The blog, goldseek.com, recently published a report on a Freedom of

Information Act request they recently filed with the US government. They

were seeking seven reports from federal audits of the gold at Fort

Knox. The government's response? They can't find those reports - even

though they reference those reports as evidence of the gold stored at

Fort Knox in a number of ways. The Resident discusses.

This article may be re-posted in full with attribution.

In this country where we live today, on the very soil we tread, the

“ideologist” of the Athenian Republic, Protagoras, proclaimed “Man is

the measure of all things”, for the first time in the history of

humanity.

The Greek people, at one of the most critical and dramatic crossroads

of a history going back several thousands of years, for which they feel

proud and justifiably so, shall be called, this coming Sunday, to

decide once again whether man is the measure of all things or money is

the measure of all things, the latter being the central “motto” and

“belief” of the global financial oligarchy, the European “elites” and

their domestic offshoots, attacking Greece. And in the face of the

Greeks, they are attacking the social and democratic conquests of all

Europeans after their victory in 1945 against fascism, if not after the

French Revolution.

A moment comes for man, societies and nations alike, when they have

to decide «where they stand». This moment has now come for the Greek

people. They will have to decide once for all that their Alexandria[1] of

a few decades of a relatively stable and democratic prosperity that

followed the fall of the junta in 1974 and accession to the EC in 1981

is definitively lost. The real question facing this people, though, is

whether they will abandon this Alexandria with dignity, as urges their

great Poet, whether they will take the thorny and dangerous road towards

a new future, a new perspective for their country, or whether they will

fall apart in a state of enslavement. 1940, 2004, 2015

The answer the Greeks are going to give to the creditors’ ultimatum

is of no less importance than the importance of the answer they gave to

Benito Mussolini’s ultimatum on October 28, 1940. An answer that led to

the first victory of the Allies in World War II and to a delaying of the

German attack against the USSR which was probably decisive for the

outcome of the war. Their answer made Winston Churchill, celebrated for

his wit and not a friend of the Greeks, say: “Hence we will not say that

Greeks fight like heroes, but that heroes fight like Greeks!.”

The Greeks didn’t give this answer to Mussolini’s ultimatum out of

sympathy for their own regime, nor because they were in a better

position than they are today. They didn’t put up the strongest

resistance, proportionally to the country’s size, in the Nazi-occupied

Europe, because the conditions were favorable to them or because they

didn’t have anything to lose. They acted the way they did because, deep

down, they felt that they could not survive without their dignity. As a

people, we may be full of faults. But, I find it hard to believe that

some decades of consumerism were sufficient to undermine our sense of

self-pride (“filotimo”) that has always been with us during the critical

times of our history.

The significance of a NO in 2015 is no lesser than that of the NO

uttered by the citizens of the Republic of Cyprus in the 2004

referendum, who refused to give in to the strongest international

pressures in order to accept a plan which would abolish their

independent and democratic state. It is no lesser either than that of

the NO uttered by the French and the Dutch (2005 referendum), the Irish

(2008 referendum) and the Icelanders (2010) against Euroliberalism,

despite the fact that these NOs, with the exception of the one in

Iceland, were later belied by their leaderships.

What these NO had in common, despite the different circumstances, was

people’s opposition to the dissolution of their national and popular

sovereignty, of their independence and democracy, in the only context

where it still exists in today’s world, that of the nation-state. This

is what the Annan plan attempted to do in Cyprus or the European

constitutional treaty in Europe. Dignity

The question History is now asking us, by means of the «take it or

leave it» question of the creditors, is whether we continue or not to

consider our national and individual dignity as the fundamental value

which allowed our people and civilization to survive in the midst of

defeats, incredible threats and disasters for several thousands of

years. We have known many defeats in the course of our history. But we

never signed off our enslavement – this is the reason that the Greek

state exists today, be it a miserable, poor one; but the only one we

have got. We shall suffer of course if we resist the will of the mighty.

But, where shall we be without our own state, in the ocean of a

barbarous, “prehistoric” globalisation which causes whole nations to

perish?

This coming Sunday we are not merely called to decide whether we

accept the creditors’ ultimatum. We are called to determine whether we

consider the existence of a state of even a rudimentary independence and

democracy, as the most fundamental prerequisite for our national

survival.

Peoples have been called times and again in their history to choose

between destruction and enslavement. The creditors do not even place us

before such a dilemma. They want both. Our destruction and our

enslavement! The only thing they are offering us is the continuation of a

program which has caused, beyond the shadow of a doubt, as the greatest

economists of Europe, America and Russia admit, the biggest financial,

social and political disaster in Western (capitalist) Europe after 1945.

Instead of apologizing for the destruction they have caused, they are

now impeding the Greek government from taking even elemental measures to

enable hundreds of thousands of people to have some food, the

medication they need, electricity, and heating, a roof over their heads;

they are killing the hopes of a whole people. These are the hands we

have permitted to take the control of Europe! The disillusionment

Many, including the SYRIZA leadership, had been under huge illusions

and, unfortunately, they are still suffering under them. They believed

that the Greek disaster was nothing but a misunderstanding, a mistake of

the prevailing European elites. After Monday, June 22, however, all

these illusions ought to have been dispelled. The Greek government

presented to the institutions a proposal which was in line,

unfortunately, with the program’s spirit, and a far cry from SΥRΙΖΑ’S

pre-electoral announcements on the basis of which it won the elections.

Had the proposal been accepted, it would not have solved any problems.

For many, this was an unacceptable proposal of capitulation.

What was the creditors’ reaction to this proposal? Initially, they

expressed their satisfaction because the spoiled leader of a «spoiled»

country was finally beginning to «see reason». After that they began

asking him for more concessions! They as good as told him “we are not

interested in taking prisoners of war, we are demanding your full

surrender and suicide.”

Faced with the political suicide option he was given for himself and

the option of a national-social suicide for his country, Alexis Tsipras

and his closest associates, who never wanted or prepared for a rupture

(on the contrary, they turned against all those of us who kept telling

them to prepare for the worse option), proclaimed – and rightly so – a

referendum, an idea which had been «brewing» since 2012 in the highest

echelons of SYRIZA.

It is now the time for the Greek people to answer whether they accept

or not the ultimatum. We hope that they will reject it with a sweeping

majority, although the indecisive stance of the SYRIZA leadership, its

weakness in defending its own choice, risks to bring about disastrous

results, aggravating the population’s doubts and fears.

The leaders of SYRIZA need to understand that they have already

crossed the Rubicon. They did so when they asked for the vote of the

Greek people in order to stop the disastrous course of the memorandum.

They crossed it yet again when they decided to hold a referendum. By so

doing they cut off bridges. They will drown and will drown us if they

attempt to reverse their course.

If they now turn around and look where they were, even a week ago,

they will turn into pillars of salt like Lot’s wife did. If they

capitulate, if they do not assume the consequences of their choices,

they will be adding ridicule to defeat.

Let not Alexis Tsipras entertain any illusions. If he cops out now,

he will not even be allowed to have George Papandreou’s relatively quiet

retirement. George is a man who always belonged to the “family”, to the

club of the “international establishment”, he is their man. Alexis

Tsipras shall be humiliated and thrown to the dogs, as an example for

all European peoples and politicians to see what is the fate of those

who dare challenge the masters.

There is only one way for the SYRIZA leaders. Rid themselves of their

remaining illusions and finish off what they started, taking all

necessary measures to organize the Greek people’s struggle for the

rescue of their country, and explaining to them what to do and why. We

shall never tire of repeating that it is not possible to organise the

Missolonghi exodus [2] by inviting people to a drink of ouzo on the beach of Aitolikon. Α la guerre, comme à la guerre, Napoleon used to say. And Greece has been at war since 2010, only, till now, it has chosen not to retaliate!

