Greece is selling off bits and pieces of its country to the creditors.

Greek deposits become eligible for bail-ins. Major retailer going out of

business because of decline in sales and revenue. Building permits

plunge in NYC as the property tax expires. Atlanta FED recalculates GDP

to 1.3 as the auto industry increases production and channel stuffs

dealerships. Bail-ins are coming to America and the FDIC will go after

depositors. Global growth has slowed according to Moody’s and the US is

not prepared for a major crisis, the US has no grain reserves since

2008.

Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter “We do not comment on future product speculation,” a Buick

spokesman said, refusing to confirm the leaks, but didn’t deny

them either.

GM sold 919,582 Buicks in China in 2014, four times as many as it

sold in the US! GM manufactures in China nearly all vehicles it sells

there. About half of GM’s earnings are generated in China. After having

been bailed out of bankruptcy by US taxpayers to keep the manufacturing

base in the US, GM bet big on China.

In July, GM announced that it would invest an additional $5 billion

in China to develop a new family of Chevrolet vehicles with its Chinese

partner SAIC. All global automakers have invested billions in China,

year after year, to build new plants, add capacity, and increase

production. More new plants are coming. More capacity is being added. It

all worked out because automakers sold these vehicles in China as fast

as they could make them.

Until this year. But now supply and capacity are still rising. Demand

has started to fall. Inventories are piling up. A vicious price war has

broken out. And the bane of the auto industry, overcapacity, is

suddenly looming ominously above them all.

Overcapacity tore up the industry in the US. It tore up the industry

in the EU. It’s a deadly disease for automakers. It led to bankruptcies

and bailouts. And now it’s spreading in China.

But there is a solution, apparently: exporting China-made vehicles to the US.

A few small-scale efforts have gone nowhere. America is a tough

market. The best companies fight it out on a daily basis and are being

taught lessons the hard way by finicky consumers.

Volvo, owned by Zhejiang Geely Holding, is starting to export its

China-made S60 Inscription to the US this summer. It’s the

long-wheelbase version of the Swedish-made S60 sedan. This will be the

first mass-produced car from China on US streets. Not exactly a tsunami.

But now GM is reportedly jumping into the game in a big way.

On Monday, the first leak appeared, and at a very inconvenient time for GM, currently in contract negotiations with the UAW. Automotive News reported that GM is planning to sell its Chinese-built compact crossover, the Buick Envision, in the US.

“It would fit perfectly in the Buick lineup at a time when crossover

sales are growing fast,” Jack Nerad, executive market analyst at Kelley

Blue Book, told Automotive News. “I’m sure a lot of Buick dealers wish they had it today.”

Crossovers are hot in China, unlike cars, whose sales volumes are

plunging. The Envision, built by GM’s joint venture Shanghai GM, arrived

in Chinese showrooms last fall. And already, over 57,000 were sold

during the first half this year. According to Buick spokesman Nick

Richards, it has been “extremely well-received.”

But China would remain by far the largest market for it. Automotive News:

Both IHS and LMC Automotive forecast a U.S. launch of the

Envision sometime in the second half of 2016, with annual volume

forecasts from the mid-20,000s to the high 30,000s. Their forecasts for

annual Envision sales in China range from 140,000 to 170,000 through

2018.

And US consumers would presumably flock to buy them:

A decade ago, the idea of China-made vehicles in U.S.

showrooms might have turned off American buyers. But that’s far less

likely today, IHS analyst Stephanie Brinley says. In recent years, GM

and other global automakers have built modern assembly plants in China.

And Americans are accustomed to their iPhones and other high-end

consumer goods being made there.

“For the U.S. consumer experience, there is likely to be little

difference between a Buick built at GM’s Orion Assembly plant [near

Detroit] or in Shanghai,” Brinley says.

That was on Monday. On Tuesday, Reuters

added fuel to the fire when it reported, based on two “sources

familiar” with GM’s plans, that “most Buick vehicles sold in the United

States after 2016 could be imported from China and Europe….”

According to the sources, “who did not want to be identified because their companies work with GM”:

Production of the compact Verano sedan will likely be shifted from Michigan to China in late 2016.

Production of the mid-size Regal sedan will likely be shifted from Canada to either China or Europe in 2017.

Buick will import the compact Cascada convertible from Europe early next year.

And production of the subcompact Encore crossover will be shifted from Korea to China.

In the future Buick lineup, only two models would be made in North

America: the replacements for the mid-size LaCrosse sedan and the large

Enclave crossover.

The automotive component industry has already centered itself in

China after the Financial Crisis in a whirlwind of bankruptcies and

reorganizations that led to hundreds of thousands of job losses in the

US. Today, Chinese-made components are used by all automakers that sell

vehicles in the US.

And Chinese-made Buicks, Chevrolets, Fords, Toyotas, and BMWs are

simply the next step. With the rosy prospects of overcapacity tearing up

the industry in China, exports to the US are a natural solution.

When GM jumps into it in a big way, other automakers will follow.

This would be the beginning of the long-awaited and much rumored tsunami

of Chinese-made cars on US streets. American consumers will get used to

them. At first, they were leery of Mexican-made cars; today, they

aren’t even asking anymore.

But hope for the vaunted “Manufacturing Renaissance” in the US takes

another hit, this time from China’s blossoming overcapacity fiasco.

China’s auto market had been the single most important element in the

convoluted recovery of GM and other global automakers. But the market

has been getting battered this year. And since the yuan devaluation, the

elements are coagulating into a toxic mix for GM. Read… China Mess, Yuan Devaluation Spread to the US

Hundreds of bankers used their work emails to register for the adultery website AshleyMadison.com, MarketWatch found after searching the data. Hackers unleashed the email and

street addresses, phone numbers and credit card details of about 36

million users of the adultery website AshleyMadison.com. Here are the financial institutions MarketWatch searched for, and how many associated email addresses were found: Wells Fargo — @wellsfargo.com: 175 Bank of America — @bankofamerica.com: 76 Deutsche Bank — @db.com: 73 Goldman Sachs — @gs.com: 45 PNC Bank — @pnc.com: 28 U.S. Bancorp — @usbank.com: 15 Bank of New York Mellon — @bnymellon.com: 14 Citigroup — @citi.com: 51 J.P. Morgan Chase — @jpmchase.com: 9 Capital One — @capitalone.com: 4 MarketWatch also searched for

@marketwatch.com emails and found none. However, the website did find 10

@dowjones.com emails. (Dow Jones is the parent company that owns

MarketWatch.) The Hill reported that the leak appears to include more than 15,000 government and military emails. According to The Hill, Washington D.C. reportedly has the highest rate of membership for the site of any city. -RW

(WASHINGTON) Someone

call Dunder Mifflin: Several states are reporting a paper crisis, after

an Ohio company that produces highly specialized paper for vital

records closed without warning.

