(Ron Haskins)

Of all the failures of recent Congresses and Presidents, none is more

important than their failure to deal with the nation’s long-term debt.

Although Congress tied itself in knots trying to address the problem,

the growth of debt remains, in the words of the Congressional Budget

Office, “unsustainable.”

Debt figures tell part of the story. When the Great Recession hit,

the federal debt was equal to about 40 percent of GDP. But to fight the

recession, Congress enacted an $800 billion dollar stimulus bill.

Stimulus spending, combined with already enacted spending and tax

policy, resulted in four years of trillion dollar deficits. As a result,

the debt ballooned to 78 percent of GDP in 2013, almost twice the

pre-recession level. The annual deficit is now declining at a stately

pace, but by 2016 it will begin increasing again, and by 2020 under

CBO’s alternative fiscal scenario, we will once again return to annual

deficits above a trillion dollars, thereby once again greatly increasing

the national debt.

The accumulation of debt should prevent federal policymakers from

feeling any sense of accomplishment. In fact, CBO estimates that the

debt will be well over 100 percent of GDP by 2039 under conservative

assumptions about spending and revenue. When CBO incorporates its

estimates of the impact of the continuing large federal deficits on the

nation’s economy, it estimates that the accumulated debt held by the

public will reach an astounding 180 percent of GDP by 2039. One wonders

if members of Congress or the President read these CBO reports.

What’s the word for our fiscal situation? Stunning? Shocking?

Desperate? In recent testimony before the Senate Budget Committee,

Boston University Economics Professor Laurence Kotlikoff, in effect,

told the Committee that all of these terms are pathetically inadequate

to describe our true fiscal situation. In compelling testimony,

Kotlikoff argues that the federal fiscal situation is much worse than

the CBO estimates let on. The reason is that CBO’s debt estimates do not

take into account the full financial obligations the government is

committed to honor, especially for future payments of Social Security,

Medicare, and interest on the debt. He asserts that the federal

government should help the public understand the nation’s true fiscal

situation by using what economists call “the infinite-horizon fiscal

gap,” defined as the value of all projected future expenditures minus

the value of all projected future receipts using a reasonable discount

rate.

What difference does the fiscal gap approach make in our

understanding of the true federal debt? CBO tells us that the national

debt was a little less than $13 trillion in 2014. But the fiscal gap in

that year as calculated by Kotlikoff was $210 trillion, more than 16

times larger than the debt estimated by CBO and already judged, by CBO

and many others, to be unsustainable. If a $13 billion gap is

unsustainable, what term should we apply to a $210 trillion gap?

Kotlikoff also calculates that the fiscal gap is equal to about 58

percent of the combined value of all future revenue. Thus, we would need

to reduce spending or increase taxes by enough to fill that 58 percent

gap if we wanted to put the federal budget on a path to solvency that

balances the interests of those now receiving benefits and those who

hope to receive benefits in the future.

Kotlikoff goes on to illustrate that the fiscal gap is increasing at

an alarming rate and that delay makes our problem much worse. In 2003,

just a little more than a decade ago, the fiscal gap was $60 trillion.

But by last year it had catapulted to $210 trillion. The fiscal gap may

not continue increasing as rapidly as it has over the past decade, but

with each passing year – as Congress and the President do their best to

avoid action – our hole grows deeper by substantial amounts.

Under the CBO estimates used by Congress, we have a huge debt hole.

Under the more comprehensive fiscal gap measurement, we have a chasm.

But little if any Congressional action is planned to deal with the

notorious level of debt. We’re headed toward a fiscal black hole.

(Chris Hedges)

All attempts to reform mass incarceration through the traditional

mechanisms of electoral politics, the courts and state and federal

legislatures are useless. Corporations, which have turned mass

incarceration into a huge revenue stream and which have unchecked

political and economic power, have no intention of diminishing their

profits. And in a system where money has replaced the vote, where

corporate lobbyists write legislation and the laws, where chronic

unemployment and underemployment, along with inadequate public

transportation, sever people in marginal communities from jobs, and

where the courts are a wholly owned subsidiary of the corporate state,

this demands a sustained, nationwide revolt.