We hope that the Greek citizens, when asked by their children if they

personally accepted the TROIKA ultimatum in 2015, will be in a position

to answer them without lowering their heads. We also hope that the

leaders of the country will find the will and the mind to meet the

historical challenge it is facing. Dimitris Konstantakopoulos can be reached through his blog: Konstantakopoulos.blogspot.com. (Translated from Greek) Notes. [1] A poem by C. Cavafy, a Greek poet from Alexandria (1863-1933) [2]

A town which had been besieged by the Ottomans during the Greek

Revolution of 1821 and the inhabitants decided on a heroic exodus after

they had been exhausted by the long siege of their town. Aitolikon is a

small city near it.

Source: Counterpunch, 3 July 2015

(ATHENS)

Greek banks are preparing contingency plans for a possible “bail-in”

of depositors amid fears the country is heading for financial collapse,

bankers and businesspeople with knowledge of the measures said on

Friday.

The plans, which call for a “haircut” of at least 30 per cent on

deposits above €8,000, sketch out an increasingly likely scenario for at

least one bank, the sources said.

A Greek bail-in could resemble the rescue plan agreed by Cyprus in

2013, when customers’ funds were seized to shore up the banks, with a

haircut imposed on uninsured deposits over €100,000.

It would be implemented as part of a recapitalisation of Greek banks

that would be agreed with the country’s creditors — the European

Commission, International Monetary Fund and European Central Bank.

“It [the haircut] would take place in the context of an overall

restructuring of the bank sector once Greece is back in a bailout

programme,” said one person following the issue. “This is not something

that is going to happen immediately.”

Eurozone officials said no decision had been taken to wind up any

Greek banks or initiate a bail-in of depositors, a process that would be

started by the ECB declaring the banks insolvent or pulling emergency

loans.

Greece’s banks have been closed since Monday, when

capital controls were imposed to prevent a bank run following the

leftwing Syriza-led government’s call for a referendum on a bailout plan

it had earlier rejected. Greece’s highest court rejected an appeal by two citizens on Friday who had asked for the referendum to be declared unconstitutional.

Depositors can withdraw only €60 a day from bank ATM cash machines,

while requests to transfer funds abroad have to be approved by a special

finance ministry committee in co-operation with the Greek central bank.

Two senior Athens bankers said the country had only enough cash to

keep ATMs supplied until the middle of next week. This followed the

ECB’s decision this week not to increase Greece’s allocation of

emergency liquidity assistance after the bailout programme ended on June

30.

The outcome of Sunday’s referendum will determine how quickly Greece

wraps up a new bailout agreement with creditors, a top Greek banker

said.

“The solvency of Greek banks is not currently an issue, but obviously

the banks will be affected by how soon the country enters a new

programme,” the same banker said.

Greek deposits are guaranteed up to €100,000, in line with EU banking

directives, but the country’s deposit insurance fund amounts to only

€3bn, which would not be enough to cover demand in case of a bank

collapse.

With few deposits over €100,000 left in the banks after six months of

capital flight, “it makes sense for the banks to consider imposing a

haircut on small depositors as part of a recapitalisation. . . It could

even be flagged as a one-off tax,” said one analyst.

The average American spends 42 minutes shopping each day, but only 35 minutes socializing.

That’s the latest result of the U.S. Bureau of Labor Statistics’

annual “American Time Use Survey.” The survey is based on annual average

data from the American Time Use Survey about how individuals age 15 and

over spend their time.

It gets better on the weekends though. Although time spent buying

things goes up to 50 minutes per day on weekends and holidays, Americans

spend 62 minutes per day socializing.

As far as sports and volunteering goes? Forget about it. The average

American spends 18 minutes per day participating in sports, exercise and

recreation, and just 9 minutes per day volunteering.

BY SKY WANDERER – a stubborn deadlock that keeps the 99% in planned poverty –

In extant financial-economic system Banks keep “bailing out”

Governments and Governments keep “bailing out” Banks, and in both cases

the 99% of us – the Taxpayers – have to pay £ / € / $ trillions.

Meanwhile the elites of each country, the “top 1%”, are getting richer

by actually grabbing these £ / € / $ trillions.

This blog-post – specifically updated and offered as a starting point

of investigation to seek legal remedies and Debt-relief for the

long-suffering Greek people [9] – explains the REAL reason behind the

global phenomenon of Public Debts, Crisis and Austerity. Loaned Money is just IOU, Debt is a phantom, Austerity is planned poverty

At the very core of the global Crisis and Debt-trap, we find a series of fictitious transactions – Government- bonds and Bank-bailouts

– that result in the many £ / € / $ trillions of odious (illegitimate)

Public Debts – also called Sovereign or National Debts – as well as in

the increasing Tax-burden and intensifying Austerity and Cuts for the

99%.

The two sides of the sequence of fictitious (phony) transactions

between Banks – via the agency of IMF and WB – and Governments that

generate the ever-increasing Odious Public Debts, are in fact two empty but giant IOUs exchanged by Banks and Governments [1,2]:

1) The Bank ‘buys’ Bonds from the Government – lends money to the

Government – from the NEW money that the Bank creates out of thin air

for the transaction; that is, the Bank ‘pays/lends’ funds by merely

issuing an empty IOU to the Government; which means, the Bank promises

to pay X amount + y interests to the Government.

2) The Government ‘sells’ Bonds to the Bank – borrows money from the

Bank – that is, the Government issues an IOU to the Bank in exchange

for the Bank’s IOU; which means, the Government promises to pay X amount

+ z interests to the Bank, in exchange for the Bank’s promise to pay X +

y to the Government.

The first point to emphasize: the exact same empty transaction – as described above – is used for both purposes:

– for Banks supposedly helping out Governments

– for Governments supposedly helping out Banks.

This fact is proof that NO real tangible help is given and/or

received by either of the two parties, and that these transactions are

phony.

No risks, No losses, No reason for “bail-outs”, No reason for “Euro-crisis”

The second main point of the same relevance: how come that Banks need to be “bailed out” by Taxpayer money if the very same Banks are the very source of creating – out of thin air – ca. 97% of all money circulating in the economy? [1, 2] In current monetary system, private Banks create NEW money (in the form of mere IOUs/promises) every time they make loans,

which implies, inter alia, that these transactions between Banks and

Governments are responsible for issuing a large percentage of the money

circulating in the economy.

What follows from above proven and given fact is the shocking truth, that Banks can NEVER go bankrupt,

since they never posses money per se to begin with. When Banks create

money, it is merely in the form of computer digits entered on their

servers. When Crisis sets in, or the illusion thereof appears, it is

merely due to the very act of fear-mongering, panic-generating and to

the crowds’ consequent intensified rush into the Banks. And apparently

this trick is used by Banks and Governments as the most effective means

to blackmail all countries – a present case in point is Greece – thus

force them to surrender to described phony Debt-creating transactions

and to the consequent Austerity-dictates by the financial oligarchy.

Another relevant angle of private banking: whenever Banks “lend”

money, they do NOT take any risks, since they do NOT draw funds from any

pre-existing money-base. Again: Banks newly create money upon lending

by simply entering the respective monetary units on the borrower’s bank

account on a bank-server. Since no risks are involved in these

transactions, no real creditors/stakeholders are behind them, who suffer

NO LOSSES whatsoever in case of the borrower defaulting on the loan.

The way referenced Guardian article [2] puts it: “Just consider what

might happen if mortgage holders realised the money the bank lent them

is not, really, the life savings of some thrifty pensioner, but

something the bank just whisked into existence through its possession of

a magic wand which we, the public, handed over to it.”

By above consideration, another extra dimension of the ongoing hoax

called “modern banking system” is to be seen via the fact that the same

Banks that are allowed to create new money out of thin air upon

extending loans to their clients, when are supposed to pay out deposits

to their clients, they “run out of money” and “must” be bailed out

by the very bank-account money of the Banks’ clients – which does NOT

even exist as real cash – and by the Tax-money of the country’s

citizens.

No reason for Austerity, and even less reason for more Debt Guardian: “The Bank of England’s dose of honesty throws the theoretical basis for austerity out the window” [1, 2]

Another equally shocking implication of the fact that NO real money

is involved in the act of giving loans: The “borrowed” funds that enter

the economy as Government-loans are newly created upon the transactions

exchanging two fictitious IOUs [1, 2] yet, the Government Deficit

arising from the Debts these transactions generate is referred to as the

very “reason” for the subsequent Austerity and Government spending

Cuts.

