Friday, July 15, 2016

The FED Repeats 2008, The Economy Is Fine Nothing To Worry About, Believe Us

1 in 3 Americans have less than $500 in their accounts, it’s less in Europe. NY real estate market is declining rapidly and it is spreading to many areas. Fed says helicopter money might be on its way here in the US. Fed reports that the economy is doing well, nothing to worry about.

Pennsylvania approves $1.3bn bailout

Pennsylvania lawmakers have approved a financial bailout after a yearlong stalemate over the state’s beleaguered budget. The $1.3 billion revenue package marks the highest election-year tax increase in the state’s recent history.

The grueling debate over the Pennsylvania’s deficit-ridden budget has

finally come to a close – for now. The $1.3 billion bailout package is a

hodgepodge of tax increases, loans from the state’s medical malpractice

insurance fund and new taxes on smokeless tobacco and electronic

cigarettes. This makes Pennsylvania the last state to impose taxes on

vaping and electronic cigarette products, the News & Observer reported.

The bailout package was necessary after a $31.5 billion spending plan was approved by the Republican-controlled legislature in June. However, it was the second revenue plan to be pitched by Pennsylvania Governor Tom Wolf (D), who initially pushed for a $2.7 billion tax package. The state’s House and Senate Republicans have historically been averse to tax increases.

Wolf’s previous spending plans for the 2015-2016 fiscal year created a budgetary stalemate between his administration and the Pennsylvania General Assembly.

While Wolf initially sought to use the $2.7 billion package to loosen charter school enrollment caps, to begin closing the disparities between the poor and wealthy school districts, this part of the deal was dropped in favor of increased taxes.

The plan uses a fusion of one-time fixes to help the budget, such as borrowing $200 million from the state medical malpractice insurance fund, along with a tax-amnesty program, extending the sales tax to digital downloads, as well as tax increases on both cigarette packs and wholesale taxes on smokeless tobacco products and electronic cigarettes.

The legislature had previously approved supermarkets and other private retailers for wine sales to generate more money from the state’s liquor laws. The House is also backing the legalization of online gaming in order to collect money from licensing fees.

The House approved the bill in a 116-75 vote, and the Senate did so with a 28-22 vote, while conservative lawmakers resisted approving tax increases.

The budget may symbolize true bipartisanship, because, as they say, a good compromise is when both sides feel like they lost.

“It’s become very clear to me that while this revenue package is not the best, it is the best Harrisburg can do, at least today,” Rep. Madeleine Dean (D-Montgomery) told the News & Observer, adding: “And the alternative, not to do our job, is unacceptable to me.”

Via RT. This piece was reprinted by RINF Alternative News with permission or license.

The bailout package was necessary after a $31.5 billion spending plan was approved by the Republican-controlled legislature in June. However, it was the second revenue plan to be pitched by Pennsylvania Governor Tom Wolf (D), who initially pushed for a $2.7 billion tax package. The state’s House and Senate Republicans have historically been averse to tax increases.

Wolf’s previous spending plans for the 2015-2016 fiscal year created a budgetary stalemate between his administration and the Pennsylvania General Assembly.

While Wolf initially sought to use the $2.7 billion package to loosen charter school enrollment caps, to begin closing the disparities between the poor and wealthy school districts, this part of the deal was dropped in favor of increased taxes.

The plan uses a fusion of one-time fixes to help the budget, such as borrowing $200 million from the state medical malpractice insurance fund, along with a tax-amnesty program, extending the sales tax to digital downloads, as well as tax increases on both cigarette packs and wholesale taxes on smokeless tobacco products and electronic cigarettes.

The legislature had previously approved supermarkets and other private retailers for wine sales to generate more money from the state’s liquor laws. The House is also backing the legalization of online gaming in order to collect money from licensing fees.

The House approved the bill in a 116-75 vote, and the Senate did so with a 28-22 vote, while conservative lawmakers resisted approving tax increases.

The budget may symbolize true bipartisanship, because, as they say, a good compromise is when both sides feel like they lost.

“It’s become very clear to me that while this revenue package is not the best, it is the best Harrisburg can do, at least today,” Rep. Madeleine Dean (D-Montgomery) told the News & Observer, adding: “And the alternative, not to do our job, is unacceptable to me.”

We are in the midst of a sickening crisis created by appalling incentives, driven by sociopathic corporate and political leadership captured by their greedy desire for power wealth and control. The sickness is pervasive and terminal.

by James Quinn

The stock market has reached new all-time highs this week, just two weeks after plunging over the BREXIT result. The bulls are exuberant as they dance on the graves of short-sellers and the purveyors of doom. This is surely proof all is well in the country and the complaints of the lowly peasants are just background noise. Record highs for the stock market must mean the economy is strong, consumers are confident, and the future is bright.

All the troubles documented by myself and all the other so called “doomers” must have dissipated under the avalanche of central banker liquidity. Printing fiat and layering more unpayable debt on top of old unpayable debt really was the solution to all our problems. I’m so relieved. I think I’ll put my life savings into Amazon and Twitter stock now that the all clear signal has been given.

As Benjamin Graham, a wise man who would be scorned and ridiculed by today’s Ivy League educated Wall Street HFT scum, sagely noted many decades ago:

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

Short-term traders can make immediate profits using momentum techniques, following the herd, and picking up pennies in front of a steamroller. Remember your brother-in-law who was getting rich day trading stocks in 1999? Remember your cousin who was getting rich flipping houses in 2005? Remember The Big Short, where the Too Big To Trust Wall Street banks were getting rich creating fraudulent mortgage derivatives and selling them to suckers? There are always profits to be made for awhile. Then the bottom drops out, because fundamentals, cash flow, valuations, and reality matter in the long run.

Lance Roberts points out some inconvenient facts, and I’ll point out a few more.

“It is worth reminding you, that while the markets are moving higher and pushing new highs currently, it is doing so against a backdrop of weak fundamentals, high valuations, and deteriorating earnings.”

History might not repeat itself, but it certainly rhymes. Late in 2007, as the housing collapse was well under way, the stock market hit all-time highs of 1,575 in October. The bulls were exuberant, even as the greatest housing crash in history was evident to everyone except Bernanke and Paulson. Corporate earnings were falling. Valuations were at levels only seen in 1929 and 2000. The so called “doomers” like Hussman, Shiller and Schiff were warning of an impending crash. Very few heeded their warning. In retrospect, the economy was already in recession by December 2007 despite economic reports saying otherwise. GDP and other falsified economic indicators were revised negative years after initially being reported as positive. Familiar?

The stock market dropped 20% from the October high by March of 2008, as Bear Stearns collapsed and struck fear into the hearts of the Wall Street sociopaths. But the Fed and their Wall Street puppeteers needed to keep the game going a little longer so they could short their own fraudulent derivative creations and screw over their clients once more. JP Morgan, which was just as insolvent as Bear Stearns, bought them and restored confidence in the ponzi scheme. The market proceeded to soar by 12% over the next two months. All was well!!! Until the bottom fell out in September. By March 2009, the market had fallen 58% from its October 2007 high.

The market topped out in May of 2015 at 2,126. Since then, corporate profits have been in freefall, consumer spending has been in the toilet, GDP has been barely positive, and virtually every economic indicator has been falling. Valuations are now higher than at the 1929, 2000, and 2007 peaks. The median existing home price of $239,700 is 55% higher than the median price in 2012. At the peak of the housing bubble in 2005/2006 the median price to median wage ratio reached 9.5. In 2012 it had fallen to a reasonable level of 5.6. It currently stands at a bubble like level of 8.3.

The market meandered about for the next seven months going nowhere. It then suddenly dropped in January and February, falling 13% from its May 2015 high. This was unacceptable to central bankers around the globe who believe stock market gains are the only factor reflecting the health of our economic system. Maybe it’s because they are only beholden to bankers, oligarchs, corporate chieftains, corrupt politicians, and unaccountable bureaucrats. Central bankers from around the world have come to the rescue by buying stocks and providing unlimited liquidity to banks and corporations so they can buyback their own stocks. The result, is new record highs.