“Organizing boycotts, work stoppages inside prisons and the refusal

by prisoners and their families to pay into the accounts of phone

companies and commissary companies is the only weapon we have left,”

said Amos Caley, who runs the Interfaith Prison Coalition,

a group formed by prisoners, the formerly incarcerated, their families

and religious leaders. “Mass incarceration is the most important civil

rights issue of our day. And it is time for communities of faith to

stand with poor people, mostly of color, who are unfairly exploited and

abused. We must halt human rights violations against the poor that grow

more pronounced each year,” Caley said here. He and other prison reform

leaders spoke Saturday at the Elmwood Presbyterian Church.

“We have to shut down the system,” said Gale Muhammad, another speaker and the founder and CEO of Women Who Never Give Up.

“All the companies that use prison labor have to be boycotted. And we

can’t stop there. We have to boycott the vending machines in the prisons

and the phone companies. We have to stop spending our money. Until we

hit them in the pocket they won’t listen.”

Former prisoners and prisoners’ relatives—suffering along with the

incarcerated under the weight of one of the most exploitative,

physically abusive and largest prison systems in the world, frustrated

and enraged by the walls that corporations have set in place to stymie

rational judicial reform—joined human rights advocates at the church to

organize state and nationwide boycotts inside and outside prisons. These

boycotts, they said, will be directed against the private phone, money

transfer and commissary companies, and against the dozens of

corporations that exploit prison labor. The boycotts will target food

and merchandise vendors, construction companies, laundry services,

uniforms companies, prison equipment vendors, cafeteria services,

manufacturers of pepper spray, body armor and the array of medieval

instruments used for the physical control of prisoners, and a host of

other contractors that profit from mass incarceration. The movement will

also call on institutions, especially churches and universities, to

divest from corporations that use prison labor.

The campaign, led by the Interfaith Prison Coalition, will include a

call to pay all prisoners at least the prevailing minimum wage of the

state in which they are held. (New Jersey’s minimum wage is $8.38 an

hour.) Wages inside prisons have remained stagnant and in real terms

have declined over the past three decades. A prisoner in New Jersey

makes, on average, $1.20 for eight hours of work, or about $28 a month.

Those incarcerated in for-profit prisons earn as little as 17 cents an

hour. Over a similar period, phone and commissary corporations have

increased fees and charges often by more than 100 percent.

There are nearly 40 states that allow private corporations to exploit prison labor.

And prison administrators throughout the country are lobbying

corporations that have sweatshops overseas, trying to lure them into the

prisons with guarantees of even cheaper labor and a total absence of

organizing or coordinated protest.

Corporations currently exploiting prison labor include Abbott

Laboratories, AT&T, AutoZone, Bank of America, Bayer, Berkshire

Hathaway, Cargill, Caterpillar, Chevron, the former Chrysler Group,

Costco Wholesale, John Deere, Eddie Bauer, Eli Lilly, ExxonMobil, Fruit

of the Loom, GEICO, GlaxoSmithKline, Glaxo Wellcome, Hoffmann-La Roche,

International Paper, JanSport, Johnson & Johnson, Kmart, Koch

Industries, Mary Kay, McDonald’s, Merck, Microsoft, Motorola, Nintendo,

Pfizer, Procter & Gamble, Quaker Oats, Sarah Lee, Sears, Shell,

Sprint, Starbucks, State Farm Insurance, United Airlines, UPS, Verizon,

Victoria’s Secret, Wal-Mart and Wendy’s.

Prisons in America are a hugely profitable business. And since profit

is the only language the involved corporations know how to speak, we

will have to speak to them in the language they understand. In New

Jersey the first boycott will be directed against Global Tel Link,

a private phone company that charges prisoners and their families

exorbitant rates and that has a monopoly. Organizers at the Saturday

event, including Gale Muhammad, called on prisoners and families to stop

paying into Global Tel Link accounts and boycott the prison phone

service. She urged families and prisoners to write letters to each other

until the company’s phone rates match those paid by the wider society

for such a service.