The neoliberal Austerity-policy is imposed on all affected countries

as the “necessary” measures to compensate for the “monetary sacrifice”

to be made in order to enable Governments and countries to properly

function. These fictitious Government-loans are to deceive the citizens

of affected countries that the “inevitable consequences” of these

transactions that our societies must suffer are increasing Taxation for

the 99%, Cuts of essential public services, severe Austerity-measures,

Privatisations, loss of jobs, decreasing salaries and lower Government

Spending.

In other words, these transactions are illegitimate, because they are empty / fictitious / no-value / phantom-transactions; they do NOT represent any pre-existing priorly earned funds;

yet the astronomical amounts of Odious Public Debts created via such

transactions are cited by Governments as the ‘reason’ to keep their

countries entrapped in the unresolvable vicious cycle of increasing

Public Debt, Deficit, intensifying Austerity, Poverty and Crisis [12].

Even if the cause of the Government Deficit and its alleged consequences

were legitimate (they aren’t) the very policies via which the

collaborating Governments attempt to “handle” the deficit-problem,

further signify the lack of legitimacy of these Governments.

For all experts in Finance and Economics – and even for those with a minimal sense of logic – it is evident that:

Austerity only contracts any Economy, thus worsens any Crisis – triggers recession even in a healthy economy, as it is demonstrated on the Crisis side of flowcharts [12]

Constantly increasing the Debt/Deficit will obviously yield the exact

opposite effect of what is “expected”; it will obviously increase the

Deficit, obviously increase the Debt and will keep the Crisis in a

downward spiral – even more so when an economy is further burdened with

Austerity. A genuinely democratic, legitimate and responsible Government

would implement policies as shown on the Recovery side of flowcharts

[12]

Why Banks and Governments all over the world inflict this scheme upon the 99% of us: the hidden reasons

All Governments that keep accumulating the Odious Public Debt/Deficit

and keep imposing the “consequent” Austerity measures – under the

disguise of “attempting to treat the Crisis” – are either fatally

ignorant (lacking even basic common sense) or are deceiving their voters

and deliberately keep them in planned poverty via the

Crisis-Debt-Austerity vicious cycle. The net result of the Odious Public

Debts and the ‘subsequently’ enforced Austerity and Privatisations is

the accelerating process of transferring all lands, resources, values,

strategic organisations such as the NHS, ie., all wealth, power and

control, into the private ownership of the global elites: banks,

corporations and richest individuals. (With the notable exception of

Iceland [5, 6, 7, 8] who rejected the conditions of the IMF, suffered

the first and WORST hit by the sinister revenge of the financial

oligarchy, yet was first to recover and start economic growth, even

outside the EU.)

As far as the principles of macroeconomics are concerned, recognition

of the fact that Austerity only worsens economic recession and pushes

an economy into a downward spiral, requires no more than basic knowledge of economics,

and it is safe to assume that the respective decision-makers who still

keep imposing these measures possess an advanced knowledge in economics

and related field(s), hence we should indeed look for a more plausible

explanation behind the idea of their attempting to “fix” the economy in a

way – via Austerity – that would actually kill even a healthy economy,

than the assumption of mere “honest mistake” on their behalf.

The actual answer is hidden somewhere else than in the elites’ mere

ignorance or mistakes. The elites deliberately keep the 99% in Crisis

because they gain£ / € / $ trillions on the ‘Crisis business‘

[10, 11]. They keep us locked into this scheme because this way the

global elites can grab real tangible values – lands, buildings,

resources, of all countries and continents – in exchange for empty computer digits.

The most profitable business that one ever had or can ever imagine.

This is the ultimate explanation behind the historically unprecedented

inequality between the globally richest class and the rest of mankind.

This is why Banks were so willing to extend subprime loans to those

countries and individuals who will certainly default on the loan [11].

This is why central banks, even though aware of the intensifying process

of subprime loans, chose to allow it to continue; they merely pretend

it that they made “mistakes” [11] They impose a system of Debt and

Austerity on us in order to maintain the vicious cycle of Crisis so that

they could continue grabbing these assets [10, 11]. An issue of constitutional democracy, democratic rule of law and national sovereignty

When loans are given to countries via their collaborating

Governments, the demonstrated phony financial transactions entered by

these Governments are the very cause of the Odious Public Debts

accumulated in many £ / € / $ trillions on behalf of the 99%.

The most relevant implication of the Public Debts is this

consideration: Rather than exchanging empty IOUs thus accepting the

burden of Debt on behalf of their citizens upon the act of financing a

country, responsible and real democratic Governments could – and should –

create the money-supply in the very amount that is necessary to be

invested into the economy and they should make these necessary direct

investments – via Public Banking and without the burden of Public Debt

– into constructive projects, creating jobs, fostering green energy and

human-centered economies, infrastructure, affordable healthcare,

children-care, education, housing, etc.

One just can’t avoid arriving at the blatant conclusion: the acts of

those Governments who choose not to finance their own citizens, and

rather collaborate with the global financial oligarchy, come down to

deliberate destruction of countries and sheer robbery of all countries’

values. Financial world-war led by the richest 1% against the 99% across all countries.

Even though this financial world-war appears to be a class-war, as

one waged by the rich against the poor, it is not. It is neither a

class-war nor an aspect of “left” or “right” party-politics. It is not

even a question of finance and economics, since finance and economics in

this regard are mere means to wage the war.

It is not a question of ethics and morality either. It is a

constitutional, hence legal issue. All Governments who surrender their

sovereign right to devise and control their respective country’s

economic and monetary system and as elected bodies surrender their

decision-making powers in fiscal and monetary policies to unelected

bodies such as Banks, give up constitutional democracy in their country.Who surrender their country to the financial crime described herein, give up democratic rule of law. In addition, those Governments who surrender their own electorate-given rights to unelected international lobbies, give up their country’s sovereignty and surrender their country as a whole to foreign interests.

With special regard to the currently intensifying Greek crisis, a

final note. From the facts and implications analysed in this post it is

evident: it is not Greece – or any of the other affected countries who

supposedly “owe” € billions, or even trillions, to Troika (EU/IMF /ECB) –

it is the way around. The ongoing financial CRIME of unprecedented

scope and magnitude described in this post, should be investigated,

ended and prevented with utmost urgency, which however requires

reinstating the democratic rule of law in all affected countries. The

citizens of Greece – and of all countries subjected to this financial

crime – should be compensated for the financial and other damages they

suffered and/or still suffer. image: http://globalpoliticalanalysis.files.wordpress.com/2014/04/banks-and-govs-debt-fraud.jpg?w=750 Related posts:

Lakshman Achuthan, co-founder at ECRI,

discusses the low growth trend in the United States economy. He speaks

on “Bloomberg Surveillance.” (Source: Bloomberg)

Official also believes Sunday’s referendum is escalation of a Greek negotiating strategy that has gone wrong

The EU official believes the debate over debt relief is irrelevant

because creditors needed assurances that Greece did not want to provide.

Photograph: Louisa Gouliamaki/AFP/Getty Images

Debt relief was not on the table during negotiations to extend

Greece’s existing bailout programme and agree a package of reforms

needed to unlock its remaining funds, according to a senior EU official.

The official told the Guardian that debt relief was “politically highly toxic for many eurozone member states”.

Any form of debt restructuring would only be possible as part of a

new programme – which would be Greece’s third – and only after the

country provided assurances that it would really implement reformsand

demonstrate that no further relief would be needed in future.

However, even then, writing off some of the debt would be a “no-go”, the official said.

A more realistic option would be applying “very long maturities with 0 [%]-interest” on the existing debt.

The revelation is at odds with the position of the International Monetary Fund, which said earlier this week that Greece needed an extra €60bn of funds and debt relief to provide its economy with “breathing space” to stabilise.