It has the feel of JP Morgan “rescuing” Bear Stearns and saving the world in early 2008. Smoke, mirrors, negative interest rates, debt creation, money printing and the artificial elevation of stock valuations by central bankers and their politician co-conspirators is not creating wealth. It is creating epic bubbles in stock markets, bond markets, home real estate markets, commercial real estate markets, and automobile markets. John Hussman chimes in with a reality based assessment of their reckless actions:

“Instead, central bankers seem to view elevated security valuations as “wealth.” The longer this fallacy persists, the worse the subsequent fallout will be. I have little doubt that future generations will look at the reckless arrogance of today’s central bankers no differently than we view speculators in the South Sea Bubble and the Dutch Tulip-mania. Unfortunately, there is no mechanism by which historically-informed pleas of “no, stop, don’t!” will penetrate their dogmatic conceit. Nor can we change the psychology of investors.”

Today is just a continuation of the bubble blowing policies of the Fed and their central banker cohorts at the ECB and BOJ. These policies are deranged, illogical, and always result in the destruction of real wealth. Promoting financial engineering, while destroying the incentive to save and invest in the real economy has gutted true investment in our country. This is why good paying jobs have disappeared and we are left with the gutted remains of decades of financialization and globalization. As Hussman points out, our real economy has died a long slow death, drowning in debt.

“One of the hallmarks of the bubble period since the late-1990’s is that the growth rate of real U.S. gross domestic investment has slowed to less than one-quarter of the rate it enjoyed in the preceding half-century. Yet because central banks have stomped on the accelerator at every turn, the quantity of outstanding debt has never been higher, and the combined value of corporate equities and debt (“enterprise value”) is now at the highest multiple of corporate gross value-added since the 2000 bubble extreme.”

Artificially boosting stock prices through convoluted liquidity schemes, devious machinations, backroom central banker deals, sending Bernanke to Japan, and helicopter money dropped on Wall Street only, has just exacerbated the wealth inequality permeating the world. The anger over this blatant pillaging by the .1% who rule the world is reflected in the chaos across Europe and the brewing civil war here in the U.S.

As Hussman notes, no wealth is being created because no productive investments are being made. Mega-corporations buying back hundreds of billions of their own stock to enrich their executives is not a productive wealth creating venture. We are in the midst of a sickening crisis created by appalling incentives, driven by sociopathic corporate and political leadership captured by their greedy desire for power wealth and control. The sickness is pervasive and terminal.

“In a healthy economy, savings are channeled to productive investment, and the new securities that are issued in the process are evidence of that transfer. In an unhealthy economy, and particularly one with very large wealth disparities, a large volume of securities may be created, but they are often simply a way of supporting debt-financed consumption. As a result, no productive investment occurs, and no national “wealth” is created. All that occurs is a wealth transfer from savers to dis-savers. Over the past 16 years, U.S. real gross domestic investment has crawled at a growth rate of just 1.0% annually, compared with a growth rate of 4.6% annually over the preceding half-century. There’s your trouble.”

A chart that caught my eye this week, along with dozens of other data points from the real world, reveals the phoniness of the stock market rally and the underlying weakness of this tottering edifice of debt. We are supposedly in the seventh year of an economic recovery. Corporate profits have been at record highs. Interest rates are at record low levels.

The Fed and the FASB have colluded to allow banks and commercial real estate companies to fake their financial statements and pretend their assets are worth more than they are and to pretend rental income from non-existent tenants in their malls and office buildings can cover their debt payments. And somehow delinquencies and charge-offs are soaring by levels seen during the height of the 2008/2009 financial crisis. It seems all those vacant mall storefronts and all those FOR LEASE signs in front of every other commercial building across America are finally coming home to roost.

This faux economic recovery has been driven by debt, with much of it subprime. The shale oil scam was built on high yield debt and false promises. The Wall Street banks reported fake profits for years by relieving their loan loss reserves created in 2009. Now the table has turned.

The three largest banks in the US—Bank of America, JPMorgan Chase, and Wells Fargo—disclosed that the number of delinquent corporate loans increased by 67% in Q1.

The “tremendous” auto recovery which drove sales (I use the term loosely since 31% of sales are actually leases and the rest are financed over an average of 67 months) from 10 million in 2010 to 18 million in 2015 has been completely driven by easy money provided to Wall Street. It’s amazing how many vehicles you can sell by doling out $350 billion in 0% loans and allowing “buyers” to finance 100% of the purchase.

When they started to run out of legitimate suckers who liked being perpetual debt slaves, they used the tried and true method that worked so well with housing in the mid-2000s – loaning money to losers who weren’t capable of repaying them. This Wall Street mindset is driven by the free money provided them by the Fed. You borrow from the Fed at 0%, lend it to deadbeats at 12% for 72 months so they can “buy” that $40,000 Cadillac Escalade and boost the economy. Over 20% of all auto loans are now being made to subprime (aka deadbeat) borrowers. Now the shit is hitting the fan belt.

Financing 100% of overpriced automobiles, extending terms, pretending

you will get repaid, and recording it as a sale is the corporate/banker

method of creating wealth. Auto loan terms between 73 and 84 months

more than doubled between 2010 and 2015. One quarter of all loans

originated in Q3 2015 were between 73 and 84 month terms, compared to

just 10% in Q3 2010. The average new-car loan rose to $29,551 during the

fourth quarter of 2015, up more than 4% over the past year, according

to Experian, one of the three major credit-reporting agencies.

The chickens are coming home to roost for subprime auto lenders and investors, with Fitch Ratings warning delinquencies in subprime car loans had reached a high not seen since October 1996. The number of borrowers who were more than 60 days late on their car bills in February rose 11.6% from the same period a year ago, bringing the delinquency rate to a total 5.16%. Subprime lending always ends in tears. Wall Street is probably betting against these packages of subprime slime while simultaneously selling them to their muppet clients. History rhymes.

These subprime auto loans look positively AAA compared to the hundreds of billions in subprime student loans distributed like candy by Obama and his government minions to artificially lower the unemployment rate and again boost the economy. Student loan delinquencies are already skyrocketing before the $400 billion doled out in the last four years has come due. The official delinquency rate reported by the government of 11% is another falsehood. The delinquency rate is really 17% when loans in deferment and forbearance — for which payments are postponed due to any reason — are included. The taxpayer will eventually foot the bill for at least $400 billion in losses.

![Student Loan Delinquencies are Sky High [Chart]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sccvdUPxZG1Gpf2LRP3M4rHzbpS4R34OimDthUtooF3d5qzixOpWKW5nngGs5Bfb44_Uo7g6FkYlytOTBsbxyqS5Yj8-Pjnoq6N8bZG3HBhe7VCjg839WLmOtKpv7JvbC1s6HAP7s8LNJXhozmfxfsHjp4KOKRO9YdjWYWWRmNCD0xjssa9_xh83TnAQzZ3v98=s0-d)

We’ve been borrowing from the future for the last 16 years because real economic growth was killed by Greenspan, Bernanke, Yellen and the rest of the Fed yahoos. The stock market has returned 60% since the 2007 peak, three times the growth in corporate profits and GDP. The all-time highs in the stock market have been driven by the $3.4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, PE expansion, and ZIRP. The valuation of the median stock is now the highest in history.

For all I know the stock market could continue to rip higher. Madness knows no bounds. The general public is not involved in this madness. They were wiped out twice in the space of eight years. Wall Street and their media mouthpieces have been unable to lure the average Joe back into the casino because the average Joe has been impoverished by Fed policies designed to benefit the .1%. The Wall Street lemming herd has gone mad, but I’m not sure they will recover their senses before they burn the entire demented financial system to the ground. But enjoy the all-time highs while they last.

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.” ? Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds

The stock market has reached new all-time highs this week, just two weeks after plunging over the BREXIT result. The bulls are exuberant as they dance on the graves of short-sellers and the purveyors of doom. This is surely proof all is well in the country and the complaints of the lowly peasants are just background noise. Record highs for the stock market must mean the economy is strong, consumers are confident, and the future is bright.

