not working in the interests of the people 78% agree that both parties are too controlled by special interests to create meaningful change 75% agree that the two party system is flawed and it's time to vote in new political parties with new ideas

Now, none of these statements should be at all surprising or

controversial to my regular readers. If anything, they're a bit weak in

their critique of the current system. But the startling thing is that

this is not a poll of International Forecaster readers or alternative

media acolytes. This is a poll of Americans of all stripes across the

meaningless left/right party lines.

It is becoming more and

more apparent by the day that the lie that we've been sold for decades

-- that we're a marginalized, fringe minority and will never be taken

seriously -- is just another lie that's been sold to the public through

the PR vehicle of the mainstream news. In fact, the vast majority of

Americans are completely fed up and are looking for fundamental change.

Suddenly Sanders and Trump don't seem like minor blips on the political

radar so much as the expression of a growing resolve by the American

people to change the way the game is played.

And this is by

no means a solely American phenomenon. The migration crisis in Europe is

causing a similar seismic shift in political discourse and sentiment

across the continent. Merkel has gone from "Person of the Year" to

fighting for her political life in record time. The inevitable reaction

to political correctness and enforced pan-European multiculturalism is

taking place right now and unleashing populist forces that are

threatening to decimate the political order in Europe and perhaps the

European Union itself.

Latin America has likewise seen a

profound shift taking place in recent months with the disintegration of

what was left of the Chavez regime in the Venezuelan meltdown, the swing

to the right in the Argentinian presidential election and the

destabilization of Rouseff in Brazil. In fact, with the Middle East even

more of a tinderbox than usual and the Asia-Pacific continuing to heat

up along new economic and political fault lines, it's difficult to find

an area of the globe where the political order is not at risk of being

upended.

Now this in and of itself is neither good news nor

bad news. When the towers of the existing political order are toppled,

revolutions tend to revolve back to the same spot one way or another and

the "populist" forces that are being released have more than a slight

stink of authoritarianism to them. All it takes is the right strong man

to come along and galvanize public opinion for the political order to

coalesce into something even more tyrannical. And in such revolutionary

moments there is always the specter of the New World Order from chaos

which has always been part of the plan of the globalists.

But

that this revolutionary moment is here is becoming more and more

difficult to deny. The old political order is dissolving. The only

question is what will take its place.

No, we're not in Kansas

anymore, but we're not over the rainbow, either. There's no Good Witch

of the North to help us on our way and no Ruby slippers to whisk us back

home. We're in a new reality, and unless we get to work making it into a

reality we actually want to live in we're going to be in a lot of

trouble.

In the 1890s Charles Dana, editor of the New York Sun,

referred to Chicago as the “Windy City.” Chicago was one of many cities

competing to host the World’s Fair, and clearly the writer intended the

double entendre to apply to the city’s weather as well as its mouthy

politicians.

When it comes to Chicago’s weather, anyone who has visited “Chi-town”

(as the city is known in CB-lingo) can attest to the screaming wind off

of Lake Michigan. It howls for what seems like days at 40 mph, carrying

with it sub-zero temperature in the winter.

As for Chicago’s politicians, spouting hot air just happens to be a trait common to people in that profession.

But now it might be time to paint some more of them with that broad brush.

Chicago Schools Are Dead Broke

There you have it. The Chicago Public School system (CPS) is broke.

Even after Mayor Rahm Emanuel took a knife to the CPS budget last

summer, cutting away almost half a billion in spending, the system still

faces a $500 million shortfall.

District officials have come up with the brilliant solution to fund

their operations by issuing bonds, as if that will bring in more tax

revenue or lower their expenses. Bond buyers would have the promise that

CPS will use its “full faith and credit” to repay the bonds.

There’s only one problem. It’s a lie, and the district officials know it.

The term “full faith and credit” means that a borrower will use all

assets available to repay a debt. But Chicago’s school system, in the

footsteps of Detroit two years ago and now Puerto Rico, has no intention

of foregoing other expenses to pay bondholders.