California has been hit the hardest by the shortage, and several

counties are now being forced to ration birth, marriage and death

certificates.

In California, the only other company that can meet its needs, under

state law, is in Canada. Officials say it would likely take months for

Canadian Bank Note Co. to get up to speed with the state’s paper needs –

but that’s only after a contract is signed. In the interim, counties

are left finding short-term solutions for the growing backlog.

The restrictions “will impact a lot of folks,” Rob Grossglauser, a

lobbyist for the County Recorders’ Association of California, told the San Francisco Chronicle.

The closure of Sekuworks, the Ohio paper company, has a handful of

states scrambling to find a fix, including Minnesota and South Carolina.

But California law is specific and requires the state to print all

vital statistic certificates using a specialized – and some argue

antiquated – type of printing, known as “intaglio.” Besides Sekuworks,

no other U.S.-based companies can handle that type of printing.

Since the company closed, several California counties there have

started to limit residents to one copy of a birth, marriage or death

certificate. The restrictions are creating major headaches for people

who are realizing just how important the documents are when trying to

obtain licenses, handle funeral arrangements or apply to schools.

Intaglio printing is done using ink that is below the surface of the

plate. The design is etched into the printing plate, which is typically

made from copper, zinc, aluminum and in some cases, coated paper. The

benefit of intaglio is that it’s a near-perfect way to prevent

counterfeits. Minnesota employs the method for a range of sensitive

documents and South Carolina – which recently adopted new standards –

used it for death certificates.

But critics argue it’s too labor intensive, antiquated and expensive.

In central California, Stanislaus County officials are now working

with area school districts to provide a free “verification of birth” for

people who otherwise would need a copy of their child’s birth

certificate to enroll in school.

California has two types of certified birth notices – an authorized

copy and an informational copy. While both are certified copies of the

original document, an authorized copy establishes the identity of a

person. An informational copy cannot be used for identity purposes and

carries an inscription across the face of the document stating,

“INFORMATIONAL, NOT A VALID DOCUMENT TO ESTABLISH IDENTITY.”

Informational copies are available to anyone who requests one. Authorized copies are not.

County Clerk-Recorder Lee Lundrigan sent letters to school districts

notifying them of the change and has been working to provide parents

with emergency options.

South Carolina initially addressed its paper shortage by limiting the number of death certificates it issued to five per person.

The move put pressure on funeral homes and handicapped their ability

to help families through the difficult process of losing a loved one.

While a five-certificate limit might sound like a lot, Pamela Amos,

general manager at McAlister-Smith Funeral Homes, told The Post and Courier

that most families need at least 10 certified copies of a death

certificate and that the state-sanctioned limits caused “a major issue

for a lot of families.”

The South Carolina Department of Health and Environmental Control –

the agency authorized to issue the certificates – was notified on July 9

Sekuworks had laid off most of its employees and was in the process of

selling its business.

South Carolina, though, lifted its five-copy limit on Aug. 11 after

the state signed a new contract with supplier R.R. Donnelley, Jim

Beasley, a spokesman with the state DHEC, told FoxNews.com. Beasley

indicated the state, unlike California, was able to revise its own

security standards, and in turn use a different kind of paper.

“In 2014, we had already begun the process of revising our

specifications for security paper to be used on birth and death

certificates,” Beasley said. “We had issued a request for proposals from

vendors to meet the new standard. Coincidentally, the bids for a new

provider were scheduled for opening on July 9, 2015, the same day we

were informed of the work situation with Sekuworks.”

The DHEC began processing back-order requests immediately and expects to resume normal operations by Wednesday, he said.

Meanwhile in Minnesota, officials at the state’s Department of Health

are working to establish a new contract with a new vendor. The state is

still about a month away before “everything is in place and a new

supply could start flowing,” Doug Schultz, a spokesman for the Minnesota

DOH, told FoxNews.com. Schultz believes there is enough supply

statewide to meet the demand if offices cut down on duplicates.

“Requests for certificates will continue to be fulfilled, but that

fulfillment may occur at locations people don’t regularly use, through

the U.S. mail or from neighboring county vital records offices,” he

said.

Multiple emails, telephone calls and other attempts by FoxNews.com to reach Sekuworks were not successful.

by James Quinn This doesn’t even take into account the hundreds of thousands

of people in Section 8 housing who are “earning” money under the table

and not reporting it to the IRS. Then there are the additional “tenants”

who pay to live there, which is also not reported. This article is only

the tip of the iceberg. Via Washington Post

A family of four in New York City makes $497,911 a year but pays

$1,574 a month to live in public housing in a three-bedroom apartment

subsidized by taxpayers.

In Los Angeles, a family of five that’s lived in public housing since

1974 made $204,784 last year but paid $1,091 for a four-bedroom

apartment. And a tenant with assets worth $1.6 million — including

stocks, real estate and retirement accounts — last year paid $300 for a

one-bedroom apartment in public housing in Oxford, Neb.

In a new report, the watchdog for the Department of Housing and Urban

Development describes these and more than 25,000 other “over income”

families earning more than the maximum income for government-subsidized

housing as an “egregious” abuse of the system. While the family in New

York with an annual income of almost $500,000 raked in $790,500 in

rental income on its real estate holdings in recent years, more than

300,000 families that really qualify for public housing lingered on

waiting lists, auditors found.

(HUD Office of Inspector General)

But HUD has no plans to kick these families out, because its policy

doesn’t require over-income tenants to leave, the agency’s inspector

general found. In fact, it encourages them to stay in public housing.

“Since regulations and policies did not require housing authorities

to evict over income families or require them to find housing in the

unassisted market, [they] continued to reside in public housing units,”

investigators for Inspector General David Montoya wrote.

The review, conducted in 2014 and 2015 at the request of Rep. Phil

Roe (R-Tenn.), found that 45 percent of the 25,226 public housing

tenants with incomes higher than the threshold to get into the system

were making $10,000 to $70,000 a year more. About 1,200 of them had

exceeded the income limits for nine years or more, and almost 18,000 for

more than a year.

HUD sets the low-income limits at 80 percent and very low-income

limits at 50 percent of the median income for the local area. The agency

sets “fair market rents” every year based on incomes, housing demand

and supply. In Los Angeles, for example, the threshold was $70,450 for a

family of five. In Oxford, Neb., it was $33,500 for an individual.