All the troubles documented by myself and all the other so called “doomers” must have dissipated under the avalanche of central banker liquidity. Printing fiat and layering more unpayable debt on top of old unpayable debt really was the solution to all our problems. I’m so relieved. I think I’ll put my life savings into Amazon and Twitter stock now that the all clear signal has been given.

Technical analysts are giving

the buy signal now that we’ve broken out of a 19 month consolidation

period. Since the entire stock market is driven by HFT supercomputers

and Ivy League MBA geniuses who all use the same algorithm in their

proprietary trading software, the lemming like behavior will likely lead

to even higher prices. Lance Roberts, someone whose opinion I respect,

reluctantly agrees we could see a market melt up:

“Wave 5, “market melt-ups” are the last bastion of hope for the

“always bullish.” Unlike, the previous advances that were backed by

improving earnings and economic growth, the final wave is pure emotion

and speculation based on “hopes” of a quick fundamental recovery to

justify market overvaluations. Such environments have always had rather

disastrous endings and this time, will likely be no different.”As Benjamin Graham, a wise man who would be scorned and ridiculed by today’s Ivy League educated Wall Street HFT scum, sagely noted many decades ago:

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

Short-term traders can make immediate profits using momentum techniques, following the herd, and picking up pennies in front of a steamroller. Remember your brother-in-law who was getting rich day trading stocks in 1999? Remember your cousin who was getting rich flipping houses in 2005? Remember The Big Short, where the Too Big To Trust Wall Street banks were getting rich creating fraudulent mortgage derivatives and selling them to suckers? There are always profits to be made for awhile. Then the bottom drops out, because fundamentals, cash flow, valuations, and reality matter in the long run.

Lance Roberts points out some inconvenient facts, and I’ll point out a few more.

“It is worth reminding you, that while the markets are moving higher and pushing new highs currently, it is doing so against a backdrop of weak fundamentals, high valuations, and deteriorating earnings.”

History might not repeat itself, but it certainly rhymes. Late in 2007, as the housing collapse was well under way, the stock market hit all-time highs of 1,575 in October. The bulls were exuberant, even as the greatest housing crash in history was evident to everyone except Bernanke and Paulson. Corporate earnings were falling. Valuations were at levels only seen in 1929 and 2000. The so called “doomers” like Hussman, Shiller and Schiff were warning of an impending crash. Very few heeded their warning. In retrospect, the economy was already in recession by December 2007 despite economic reports saying otherwise. GDP and other falsified economic indicators were revised negative years after initially being reported as positive. Familiar?

The stock market dropped 20% from the October high by March of 2008, as Bear Stearns collapsed and struck fear into the hearts of the Wall Street sociopaths. But the Fed and their Wall Street puppeteers needed to keep the game going a little longer so they could short their own fraudulent derivative creations and screw over their clients once more. JP Morgan, which was just as insolvent as Bear Stearns, bought them and restored confidence in the ponzi scheme. The market proceeded to soar by 12% over the next two months. All was well!!! Until the bottom fell out in September. By March 2009, the market had fallen 58% from its October 2007 high.

The market topped out in May of 2015 at 2,126. Since then, corporate profits have been in freefall, consumer spending has been in the toilet, GDP has been barely positive, and virtually every economic indicator has been falling. Valuations are now higher than at the 1929, 2000, and 2007 peaks. The median existing home price of $239,700 is 55% higher than the median price in 2012. At the peak of the housing bubble in 2005/2006 the median price to median wage ratio reached 9.5. In 2012 it had fallen to a reasonable level of 5.6. It currently stands at a bubble like level of 8.3.

The market meandered about for the next seven months going nowhere. It then suddenly dropped in January and February, falling 13% from its May 2015 high. This was unacceptable to central bankers around the globe who believe stock market gains are the only factor reflecting the health of our economic system. Maybe it’s because they are only beholden to bankers, oligarchs, corporate chieftains, corrupt politicians, and unaccountable bureaucrats. Central bankers from around the world have come to the rescue by buying stocks and providing unlimited liquidity to banks and corporations so they can buyback their own stocks. The result, is new record highs.

It has the feel of JP Morgan “rescuing” Bear Stearns and saving the world in early 2008. Smoke, mirrors, negative interest rates, debt creation, money printing and the artificial elevation of stock valuations by central bankers and their politician co-conspirators is not creating wealth. It is creating epic bubbles in stock markets, bond markets, home real estate markets, commercial real estate markets, and automobile markets. John Hussman chimes in with a reality based assessment of their reckless actions:

“Instead, central bankers seem to view elevated security valuations as “wealth.” The longer this fallacy persists, the worse the subsequent fallout will be. I have little doubt that future generations will look at the reckless arrogance of today’s central bankers no differently than we view speculators in the South Sea Bubble and the Dutch Tulip-mania. Unfortunately, there is no mechanism by which historically-informed pleas of “no, stop, don’t!” will penetrate their dogmatic conceit. Nor can we change the psychology of investors.”

Today is just a continuation of the bubble blowing policies of the Fed and their central banker cohorts at the ECB and BOJ. These policies are deranged, illogical, and always result in the destruction of real wealth. Promoting financial engineering, while destroying the incentive to save and invest in the real economy has gutted true investment in our country. This is why good paying jobs have disappeared and we are left with the gutted remains of decades of financialization and globalization. As Hussman points out, our real economy has died a long slow death, drowning in debt.

“One of the hallmarks of the bubble period since the late-1990’s is that the growth rate of real U.S. gross domestic investment has slowed to less than one-quarter of the rate it enjoyed in the preceding half-century. Yet because central banks have stomped on the accelerator at every turn, the quantity of outstanding debt has never been higher, and the combined value of corporate equities and debt (“enterprise value”) is now at the highest multiple of corporate gross value-added since the 2000 bubble extreme.”

Artificially boosting stock prices through convoluted liquidity schemes, devious machinations, backroom central banker deals, sending Bernanke to Japan, and helicopter money dropped on Wall Street only, has just exacerbated the wealth inequality permeating the world. The anger over this blatant pillaging by the .1% who rule the world is reflected in the chaos across Europe and the brewing civil war here in the U.S.

As Hussman notes, no wealth is being created because no productive investments are being made. Mega-corporations buying back hundreds of billions of their own stock to enrich their executives is not a productive wealth creating venture. We are in the midst of a sickening crisis created by appalling incentives, driven by sociopathic corporate and political leadership captured by their greedy desire for power wealth and control. The sickness is pervasive and terminal.

“In a healthy economy, savings are channeled to productive investment, and the new securities that are issued in the process are evidence of that transfer. In an unhealthy economy, and particularly one with very large wealth disparities, a large volume of securities may be created, but they are often simply a way of supporting debt-financed consumption. As a result, no productive investment occurs, and no national “wealth” is created. All that occurs is a wealth transfer from savers to dis-savers. Over the past 16 years, U.S. real gross domestic investment has crawled at a growth rate of just 1.0% annually, compared with a growth rate of 4.6% annually over the preceding half-century. There’s your trouble.”

A chart that caught my eye this week, along with dozens of other data points from the real world, reveals the phoniness of the stock market rally and the underlying weakness of this tottering edifice of debt. We are supposedly in the seventh year of an economic recovery. Corporate profits have been at record highs. Interest rates are at record low levels.

The Fed and the FASB have colluded to allow banks and commercial real estate companies to fake their financial statements and pretend their assets are worth more than they are and to pretend rental income from non-existent tenants in their malls and office buildings can cover their debt payments. And somehow delinquencies and charge-offs are soaring by levels seen during the height of the 2008/2009 financial crisis. It seems all those vacant mall storefronts and all those FOR LEASE signs in front of every other commercial building across America are finally coming home to roost.

This faux economic recovery has been driven by debt, with much of it subprime. The shale oil scam was built on high yield debt and false promises. The Wall Street banks reported fake profits for years by relieving their loan loss reserves created in 2009. Now the table has turned.

The three largest banks in the US—Bank of America, JPMorgan Chase, and Wells Fargo—disclosed that the number of delinquent corporate loans increased by 67% in Q1.