“Prisoner telephone rates in New Jersey are some of the highest in

the country,” Caley said. “Global Tel Link charges prisoners and their

families $4.95 for a 15-minute phone call, which is about two and a half

times the national average for local inmate calling services.”

Prison phone services are a $1.2-billion-a-year industry. Prisoners

outside New Jersey are charged by Global Tel Link, which makes about

$500 million a year, as much as $17 for a 15-minute phone call. A call

of that duration outside a prison would cost about $2. If a customer deposits $25 into a Global Tel Link phone account, he or she must pay an additional service charge of $6.95.

And Global Tel Link is only one of several large corporations that

exploit prisoners and their families. JPay is a corporation that deals

in privatized money transfers to prisoners. It controls money transfers

for about 70 percent of the prison population. The company charges

families that put money into prisoners’ accounts additional service fees

of as much as 45 percent. JPay generates more than $50 million a year

in revenue. The Keefer Group, which controls prison commissaries in more

than 800 public and private prisons, and which often charges prisoners

double what items cost outside prison walls, makes $41 million a year in

profit. All of these companies have to be targeted.

It will be a long and hard battle. It will require tremendous

sacrifices from those who have loved ones who are incarcerated and from

the 2.3 million locked in cages in the United States’ vast archipelagos

of prisons. It will require those on the outside to boycott corporations

that use prison labor and corporations that gouge prisoners and their

families. It will require us to build networks to support prisoners when

they begin, as they must, to carry out work stoppages to demand the

minimum wage. Building a movement is our only hope.

Michelle Alexander, the author of “The New Jim Crow,” is outspoken

about the imperative for organizing to fight back. In a speech at Union

Theological Seminary in New York City in March she told her audience:

“Jesus taught that he who is without sin should cast the first stone.

Well, we have become a nation of stone throwers. And in this era of mass

incarceration it is not enough to drop your stone. We have to be

willing to catch the stones raining down on the most vulnerable. And we

must be willing to stand up to the stone throwers and disarm them.”

“I believe we now find ourselves at a fork in the road,” she went on.

“We can continue down the road most traveled of business and politics

as usual, the path of reforming our political institutions here and

there, the path Dr. King was determined to leave behind, or we can

choose a different path, the rocky, dangerous path that comes without a

map. It is a path that is beckoning us again, thanks in large part to

the courage of the young people in Ferguson who stood up when Michael

Brown was shot down. It inspired thousands of people to wake up, get up

and march here in New York City and beyond. If we choose this rocky path

there will be no guidebooks, no map, no instructions. All we will have

is our moral compass and the whispering of our angels and our ancestors

in our ears reminding us to dig for deeper truths and to speak and to

act with greater courage, reminding us, in the words of Dr. James Cone, that humanity’s salvation is available only through our solidarity with the crucified people in our midst.”

She called on the audience to “speak difficult and unpopular truths,”

not to avoid “the racial dimensions or the profound moral questions for

purposes of expediency” and not to seek “justice on the cheap.”

“We can and we must build a movement, and not only [about] mass

incarceration and mass deportation, but a broad-based radical, human

rights movement that ends once and for all our history’s cycle of

creating caste-like systems in America, a movement for education, not

incarceration, for jobs, not jails, a movement to end all forms of legal

discrimination against people released from prison, discrimination that

denies them basic human rights to work, to shelter, to food, a movement

for voting rights for all, including those behind bars … a movement

that will end the war on drugs, once and for all, and shift to a public

health model dealing with drug addiction and drug abuse, a movement that

will stand up to the police unions and transform the police itself from

warriors into peace officers directly accountable to the communities

they serve, a movement that will ensure that every dollar saved from

ending the wars that have been declared on poor communities of color,

the wars on crime and drugs, will be invested back into these

communities, the communities most harmed, meaningful reparations and

justice reinvestment, a movement that abandons our purely punitive

approach to dealing with violence and violent crimes and embraces a more

restorative and rehabilitative approach … a movement that is rooted in

the dignity and humanity of us all, no matter who we are, where we come

from or what we may have done.”