New York, Puerto Rico and Texas had the most over-income families in

public housing, while Utah, Idaho and Wyoming had the fewest,

investigators found.

(HUD Office of Inspector General)

About 1.1 million families in the country live in public housing. The

over-income tenants represent 2.6 percent of the system. Based on these

numbers, HUD officials said the inspector general was “overemphasizing”

the problem. But the watchdog didn’t buy it.

“Although 25,226 over income families is a small percentage of the

approximate 1.1 million families receiving public housing assistance, we

did not find that HUD and public housing authorities had taken or

planned to take sufficient steps to reduce at least the egregious

examples of over income families in public housing,” the audit said.

“Therefore, it is reasonable to expect the number of over income

families participating in the program to increase over time.”

The watchdog estimated that taxpayers will pay more than $104 million

over the next year to keep these families in public housing, money that

should be used for low-income people.

But under HUD regulations, public housing tenants can stay as long as

they want, no matter how much money they make, as long as they are good

tenants. The agency is only required to consider a tenant’s income when

an individual or family applies for housing, not once they’re in the

system. This is different from the housing choice voucher program that

used to be called Section 8, which gives families subsidies for rentals

in private apartment buildings. That program has an annual income limit;

tenants who go above it get less money.

Tenants can wait years to get into both programs.

(HUD Office of Inspector General)

HUD tweaked its policy on high-earning tenants in 2004, encouraging

the thousands of housing authorities in the system to move families out

of public housing if they earn more than the income limit for their

area. While HUD gives money to the housing authorities, they’re run by

states and local governments.

But the 15 authorities investigators looked at told them they had no

plans to evict these families, because if they did, poverty would

continue to be concentrated in government-subsidized housing. The goal,

they said, was to create diverse, mixed-income communities and allow

tenants who are making good money to serve as role models for others.

HUD officials repeatedly objected to the audit, saying that evicting

over-income families could “negatively affect their employment and

destabilize properties.”

“There are positive social benefits from having families with varying

income levels residing in the same property,” Milan Ozdinec, HUD’s

deputy assistant secretary for public housing and voucher programs,

wrote in a lengthy rebuttal to the inspector general.

“Forcing families to leave public housing could impact their ability

to maintain employment if they are not able to find suitable housing in

the neighborhood,” Ozdinec wrote. “Further, for families with children,

it may be more difficult to find affordable child care, and it may

impact school-age children’s learning if they are forced to change

schools during a school year.”

The watchdog said it didn’t believe that HUD should kick out every

family that earns more than the income threshold. But at the very least,

the agency should create “limits to avoid egregious cases.”

(Susan Madrak) Grayson is really good at getting bipartisan support for his bills, and he says he thinks he can get this one passed:

Shoring up Social Security and Medicare are among the

issues Alan Grayson has said he wants to emphasize as a candidate for

the Democratic U.S. Senate nomination.

Following up on that promise, Grayson has unveiled a proposal that would increase Social Security retirement benefits and tie future increases to a new cost-of-living index.

The Orlando Democrat says that cost-of-living-allowances (COLAs) have

been miscalculated for decades, saying that when they were introduced

in 1975, they’ve been calculated on the cost of living for people who

work. But he says that most people on Social Security are obviously

retired, so the government has been consistently understating the

increase in inflation that seniors face on a year-to-year basis.

Seniors spend twice as much on health care as other people do, he said. “And

the cost of health care has risen much faster than the general costs of

living over the past 40 years, but that isn’t reflected in their

adjustments,” he said. “On the other hand, seniors use less

gasoline than other people do.” He said the cost of gasoline hit an

all-time high in real terms in 1981, and has been falling ever since.

Overall, Grayson said, seniors have been cheated out of more than $300 billion.

The congressman and Senate candidate said he also has another bill on

addressing Social Security solvency that he’ll introduce later this

year.

But he says the short answer to curing any concerns about the

program’s life is to “scrap the cap.” That’s shorthand for eliminating

the current cap on payroll taxes that come out of salaried workers

checks and goes toward the federal retirement benefits program. Right

now, every American is taxed at a 6.2 percent rate, until they reach

$117,000 a year. Then the tax is cut off.

He uses the salary of NBA star LeBron as an example of the inequities with the current system.

“LeBron James makes over $20 million a year, He gets paid to play 82

games a year. He’s done paying his Social Security in the first quarter

of the first game of the year, and for the rest of that game, for the

rest of the next 81 games, he doesn’t have to pay anyting in Social

Security,” he says. “That isn’t really fair. If you scrap the cap, then

Social Security is solvent forever.”

Grayson is confident he can get his soon-to-be officially filed bill through Congress.

“I think they’re actually good,” he said about the prospects of

passage.”We’re talking about being fair to seniors. Seniors can be

Republicans, Democrats, independents.This is not really an

ideological matter in any real sense. It’s a matter of the government

essentially cheating seniors out of large amounts of money, and I think

the Republicans should be just as sensitive of that as the Democrats, that we need to be fair to everybody and keep the promises that we make.”

(News Machete) Did

you know that under certain circumstances, sellers of TV stations had

to pay higher taxes when selling the stations to white people than black

people? It sounds racist (it is racist!), but it is true. Even more

bizarre, liberals want to reinstate it, creating different tax rates based on the color of the skin of the buyer:

Minority owners are burdened by the legacy of racism.

When the U.S. government first started giving away our airwaves in the

1930s, they were distributed exclusively to white, male owners. It

mostly stayed this way until the 1970s, when the FCC tried to remedy the

problem by implementing a “Minority Ownership Policy.” The measure

offered tax incentives to people seeking to sell stations to minority

owners.

In other words, sell to a minority, and you get a lower tax; sell to a

white person, and you get a higher tax. I wonder if the old apartheid

South Africa had race-based taxes as well…or is this just something

liberals here perfected?

The policy worked. Within two years of its passage, the

country went from one black-owned television station to 10. Over its

total 17 year existence, minority ownership increased five-fold. But it

was struck down by the newly-elected Republican Congress in 1995 and

since then, its success has been mostly undone

What business does the Congress have meddling in the private sector,

setting tax rates based on race? What busines is it of Congress to

determine the “appropriate” level of minority ownership of television

stations?

More importantly, what does it mean to have minority ownership of a

television station? Many stations are owned by publicly traded

companies. Was Time Warner “black” when Dick Parsons was in charge but

“white” now that he is gone? When you start trying to classify large

companies by race, you see how ridiculous it becomes.

Last year, in fact, just two television stations were owned by black owners.