- JPMorgan’s delinquent corporate loans increased by 50% to $2.21 billion

- Bank of America’s delinquent loans increased 32% to $1.6 billion

- Wells Fargo’s delinquent loans increased by 64%, to $3.97 billion

The “tremendous” auto recovery which drove sales (I use the term loosely since 31% of sales are actually leases and the rest are financed over an average of 67 months) from 10 million in 2010 to 18 million in 2015 has been completely driven by easy money provided to Wall Street. It’s amazing how many vehicles you can sell by doling out $350 billion in 0% loans and allowing “buyers” to finance 100% of the purchase.

When they started to run out of legitimate suckers who liked being perpetual debt slaves, they used the tried and true method that worked so well with housing in the mid-2000s – loaning money to losers who weren’t capable of repaying them. This Wall Street mindset is driven by the free money provided them by the Fed. You borrow from the Fed at 0%, lend it to deadbeats at 12% for 72 months so they can “buy” that $40,000 Cadillac Escalade and boost the economy. Over 20% of all auto loans are now being made to subprime (aka deadbeat) borrowers. Now the shit is hitting the fan belt.

Serious Delinquency Rates for Auto Loans by Term

| Risk Tier | |||

| Loan Term | Subprime | Prime | Super prime |

| 49-60 months | 22.4% | 3.4% | 0.4% |

| 61-72 months | 22.8% | 5.0% | 0.9% |

| 73-84 months | 30.7% | 7.1% | 1.8% |

The chickens are coming home to roost for subprime auto lenders and investors, with Fitch Ratings warning delinquencies in subprime car loans had reached a high not seen since October 1996. The number of borrowers who were more than 60 days late on their car bills in February rose 11.6% from the same period a year ago, bringing the delinquency rate to a total 5.16%. Subprime lending always ends in tears. Wall Street is probably betting against these packages of subprime slime while simultaneously selling them to their muppet clients. History rhymes.

These subprime auto loans look positively AAA compared to the hundreds of billions in subprime student loans distributed like candy by Obama and his government minions to artificially lower the unemployment rate and again boost the economy. Student loan delinquencies are already skyrocketing before the $400 billion doled out in the last four years has come due. The official delinquency rate reported by the government of 11% is another falsehood. The delinquency rate is really 17% when loans in deferment and forbearance — for which payments are postponed due to any reason — are included. The taxpayer will eventually foot the bill for at least $400 billion in losses.

We’ve been borrowing from the future for the last 16 years because real economic growth was killed by Greenspan, Bernanke, Yellen and the rest of the Fed yahoos. The stock market has returned 60% since the 2007 peak, three times the growth in corporate profits and GDP. The all-time highs in the stock market have been driven by the $3.4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, PE expansion, and ZIRP. The valuation of the median stock is now the highest in history.

For all I know the stock market could continue to rip higher. Madness knows no bounds. The general public is not involved in this madness. They were wiped out twice in the space of eight years. Wall Street and their media mouthpieces have been unable to lure the average Joe back into the casino because the average Joe has been impoverished by Fed policies designed to benefit the .1%. The Wall Street lemming herd has gone mad, but I’m not sure they will recover their senses before they burn the entire demented financial system to the ground. But enjoy the all-time highs while they last.

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.” ? Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds

Italy’s banking sector is looking increasingly vulnerable and analysts are starting to fear that the euro zone’s third largest economy could “go under,” warning of the potential for bank runs, credit rating downgrades and the threat to the wider European banking system.

We have reports from readers in Italy that ATM machines are being emptied. A run on banks is beginning in Italy.

https://www.armstrongeconomics.com/world-news/sovereign-debt-crisis/banking-panic-in-italy/

Bank runs, bailouts and downgrades? What Italy’s future could look like

Italy’s banking sector is looking increasingly vulnerable and analysts are starting to fear that the euro zone’s third largest economy could “go under,” warning of the potential for bank runs, credit rating downgrades and the threat to the wider European banking system.http://www.cnbc.com/2016/07/06/bank-runs-bailouts-and-downgrades-what-italys-future-could-look-like.html

“Italy could be a bigger threat to euro zone stability than Brexit,” Andrew Edwards, chief executive of London spread better ETX Capital said in a note on Tuesday. “The nation has a creaking banking sector that could undo all the European Central Bank‘s efforts to save the euro if not handled correctly.”

“Unlike other countries, Italy did not carry out a full spring clean of its banks post-Lehmans and there is trouble brewing with the country’s banks holding 360 billion euros ($400 billion) in non-performing loans (NPLs) – a third of all the euro zone’s bad debt and about a fifth of all consumer loans in Italy,” Edwards noted, highlighting the extent of Italy’s banking vulnerabilities.

While Central Banks Have Gone All In, Delinquency Rates Rising. Is A New Banking Crisis imminent?

Technically Speaking: Breakout Or Market Meltup? – Lance Roberts

While Central Banks have gone all in, including the BOJ with additional QE measures of $100 billion, to bail out financial markets and banks following the “Brexit” referendum, it could backfire badly if the US dollar rises from foreign inflows. As shown below, a stronger dollar will provide another headwind to already weak earnings and oil prices in the months ahead which could put a damper on the expected year-end “hockey stick” recovery currently expected.

https://realinvestmentadvice.com/technically-speaking-breakout-or-market-meltup/

Delinquency Rates Rising – Is A New Banking Crisis imminent?

A clear danger sign: delinquency rates on commercial and industrial loans are creeping up. Source: St Louis Fed

A clear danger sign: delinquency rates on commercial and industrial loans are creeping up. Source: St Louis Fed

In dollar terms the shift is even more pronounced. This is

of course the result of our staggering debt levels, which are not

apparent in the relative numbers. Source: St Louis Fed

In dollar terms the shift is even more pronounced. This is

of course the result of our staggering debt levels, which are not

apparent in the relative numbers. Source: St Louis Fed

In line with increasing loan delinquencies, charge-off rates

on commercial and industrial loans are picking up as well (charge-off

rates tend to lag somewhat). Source: St Louis Fed

Even if we are on the verge of a new banking crisis, the headline number will never tell us so.

In line with increasing loan delinquencies, charge-off rates

on commercial and industrial loans are picking up as well (charge-off

rates tend to lag somewhat). Source: St Louis Fed

Even if we are on the verge of a new banking crisis, the headline number will never tell us so.

https://mises.org/blog/delinquency-rates-rising-new-crisis-approaching

Former FDIC Chair Sheila Bair expects more pain ahead for US banks

“I think it’s been ill-advised to rely on monetary policy, but that still appears to be the only game in town.”

http://www.cnbc.com/2016/07/11/former-fdic-chair-sheila-bair-expects-more-pain-ahead-for-us-banks.html

Gerald Celente-Panic Of 2016 At The Doorstep

All links can be found here: http://usawatchdog.com/separate-laws-…

While Central Banks have gone all in, including the BOJ with additional QE measures of $100 billion, to bail out financial markets and banks following the “Brexit” referendum, it could backfire badly if the US dollar rises from foreign inflows. As shown below, a stronger dollar will provide another headwind to already weak earnings and oil prices in the months ahead which could put a damper on the expected year-end “hockey stick” recovery currently expected.

https://realinvestmentadvice.com/technically-speaking-breakout-or-market-meltup/

Delinquency Rates Rising – Is A New Banking Crisis imminent?

The delinquency rate on loans is

key in understanding banking. It answers one question: what percentage

of loans is overdue for payment? The delinquency rate is by far the most

useful indicator for “credit stress.” It seems, however, as if

delinquency no longer counts. Few are paying attention to the quick and

sudden rise of the delinquency rate. What does it tell us and is a new

banking crisis imminent?

…https://mises.org/blog/delinquency-rates-rising-new-crisis-approaching

Former FDIC Chair Sheila Bair expects more pain ahead for US banks

“I think it’s been ill-advised to rely on monetary policy, but that still appears to be the only game in town.”

http://www.cnbc.com/2016/07/11/former-fdic-chair-sheila-bair-expects-more-pain-ahead-for-us-banks.html

Gerald Celente-Panic Of 2016 At The Doorstep

Published on Jul 10, 2016

At the beginning of this year, Gerald Celente,

the publisher of the Trends Journal, put out a magazine cover that

predicted the “Panic of 2016.” How close are we to the “panic”? Celente

says, “We are at the doorstep, and it’s ready to go. Look at gold

prices. Look at how they have been going up. They are up 28% year to

date. I ask people, would you buy a bond where you know you are going to

get less back than what you paid for it in 10 years? Or, do you think

gold prices will be higher in 10 years than they are now? That’s why you

are seeing gold as the safe haven.”