According to the IMF’s analysis, Athens’ debts are unsustainable and

require large-scale relief: a 20-year grace period, or a haircut that

yields a reduction in debt of more than 30% of GDP.

However, the EU official believes that the debate over debt relief is irrelevant because creditors needed assurances that Greece did not want to provide.

When asked why he thought Greece had called a referendum on whether

to accept the creditors’ proposals, the official says that he believes

that the vote is an escalation of a negotiating strategy gone wrong.

First, the prime minister, Alexis Tsipras, would have been unable to get a credible agreement through parliament.

Second, the finance minister, Yanis Varoufakis, had been calculating

with 100% confidence that the EU would not allow an exit from the euro

because of political and geopolitical considerations.

Because of these two factors the Greek government pretended to

negotiate while waiting for a political solution. But a deal was close

even under these “fake negotiations”, so they chose to escalate the

situation.

Things happened too fast for game theorist [Varoufakis] to adapt, and

not only is he destroying his economy, but has made a huge tactical

mistake.

The official is adamant that if the first bailout programme had been

fully implemented, Greece would have been recovering in three to four

years like Ireland or Portugal.

Instead there were no structural reforms. This lead to “ad hoc savings” to meet fiscal targets, which are bad for growth.

(Marguerite Ward)

Fire up the grill and break out the red, white and blue cutlery. This

July Fourth is going to bring sizzling food and retail sales totaling

$6.6 billion, a 6.4 percent increase from last year, according to a survey by the National Retail Federation.

Whether it’s potato salad, barbecue meat or buns, the average

American household will spend $71.23 on food items this year for

Independence Day, up from last year’s average of $68.16.

The uptick in spending is likely a mix of factors including higher food prices and a general trend in more consumer spending. The consumer price index for grocery store food items—a measure of price change—is 0.6 percent higher than last May.

The increased July 4 food spending comes despite a 60 percent decrease in the cost of propane on a year over year basis and a price drop to certain foods like poultry and beer.

Most of the data on people’s plans from this year was in line with last year’s findings, with a slight uptick in those attending a barbecue, cookout or picnic.

Like last year, about 11 percent of survey responders won’t be celebrating July Fourth at all.

The National Retail Federation’s 2015 Independence Day survey,

conducted by Prosper Insights & Analytics, surveyed 6,431 consumers

between June 2-9, 2015.

‘Huge’ Holiday for Watermelon Growers

For several food industries, July 4 means the beginning of a crucial sale period.

“July Fourth is huge for us,” said Bob Morrissey, executive director

of National Watermelon Association, a group of about 500 growers. With

the exception of those impacted by severe rainfall in Texas, most

watermelon growers have seen a good season, said Morrissey.

Hot dog sales also peak on July 4 weekend.

“It’s the single biggest weekend for hot dog sales,” said Eric

Mittenthal, vice president of public affairs at the National Hot Dog and

Sausage Council.

About 150 million hot dogs are sold over the July 4th weekend, according to Mittenthal.

Hamburgers won’t be cheap this year. Ground beef costs about 7

percent more this year, accounting for inflation at $4.136 per pound.

This is just below the 10 year historical high of $4.235 per pound this

past January, according to theBureau of Labor Statistics.

Chicken prices have inched down this year the aftermath of an avian

flu outbreak. With multiple countries banning or partially banning U.S.

poultry exports, there’s been downward pressure on retail chicken

prices, according to the USDA. Chicken prices are down about 2 percent

from last year, with inflation factored in.

Party-throwers will be also paying slightly less for beer than they did last year. Prices of all malt products are down about 4 percent compared to last year.

For backyard grillers and celebrity chefs alike, this year’s Fourth of July will mean a lot of delicious food purchases.

(ASHEVILLE) If

you find yourself suffering from sticker shock in the grocery aisle,

it’s not your imagination. A confluence of factors, environmental and

otherwise, is driving up prices for consumers.

Drought in California, where virtually all U.S. almonds and

the majority of broccoli, garlic and spinach is grown, is tinkering with

produce prices. Egg prices are climbing. Not even orange juice is safe,

with a citrus greening disease causing bitter fruit and low production.

Even coffee is stressed, according to Waking Life Espresso

cafe owner Jared Rutledge, who said a devastating fungus called coffee

leaf rust is causing bean prices to rise.

Clearly the breakfast table is suffering, though not on the

bacon front; pork prices are falling, one of the few sectors where

there’s good news.

“There have been different things in different industries,

but I think when you put it all together, it means overall, what people

are spending on groceries has increased,” said Leah McGrath, Ingles

dietitian.

Eggs in particular have lately been bedeviling consumers.

Avian flu has decimated almost 10 percent of the country’s population of

laying hens, with wholesale prices reaching record levels on the

national market, according to local egg farmer Mike Brown of Farside

Farms.

“About six weeks ago, eggs started going up five to six

cents an egg a day, going as far as $2.50 a dozen wholesale — the

highest it’s ever been,” Brown said.

Avian influenza, also known as the bird flu, is a virus that

infects wild birds and domestic poultry, including chickens and

turkeys. The most devastating form of the flu, HPAI, is a merciless and

swift bird killer.

“When you have one sick chicken, you’re out of business,” Brown said. “You lose them all.”

So far, the flu has resulted in the deaths of nearly 50 million birds, largely in the Northwest and Midwest.

North Carolina is taking preventative measures to keep the

disease from infiltrating the state, canceling poultry shows and

disallowing fowl at state fairs after Aug. 1.

Even though the spread of the flu is slowing, eggs are still

pricy as farmers try to recover. And even if prices return to normal

this summer, there could be another epidemic as soon as cooler weather

spurs migratory movements of wild birds, spreading disease again.

For now, poultry farmers are in rebuilding mode, Brown said.

“It will take six months minimum to get those facilities back into

production,” he said.

It’s not just eggs that have consumers dropping extra cash at the store. Wholesale and retail beef is also at record highs.

“The beef cattle markets have soared due to a shortage of

cattle,” Brown said. “They’re a long process; you can’t build them back

overnight.”

Cattle inventory is down because the expense of raising,

slaughtering and selling steers for meat at market is high, while the

return is basically equivalent to what a farmer might fetch selling

cattle in the stockyard.

“It’s a no-brainer,” Brown said. “You can just collect your check and go about your business.”

Eating their egg prices

Retail food operations rarely have the same options as

wholesalers. At least two local bakers say they’re eating the rising

cost of one of their most important commodities.

Karen Donatelli of Karen Donatelli Cake Designs is accustomed to fluctuations in cost, she said.

“We had heavy cream not long ago, and about four or five months ago, the butter prices were going through the roof,” she said.

But changing menu prices to reflect a volatile market is

simply not feasible. Donatelli raised her prices shortly after the

holidays, and doesn’t plan to do it again any time soon.

“I feel like we’re going to try to weather the storm,” she

said. “Sometimes prices do come back down, and we’ll be right at where

we’re supposed to be.”

At True Confections in the Grove Arcade, Carole Miller has

seen prices for eggs soar more than 50 percent, climbing from $24 to $37

a case in one week.

But she’s not raising her prices either, she said. “It

shouldn’t take that long for the next crop of layers to mature, but that

was a big bite out of my food budget.”

Why are customers more willing to weather rising prices at

the grocery store, but less tolerant of climbing restaurant prices?

That’s just the way it is, Miller said. “Life’s not fair.”

John Brinker, scanning coordinator for the French Broad Food

Co-Op in downtown Asheville, is one of the few grocers who could say

his store would not see fluctuating egg prices.

“We tend to eat a little profit on eggs because you really

want to give your customer a good, low price on eggs,” he said. “We may

not be raising our price as much on those as our competitors might be.”

But the co-op’s egg prices haven’t changed much, he said, largely because they’re coming from local sources.

Brinker couldn’t say the same for almonds and almond

products. “Almond milk, bulk almonds, almond crackers … are going up in

direct proportion to the direness of the news from California about the

water shortage,” he said. “My assumption has been that there’s a direct

correlation there.”

Going nuts over prices

At True Confections, Miller said she’d be phasing out the use of almond milk soon, replacing it with soy products.