And how many were owned by publicly traded companies, or private

companies with a diverse ownership? The WaPo didn’t see fit to report

that. It’s like saying, “Why aren’t more oil companies owned by

blacks? Why isn’t ExxonMobil, the publicly traded company, ‘black'”?

Media consolidation is at the heart of the problem. Clear

Channel, for example, famously wiped out small and minority radio

station owners with its buying spree, which allowed the company to

snatch up as many as seven stations in a single market.

How awful! In a private market, black owners voluntarily sold their stations and made a profit.

Racism is where TV station owners refuse to sell their companies to

minorities when they put them on the market. Racism is also setting tax

rates based on race. But “not enough black owned stations,” by itself,

means about as much as “not enough blacks at the ballet.”

Down nearly 5% right now.

Via: Reuters:

Oil prices fell about 4 percent on Wednesday, with U.S. crude

hitting 6-1/2 year lows and threatening to break below $40, after a huge

unexpected stockpile build in the United States reinforced concerns

about a growing global oil glut.

U.S. crude inventories rose by 2.6 million barrels last week to

456.21 million, the government’s Energy Information Administration said.

The figures stunned energy market analysts on Wall Street, as well as

traders and investors who had been expecting a stockpile drawdown

despite the peak U.S. summer driving season nearing its end and refinery

problems cutting fuel processing capabilities.

(Ambrose Evans-Pritchard)

World shipping has fallen into a deep slump over the late summer,

dashing hopes of a quick recovery from the global trade recession

earlier this year and heightening fears that the six-year economic

expansion may be on its last legs.

Freight rates for container shipping from Asia to Europe fell by over

20pc in the second week of August, even though trade volumes should be

picking up at this time of the year. The Shanghai Containerized Freight

Index (SCFI) for routes to north European ports crashed by 23pc in five

trading days.

The storm in the shipping industry comes as the New York state manufacturing index for

July plummeted to a recessionary low of minus 14.9, the lowest since

the Great Recession and one of the steepest one-month drops ever

recorded.

The new shipments component fell to -13.8, and new orders to -15.7. A

similar drop occurred in 2005 and proved to be a false alarm but the

latest fall comes at a delicate moment for the world economy.

There is now a full-blown August storm sweeping through global

markets. The Bloomberg commodity index dropped to a fresh 13-year low on

Monday and the MSCI index of emerging market equities touched depths

not seen since August 2009.

A closely-watched gauge of emerging market currencies has fallen for

the eighth week – the longest run of unbroken declines since the

beginning of the century – led by the Malaysian Ringgit, the Russian

rouble and the Turkish lira. Asian currencies have dropped against the dollar over the last year

China’s surprise devaluation last week continues to send after-shocks

through skittish global markets, already on edge over a likely rate

rise by the US Federal Reserve in September – though this is now in

doubt.

The currency move was widely taken as a warning that the Chinese

economy is in deeper trouble than admitted so far, a menacing prospect

for exporters of raw materials and for trade competitors in Asia. It

threatens to transmit a fresh deflationary impulse through the global

system.

The great worry is that companies in emerging markets will struggle

to service $4.5 trillion of US dollar debt taken out in the boom years

when quantitative easing by the Fed flooded the world with cheap money,

much of it at irresistible real rates of 1pc. This is up from $1

trillion in 2002.

The monetary cycle has gone into reverse since the Fed ended QE in

October 2014 and cut off the flow of fresh liquidity. While the first

rate rise in eight years has been well-telegraphed, nobody knows for

sure what will happen once tightening starts in earnest.

This stress-test could prove even more painful if China really has

abandoned its (crawling) dollar peg and is seeking to protect export

margins by driving down its currency.

The yuan has risen by 60pc against the Japanese yen and 105pc against

the rouble since mid-2012. Yet China nevertheless has a trade surplus

of 6pc of GDP.

Data from the Port of Hamburg

released on Monday show much damage this currency surge may be doing to

Chinese companies. Axel Mattern, the port’s chief executive, said a

10.9pc drop in trade with China was the chief reason why volumes of

container cargoes passing through the port fell 6.8pc in the first six

months.

“During the first six months of the years the euro was on average 19

percent lower than the yuan, making purchase of Chinese goods costlier

for European importers,” he said.

If so, this is grist to the mill of those arguing that China timed

its switch to a market-driven exchange rate in order to disguise what is

really “currency warfare”, or a beggar-thy-neighbour strategy as it

used to be known. The Chinese central bank has dismissed such claims as

“nonsense”. It has intervened to stabilize the yuan over the last three

days.

The port of Hamburg said trade with Russia collapsed by 36pc, the

latest evidence that the rouble crash and deepening recession has forced

Russian consumers to cut back drastically on purchases of imported cars

and heavy goods.

The Dutch CPB index of world trade fell in both April and May in

absolute terms, culminating five months of dire shipping activity. It

had been widely-assumed that the worst was over. World trade has slumped

Yet more recent data from Container Trades Statistics shows that

global volumes fell 3.1pc in June from the already depressed levels the

month before. This has come as shock: the period from June to August is

typically the strongest time of the year, boosted by pre-shipments for

the Christmas season.

What is even more disturbing is that fresh port data from Asia

suggest that the downturn dragged on into July, and may even have

deteriorated.

Singapore – the world’s second largest entrepot – saw a 13.3pc

contraction in container volumes from a year earlier, the worst

performance since the sudden-stop in trade after the Lehman crisis.

The growth in cargo shipments for all the major ports in East Asia

(that have reported so far) fell to a new cycle-low of 0.6pc in July,

according to tracking data collected by Nomura. “The clock is ticking on

the third quarter. We remain sceptical of those trying to “call a

bottom”,” it said.

It is still unclear how much of this weakness reflects recessionary

conditions, and how much stems from a more benign shift in the structure

of the global economy.

China’s reliance on imported components for its export industry has

fallen to 35pc from 75pc in 1992 as the country moves up the technology

ladder. The Communist Party is deliberately weaning the economy off

heavy industry and mass production, shifting to a more mature service

economy that relies less of trade.

At the same time, the US and Europe have been “re-shoring”

manufacturing plant from China as Asian labour costs rise, reversing the

process of globalisation.

These changes mean that the “trade-intensity” of the global economy

is falling. The trade share of world GDP was 40pc in 1990. It rose to a

peak of 61pc in 2011, and has since drifted down to below 60pc.

A recent study

by the International Monetary Fund said the expansion of global supply

chains driven by the US and China in the early 2000s is “exhausted”.

The implication is that trade is no longer the pulse of the global economy. Other indicators are less worrying.