Join Greg Hunter as he goes One-on-One with Gerald Celente, publisher of The Trends Journal.All links can be found here: http://usawatchdog.com/separate-laws-…

Ireland exposes the flaws of using GDP as an economic measure

by Shaun Richards

Firstly let me welcome you all to what is already being called MayDay in the UK as it will see our second female Prime Minister. However as I noted yesterday there has been quite an event in the world of economic measurement that has occurred across the Irish Sea and it is something which has taken place in spite of all the “improvements” that were made with the ESA 10 changes. Indeed more than a few of you may be wondering if someone has been indulging rather too liberally in one of the boosts to GDP (Gross Domestic Product) that it brought namely the addition of illegal drugs such as cocaine.

The Financial Times summarised it thus.

The gap between GDP and GNP

This has been a regular topic on here concerning Ireland.

An Inflation Problem

We are regularly told that there is no inflation in the Euro area and consumer inflation in Ireland has been close to zero for some time. Thus you will not be surprised to note my eyes alighted on these inflation measures. The deflator for GDP rose by 4.9% in 2015 and the deflator for GNP rose by 4.5%. So if Ireland had its own monetary policy and used the widest inflation measure of all for monetary policy then it certainly would not have an official deposit rate of -0.4%!

Care is needed as consumer inflation is a significant part of the GDP deflator (24% in the UK for example) but is far from all of it. The catch is that as I look elsewhere I see few signs of the difference. For example we know that there is some services inflation around but if we look it falls well short of what we are told.

There was a burst of inflation in the output price index for manufacturing early in 2015 as the annual rate rose to 9.5% but by the end of the year this had faded. But we have a problem as you see output is recorded as much higher and it seems to have done so accompanied by higher prices! If only we could all do that…….

Ch-ch-changes

This came in the world of net trade so let me take you back to where we thought we were only a few short months ago.

Manufacturing

I did point out that there was a potential issue with prices being higher whilst output also surges. As the surge in prices was taking place then quarterly exports of merchandise trade rose from 30.1 billion Euros to 46.5 billion Euros. Apart from the obvious question of how this happened without the official statisticians noticing there is a lot which requires investigation here. The national accounts do provide a clue of sorts.

Comment

Let me now bring in some of the factors which have been at play here. A lot of aircraft leasing activity takes place in Ireland. This has been booked as an increase in assets and therefore GDP. An explanation has been provided by Colm McCarthy on the Irish Economy website.

Oh and as Claus Vistesen points out

Firstly let me welcome you all to what is already being called MayDay in the UK as it will see our second female Prime Minister. However as I noted yesterday there has been quite an event in the world of economic measurement that has occurred across the Irish Sea and it is something which has taken place in spite of all the “improvements” that were made with the ESA 10 changes. Indeed more than a few of you may be wondering if someone has been indulging rather too liberally in one of the boosts to GDP (Gross Domestic Product) that it brought namely the addition of illegal drugs such as cocaine.

The Financial Times summarised it thus.

That is the highest level of growth for decades and far outstrips the original estimate of Irish economic activity last year, which the official Central Statistics Office had put at 7.8 per cent. A growth rate of more than 26 per cent is nearly three times the highest level recorded during Ireland’s Celtic Tiger boom years in the early 2000s.To be precise the annual rate of growth was revised upwards to 26.3% with the first quarter of 2015 being the main culprit as it recorded economic growth of 21%. It was only on the 22nd of last month that I pointed out that the Irish economy was doing well so here is the comparison with what we were previously told.

Preliminary estimates indicate that GDP in volume terms increased by 7.8 per cent for the year 2015. GNP showed an increase of 5.7 per cent in 2015 over 2014.

As you can see 26.3% is the new

7.8%! This of course was quite a rate of economic growth in itself. Also

we should not move on without considering the point that this is treble

the rate of growth claimed in the Celtic Tiger boom which of course

ended in a painful bust.

There is another consequence of all this and let me explain with something else from the 22nd of June.In 2015 GDP was 203.5 billion Euros and GNP (Gross National Product) was 171.9 billion Euros.I was using this to explain a problem I will return to in a moment. But you will get my point if I tell you that the new revised 2015 GDP is 243.9 billion Euros and the new 2015 GNP is 194 billion Euros. So they are 20% higher and 13% higher respectively! Let us just remind ourselves that this is for the year just gone and consider the scale of this when sometimes changes in GDP growth rates as small as 0.1% are debated and indeed forecast.

The gap between GDP and GNP

This has been a regular topic on here concerning Ireland.

The difference is that a lot of businesses in Ireland are non-domiciled there and send the money home. They want to take advantage of the low corporation tax rate and other benefits but do not consider it to be home. As you can see it is a big deal.The difference is that the “big deal” as I called it has just got a lot bigger. The gap was previously reported as 31.6 billion Euros and is now 49.9 billion Euros. But this is only part of the story as GNP rose by 18.7% itself in 2015.

An Inflation Problem

We are regularly told that there is no inflation in the Euro area and consumer inflation in Ireland has been close to zero for some time. Thus you will not be surprised to note my eyes alighted on these inflation measures. The deflator for GDP rose by 4.9% in 2015 and the deflator for GNP rose by 4.5%. So if Ireland had its own monetary policy and used the widest inflation measure of all for monetary policy then it certainly would not have an official deposit rate of -0.4%!

Care is needed as consumer inflation is a significant part of the GDP deflator (24% in the UK for example) but is far from all of it. The catch is that as I look elsewhere I see few signs of the difference. For example we know that there is some services inflation around but if we look it falls well short of what we are told.

Services prices in Quarter 1 2016, as measured by the experimental SPPI, were on average 1.5% higher in the year when compared with the same period last year.Actually services inflation was a fair bit higher early in 2014.

There was a burst of inflation in the output price index for manufacturing early in 2015 as the annual rate rose to 9.5% but by the end of the year this had faded. But we have a problem as you see output is recorded as much higher and it seems to have done so accompanied by higher prices! If only we could all do that…….

Ch-ch-changes

This came in the world of net trade so let me take you back to where we thought we were only a few short months ago.

Import growth during the year of 16.4 per cent outpaced that of exports at 13.8 per cent.I pointed out back then that Ireland was doing its bit for world and European trade. However that story has expired also and been replaced by a new version.

On the expenditure side of the accounts exports grew by 34.4% between 2014 and 2015 (Table 6, at constant prices). Imports increased also, by 21.7%, over the same period.So as you can see there was an exports surge and in fact rather than helping demand in other nations Ireland in fact has increased its own current account surplus. So export led growth for it but not so good for its trading partners as we observe yet another large change.

The revised current account surplus for 2015 was €26,157m, an increase of €22,954m on 2014.The current account surplus is now on its way to 15% of GDP. So is it Ireland that has used a lower exchange rate to boost its exports in the same way as Germany? That point is a little tongue in cheek but there is a point to it.

Manufacturing

I did point out that there was a potential issue with prices being higher whilst output also surges. As the surge in prices was taking place then quarterly exports of merchandise trade rose from 30.1 billion Euros to 46.5 billion Euros. Apart from the obvious question of how this happened without the official statisticians noticing there is a lot which requires investigation here. The national accounts do provide a clue of sorts.

Industry (including building) advanced by 87.3% ( in 2015)That happened without anybody noticing it for quite a while.

Comment

Let me now bring in some of the factors which have been at play here. A lot of aircraft leasing activity takes place in Ireland. This has been booked as an increase in assets and therefore GDP. An explanation has been provided by Colm McCarthy on the Irish Economy website.

There are roughly 750 commercial passenger aircraft on the Irish register for April 2016. The number actually based at Irish airports and serving Irish traffic is only about 100. Ryanair registers all its 340 aircraft here but only 10% are based at Irish airports.There is debate over the numbers but not the principle. Also it appears that factors such as the patents of international firms have been booked in Ireland and counted in GDP. Did I say firms as this from the Central Statistics Office might mean one firm?!