“It’s a more sustainable crop,” she said.

California, stricken by yearslong drought, produces more

than 80 percent of the world’s almonds, and the trees’ water usage is

substantial.

The New York Times recently estimated that it takes 15.3

gallons to produce 16 almonds. Limits on water for California farmers

means more stress for almonds, which translates to lower production and,

eventually, higher prices.

McGrath said Ingles is working to keep the prices down on

all produce, which may mean sourcing from other growing areas such as

Texas and Mexico.

“But there’s so many things going on,” she said. “There’s a greening problem in Florida that’s devastating the orange crops.”

Last year, Florida produced just half of the oranges it had a

decade earlier. According to information on the website of Uncle Matt’s

Organic orange juice, once a tree is infected, there is no cure. It’s

already devastated millions of acres of citrus crops throughout the

United States and abroad.

The rapid decline of tree health has severely affected the

$11 billion combined citrus industry in Florida and California, putting

many growers out of business.

Currently, the rise of citrus greening has significantly

reduced supply and driven up production costs, and growers and shoppers

alike are feeling the pinch.

“There’s these problems in a lot of crops right now that

have food suppliers wondering what’s next,” McGrath said. “If we have a

drought problem in California and a greening problem in Florida, where

are we going to get our citrus crop?”

For now, McGrath said to work on curbing food waste and shopping smarter to help keep grocery bills down.

“We spend so little on food in comparison to other developed

nations, but I think it’s so noticeable because people are on a more

fixed income,” she said. “But we can be a nation that really wants the

smorgasbord. We want all you can eat at one cost.”

At least for now, going shopping might require biting the

bullet. With wages flat and the cost of goods rising, sometimes that’s

easier said than done.

A look at 2015 food prices from the USDA

• Wholesale beef prices rose, increasing 0.8 percent on the month and are now up 12.3 percent year over year.

• Prices for farm-level eggs increased 35.4 percent from April to May; prices are now up 9.2 percent from May 2014 levels.

• The

ongoing drought in California has raised concerns about rising produce

prices at supermarkets or grocery stores. Prices for both farm-level

fruit and vegetables rose in May. Farm-level fruit prices increased 3.9

percent in May, while farm-level vegetable prices rose 5.7 percent month

over month — an indication that retail produce prices could further

increase in the coming months.

America is better off when President Obama is out on the stump

bloviating and boasting rather than in Washington actively doing harm.

But the whoppers he just told the students at the University of

Wisconsin are beyond the pale. Said our spinmeister-in-chief:

And the unemployment rate is now down to 5.3 percent.

(Applause.) Keep in mind, when I came into office it was hovering around

10 percent. All told, we’ve now seen 64 straight months of private

sector job growth, which is a new record — (applause) — new record — 12.8 million new jobs all told.

That’s a pack of context-free factoids. There is still such a thing

as the business cycle, and only economically illiterate hacks—-like

those who work on the White House speech writing staff—-would measure

anything from an all-time momentary bottom that happened to occur during

Obama’s second year in office. What counts is not that we’ve had a

bounce after a terrible bust, but where we are now on a trend basis.

The answer is absolutely nowhere!

We are now 29 quarters from the pre-crisis peak and total non-farm

labor hours utilized by the US economy are no higher than they were in

Q4 2007. In other words, if you use a common unit of measure—–labor

hours rather than job slots which treat coal-miners and part-time pizza

delivery boys alike—–there have been no newunits

of employment at all. Our teleprompter reading President is actually

tooting his own horn about recycled hours and “born again” jobs and

doesn’t even know it.

image:

http://research.stlouisfed.org/fredgraph.jpg?hires=1&type=image/jpeg&chart_type=line&recession_bars=on&log_scales=&bgcolor=%23e1e9f0&graph_bgcolor=%23ffffff&fo=verdana&ts=12&tts=12&txtcolor=%23444444&show_legend=yes&show_axis_titles=yes&drp=0&cosd=2007-09-01&coed=2015-01-01&height=350&stacking=&range=Custom&mode=fred&id=HOANBS&transformation=lin&nd=&ost=-99999&oet=99999&lsv=&lev=&scale=left&line_color=%234572a7&line_style=solid&lw=2&mark_type=none&mw=2&mma=0&fml=a&fgst=lin&fgsnd=2007-12-01&fq=Quarterly&fam=avg&vintage_date=&revision_date=&width=670

And, no, he can’t take credit for digging us out of the hole created

by the Great Recession, either. The long, slow climb back to square one

shown in the chart above was due to the natural resilience of our

capitalist economy—notwithstanding the tax, regulatory and massive debt

hurdles that Washington policies have thrown at it.

The truth of the matter is that America’s employment machine has been

failing for this entire century. As shown below, the number of non-farm

labor hours utilized during the most recent quarter was only 1% higher

than in the spring of 2000—-way back when Bill Clinton still had his

hands on things in the Oval Office. In short, we have gone through two business cycles and have essentially added zero new employment inputs to the US economy.

And that marks a sharp and devastating reversal of previous trends. In

fact, the BLS’ own data convey an out-and-out crisis that the President

should have been lamenting, not a cherry-picked simulacrum of growth

based on born again jobs slots.

Thus, during the comparable 29 quarters after the 1990 business cycle

peak (Q2 1990 to Q3 1997) non-farm labor hours had increased by 12% and during the same period of time after the 1981 peak (Q3 1981 to Q4 1988) labor hours expanded by 17 percent. That’s what employment growth used to look like, and absolutely nothing like that has happened on Obama’s watch.

image:

http://research.stlouisfed.org/fredgraph.jpg?hires=1&type=image/jpeg&chart_type=line&recession_bars=on&log_scales=&bgcolor=%23e1e9f0&graph_bgcolor=%23ffffff&fo=verdana&ts=12&tts=12&txtcolor=%23444444&show_legend=yes&show_axis_titles=yes&drp=0&cosd=1981-03-12&coed=2015-01-01&height=450&stacking=&range=Custom&mode=fred&id=HOANBS&transformation=lin&nd=&ost=-99999&oet=99999&lsv=&lev=&scale=left&line_color=%234572a7&line_style=solid&lw=2&mark_type=none&mw=2&mma=0&fml=a&fgst=lin&fgsnd=2007-12-01&fq=Quarterly&fam=avg&vintage_date=&revision_date=&width=670

When you get right down to it, however, even labor hours do not fully

capture the actual jobs disaster happening in America. That’s because

we keep shedding high productivity hours in the full-time jobs sector

in favor of lower skill, low pay gigs in bars, restaurants, Wal-Marts

and temp agencies.

So notwithstanding another month of 200,000 plus headline job gains,

here’s where we actually are. The number of breadwinner jobs—–full-time

positions in energy and mining, construction, manufacturing, the white

collar professions, information technology, transportation/distribution

and finance, insurance and real estate—-is still 1.7 million below the

level of December 2007; in fact, it is still lower than it was at the

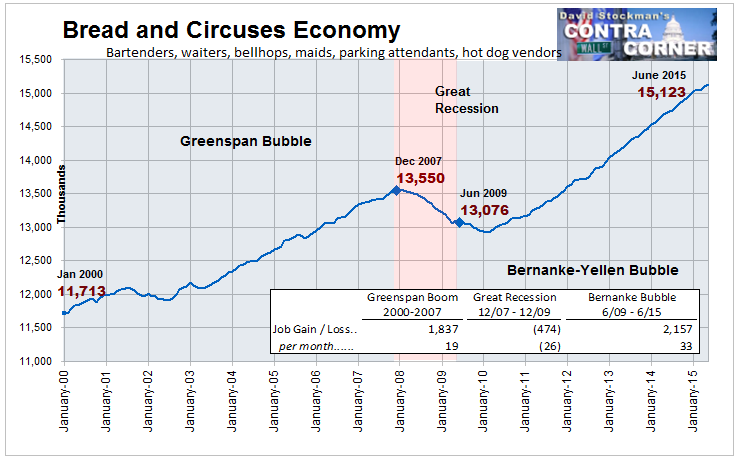

turn of the century. image: http://davidstockmanscontracorner.com/wp-content/uploads/2015/07/breadwinner1-480x299.png

There is no mystery as to how the White House and Wall Street

celebrate year after year of “jobs growth” when the long-term trend of

full-time family supporting employment levels is heading south. Its

called “trickle-down economics”, and not of the good kind, either.