Both credit and key measures of the money supply are rising briskly

in Europe, the US, and latterly in China as well, pointing to a recovery

later this year. These forces may prove to be more powerful in the end.

`

(CALIFORNIA)

A Pacific Northwest grocery chain that recently acquired two Coachella

Valley stores is closing 27 locations, including 16 in California.

Haggen called the move an effort “to continue to improve its business and strengthen its competitive position.”

Neither of Haggen’s Coachella Valley locations will be impacted at this time.

In December, Haggen took over the Vons location in Palm Desert on

Highway 111, and the Pavillions on Bob Hope Drive in Rancho Mirage.

In a news release,

a Haggen representative said most of the stores being closed or sold

had been acquired as part of a divestment deal with Albertsons and

Safeway. At that time, Haggen expanded from 18 stores to 146, and

increased its workforce from 2,000 to 10,000.

More stores could close in the future.

“Haggen’s goal going forward is to ensure a stable, healthy company

that will benefit our customers, associates, vendors, creditors,

stakeholders as well as the communities we serve,” said Haggen CEO

Pacific Southwest, Bill Shaner. “By making the tough choice to close and

sell some stores, we will be able to invest in stores that have the

potential to thrive under the Haggen banner.”

Stores slated to close: Arizona

Tucson – 10380 E Broadway Blvd.

Tucson – 8740 E. Broadway

Anthem – W. Anthem Way

Flagstaff – E. Route 66

Prescott Valley – E. Hwy. 69 California

Newbury Park – Newbury Rd.

Los Osos – Los Osos Valley Rd.

Simi Valley – Cochran St.

Simi Valley – Madera, 660 E. Los Angeles Ave.

Bakersfield – E. Stockdale Hwy.

Santa Clarita – McBean Pkwy.

Irvine – Portola Pkwy.

Mission Viejo – Los Alisos Blvd.

Tustin – 17th Street

San Marcos – Rancho Santa Fe

El Cajon – Fletcher Pkwy.

La Mesa – Lake Murray Blvd.

Chula Vista – Telegraph Canyon Rd.

Chula Vista – Third Ave.

San Ysidro – W. San Ysidro Blvd. Oregon

Tualatin – SW Tualatin-Sherwood Rd

Klamath Falls — North 8th St.

Klamath Falls – South 6th St

Grants Pass – NE Beacon Dr.

Keizer – River Road North Washington

Spanaway – Pacific Ave. S.

Jennifer Larino)

Layoffs are starting to hit New Orleans as Royal Dutch Shell moves

forward with plans to eliminate 6,500 jobs worldwide. The cuts come as

Shell seeks to cut costs amid lower oil and gas prices.

Shell spokeswoman Kimberly Windon confirmed in an email the company

has started to cut jobs at its New Orleans and Houston offices, though

it is not providing a “specific breakdown of workforce numbers.”

About 2,300 Shell employees and contractors are at One Shell Square

on Poydras Street, and the majority support Shell’s drilling and

exploration operations in the deepwater Gulf of Mexico. Windon said the

deepwater segment “continues to be an important part of the Shell global

portfolio.”

“We had to make some difficult decisions in an effort to reduce costs

while seeking opportunities to improve efficiencies and ensure

long-term competitiveness and profitability,” Windon said.

According to sources at One Shell Square, employees and contractors

in New Orleans were told earlier this month that Shell plans a 30

percent cut to its local workforce by November. The sources asked not to

be named out of concern for their jobs.

Sources said Shell has started to offer severance packages to senior workers.

Windon said the New Orleans cuts are “part of a global reduction”

and, as such, the company is not disclosing workforce numbers specific

to each market.

Royal Dutch Shell, based in Holland, said July 30 it would cut its

capital investment and reduce its global workforce by 6,500 positions as

falling oil prices continue to undercut profit. Shell employs about

94,000 worldwide.

Shell reported $3.8 billion in second quarter earnings, down from $6.1 billion during the same period in 2014.

Oil prices reached $40.77 per barrel in futures trading Wednesday

morning — their lowest level since March 2009 and down from $92 a year

ago. Read the full email statement from Shell spokeswoman Kimberly Windon.

We live in some kind of fractal economy in which everything is connected and no one knows, how this macroeconomy

is working. This fiat currency miracle is working some how. It’s fake

and illusion and its working. I expected crash 2 years ago and bubble is

just expanding since then.

But anyways – we need new Breton woods. We need new currency for new

millenium. Now we live in a world, when dollar empire is slowly

disintegrating. Bretton woods put all the power into hands of few, who

control the most powerful currency of all times – dollar. And now, when

dollar is dying, its masters don’t want to let all that power out of

their hand.

And as wounded beast is most bloodthirsty, world is drowning in

blood… Only collapse of dollar can stop this madness, but there will be a

lot of blood…

Weekly Commentary: China

…The “currency war” issue garnered deserved attention this week. With

currency markets in disarray and disinflationary pressures mounting

globally, increasingly desperate central bank measures attempt to spur

inflation. “Enrich thy neighbor” – Ben Bernanke’s answer to

“beggar thy neighbor” concerns – sounds even more ridiculous these days.

Asian currencies were under intense pressure this week. Perhaps it’s

related to fears of a cycle of competitive devaluations. Mainly,

I believe it is part of an intensifying exodus of “hot money” from a

region especially vulnerable to financial contagion, instability and

even calamity. And the more currencies weaken the more unmanageable the

debt loads. Chinese devaluation only stokes this fire.

This week’s 2.8% currency decline (vs. the dollar) offers little

relief to Chinese manufactures. And while I do believe the Chinese

economic downturn has gained important (post-stock market Bubble)

momentum, I don’t see economic weakness as the driving force behind this

week’s policy move. Chinese officials are alarmed about a sudden Credit

slowdown and the risk of a self-reinforcing deflationary dynamic. The

Chinese are fearful of their increasingly fragile Credit system.

Currency pegs are dangerously seductive. The longer they remain in

place the more advantageous they appear. They are pro-“hot money” flows.

Over time they become increasingly pro-leverage and speculation. They

are pro-Bubble – which means pro-tantalizing boom. In the end, currency

peg regimes ensure precarious financial and economic imbalances. And,

repeatedly, derivatives markets have become the epicenter of boom and

bust dynamics. Peg the two most important global currencies together,

adopt flawed policies, let Bubbles run loose, promote historic

expansions of “money” and Credit – and you’re asking for trouble.

Most view the Chinese currency as fundamentally strong. Surely

Chinese policymakers see it this way. After all, China has a colossal

export sector. The People’s Bank of China is sitting on an unmatched

$3.7 TN hoard of international reserves. But is the currency sound? What

are intermediate to longer-term prospects? How fragile is the Chinese

Credit system? How much central government debt and monetization will be

employed to counter a Credit and economic bust?