At Saturday’s gathering in Newark, among the roughly 100 participants were leading advocates for prison reform such as Bonnie Kerness, the director of the American Friends Service Committee Prison Watch Project; Gale Muhammad; and Larry Hamm,

the chairman of People’s Organization for Progress. There were mothers

and fathers of incarcerated sons and daughters, former prisoners

including Earl Amin,

who was leader of the Black Panthers in Newark and spent 34 years in

prison solely for discussing the possibility of carrying out a bank

robbery, and Ojore Lutalo, who was in the Black Liberation Army and

spent 22 years in solitary confinement in Trenton’s supermax prison.

There was universal and emphatic agreement that if we do not organize to

destroy this country’s system of mass incarceration it will spread like

a cancer, destroying more lives, more families and more communities.

The corporate state seeks to reduce all workers at home and abroad to

the status of prison labor. Workers are to be so heavily controlled

that organizing unions or resistance will become impossible. Benefits,

pensions, overtime are to be abolished. Workers who are not slavishly

submissive to the will of corporate power will be dismissed. There will

be no sick days or paid vacations. No one will be able to challenge

unsafe and physically difficult working conditions. And wages will be

suppressed to keep workers in poverty. This is the goal of corporate

power. The 1 million prisoners employed at substandard wages by

corporations inside prisons are, in the eyes of our corporate masters,

the ideal workers. And those Americans who ignore the plight of prison

labor and refuse to organize against it will increasingly find prison

working conditions replicated outside prison walls.

Prisons, to swell corporate profits, force prisoners to pay for basic

items including shoes. Prisoners in New Jersey pay $45 for a pair of

basic Reebok shoes—almost twice the average monthly wage. If a prisoner

needs an insulated undergarment or an extra blanket to ward off the cold

at night he must buy it. Packages from home, once permitted, have been

banned to force prisoners to buy grossly overpriced items at the

commissary or company-run store. Some states have begun to charge

prisoners rent. This gouging is burying many prisoners and their

families in crippling debt, debt that prisoners carry when they are

released from prison.

The United States has 2.3 million people in prison, 25 percent of the

world’s prison population, although we are only 5 percent of the

world’s population. We have increased our prison population by about 700

percent since 1970. Corporations control about 18 percent of federal

prisoners and 6.7 percent of all state prisoners. And corporate prisons

account for nearly all newly built prisons. Nearly half of all

immigrants detained by the federal government are shipped to

corporate-run prisons. And slavery is legal in prisons under the 13th

Amendment of the U.S. Constitution. It reads: “Neither slavery nor

involuntary servitude, except as punishment for crime whereof the party

shall have been duly convicted, shall exist within the United States.”

Vast sums are at stake. The for-profit prison industry is worth $70

billion. Corrections Corporation of America (CCA), the largest owner of

for-profit prisons and immigration detention facilities in the country,

had revenues of $1.7 billion in 2013 and profits of $300 million. CCA

holds an average of 81,384 inmates in its facilities on any one day.

Aramark Holdings Corp., a Philadelphia-based company that contracts

through Aramark Correctional Services to provide food to 600

correctional institutions across the United States, was acquired in 2007

for $8.3 billion by investors that included Goldman Sachs. And, as in

the wider society, while members of a tiny, oligarchic corporate elite

each are paid tens or even hundreds of millions of dollars annually, the

workers who generate these profits live in misery.

“It is an abomination that prisoners are paid 22 cents an hour, $1.20

cents a day,” Larry Hamm told the Newark meeting. “Every prisoner

should get the minimum wage of New Jersey, $8.38 per hour.”