What is happening is that the Keynesian money printers at the Fed are

fueling serial financial bubbles. This generate a temporary lift in the

discretionary incomes of the top 10% of households, which own 85% of

the financial assets, and the next 10-20% which feed off the their

winnings. Accordingly, the leisure and hospitality sectors boom,

creating a lot of job slots for bar tenders, waiters, bellhops, etc.

I call this the “bread and circuses economy, but it has two problems.

Most of these slots generate only about 26 hours per week and $14 per

hour. That’s about $19,000 on an annual basis, and means these

slots constitute 40% jobs compared to the breadwinner category at about

$50,000 per year. Besides that, a soon as the financial bubble goes

bust, these jobs quickly disappear. image: http://davidstockmanscontracorner.com/wp-content/uploads/2015/07/breadcircus-480x299.png

This is reason enough for Obama to pipe down on the boasting, but he

actually went in the opposite direction claiming a big recovery in

manufacturing jobs.

And after a decade of decline, thanks to some of the

steps we took…….we’ve added nearly 900,000 new manufacturing jobs.

Manufacturing is actually growing faster than the rest of the economy.

(Applause.)

But that one is not even a whopper; its a bald-faced lie. There has

not been one “new” manufacturing job created during Obama’s term in

office; and, in fact, the 12.3 million manufacturing jobs

reported for June was still 10% below the level of December 2007, and

nearly 30% lower than the 17.3 million manufacturing jobs reported in

January 2000.

That is not evidence of a trend reversal; its an exercise in political hogwash.

Indeed, if you take the entire high productivity, high pay goods

production sector—-energy, mining, manufacturing and construction—the

trend is even worse. As shown below, the 19.6 million goods producing jobs in June was 5 million lower than in January 2000.Is there any wonder that the median real household income has declined by 7% over the last 15 years? image: http://davidstockmanscontracorner.com/wp-content/uploads/2015/07/goods-480x299.png

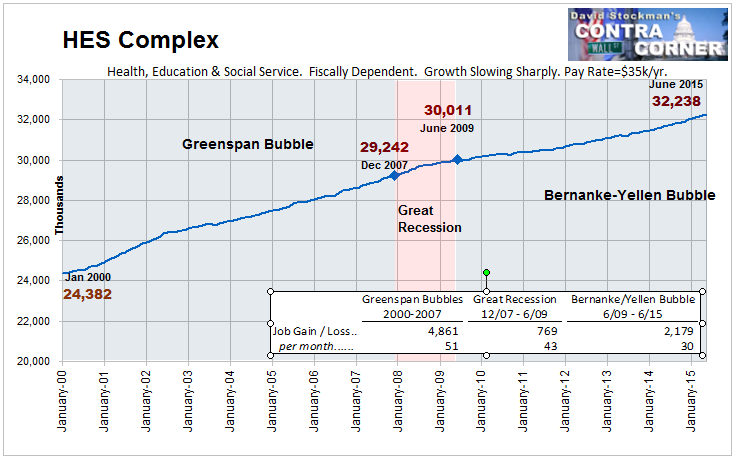

Here’s the real truth beneath the bloviation issuing from stumping

politicians and Wall Street stock touts alike. The June BLS report

showed that the HES Complex (health, education and social services)

generated another 48,000 jobs in June. This figure is nearly dead on the

42,000 monthly average for this sector since the turn of the century.

The minor problem with that trend is these jobs pay on average only

$35,000 per year—–a level that does not remotely support a middle class

standard of living, especially after payroll and income taxes are

extracted from this gross pay figure.

The much bigger skunk in the woodpile, however, is that these jobs

are almost entirely fiscally dependent. Yet the public sector in America

is broke, and the total public debt just keeps on climbing higher.

To wit, the 32.2 million jobs in the HES Complex are funded by $1.5

trillion annually of Medicare, Medicaid and other health and social

services funding. On top of that there is also about $1 trillion of

public sector education funding, $200 billion per year of government

guaranteed student loans and $200 billion annually in tax subsidies for

employer provided health plans. image: http://davidstockmanscontracorner.com/wp-content/uploads/2015/07/HES-480x299.png

In effect, the public sector borrows and taxes to create low

productivity jobs among the nation’s highly inefficient, wasteful and

monopolistic health and education cartels—- but in the process squeezes

everything else. In fact, there have been virtually no new jobs—even on a

headcount basis—–outside of the HES Complex during the entirety of the

21st Century to date. image: http://davidstockmanscontracorner.com/wp-content/uploads/2015/07/nfp-hes-480x300.png

One of these days the public sector is going to exhaust its capacity

to tax and borrow, and to thereby finance job growth even in the HES

Complex. Needless to say, Washington and Wall Street will be as clueless

then as they are now.

Meanwhile, the White House whoppers will keep on coming.

by Golem XIV

If the Greeks were to vote ‘No’ what would happen next? Well no one

can say. But here is a quick thought on what I hope the Greek government

might have been exploring if they are excluded from the euro. It’s just

food for thought nothing more.

They have to be prepared to have a currency that does not depend on

Europe supplying Euros. So they will need another currency – hopefully

their own. I think we can be sure no western company has been printing

them. There are few such companies and there is, I think, no possibility

that they would be able to keep secret a contract from Greece. But

both Russia and China can print notes. So would it not have been prudent

to ask Putin to print up plane loads of Drachma and be prepared to fly

them in?

Who would back this currency? Greece is not Great Britain with a

long established reasonably trusted currency backed by a big slice of

global financial trade. So I do not think they could launch an orphan

currency which the drachma would be if it did not have some relation to a

major clearing or reserve currency.

For all Obama has, apparently, lobbied the EU to be more conciliatory

towards Greece I am not sure he would leap at the chance to help Greece

with its debt. He might of course. A chance to reenforce US power in

that part of the world. But he already has power there so I doubt he

would be willing to ‘pay’ much. Russia and China, however would gain

much more by having Greece as a beach head in to the EU and, more

importantly, into Nato.

Russia has already signed a large gas pipeline deal with Greece.

The deal will make Greece the European terminal for the so-called

TurkStream which would be a southern counterpart for the NordStream

which runs under the Baltic and has its European terminal in Germany.

This pipeline would bring Russian gas to Europe cutting out Ukraine. A

nice end run around the Western puppet government/influence in Ukraine

(you decide which one you prefer). It will also bring closer Russian

ability to pipe gas from further east and from Iran. Which would also be

an end run round the southern front of the Great Gas War being fought

in Syria.

Earlier this year Russian also signed a deal with Cyprus to give Russian ships access to Cypriot ports.

So It would make sense to me that Russia might see advantage in

helping Greece in the event of a ‘No’ vote. But I do not think Russia

is in much of a position to help financially. Their help can be

practical and trade in gas and their reward is military. Greece and

Cyprus together could perhaps get themselves a chip in the big game by

being the key to allowing Russia to project military power in to Nato.

Which raises the intriguing possibility that Russia might ask Greece

is they could station some military hardware in Greece. Not something

Greece would lightly say yes to. BUT if there was a ‘no’ vote and then

Europe tried to get really vindictive or even started sabre rattling

about ‘radical’ possibly ‘illegitimate’ leftist governments (AKA Syriza)

might Syriza gain some advantage by letting it be known they might

consider letting Russia dock missile carrying warships in their ports,

or allow certain early warning systems on their territory? Or if the

Great Gas War, which is surely the new Cold War, where Ukraine is the

new Germany divided East and West (all we need now is a wall somewhere),

heats up and the US does deploy missile systems there, would Russia

think it advantageous to befriend Greece so they could ask an indebted

Greek government to allow Russia to retaliate with missiles right in the

heart of Europe?