Hook, Line, and Sinker

Their plan, just like Detroit and Puerto Rico, is to con whomever

they can into giving the system cash. They have one goal: hold off

bankruptcy just one more day, until there’s not another sucker willing

to take the bait.

In this case, the bait is pretty tempting. The Chicago Public School

system is offering an 8.5% yield on a municipal bond, which equates to a

12.3% taxable yield at a 35% tax rate.

With property as valuable as Chicago’s backing such an offering,

Chicago’s school system is counting on investors to give into greed,

rather than the fear of non-payment. Many of them will. But just as I warned investors away from Puerto Rico’s last bond offering, they should stay away from this piece of kryptonite.

The sad part of the situation in Chicago is that it didn’t have to

happen. The sadder part is that the same story is unfolding around the

country.

The Likely Suspects

The tale starts like so many others: with pensions. Many years ago

the Chicago school system granted generous pension benefits to its

employees. But then the city, which operates the school system, didn’t

keep up with its end of the funding.

From 1995 to 2004, the city of Chicago didn’t contribute one nickel

to the school district’s pension system, even though it is responsible

for a portion of contributions in addition to what employees put in.

In the mid-2000s the city got back on track, but by that time the

system had a significant shortfall. Then the financial crisis of 2008

hit, crushing the value of the pension and also weighing on the city’s

ability to make its obligatory payments.

To give itself some breathing room, the city granted itself a

“pension holiday” from 2011 to 2013, allowing for smaller payments than

it should have made. Today the city of Chicago must contribute about

$700 million to the CPS pension system, an amount that’s increasing by

roughly 7% per year.

For a school system that is running half a billion dollars in the red, that’s simply an unworkable number.

Failed Attempts

The city tried to cut pension benefits (a mixture of lower payments,

longer vesting, and higher employee contributions), but a judge found

that the changes violated the state constitution.

According to that document, any state contractual benefit, such as

pensions, that has been earned or offered in the future, can’t be

reduced. This leaves employees like teachers and administrators in a

strong legal position to demand every cent they were promised.

But the city can’t pay. So it has turned to the state.

Governor Rauner won’t write a blank check to Chicago’s public school

system. He’s willing to bail it out, but only if the city turns over

control and the legislature agrees to let the school system and the city

of Chicago declare bankruptcy.

Hmm.

In a nutshell…

The CPS has zero chance of paying its pension obligations.

The city won’t raise taxes high enough to make good on its debts.

The state will come in only if these entities can declare bankruptcy

and discharge at least some of their debts. Typically that means reduced

bond payments instead of harming employees or retirees, just like

Detroit.

And yet the school system wants to sell new bonds backed by its “full faith and credit.

Right.

What’s Really Scary…

While the situation in Chicago is close to a boiling point, the same

factors are percolating in school districts, cities, counties, and

states across the country.

Just look at this top 10 list of the states with the most underfunded pensions.

The state that tops the list is Illinois, home of the Windy City

itself. As of 2014, only two states have fully solvent pension systems:

South Dakota and Wisconsin.

That’s why it’s so important to research potential bond investments

extensively before you put your money down. You don’t want to end up

relying on the “full faith and credit” of the next Detroit.

Rodney

Follow me on Twitter @RJHSDent

It’s hard to see anything more than more of the same

The great thing about Sundays once the kids quit the nest is that it

can revert to being a time for cool reflection. I include this next

chart not to be a wiseass (I am that man, after all, who hung onto bear

notes for a year too long) but to act as an antidote to the denialist

bollocks we’ve been getting from the 3% for the last three weeks. It

looks at what has happened to the FTSE index since its peak in early May

2015:

The drop between then and now is from 7080 to 5400 – a plunge of

nearly 24%, or just over a quarter. Many commentators haven’t noticed,

but that’s actually a sharper fall than the Shanghai composite has suffered.

I removed my SIPP pension from market exposure last March; add to

that a bit of pension trust bank account interest, and I’m 25% better

off in terms of drawdown income than I was a year ago.