He went on. “Even when you come out [of prison] it moves from slavery

to sharecropping because they have these fines and obligations that

they put on people. … That is how sharecropping was. That is why a lot

of our great-grandparents and grandparents couldn’t leave the South.

Everything was owned by the former slave master. If they bought a plow

they ended up in debt over the plow. If they bought seeds they ended up

in debt over the seeds. They were tied to the land. Probation is like

sharecropping. You are off the plantation, but you still belong to us.

And look at this rapacious, exploitative system where phone companies

make 50 times what a phone call should cost. And people are charging

high commissary fees.

“This is capitalist exploitation, and it must stop,” Hamm thundered.

“But it won’t stop unless we build a movement to make it stop. Every

organization that calls itself a civil rights or human rights

organization, if they do not have the plight and condition of the

incarcerated on their agenda they need to hand in their credentials.”

Last week’s call to launch nationwide boycotts signals the start of

the most important frontal assault yet against the prison-industrial

complex. I do not know if it will succeed. But I do know it is our only

hope. Halting the abuse and exploitation of the poor inside prisons is

not only the most important civil rights issue of our time, it promises

to be a vital check against a corporate state that, if not dismantled,

will imprison us all.

by John Rubino

One of the oddities of floating exchange rates is that they cause

people to view the world in terms of their own national currency. For

Americans that means looking out through a window that is distorted by

the dollar’s recent surge. A C$100-a-night Vancouver BC hotel room, for

instance, cost about US$100 in 2013 and now costs about $80. Most other

Canadian products are commensurately cheaper, making a week north of the

border suddenly a lot easier to fit into the family budget. Though fundamentally not much has changed.

Another big distortion is in local-currency gold

prices. Here in the US, gold has been in a brutal bear market since

2013. But for people in most other countries,living as they are with

relatively weak currencies, gold’s bull market has resumed without

missing a beat. In the past week, gold rose by 3.5% and 2.2% in euros

and pounds, respectively. And that’s par for the recent course. Here’s a

chart from Kitco

showing the past six months’ gold price action. Note that it’s down a

bit in US dollars but up by varying amounts against the other major

currencies. These are six-month numbers, so annualizing them produces

very nice gains, especially in euros where it’s about 35%.

image: http://dollarcollapse.com/wp-content/uploads/2015/04/Gold-in-other-currencies-April-2015.jpg

Two conclusions can be drawn from this:

1) People everywhere are getting seriously distorted pictures of

their world. Europeans and Japanese especially are seeing zero consumer

price inflation but rapid currency depreciation against assets such as

equities, penthouses and, lately, gold. So is that inflation or

deflation? This question is just as confusing for economists as it is

for regular people.

2) The US, now feeling the impact of a too-strong

dollar on corporate revenues and (potentially) earnings and therefore

share prices, can’t keep this up much longer and will have to not just

delay the promised rate increases but change course entirely and join

the global devaluation party. Deflation is not an option when your debts

exceed 300% of GDP.

But in the meantime, the world’s non-US gold miners (which comprise

the vast majority of the sector) are seeing the world through a

less-confusing, more rose-colored lens. The price of the gold they’re

mining is up nicely, usually at a double-digit annual rate, while their

labor costs are stable due to flat local wage growth and their fuel

costs are down big thanks to the (partially strong-dollar-induced)

plunge in oil prices.

So almost alone among major industries, the miners are entering a

margin sweet spot, with higher selling prices and flat-to-falling costs.

They won’t blow the doors off of analyst expectations this quarter,

especially with all the write-downs that are baked into the cake, though

they might surprise to the upside a bit more than in the recent past.

But let the current environment persist for a while and the gap between

cost and sales trends might reach a point where it gets noticed. That

combination — beaten-down stocks and widening margins — is what puts a

period at the end of bear markets.

Greece has six days to present their proposals for the next payment.

Italy wants to leave the Euro zone. Malls are closing down. Real estate

recovery is a hoax. The White House warns states to be prepared for the

next collapse. Protesters use holograms to protest the gag law. German

businesses angry because they are losing billions because of the Russian

sanctions. NATO getting ready the Russian Rapid Force by having drills.