… http://creditbubblebulletin.blogspot.com/2015/08/weekly-commentary-china.html

Bad Moon rising: Americans bracing for September shocker

Across the vast expanse of the

internet, everyone from professional economists to armchair theorists

are sounding the alarm that next month may hold some ugly surprises for

the global economy.

Despite exorbitant executive salaries, record earnings on Wall Street

and a surging dollar, an increasing number of forecasters are warning

the feel-good data is severely skewered – a bit like a new coat of paint

that used-car dealerships use to conceal the fact that a car’s engine

is shot. Indeed, many experts are giving the rickety US-made jalopy just

months before the big collapse begins.

Gerald Celente, the founder of Trends Research, who predicted the

“panic of 2008,” says the economic earthquake will send reverberations around the world. “You’re going to see a global stock market crash,” Celente told King World News. “There’s going to be panic on the streets from Wall Street to Shanghai, to the UK down to Brazil.” “You’re going to see one market after another begin to collapse.”

Doug Casey, a successful investor and the head of Casey Research, saw little to be upbeat about in the current economic climate.

“With these stupid governments printing trillions and trillions of

new currency units,” Casey, describing the US Federal Reserve’s

quantitative easing program, told Reason magazine in a recent interview, “it’s building up to a catastrophe of historic proportions.”

And he certainly does not advise keeping much money in any financial institution. “Most of the banks in the world are bankrupt,” he said.

In a recent conversation between senior analyst Larry Edelson and

Mike Burnick, the Research Director for Weiss Research, Edelson made a

stunning prediction, even providing an exact date for what he predicts will be a “rollercoaster ride through hell.” “On October 7, 2015, the first economic super cycle since 1929

will trigger a global financial crisis of epic proportions. It will

bring Europe, Japan and the United States to their knees, sending nearly

one billion human beings on a roller-coaster ride through hell for the

next five years. A ride like no generation has ever seen. I am 100

percent confident it will hit within the next few months.”

And there are dozens of other such apocalyptic predictions on the

health of the global economy that it leaves one feeling dizzy and

desperate – something like watching an approaching tidal wave in the

full knowledge there is no hope of outrunning it.

Meanwhile, confidence in the US economy among Americans dropped

sharply in July to its lowest level in 2015, according to a new US

Economic Confidence Index rating released by Gallup earlier this month.

Perhaps the non-stop onslaught of super-negative news – everything

from the Greek tragedy to the Chinese currency devaluation – has got

Americans convinced the global economy has entered dangerous waters.

Indeed, scratch the shiny surface of the US economy and the wear and

rust is immediately apparent.

Jeff Berwick, Canadian entrepreneur and editor of The Dollar Vigilante, recently told Gordon T. Long in an interview:“There’s enough going on in September to have me incredibly curious and concerned about what’s going to happen.” http://www.rt.com/op-edge/312576-september-economy-crash-eclipse/ Hedge fund billionaire Stan Druckenmiller has made a huge bet on gold

Legendary hedge fund manager Stanley Druckenmiller, who runs Duquesne

Capital, made a huge bet on gold during the second quarter.

Duquesne, which is now run as a family office, finished the second

quarter with 2.88 million shares of SPDR Gold Trust, according to the

fund’s 13F filing.

The new position is now Druckenmiller’s largest long position.

Druckenmiller’s GLD stake had a value of $300.3 million at the end of the quarter based on the June 30 closing share price of $104.27. Shares of GLD have fallen 5.5% since then.

Druckenmiller has previously said that when he sees something that really excites him he will “bet the ranch on it.” We reached out to Druckenmiller for comment on his GLD position.

Druckenmiller also increased his position in Facebook to 1,872,700 shares, up from 252,000 shares in the first quarter.

He also took big new positions in Freeport-McMoRan (3.547 million

shares), Halliburton (1.547 million shares), and Wells Fargo (1,679,400

shares), the filing shows.

Read more: http://www.businessinsider.com/druckenmiller-buys-gld-shares-2015-8#ixzz3j7cZbruf

As markets await the release of the minutes for the July Federal Open

Market Committee (FOMC) meeting, Kitco’s global trading director Peter

Hug tells Kitco News he doesn’t expect the central bank to make a move

on rates in September. “I’ve been in the camp that the Fed may not move

until 2016,” he says. “I’m sort of begging Yellen to raise the rate in

September and get it out of the way. She’s got herself in a corner.”

Looking at gold, Hug seems optimistic about the metal, stating that he’s

’surprised’ with the current consolidation levels. “Every time gold

tries to break down below $1,110 there seems to be buying interest. So I

am constructive gold at these levels.” Hug shares the same sentiment

towards silver, although he adds that it may be a little riskier right

now. “Silver is still tentatively a bit of a risk here but at a 75:1

ratio…I think silver is a good buy at the 14.80 level.” Tune in now to

find out where he sees the gold and silver prices headed for the rest of

August. Kitco News, August 19, 2015.

by Dana Lyons

You may hear the term “decouple” bandied about in investment circles

when discussing global markets. It simply refers to one market’s ability

to move irrespective of other global markets. In recent years, unlike

emerging markets, developed markets have tended to move more or less in a

correlated fashion, i.e. they have not decoupled. This has been

especially true this year as emerging markets have had a rough go of it

while most developed markets have hung in pretty well, even if they

haven’t made much headway.

One subtle change in this dynamic occurred last week. Most developed

markets have weathered the recent volatility without breaking any key

support levels. The Australian stock market is an exception, however,

having now broken, er, down under a key support area.

Specifically, the broad Australian All Ordinaries Index broke below

the 5440 area which was marked by several key analyses including:

The 23.6% Fibonacci Retracement of the 2011-2015 Rally ~5459

The 38.2% Fibonacci Retracement of the 2013-2015 Rally ~5447

The 61.8% Fibonacci Retracement of the 2014-2015 Rally ~5443

The Post-2012 UP Trendline

For the All Ordinaries Index, this 5440 level now becomes resistance

that should pose a hurdle to any bounce attempt. Meanwhile, it opens up

immediate downside of about 5% down to the 5120-5150 level. While that

isn’t a substantial amount of risk, there may be a bigger message to the

price violation.

Given the lack of decoupling – again, most developed markets have

been highly correlated – an expectation has developed that these markets

will trade in lockstep. Therefore, with the rest of the developed world

exhibiting impressive resilience, the possibility of any type of

meaningful price breakdown has been considered remote. Perhaps this

breakdown in the Australian market at least cracks the door open a bit

more to that possibility.