As a consequence of the overall scale of these additions, elements of the results that would previously been published are now suppressed to protect the confidentiality of the contributing companies, in accordance with the Statistics Act 1993.Even the Governor of the Central Bank of Ireland is concerned by this according to the Irish Times.

The Irish Times has learned Prof Lane met the CSO on Monday and made known his concerns that the GDP growth figures do not accurately reflect economic activity in Ireland.Please do not misunderstand me I think that the Irish economy is growing as there are other measures such as the rise in employment. But the sad part is that we now have very little idea of at what rate! Rather ironically Ireland will be paying more to the European Union because of all of this and because of money it may never see. At least the rate of growth for net national income was a more subdued 6.5%. But it is time to hear from Marvin Gaye one more time.

Oh, what’s going on?Meanwhile I did point out on the 22nd of June that other measures pose questions as to the whole narrative.

What’s going on?

Ya, what’s going on?

Ah, what’s going on?

Ireland and Luxemburg showing a very large difference between these two measures of household welfare. Using the AIC measure, Irish households are closer to Italian than Danish levels of welfare.As the television series Soap used to tell us “Confused? You soon will be!”

Oh and as Claus Vistesen points out

Bonkers … it will likely lead to an upward revision of EZ GDP growth of 0.3pp in 2015. That’s 1.9% then, punchy

Cargo Volume At Chinese Ports Falls To 7-Year Low

More bad news for the world economy as China watches port volume fall to a 7 year low according to this WSJ report.

Cargo volumes through China’s ports grew at the slowest pace in seven years in the first half of 2016, according to an industry report that showed the country’s trade slump hitting its biggest gateways.

China port container volumes rose 2.5% in the January-June period from a year ago, research group Alphaliner said in a report this week, and the ports of Shanghai and Shenzhen—China’s two biggest sites for imports and exports—both saw container traffic decline 1%.

“Overall container volumes at Chinese ports are growing at the slowest pace since 2009,” Alphaliner said in its weekly newsletter on shipping industry trends. Chinese ports registered a 4.6% drop in volumes that year.

The sluggish business at China’s main gateways comes as the country’s trade downturn is accelerating. The China General Administration of Customs reported Wednesday that China’s exports, which have long been a central piece of the global economy, declined 4.8% in May while imports fell 8.4%.

Truck plows into crowd, killing at least 84 in Nice, France

Scene of chaos at Bastille Day celebration

Reuters

Reuters

NICE, France — A truck driver barreled for more than a mile through Bastille Day revelers thronging the famed seaside promenade here Thursday, killing scores of people and sending a terror-scarred nation reeling again.

The driver slammed the massive vehicle, which an official said was loaded with explosives and weapons, into a crowd packed with families that had come to see the celebratory fireworks, leaving bodies in his wake.

At least 84 people were killed and 18 critically wounded, a French official said.

Truck driver kills dozens in Nice, France

A truck driver plowed through a crowd gathered on a coastal promenade at a Bastille Day celebration on Thursday in Nice, France, killing several dozens of people and sending hundreds fleeing from the scene. Photo: Getty Images“France has been struck on its national day — July 14, a symbol of freedom — because human rights are denied by fanatics and France is of course their target,” Hollande said.

Witnesses said the driver steered the truck into the crowd deliberately, maintaining speed as he ripped through the revelers. The rampage ended in a hail of police bullets that killed the driver, bringing the truck to a halt, officials said.

“We thought he lost control. We all shouted: ‘Stop! Stop!’” said Nader Shafa’ai, an Egyptian tourist, who captured the mayhem on his video camera as the truck came careering through the crowd. “Then it was clear it wasn’t an accident.”

The footage Mr. Shafa’ai shot shows French police as they surrounded the white truck and fired rounds at the driver. The footage also shows scores of bodies under and behind the truck.

“I filmed it because I was in shock,” Shafa’ai said.

Reuters

Reuters

Images on French TV showed a cargo truck windshield pocked with bullet holes.

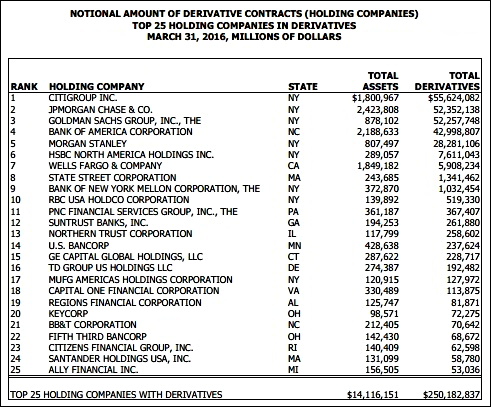

Citigroup Has More Derivatives than 4,701 U.S. Banks Combined; After Blowing Itself Up With Derivatives in 2008

Derivatives at Bank Holding Companies, March 31, 2016 (OCC Report)

According to the Federal Deposit Insurance Corporation (FDIC), as of March 31, 2016, there were 6,122 FDIC insured financial institutions in the United States. Of those 6,122 commercial banks and savings associations, 4,701 did not hold any derivatives. To put that another way, 77 percent of all U.S. banks found zero reason to engage in high-risk derivative trading.

Citigroup, however, the bank that spectacularly blew itself up with toxic derivatives and subprime debt in 2008, became a 99-cent stock during the crisis, and received the largest taxpayer bailout in U.S. financial history despite being insolvent at the time, today holds more derivatives than 4,701 other banks combined which are backstopped by the taxpayer.

The total notional amount of derivatives sitting at Citigroup’s bank holding company is $55.6 trillion according to the March 31, 2016 report from the Office of the Comptroller of the Currency (OCC), one of the regulators of national banks. (See chart above.) Out of Citigroup’s total notional (face amount) exposure of $55.6 trillion in derivatives, $52 trillion of that is sitting at its insured depository institution, Citibank, which is still decidedly too-big-to-fail and would require a taxpayer bailout again in a collapse.

If you add in four other mega Wall Street banks (JPMorgan Chase, Goldman Sachs, Bank of America and Morgan Stanley) to Citigroup’s haul in derivatives, there is a staggering $231.4 trillion in derivatives or 93 percent of all derivatives in the entire FDIC banking universe of 6,122 banks and savings associations.

Didn’t the Obama administration tell the public that allowing these Frankenbanks to continue to gamble in derivatives while putting the U.S. economy and taxpayers at risk was going to end under his Dodd-Frank financial reform legislation passed in 2010? How could there have been meaningful reform of Wall Street if Citigroup and these other four banks are still holding a loaded gun to the taxpayers’ head?

Under the “Push-Out Rule” (Section 716 of the Dodd-Frank Wall Street Reform and Consumer Protection Act), insured banks were not going to be allowed to hold these derivatives when the rule was fully implemented in July 2015. The mega banks would have to “push-out” the derivatives to their uninsured affiliates so that the taxpayer wasn’t on the hook for future losses or bank implosions. But in December 2014, Citigroup was able to slip language into the must-pass spending bill that effectively repealed this critical Dodd-Frank provision and President Obama signed the bill into law.

According to OCC data, prior to Citigroup’s massive bailout in 2008, it held $41.3 trillion in notional derivatives as of March 31, 2008. Instead of regulators forcing the unruly bank to pare back its exposures, its tally today of $55.6 trillion shows it has been allowed to grow its derivative risks by 35 percent.

According to the General Accountability Office, this is how much Citigroup needed to remain afloat the last time it blew itself up: On October 28, 2008, Citigroup received $25 billion in Troubled Asset Relief Program (TARP) funds. Less than a month later, it was teetering again and received another $20 billion. But its capital moorings were so shaky that it simultaneously needed another $306 billion in government asset guarantees. And all of this disclosed money spigot came on top of the Federal Reserve secretly funneling to Citigroup over $2 trillion in cumulative loans over more than two years at interest rates frequently below 1 percent.