I realise this is pure speculation but it’s fun and I think it’s good

to think the unthinkable now and again. Our leaders regularly do the

unthinkable. We should at least think it.

Anyway, I can see reasons why Russia would think it to their advantage to help Greece and have favours to call in.

Then there is China. China is too far away for military pretensions

in the Med. Better to leave that to Russia. What China has is money.

Just yesterday the director of the Quantitative Finance Department at

China’s Institute of Quantitative and Technical Economics, Mr Fan

Mingtao, said in an interview,

“I believe there are two ways to give Greece Chinese aid.

First, within the framework of the international aid through EU

countries. Second, China could aid Greece directly. Especially

considering the Silk Road Economic Belt and the Asian Infrastructure

Investment Bank. China has this ability,”

I don’t know if this is pure kite flying but it’s interesting.

The Asian Infrastructure Investment Bank (AIIB) is a China led rival to

the US led World Bank. America was very against it and hugely put out

when various European and other countries defied America and merrily

joined it. Led by Britain

which is a founder member. This is a major step in China’s policy of

projecting power abroad but also a major step in its campaign to either

have the Yuan as a new reserve currencyor position a new currency in which China and the Yuan are constituent backers.

Again this is all speculation. But China is sick of America excluding

it from governance of the World Bank and the IMF. Plus China will soon

need – not just want – but need the Yuan to be at the very least a much

more widely used settlement currency if not a full blown reserve

currency. The reason I suggest this, is because of China’s ballooning

domestic debt problem. Back in 2011 I wrote about the way regional

governments were largely outside of direct and effective central control

particularly their issuance of debt (Making the New Sub Prime – Backdoor to China) and how that debt was going bad (China – 10.7 trillion Yuan of debt going bad).

That analysis is, I think, now vindicated. That regional debt has now

blow up and is on the point of taking many of China’s banks down with

it. The central chinese government now has, I think, little choice but

to backstop all that regional debt. The hope is that this will save

their regional governments from defaulting and also bail out all the

banks that are holding that debt and would be bankrupted by such a

default. Essentially this is a colossal bank bail out much like they

were obliged to do back in the 90?s and we did a decade later. I am not

alone in thinking this is the dynamic at play. As reported in the Wall

Street Journal and ZeroHedge,

“The debt swap is effectively a debt restructuring for

banks,” said Zhu Haibin, J.P. Morgan Chase & Co.’s chief China

economist.

Because the central government is ultimately responsible

for guaranteeing local government debt, and because yields on the new

muni bonds are so close to those on treasurys, the newly issued local

government bonds are really just treasury bonds, meaning that, in

essence, the supply of Chinese government bonds is set to jump by CNY2

trillion in the coming months. If all of the local government debt ends

up being refinanced, the end result will be the equivalent on CNY20

trillion in additional treasury supply.

What I foresee is that China’s new regional debt and bank bail out is

forcing it in to what is essentially QE. The flow of Yuan is going to

be vastly increased. A good idea would be to have lots of people ‘need’

these yuan and be keen to soak them up. That is what would happen if the

Yuan becomes a new reserve currency or, failing that, if there is at

least a greater use of the Yuan as a settlement currency for major

international trades.

Which brings me to my speculation about Greece and the report quoted

above about China helping Greece via the new AIIB. Might it not

suit China, with its coming flood of new Yuan, to offer Greece a hand

with a few Yuan. Greece might offer to conduct all its foreign trade in

Yuan rather than dollars or Euros. Greece would benefit because it would

not be beholden to America or Europe for a flow of their currencies. It

could look to China instead. Russian would be happy with this because

it has a settlement agreement with China. Any gas pipelie work could be

financed in Yuan with chinese government backed Yuan loans. The AIIB

could help Greece out with a loan to allow it to operate. Such a loan

would not be blockable from Europe or America. Greece could default and

still have operating money. China could spin it as almost humanitarian

aid: The Chinese people reaching out to the desperate, impoverished but

brave Greeks when the wicked capitalist Europeans would not.

Greece would survive, have new powerful friends, have bargaining

chips that neither Europe nor America could ignore , China would have

projected the use of the Yuan right in to Europe and Russia would have

more than a toe-hold for military power right inside Natio.

If I was Tsipras or Varoufakis I would be on the phone right now.

The International Monetary Fund is one of the most secretive and powerful organizations in the world.

They monitor the financial health of more than 185 countries… they

establish global money rules… and provide “bail-out” assistance to

bankrupt nations.

And on Oct 20th of this year, the IMF is expected to announce a

reserve currency alternative to the U.S. dollar, which will send

hundreds of billions of dollars moving around the world, literally

overnight.

According to Juan Zarate, who helped implement financial sanctions

while serving in George W. Bush’s Treasury department, “Once the [other

currency] becomes an alternative to the dollar, rules of the game begin

to change.”

And Leong Sing Chiong, Assistant Managing Director at a major central

bank, said this dollar alternative “is likely to transform the

financial landscape in the next 5-10 years.”

According to currency expert, Dr. Steve Sjuggerud (recently featured on CNBC, and Bloomberg),

“I’ve been active in the markets for over two decades

now… but I’ve never seen anything that could move so much money, so

quickly. Hundreds of billions of dollars could change hands in a single

day after this announcement is made.”

“The announcement will start a domino effect, that will basically

determine who in America gets rich in the years to come… and who

struggles.”

Dr. Sjuggerud says if you own any U.S. assets—and that includes

stocks, bonds, real estate, or just cash in a bank account–you should be

aware of what’s about to happen, and know how to prepare.

Experts say this announcement, expected Oct. 20th, could trigger one of the most profound transfers of wealth in our lifetime.

But as Dr. Sjuggerud explains, if you understand what’s taking place, and can get ahead of this move, you can not only protect your money, but safely make a small fortune in the next few years.

Dr. Steve Sjuggerud and his research team have put together a full

analysis on not only what this announcement means for the economy, but

also how it could affect you, your money, and your investments,

personally.

As expected (and as tipped here

on Thursday immediately after news broke that an IMF study conducted

prior to the imposition of capital controls in Greece suggests debt

relief for Athens is necessary if anyone hopes to create some semblance

of sustainability), Greek PM Alexis Tsipras is now leaning hard on

voters to carefully consider the fact that one-third of the troika has

effectively validated the Greek government’s position on creditor

writedowns.

“This position was never proposed to the Greek government over the five months of negotiations, wasn’t included in final offer tabled by creditor institutions, on which people are going to vote on July 5,”

Tsipras said in a televised address, making it clear to Greeks that the

proposals they are voting on effectively do not reflect the views of

the institution that is perhaps the country’s most influential

creditor. “This IMF report justifies our choice not to accept an agreement which ignores the fundamental issue of debt,” he added, driving the point home.

Clearly, this puts Europe, and especially Germany, in a rather

unpalatable position. Many EU officials have for months insisted that

IMF participation is critical if the Greeks hope to secure a third

bailout. The IMF meanwhile, has stuck to a position first adopted years

ago (something we’ve noted in these pages multiple times of late);

namely that official sector writedowns will ultimately be necessary if

Brussels hopes to finally put the Greek tragicomedy to bed. This means

Brussels (and Berlin) will now be forced to choose between IMF

involvement (which the EU says is a precondition for a deal) and

haircuts (which the EU says aren’t possible).

Here’s Barclays - a major investment bank - with its own confirmation that the IMF may have assured a No vote over the weekend.

The document basically argues that OSI is a necessary condition in order to secure sovereign solvency with a high probability.

This means that before the IMF re-engages in any lending activities

with Greece, OSI will be required in the form of NPV debt relief.

The timing of

the publication of this report it is very important. Debt relief is

something that the Greek authorities have repeatedly demanded;

therefore, in a way this report can be interpreted as the IMF backing

the Greek government's demands. By extension, it could also be

interpreted as supportive of a 'No' vote, which is what the Greek

government is campaigning for.

We agree broadly with the analytical content of the report and the need for further OSI. This

is in fact hardly new news. Europe has recognized since November 2012

that Greece needs further OSI to make debt dynamics sustainable with

high probability. The IMF advice of an NPV haircut via a debt maturity

extension (to 40 years) is in line with expectations.