Certainly the dynamics of the Australian market, e.g., heavily

influenced by commodities and China, render it unique among the

developed world. Thus, it is possible that it truly has decoupled and

that the recent price breakdown is simply a one-off. Then again, perhaps

it is a warning that the major global indices are not as bullet-proof

as they are thought to be.

KIEV, August 19. /TASS/. In the

framework of aid to Poland, the power engineering sector of which has

been hit by an anomalous heatwave, Ukraine will sell electricity to that

country at 7.5 eurocents per 1 kwh, the National Commission for Energy

and Utilities said on Wednesday.

Operators of Polish and Ukrainian power grids signed an agreement on

August 17 on supplies of electricity to Poland. The national operator of

power grids, Ukrenergo, says the maximum size of Poland’s emergency

need for electricity is 235 megawatts.

Experts say 7.5 eurocents per 1 kwh is high enough a price. It stands

in a marked contrast to the 3.68 eurocents per 1 kwh, which the

Minister of Energy and Coalmines Vladimir Demchishin named to TASS

somewhat earlier as the price of purchasing electric power from Russia.

Exports of Ukrainian electricity to Russia from January through to

June 2015 totaled 0.8 million kwh, while in the same period of last year

no such exports took place.

At the same time, Ukraine imported 1.393 billion kwh of electricity

from Russia. The exports in June alone totaled 2.8 million kwh.

The "one-off" adjustment has now reached its 3rd day as The PBOC has now devalued the Yuan fix by 4.65% back to July 2011 lows. The PBOC seeks to reassure...

*CHINA PBOC SAYS YUAN REMAINS STRONG CURRENCY IN LONG-TERM

*PBOC SAYS THERE IS DEMAND FOR DEVALUATION OF YUAN VS USD

*PBOC CHANGE OF YUAN MECHANISM RELATED TO JULY CREDIT: ZHANG

*PBOC SAYS YUAN CHANGE IS BENEFICIAL TO LONG TERM STABILITY

*PBOC SAYS YUAN EXCHANGE RATE ADJUSTMENT ALMOST COMPLETED

*YUAN RATE ADJUSTMENT POSITIVE TO CONFIDENCE IN YUAN: PBOC'S YI

*NEW YUAN MECHANISM `POSITIVE' TO INTERNATIONALIZATION: PBOC YI

*PBOC SAYS NO BASIS FOR YUAN'S CONSTANT DEVALUATION: ZHANG

Even before this evening's date with debasement history, Japan felt

the need to step up the currency war rhetoric. Following disappointing

Machine Orders data, Abe advisors Hamada warned that "Japan can offset Yuan devaluation by monetary easing," and so the race to the bottom escalates. China has its own problems as BofAML's leading economic indicator showed "the foundation for a growth recovery is not solid, facing more downward pressure,"

and while confusion reigns over why The PBOC would intervene at the

close to strengthen the Yuan last night, the reality is the commitment

isn’t to a devaluation for China’s exports, but undoubtedly its actions are directed toward trying to keep the wholesale finance interfaces somewhat orderly. Finally, China’s devaluation couldn’t come at a worse time for Argentina

- about a quarter of the country’s $33.7 billion of foreign reserves

are now denominated in yuan, which suffered its biggest loss since 1994

on Tuesday. Having devalued the (onshore) Yuan fix by 3.5% in the last 2 days, China did it again... shifting Yuan to 4 year lows

*CHINA SETS YUAN REFERENCE RATE AT 6.4010 AGAINST U.S. DOLLAR

Offshore Yuan dropped back to 6.50...

And China Stocks have opened lower...

*CHINA'S CSI 300 STOCK-INDEX FUTURES FALL 1% TO 3,975.2

S&P Futures are fading...

Some more liquidity needed...

*PBOC TO INJECT 40B YUAN WITH 7-DAY REVERSE REPOS: TRADER

And sure enough, not be outdone, Japan threatens to re-escalate the currency war...

*ABE ADVISER HAMADA SAYS CHINA'S FX MOVE WILL TEND TO BOOST YEN

*HAMADA: JAPAN CAN OFFSET YUAN DEVALUATION BY MONETARY EASING

*HAMADA:BOJ MAY EASE IF CHINA MOVE HITS EXTERNAL DEMAND TOO MUCH

But China has it's own problems, as BofAML notes,

China LEAP (leading economic activity pulse) fell to-3.9% YoY in July

from -2.6% in June, as five of the seven LEAP components weakened.

Similarly, other macro activity data released in July worsened from a surprisingly strong June and disappointed the market. It suggests the foundation for a growth recovery is not solid, and economic growth faces more downward pressure as financial sector activity has slowed after the recent stock market slump.

On the demand side, housing starts further declined

to 16.4% yoy in July after dropping 14.3% in June. We think destocking

could still be ongoing in tier 3-4 cities and the housing market

recovery has yet to drive acceleration in housing starts. Auto sales

growth slumped to -7.1% YoY from -2.3%, likely due to weakening consumer

demand for some big-ticket items amid stock market turmoil while staple

good sales remained resilient.

Production-side components were mixed, with weaker

power and steel output growth but slightly better cement output growth.

Power and steel output growth was particularly poor in July, likely due

to plummet in commodity and raw material prices on a bearish growth

outlook amid stock market turmoil.

Medium- to long-term loan growth edged down by 0.8pp, but if taking into account local government debt swap, the decline would be 0.3pp instead.

* * * The fallout from China's decision is going global...

China’s devaluation couldn’t come at a worse time for Argentina.

About a quarter of the country’s $33.7 billion of foreign reserves are now denominated in yuan, which suffered its biggest loss since 1994 on Tuesday.

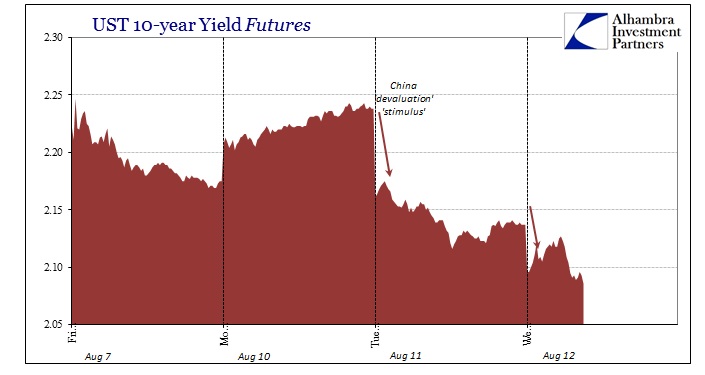

* * * And finally, here is Jeffrey Snider of Alhambra Investment Partners discussing the other reality of what is occurring in China

- as opposed to the paint-by-numbers version spun on TV - explaining

why the PBOC would seemingly “allow” devaluation one day and then act

against it the very next. They are just trying to hold on for dear life, managing imbalances that are beyond their grasp.