The official report on the financial crisis of 2008 from the Financial Crisis Inquiry Commission explained the interconnected nature of the derivatives crisis as follows:

“Large derivatives positions, and the

resulting counterparty credit and operational risks, were concentrated

in a very few firms. Among U.S. bank holding companies, the following

institutions held enormous OTC derivatives positions as of June 30,

2008: $94.5 trillion in notional amount for JP Morgan, $37.7 trillion

for Bank of America, $35.8 trillion for Citigroup, $4.1trillion for

Wachovia, and $3.9 trillion for HSBC. Goldman Sachs and Morgan Stanley,

which began to report their holdings only after they became bank holding

companies in 2008, held $45.9 and $37 trillion, respectively, in

notional amount of OTC derivatives in the first quarter of 2009. In

2008, the current and potential exposure to derivatives at the top five

U.S. bank holding companies was on average three times greater than the

capital they had on hand to meet regulatory requirements. The risk was

even higher at the investment banks. Goldman Sachs, just after it

changed its charter, had derivatives exposure more than 10 times

capital. These concentrations of positions in the hands of the largest

bank holding companies and investment banks posed risks for the

financial system because of their interconnections with other financial

institutions.”

The counterparties to this mass gluttony in derivatives by the mega

Wall Street banks included the two government sponsored enterprises,

Fannie Mae and Freddie Mac, and the large insurer, AIG.In May of this year we reported that the U.S. government is still quietly paying out billions of dollars to Wall Street banks for derivatives held by Fannie Mae and Freddie Mac, companies the government was forced to place into conservatorship because of their massive losses during the 2008 crisis. In April of this year we reported the following about AIG’s derivative losses during the crisis:

“AIG received a taxpayer backstop of $185

billion and had to be taken over by the Federal government. But the

bailout of AIG was in reality a backdoor bailout of the biggest Wall

Street banks and their foreign big bank kin who had used AIG as a

counterparty on their casino-like derivative bets and for securities

loans that AIG could not make good on.

“It was eventually revealed that major

Wall Street banks, foreign banks and hedge funds received more than half

of AIG’s bailout money ($93.2 billion). Public pressure eventually

forced AIG to release a chart of

these payments, but the chart showed just a narrow window of

disbursements from September to December 2008. How vast the full total

of payments were to the big banks is yet to see the light of day.”

The banking crisis and economic collapse in 2008 was the largest

financial disaster in the United States since the Great Depression. To

understand that the Obama administration and the U.S. Congress have not

only failed to rein in the risks of a recurrence but have actually

allowed the risks to dramatically grow, is an indictment of our entire

political system and a siren call for the political revolution that

Senator Bernie Sanders has now surrendered to the Clinton Wing of the

Democratic Party — otherwise known as the Wall Street Banksters.Related Article:

Interconnected Banks Pose Greatest Threat to U.S. Financial System

Dr. Lacy Hunt: Yes, The Economy Is Actually That Bad

by Robert Johnson

Debt. It’s good, it’s bad, there’s too much of it, the government keeps piling on more of it. What’s the deal?

You may have none, you may have too much, but one thing is certain, debt is a major driving force behind the world economy. Both in our personal lives and in the lives of immense corporations struggling to hold on in an ever-changing economy. Make no mistake, debt patterns will continue to shape all of our financial landscapes.

Given this unavoidable fact of life, when we had the chance to sit down with Dr. Lacy Hunt of Hoisington Investment Management to discuss his upcoming appearance at our Irrational Economic Summit in October, debt is where we began.

See, when you agree to spend borrowed money today, you’re leveraging that against your future income. That means that the dollars you’ll earn tomorrow are already spent and will not be there to use in the future for anything else. Seems obvious, right?

Of course, this is not a problem if you expect your income to increase as time marches along and your payments become due. But how many people in America are facing an increase in personal income when the standard of living hasn’t changed one iota in 20 years? Not many.

Unfortunately, this is not on the forefront of most people’s thoughts when they go to buy something like a new car. Dr. Hunt points out that new car sales are buoying portions of the economy, but that credit-lending standards have slipped, much like they did for mortgages prior to the housing crisis in 2008 (Harry has been talking about the auto sector soon getting turned on its head for months!).

To illustrate this, Dr. Hunt points out that the average automobile loan has gone from six years to eight in order to allow less qualified buyers to purchase more expensive cars than they might otherwise have been able to afford.

This allows buyers to make smaller payments over a longer term, but also exposes them to the risk of missing any one of those 96 monthly payments.

But what about student debt? That has always been one way to invest in ourselves, and our children, and foster new revenue streams to pay down interest and principal. Dr. Hunt has bad news on that front, as well.

From Dr. Hunt’s interview with Rodney Johnson:

Unfortunately, the economy is performing so poorly that a lot of our college graduates are coming out and they’re having to settle for jobs that are not much better than what they would’ve received if they had gone directly into the labor force from high school.

Even classically “good debt” like a college education has become a non-performing investment. That’s scary because Dr. Hunt also points out that this deluge of debt, and our eagerness both as a country and as consumers to incur the “wrong type of debt” is killing growth.

This debt is slowing GDP growth and the growth of our personal incomes and investments. “That’s why”, Dr. Hunt points out, “the standard of living is unchanged from where it was 20 years ago.”

These are some cold, hard facts from one of the premier investment adviser’s in the country. It’s tough to read and painful to understand, but it’s true. And ideally, we’re in the business of truth and understanding the challenges facing all investors.

If you’re up for more of it, stay tuned because we’ll be bringing you excerpts from interviews with all our upcoming Irrational Economic Summit speakers in the weeks leading up the October event.

Thanks and play safe,

Robert Johnson

Editorial Director, Dent Research

Debt. It’s good, it’s bad, there’s too much of it, the government keeps piling on more of it. What’s the deal?

You may have none, you may have too much, but one thing is certain, debt is a major driving force behind the world economy. Both in our personal lives and in the lives of immense corporations struggling to hold on in an ever-changing economy. Make no mistake, debt patterns will continue to shape all of our financial landscapes.

Given this unavoidable fact of life, when we had the chance to sit down with Dr. Lacy Hunt of Hoisington Investment Management to discuss his upcoming appearance at our Irrational Economic Summit in October, debt is where we began.

U.S. consumers have racked up

almost $1 trillion in credit card debt, despite some saying this is a

great sign, that this means consumers are optimistic and will buoy the

economy, Dr. Hunt does not agree.

He immediately points out that debt is a two-edged sword and that if

additional indebtedness doesn’t work to create income to pay down

interest and principle, it is a no-win deal.See, when you agree to spend borrowed money today, you’re leveraging that against your future income. That means that the dollars you’ll earn tomorrow are already spent and will not be there to use in the future for anything else. Seems obvious, right?

Of course, this is not a problem if you expect your income to increase as time marches along and your payments become due. But how many people in America are facing an increase in personal income when the standard of living hasn’t changed one iota in 20 years? Not many.

Unfortunately, this is not on the forefront of most people’s thoughts when they go to buy something like a new car. Dr. Hunt points out that new car sales are buoying portions of the economy, but that credit-lending standards have slipped, much like they did for mortgages prior to the housing crisis in 2008 (Harry has been talking about the auto sector soon getting turned on its head for months!).

To illustrate this, Dr. Hunt points out that the average automobile loan has gone from six years to eight in order to allow less qualified buyers to purchase more expensive cars than they might otherwise have been able to afford.

This allows buyers to make smaller payments over a longer term, but also exposes them to the risk of missing any one of those 96 monthly payments.

But what about student debt? That has always been one way to invest in ourselves, and our children, and foster new revenue streams to pay down interest and principal. Dr. Hunt has bad news on that front, as well.

From Dr. Hunt’s interview with Rodney Johnson:

Unfortunately, the economy is performing so poorly that a lot of our college graduates are coming out and they’re having to settle for jobs that are not much better than what they would’ve received if they had gone directly into the labor force from high school.

Even classically “good debt” like a college education has become a non-performing investment. That’s scary because Dr. Hunt also points out that this deluge of debt, and our eagerness both as a country and as consumers to incur the “wrong type of debt” is killing growth.

This debt is slowing GDP growth and the growth of our personal incomes and investments. “That’s why”, Dr. Hunt points out, “the standard of living is unchanged from where it was 20 years ago.”