US not evacuating US citizens in Yemen. FBI sets up another fake IS

sting.

Our modern society is highly dependent upon the “system.” Not only do we

rely upon utility services to bring us electricity, water and natural

gas, but also on an incredibly complex supply chain which provides us

with everything from food to computers. Without that supply chain, most

of us wouldn’t know what to do.

This situation is actually becoming worse, rather than better. When I

compare my generation (I’m in my 50s) to that of my children, I see some

striking differences. In my generation it was normal for a boy to grow

up learning how to do a wide variety of trade skills from his father,

and seemingly everyone knew how to do basic carpentry and mechanic work.

But that’s no longer normal. - See more at:

http://www.naturalblaze.com/2015/04/8-forgotten-survival-skills-your-great.html#sthash.3n6wjNBr.dpuf

From Filip Karinja, for Birch Gold Group

Just this week, former Treasury Secretary Larry Summers wrote an eye-opening and scathing op-ed outlining where America stands in the rapidly changing global economy.

Titled ‘Time U.S. leadership woke up to new economic era’,

the piece looks at the many ways in which the United States is losing

influence around the world to China and other emerging markets, while at

the same time becoming increasingly isolated.

Summers especially points to the charade that is our two-party

political system as a main culprit for our dysfunction, saying that both

the left and right are responsible for not only the decline of the

country, but also allowing other nations, like China, to fill the void

we’ve created. Former Treasury Secretary Larry Summers

China’s rise in power has been well documented, and appears to be only growing stronger as more and more nations turn their back on the U.S. dollar.

What’s the latest move away from the U.S. as global economic superpower? Despite serious disapproval from Washington,

many of America’s allies are joining China’s proposed new financial

institution, the Asian Infrastructure Investment Bank (AIIB). This

include our closest of allies, including England and Israel.

What’s more, many countries that the U.S. has an open disdain for, such as Russia and Iran, are founding members of the AIIB.

They say a picture tells a thousand words. Here’s that map again from

the top of this article, of who’s in and who’s out of the AIIB:

Take a good look at this map. Think the U.S. is becoming isolated and irrelevant?

Besides the U.S., the only other notable non-applicant country is Japan, who is facing a debt crisis of their own. But even the Japanese are ultimately expected to join – and that’s despite its ongoing and bitter dispute with China over the Senkaku Islands.

Summers argues that institutions such as the AIIB are rising because

the U.S. has increasingly and stubbornly refused to cede power within

the International Monetary Fund (IMF) to other nations. Another

attraction for many nations is that, unlike at the World Bank and IMF,

powerful nations like the UK, China and U.S. are not given veto powers.

This ensures a level playing field.

A level playing field on the global stage is not something the U.S.

is accustomed to. Without veto powers, the U.S. is like Dorothy from the

Wizard of Oz without her ruby slippers; although in the case of the

AIIB, Dorothy is not even in Neverland, let alone wearing her slippers!

Just to show you how fed up the rest of the world has become with the

U.S., take a look at the 10 million Venezuelans that have signed a

petition this month protesting U.S. aggression. That’s one-third of the entire country putting pen to paper!

It seems former Congressman and Presidential candidate Ron Paul was right all along in saying that American prosperity would be damaged by welfare, warfare, corporatism and fiat money.

Now that the decline of America is in full view, this message is

starting to find its way into the mainstream, with people like Larry

Summers stating what many of us have been saying for a long time.

It might be too late for America to remain the world’s super power. But it’s not too late to save face.