However, the critical point is that the IMF now requires

debt-relief before it engages in a new programme, which confronts

Europeans with a tough political decision. Many in Europe,

including Germany, considered OSI as a future carrot in exchange for

reforms today following good programme execution. Debt relief was

conceived as a part of a third programme to be negotiated possibly with a

new Greek government.

At the same time, Germany has been adamant about the

importance of IMF involvement in any financial support programme for

Greece. Thus, Germany will now be confronted with a tough choice: to

deliver on the IMF's demand, ie to engage in OSI negotiations in the

form of NPV debt relief, or give up on IMF involvement. We

believe that there is mounting support across other member states for

the OSI discussion, therefore, we believe that Germany may not be able

to resist such discussions any longer.

"I am guessing that this is a negotiating tactic ahead of the

negotiations for a new programme for Greece. The IMF very well knows

that a debt write-off is out of the question," one unnamed EU official

told MNI. “The numbers are quite high, not in line with our assessment and our baseline scenario.

We are examining different scenarios for the day after the referendum

and provided the vote is Yes, we are ready to come up with solutions.

But it is not going to be easy to agree. Certainly this report does not make it any easier," another source said.

It's easy to see why Europe is reluctant to accept the IMF's assessment. As discussed at length on Thursday, were Europe to go down the OMI road, Brussels would be opening Pandora's Box. Here's why:

By now it should be clear to all that the only reason why Germany

has been so steadfast in its negotiating stance with Greece is because

it knows very well that if it concedes to a public debt

reduction (as opposed to haircut on debt held mostly by private entities

such as hedge funds which already happened in 2012), then the rest of

the PIIGS will come pouring in: first Italy, then Spain, then Portugal,

then Ireland.

The problem is that while it took Europe some 5 years to transfer

a little over €200 billion in Greek private debt exposure to the public

balance sheet (by way of the ECB, EFSF, ESM and countless other ad hoc

acronyms) at a cost of countless summits and endless negotiations, which

may or may not result with the first casualty of the common currency

which may prove to be reversible as soon as next week, nobody in Europe harbors any doubt that the same exercise can be repeated with Italy, or Spain, or even Portugal. They are just too big (and their nonperforming loans are in the hundreds of billions).

As for the IMF's position, Barclays notes that a permanent default by

Greece would not be a trivial event, thus providing further incentive

for the Fund to push for EU writedowns:

With the IMF’s total resources being roughly USD760bn – USD420bn of which are considered the ‘forward commitment capacity’ – the IMF has the firepower to ‘survive’ a permanent default of Greece while maintaining sufficient resources to be able to lend out fresh credit for countries in need. However,

it would make a significant dent in the ongoing IMF finances – eg, the

interest paid on IMF loans is used to cover IMF’s operational cost – and

would very likely create intense debate about Europe’s relationship

with the IMF and the balance of power between DM and EM members. One

question could also be whether or not the euro area IMF members should

not in some way be liable for the outstanding Greek debts. In turn, this

would also intensify a debate about the sharing of

liabilities/solidarity within the euro area and the EU.

So, thanks to a well-timed IMF report, Tsipras can now frame Sunday's

plebiscite as a simple Yes/No vote on Greece's debt pile, which makes

it far easier to vote "no." "Do you think Europe should forgive your debt, check box 'Yes' or 'No'."

That should be an easy choice, although it depends upon the Greek

public understanding the significance of the IMF's position which, as

indicated above, Tsipras is doing his very best to facilitate. The

bottom line: Sunday's vote is about whether Greece will agree to remain

a debt colony of Germany, pardon Europe, even as the IMF (and, paradoxically, Germany) agrees with Athens that the country's debt is unsustainable.

"No" means a lot of pain now and recovery later. "Yes" means less pain now but no hope of recovery ever. * * * Choose wisely...

(CNSNews.com) - A record 93,626,000 Americans 16 or older did not

participate in the nation’s labor force in June, as the labor force

participation rate dropped to 62.6 percent, a 38-year low, according to

the Bureau of Labor Statistics.

In June, according to BLS, the

nation’s civilian noninstitutional population, consisting of all people

16 or older who were not in the military or an institution, hit

250,663,000. Of those, 157,037,000 participated in the labor force by

either holding a job or actively seeking one.

The 157,037,000 who

participated in the labor force equaled only 62.6 percent of the

250,663,000 civilian noninstitutional population, the lowest labor force

participation rate seen in 38 years. It hasn’t been this low since

October 1977 when the participation rate was 62.4 percent.

Another

93,626,000 did not participate in the labor force. These Americans did

not have a job and were not actively trying to find one.

Of the

157,037,000 who did participate in the labor force, 148,739,000 had a

job, and 8,299,000 did not have a job were actively seeking one—making

them the nation’s unemployed.

The 8,299,000 job seekers were 5.3

percent of the 157,037,000 actively participating in the labor force

during the month. Thus, the unemployment rate was 5.3 percent which

dropped from the 5.5 percent unemployment seen in May.

The number

of employed Americans dropped from 148,795,000 in May to 148,739,000 in

June, a decline of 56,000. The number of unemployed Americans also

dropped over the month from 8,674,000 in May to 8,299,000 in June, a

decline of 375,000.

File photo shows a Canadian dollar coin. Two major banks say the country is headed for recession in the first half of 2015.

The US-based Bank of America Merrill Lynch and Canadian-based Nomura

Bank both released statements on Thursday, warning of a financial slump

for the economy of Canada.

An economic recession is defined as two consecutive quarters of economic contraction.

Canada’s economic growth rate shrank 0.6 percent at an annualized rate in the first quarter of the 2015 fiscal year.

"The

economy has surprised to the downside this year and appears to have

entered a recession in 1H 2015, even after policy easing in January,"

the Bank of America Merrill Lynch economist, Emanuella Enenajor, said.

Canada

is the 14th richest country in the world based on purchasing power

parity (PPP). It is also the world’s fifth biggest oil producer.

The country, however, has been hard hit by a recent slump in global oil prices because of a glut in the global supply of crude.

Analysts

say the downturn is also likely to hit the Canadian dollar, which could

drop down to 70 cents on the US dollar by the end of the year.

HDS/MHB/SS

(NaturalNews) Banks around the world are no longer the quaint little

savings-and-loan depositories of yesterday. Today, most of them are

owned or co-opted by giant mega-wealthy criminal conglomerates that

charge customers for everything from cash deposits to ATM fees.

One

Western country finally figured out that allowing these criminal

enterprises to continue operating business as usual was hurting growth

and destroying its economy, so its government decided to make some

serious reforms.

Instead of bailing out the big criminal banking enterprises, Iceland instead chose to try, convict and jail criminal banksters. And as a result, the country has the fastest recovering economy in all of fiscally moribund Europe.

Public faith being restored with economy

As reported by The AntiMedia:

After

Iceland suffered a heavy hit in the 2008-2009 financial crisis, which

famously resulted in convictions and jail terms for a number of top

banking executives, the IMF now says the country has managed to achieve

economic recovery—"without compromising its welfare model," which

includes universal healthcare and education. In fact, Iceland is on

track to become the first European country that suffered in the

financial meltdown to "surpass its pre-crisis peak of economic

output"—essentially proving to the U.S. that bailing out "too big to

fail" banks wasn't the way to go.

What is unfortunate is that Iceland

seems to be the lone exception in how the country chose to handle the

economic disaster: Rather than commit hundreds of billions in currency

to preserving what was obviously a failed business model, the government

simply let the banks fail, a decision which resulted in about $85

billion worth of defaults.

But that figure nevertheless gave the

government ample justification to prosecute and convict a number of bank

executives over a raft of fraud-related charges. And while the decision

to proceed in that manner shocked a number of governments and financial

"experts" at the time, it was a gamble that has since paid off.

Contrast

Iceland's decision with the U.S. decision to bail out its global banks

and allow the bank executives to get away with defrauding the country of