While

everyone remains sure that the PBOC is actively trying to “allow” the

yuan to depreciate as some kind of export catalyst, the “dollar”

continues to show (not suggest) otherwise. Liquidity and “dollar” markets are still roiled rather than soothed, especially

the US treasury market where the bid right at the open (what look very

much like continued collateral calls) pushes more like a combination of

October 15 and January 15.

As if to underscore the runaway nature, the PBOC apparently intervened against this “devaluation” just last night. From the Wall Street Journal:

Tuesday, the People’s Bank of China surprised global markets with

what looked like a win-win currency depreciation for the

country—appearing to cede more control of its exchange rate to market

forces, which the International Monetary Fund and others have long urged

it to do, while also helping Chinese exporters.

Its intervention only one day later raised questions about its

commitment to an exchange rate driven more by supply and demand and less

by government direction.

The Journal’s confusion here is demonstrated by what is a mistaken

assumption in the first paragraph leading to the mystery of the second. The

PBOC’s commitment isn’t to a devaluation for China’s exports, but

undoubtedly its actions are directed toward trying to keep the wholesale

finance interfaces somewhat orderly. When the

yuan was trading exactly sideways for nearly five months, that was the

same setup; the PBOC was keeping the yuan stable so that it wouldn’t devalue and thus signal the depth of the “dollar” financing strain.

That is the problem orthodox commentary and theory has with wholesale finance, they just don’t get it.

Devaluation of currency doesn’t mean that in this context just as a

“strong dollar” isn’t anything like the term. Both are forms of internal

disruption, the direction of that is just an expression of what manner

of wholesale finance is becoming most unruly. Credit-based “money”

systems do not operate like the currency systems from before 1971.

Floating currencies aren’t really that, so much as they are just another

form of traded liabilities in global banking.

The Chinese have a “dollar” problem just the same as the Swiss, Brazilians and the rest (including the dollar). There is a global retreat in eurodollar funding that is wreaking havoc, expectedly, globally. And

in China that is particularly true as the Chinese banks through

external corporates joined the “dollar short” several years back. Joined

now under PBOC “reform”, there has been an almost hostility if not at

least disfavor over the “dollar” intrusion as it has been taken as one

primary element of the bubbles (what mainstream mistakes for “hot

money”). As a result, the PBOC has been almost chasing “dollars” out of

the system in an attempted orderly purge.

That led to what looked like historic “outflows” in 2015 as “dollar”

conditions for the Chinese “short”, so it is absolutely no surprise to

see this occurring now. The only mystery has been, as I have been

writing for some time, what the PBOC was doing to counteract it during

those five months. That would tell us both how serious the turmoil was

and how ineffective whatever intervention would ultimately be.

From July 22:

The yuan has suddenly, right at the March FOMC meeting, gone limp.

Trading has been confined, except for very brief, intraday outbursts, to

an increasingly narrow range. Given its behavior particularly as a full

part of the reform agenda to that point, this amounts to what can only

be hidden and inorganic factors. Whether that means PBOC intervention is

unclear, though suggested by even TIC, but this is the most important

and unexplained dynamic in the “dollar” world at present.

Perhaps the June TIC updates will help shed some light on what has

been going on with China’s “dollar short”, but I doubt it. The nature

and especially the scale of what might be happening in the money markets

has global implications, and may (conjecture on my part) start to

explain the reversal in the Chinese stock bubble and ultimately even

relate to the “dollar’s” renewed disruption in July so far.

Earlier July 8:

It’s not enough to notice how this [zero yuan volatility] is odd, as

it appears, given wider circumstances, to be almost odd with a purpose.

Whenever uncertainties grew about China’s reform, especially “allowing”

defaults, “dollar” supplies tightened significantly and the yuan

devalued. Given the fragility of the current situation, you can

understand why, possibly, the PBOC might not want too much to get so far

out of hand and so they may be supplying “dollars” to maintain orderly

money markets both onshore and off. Given the plunge in import activity

they may not really need to supply all that much, particularly in

combination with prior and intended outflows as they effectively tried

to chase speculators out of the country. Perhaps they did too much?

Whatever the case may ultimately be, it bears close scrutiny for

several reasons. First, if this is correct (a very big “if”) then the financial system in China is worse, far worse, than it appears.

Second, central bank attempts such as this are extremely finite as they

are, over time, hugely inefficient. The PBOC might just be throwing

everything in its arsenal at the financial system short of open “flood”

declarations (which are themselves destabilizing; declaring an open

emergency is as much confirmation of how bad everything is) trying to

calm everything down in order to reassess. [emphasis added]

That is why the PBOC would seemingly “allow” devaluation one

day and then act against it the very next. They are just trying to hold

on for dear life, managing imbalances that are beyond their grasp. That

is what occurred last night, as the Wall Street Journal confirms that

Chinese banks were “selling” dollars on the PBOC’s behalf; which is, in

the wholesale context, supplying “dollars.” The currency

translation is just the recognition of that imbalance, which is in many

forms like this kind of convertibility almost a “run.”

The PBOC then instructed state-owned Chinese banks to sell dollars on

its behalf in the last 15 minutes of Wednesday’s trading, according to

people close to the state banks.

The central bank took it as far as it could and then the

“dollar” dam just burst on really bad economic data that was expected

instead to confirm the bottom. At this point, it looks like

they are left only to try to mitigate the damage they had been for five

months hoping would never occur as the global economy was supposed to

have healed on its own long before then (which was nothing more than

FOMC and orthodox pipe dreams).

Another central bank has fallen prey to the decomposing “dollar”, as the global tremors of such central bank upsets ripple further and further.

KIEV, August 19. /TASS/. In the

framework of aid to Poland, the power engineering sector of which has

been hit by an anomalous heatwave, Ukraine will sell electricity to that

country at 7.5 eurocents per 1 kwh, the National Commission for Energy

and Utilities said on Wednesday.

KIEV, August 19. /TASS/. In the

framework of aid to Poland, the power engineering sector of which has

been hit by an anomalous heatwave, Ukraine will sell electricity to that

country at 7.5 eurocents per 1 kwh, the National Commission for Energy

and Utilities said on Wednesday.