These are some cold, hard facts from one of the premier investment adviser’s in the country. It’s tough to read and painful to understand, but it’s true. And ideally, we’re in the business of truth and understanding the challenges facing all investors.

If you’re up for more of it, stay tuned because we’ll be bringing you excerpts from interviews with all our upcoming Irrational Economic Summit speakers in the weeks leading up the October event.

Thanks and play safe,

Robert Johnson

Editorial Director, Dent Research

GLOBAL MARKETS SKATING ON THIN ICE

The market is starting to skate on thin ice. What will fall first? Every sector is getting erratic.

No Way Around European Banking System Bailout

Jason Burack and Eric Dubin are back for Episode #24 of Welcome to Dystopia!

During this episode, Jason and Eric start off by discussing Brexit and how gold and silver markets reacted to Brexit.

Jason and Eric discuss the gold and silver markets, an imminent European banking Crisis involving Deutsche Bank and other European banks, why it’s happening and what can be done about it along with other current events going on all over the globe including:

1) Japanese Savers Flooding to Physical Gold http://www.zerohedge.com/news/2016-07…

2) China planning to use more than $300 billion in saver’s pension

fund capital for a bailout/Plunge Protection Team of their stock market http://www.zerohedge.com/news/2016-07…3) Ben Bernanke visits Abe and Kuroda in Japan to discuss a new 10 trillion Yen “helicopter money” plan in next stage of Abenomics.

4) The more than $12 trillion in global government bonds that now have negative interest rates.

Peter Schiff joining team Bitgold/Gold Money!

Scumbag Nominees:

1) Hillary Clinton for getting off the FBI charging her http://www.nmws.us/fbi-insider-leaks-…

http://www.infowars.com/fbi-source-cl…

2) 26 Democrats who did the gun law “sit in” all own guns! https://heatst.com/politics/26-of-the…

3) Congresswoman Corrine Brown and her assistant running a fake charity and stealing $800k facing up to 300 years in prison http://thehill.com/blogs/blog-briefin…

4) Bernie Sanders endorses Hillary Clinton this week! What a hypocrite!

WE COULD HAVE SPENT OVER AN HOUR OF THE SHOW NAMING ADDITIONAL SCUMBAG NOMINEES INCLUDING THE TSA AGENTS WHO ASSAULTED A DISABLED GIRL, THE FAST AND FURIOUS PROGRAM SELLING GUNS TO THE PARIS TERRORISTS IN ARIZONA, AND THE POLICE OFFICERS WHO DELETED THE VIDEO OF DIAMOND REYNOLDS’ PHONE OF HER BOYFRIEND’S SHOOTINGhttp://www.againstcronycapitalism.org…

The People Want Answers To Why Their Standard Of Living Hasn’t Improved In 30 Years.

by James Quinn

The economy sucks for the majority of Americans. While the libs try to make the election about blacks, gays, and globull warming, the people want answers to why their standard of living hasn’t improved in 30 years.

You will find more statistics at Statista

The economy sucks for the majority of Americans. While the libs try to make the election about blacks, gays, and globull warming, the people want answers to why their standard of living hasn’t improved in 30 years.

You will find more statistics at Statista

Ron Paul Says the PPT Is Keeping Wall St in Record Territory! Etai Friedman: Fund Manager Goes All In On Precious Metals – Most Obvious Trade On the Planet!

Etai Friedman says he has never

seen a bigger green light in his life. It is literally the most obvious

trade on the planet. The trade is so good that Etai just rebalanced his

portfolio from a very small gold and silver allocation to 75%! And he’s

not done yet. He expects to go 100% towards precious metals within the

next couple months.

Etai believes that only 2 or 3 things will hold their value in the

coming crash.. gold, silver and maybe bitcoin. Gold and silver will

explode in anticipation of all the money printing that is in the works.The monetary easing is spilling into the US, and is taking down the 10 and 30 year treasuries, as well as the long-term interest rates. Every central bank is telegraphing us that they have the intention of debasing their currency in the hopes of spurring economic growth by fostering debt creation. That scenario has played out many times in the last 25 years, and it’s not going to work this time. Etai sees a collapse in the world economy and consequent money printing that will go into overdrive resulting in high rates of inflation within the next 5 years.

US stocks are the 2nd most overvalued that they have ever been in history. Stocks are ludicrously priced. The risk/reward in equities makes no sense. You can ride them up for maybe another 5 or 10 percent, but Etai is predicting an 80 percent drop in equities. It may take 3, 4, 5 years for that to happen but it will happen. Corporate bonds will be devastated, as well as government bonds when money printing goes into overdrive. We will go to negative yields.

Also, the end of the government bond market rally will be the world sliding into full-blown recession because it will be extremely deflationary, and when that gets detected by central banks, the money printing will explode. This will mean double-digit levels of inflation, possibly even hyperinflation. At that time, Etai might shift from precious metals into financial assets in the midst of a financial apocalypse where de-leveraging is happening on a major scale and paper money has lost 2/3 to 80% of it’s value.

Further, Etai contends that the Fed is done raising interest rates. The next move will be an interest rate cut, but it won’t happen overnight. In the first quarter of 2017 we will see a rate cut in the US and then probably negative rates. All of this coupled with the fact that the world can’t take on more debt is the biggest green light for owning gold and silver that has happened since the 70’s. If you are not long in gold and silver, you are badly positioned.

Cash-Strapped Towns Are Un-Paving Roads They Can’t Afford to Fix

City Hall received a hollering from a couple living on Bliss Road in the Vermont capital who wanted to sell their home, but feared the horrifying pavement in front of the house would scare away buyers. They had reason to be pissed off: The city of 8,000 people ranks pavement on an index of one to 100. Bliss Road scored a one.

Repaving roads is expensive, so Montpelier instead used its diminishing public works budget to take a step back in time and un-pave the road. Workers hauled out a machine called a “reclaimer” and pulverized the damaged asphalt and smoothed out the road’s exterior. They filled the space between Vermont’s cruddy soil and hardier dirt and gravel up top with a “geotextile”, a hardy fabric that helps with erosion, stability and drainage.

“We didn’t know how prevalent this was,” says Laura Fay, an environmental science researcher with Montana State University’s Western Transportation Institute, who helped compile the report. But there’s clear reason for it. The Congressional Budget Office finds that the while public spending on transportation and water infrastructure has actually increased since 2003, the costs of asphalt, concrete, and cement have jumped even faster. With those extra expenses factored in, public expenditures on transportation infrastructure relative to cost fell by nine percent between 2003 and 2014.

CONTINUE READING

Eurozone to EXPLODE: Demand for referendums after Brexit 'puts currency on the brink'

THE eurozone is set to be destroyed due to the poor economies of Greece and Italy, a leading economist has warned.

The economist told German Magazine Focus southern countries who cannot afford reforms would be forced to leave the Euro as he said the anti-EU sentiment “cannot be avoided”.

He said: “In France populist voices may get very strong. It would be highly likely though that the EU would be destroyed if France was to exit. Anything else, aside from Germany, the EU can take.

"Instead we are doing the opposite, meaning, we are now also burdening the German banking system with a union based on joint liabilities only to drag on the insolvency of the south and to go into insolvency together one day.”

Economists are already fearing struggling Italian banks could spark a major financial crash as the European Central Bank deals with a struggling eurozone economy and debt-burdened Greece, Italy, Spain and Portugal.

GETTY

GETTY

Mr Otte said at some point the eurozone will explode.

He said: “Today we know that the Euro has damaged and thrown back the EU immensely. I said in my presentation in April 1998 that the system will last for about ten years, before the difficulties would begin.

“I don't expect that the Euro will explode in the next years. At some point it has to explode because it's artificial and can't function in this form.”

In June it was decided the European Central Bank would be allowed to buy up debt and prop up the eurozone’s ailing economies, supported by Germany’s central bank.

But Mr Otte said the crisis is ongoing when the EU needs to pull together.

He said: “We have indeed entered a financial crisis in instalments. We're facing tough times - I can confirm that. I can't yet see the figurative light at the end of the tunnel.”