If the U.S. does indeed decide to join the AIIB, it will be part of a

network of emerging economies that will trade in a more democratic

style than the current structure. But should the U.S. continue to

stubbornly sit on the sidelines, it will face being ostracised by

rapidly growing foreign economies at a time when it needs all the help

it can get. Read more…

by Jesse’s Café Américain

image: https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEhzNzmDOueQUlS_DA-9lTgtn3nGKgZnla1gcHT77NAu1PkmBhMkxPqcNDYfMaL6-3s_M92ueOZQFx1JEltyBnBR5Kt9z8q7dDUlEn8_oJNxDa-uv9K2oF42z3kmF9LNYR8HC3CNc9kJLbE/s1600/414mnuJe8dL__UY250_.jpg

I have just started reading a new book by Janet Tavakoli called Decisions: Life and Death on Wall Street.

There is also a paperback version of it available in the US and Canada here.

This is a non-fiction story of her travels in the world of finance

that asks the question, ‘What would you be willing to do for money and

power?’

As usual Janet does not pull her punches. The description on Amazon is rather intriguing.

In New York, the Federal Reserve Bank hides damaging

information about too-big-too-fail banks from the public eye. A

prominent bank CEO seems on the verge of a nervous breakdown.

In Washington D.C., a former Wall Street regulator checks into a

hotel using the name of a hedge fund manager for an illicit meeting with

a prostitute. In a D.C. suburb, the CFO of a beleaguered mortgage giant

chooses a drastic personal end to “relentless pressure”.

In a picturesque suburb of Zug, Switzerland, the

CFO of a major insurance company decides to end his life. In London, a

financier kills himself in a way he once said he never would.

In her new memoir, Janet Tavakoli shines a bright light on the

money-driven culture of Wall Street and Washington, and the life and

death consequences of our decisions that put profit above all.

“The U.S. went off the gold standard in August 1971. With no benchmark,

central banks could print money and debase currencies. That opened the

door for huge bailouts after big banks screwed up in a big way.

Taxpayers—not incompetent bankers—paid the price.

By [the late 1980’s], the Federal Reserve Bank and large U.S. banks

had established a pattern to control the public relations damage each

time banks had a major screw-up: accountants and regulators let banks

lie about the size of the problem to stall for time; the Federal Reserve

blew smoke at the media; finally, the Fed would bail out the banks in a

way that most taxpayers would not understand.

Banks didn’t have to get smarter or more competent. The Fed trained

the banks that uninformed taxpayers would eat the losses, and fake

accounting would let bank officers keep their positions and their

money.”

If ‘rule under law’ were more than just a slogan in the United

States, men who occupied the senior-most positions in too-big-to-fail

banks would have been disgraced, prosecuted, and jailed. But no bank

executive was held accountable.”

Oppressive Taxes And Regulations Killing Upstate New York Economy

Oppressive government regulations and taxes beating down Upstate New

Yorkers have assaulted the region for years, leaving cities like

Binghamton on the path to Detroit-level devastation. However, all is not

lost. The hope of prosperity is evidenced in the success of less

regulated and prosperous Native American tribe businesses image: http://images.intellitxt.com/ast/adTypes/icon1.png in the state.

The Upstate cities of Rochester, Buffalo, Syracuse,

and Binghamton have experienced poverty levels upwards of 30 percent in

2013, all having increased from 2010 levels, according to U.S. Census

data. Detroit sits at a 39.3 percent poverty rate with Syracuse,

Binghamton, and Rochester right behind at levels of 34.6 percent, 33.3

percent, and 32.9 percent respectively.

Detroit edges out the others in home ownership, with 52 percent

homeowner-occupied housing between 2009 and 2013, whereas the New York

cities mentioned host rates as low as 39 percent. Each city had a

similar population density to Detroit.

Jobs, income, and residents in the former agriculture and

manufacturing-leading Upstate New York regions have been experiencing

the pain of government overreach for over 50 years, argues a Deseret

News article.

“Basically what you’ve got in New York is a state tax code and regulatory regimen written for New York City,” Joseph Henchman, vice president image: http://images.intellitxt.com/ast/adTypes/icon1.png

for state projects at the Tax Foundation in Washington, told the paper.

“Legislators say, `Look, New York is a center of world commerce.

Businesses have to be here. It doesn’t matter how high we tax them.’ I

hear that a lot. But when you apply that same logic to upstate, the

impact is devastating.”