Thinking of the above as a seismograph, the correction to bear market

(blamed on China) began last August; this year so far – just six weeks

in – we’ve had three further corrections (blamed first on China, then on

an oil glut, then on stupidity) which almost exactly doubled the

correction. But even before August (with no China data on the radar) the

trend was downwards.

The one-liner here is small drops, medium rallies, huge shock, medium rally, medium shocks, medium rallies.

Following Yellen’s Fed evidence – and with some good tech and

blue-chip results – Friday began another rally. I think my

interpretation fits the facts better than the Davos Dancers, in that

The oil glut story is only a half-truth; as I showed 11 days ago,

there is bigtime storage going on both pre and post refinement. Demand

for oil has been falling since mid December. World trade has been off

for nearly a year.

Bank stocks are dragging the indices further down. After 2008, the

markets no longer fall for the banker balm about solidity and

capitalisation. I don’t call this stupidity, I call it wising up.

It’s now obvious to traders and analysts that the Central Banks,

having run out of ideas, are into ‘one more heave’ mode in the shape of

negative interest rates. Markets are nervous because monetarist tricks

haven’t worked, and there are no further tricks up the conjuror’s

sleeve. Nirp, they feel, is a mad idea….and probably unconstitutional in

the US.

So, what would one expect to happen next? My gut-feel common sense

says that, with no more intervention and nerve-stroking due now until

March 10th – and no credible good news on the horizon – nerves based on

profound doubt will continue. My sense is that what they doubt is the

fitness for purpose of monetarism…but I could be wrong: at the minute,

the doubt is being – openly at last – expressed as “seems like the Fed

has run out of ammo”.

OK, now let’s assess what the bad news might be.

First stop, ClubMed. There are bond spikes popping through the

terrain again – most noticeably in Portugal, but also in Greece and

Italy. Predictably, this is being blamed on valotivvedee again, but

there’s more to it than that. As I’ve been wittering on about for 18

months or more, when the Italian Fibbing and Banking scandal breaks

properly, all Hell will break loose….and austerity – another dimension

of BB and Berlin monetarism – has left Greece a shamefully overtaxed

disaster area.

Portugal is small but more interesting. Investors were shaken by

the Novo Banco bail-in – and wary of the Government’s inability to sell

it. Its ties to Brazil are another concern; and the controversial 2016

budget – submitted over three months late to the EC – reversed public

wage cuts implemented by its Troika-poked predecessors. The word in

Brussels is that the budget only just squeaked through….and

Dijesselbloem is already saying it “needs to be tightened”. Jeroan does

not, however, seem to have grasped that his policies halved th expected

growth in Portugal last year. But such is only to be expected, as the

man looks and sounds like a sociopathic version of Mr Bean.

Next, the Shanghai reopens later tonight. After the gungeefachoi

break, will the traders – back at their desks after ten days – do what

the West did after its New Year…that is, suffer eyes minus scales

syndrome? Well, off-piste the Shangheisters are buying every ounce of

gold they can lay their severely burned fingers on. This does not

suggest a surge in confidence about equities.

Oddly enough, both the US and Canada are closed tomorrow…so if China

starts to panic, things could get interesting on Tuesday in New York.

I leave you to your Sunday lunches with two final (and to me, significant) signs of real market sentiment.

First, Gold is looking bullish again, and this time the optimism

looks more settled than at any time since 2013. This is the latest

30-day chart:

As for the real thing, there seems little doubt among the US, UK and

Asian retailers that the stuff is flying off the shelves. So one big

fundamental seems to be returning…with potentially disastrous results

for stock markets if a real gold-rush starts.

And finally, you may have noticed the banker excuses being dusted off

and readied last week: regulation has starved us of capital, Zirp is

killing us, but fear ye not because we have complied, lowered our

leverage ratios and as for complex derivatives, haha, what complex

derivatives?

If ever there was a clincher about things being mammories skywards, that one is it.