Similar to the exodus seen from California, businesses have forsaken

the Upstate region for more friendly venues. “In 1988, Kodak employed

62,000 people in Rochester, ” Rochester Business Alliance president image: http://images.intellitxt.com/ast/adTypes/icon1.png

Sandra Parker told Deseret News. “Today it employs 4,000. Xerox has

moved most of its people out while Bausch & Lomb, which was founded

in Rochester in 1858, has left entirely.”

http://www.breitbart.com/big-government/2015/04/11/oppressive-taxes-and-regulations-killing-upstate-new-york-economy/ How high taxes and regulation are killing one of the most prosperous states in the nation

Upstate New York is becoming Detroit with grass.

Binghamton, New York — once a powerhouse of industry — is now

approaching Detroit in many economic measures, according to the U.S.

Census. In Binghamton, more than 31 percent of city residents are at or

below the federal poverty level compared to 38 percent in Detroit.

Average household income in Binghamton at $30,179 in 2012 barely

outpaces Detroit’s $26,955. By some metrics, Binghamton is behind

Detroit. Some 45 percent of Binghamton residents own their dwellings

while more than 52 percent of Detroit residents are homeowners. Both

“Rust Belt” cities have lost more than 2 percent of their populations.

Binghamton is not alone. Upstate New York — that

vast 50,000-square mile region north of New York City — seems to be in

an economic death spiral.

The fate of the area is a small scene in a larger story playing out

across rural America. As the balance of population shifts from farms to

cities, urban elites are increasingly favoring laws and regulations that

benefit urban voters over those who live in small towns or out in the

country. The implications are more than just economic: it’s a trend that

fuels the intense populism and angry politics that has shattered the

post-World War II consensus and divided the nation.

Upstate New York, the portion that lies beyond the New York

metropolitan area, has become “The Land That Time Forgot,” a broad swath

of depressed cities and low-profit farmlands that stretches from

Newburgh and Poughkeepsie in the Hudson Valley through the old

manufacturing centers of Schenectady and Troy, across the Allegheny

Plateau to Syracuse, Rochester and Buffalo, all the way west to

Jamestown, the city with the lowest percentage of college graduates in

America. http://www.deseretnews.com/article/865626141/How-high-taxes-and-regulation-are-killing-one-of-the-most-prosperous-states-in-the-nation.html?pg=all

Upstate New York is becoming Detroit with grass.

Binghamton, New York — once a powerhouse of industry — is now

approaching Detroit in many economic measures, according to the U.S.

Census. In Binghamton, more than 31 percent of city residents are at or

below the federal poverty level compared to 38 percent in Detroit.

Average household income in Binghamton at $30,179 in 2012 barely

outpaces Detroit’s $26,955. By some metrics, Binghamton is behind

Detroit. Some 45 percent of Binghamton residents own their dwellings

while more than 52 percent of Detroit residents are homeowners. Both

“Rust Belt” cities have lost more than 2 percent of their populations.

Binghamton is not alone. Upstate New York — that vast 50,000-square mile

region north of New York City — seems to be in an economic death

spiral.

The fate of the area is a small scene in a larger story playing out

across rural America. As the balance of population shifts from farms to

cities, urban elites are increasingly favoring laws and regulations that

benefit urban voters over those who live in small towns or out in the

country. The implications are more than just economic: it's a trend that

fuels the intense populism and angry politics that has shattered the

post-World War II consensus and divided the nation.

Upstate New York, the portion that lies beyond the New York metropolitan

area, has become “The Land That Time Forgot,” a broad swath of

depressed cities and low-profit farmlands that stretches from Newburgh

and Poughkeepsie in the Hudson Valley through the old manufacturing

centers of Schenectady and Troy, across the Allegheny Plateau to

Syracuse, Rochester and Buffalo, all the way west to Jamestown, the city

with the lowest percentage of college graduates in America.

For more than half a century, this huge region — once the nation’s

breadbasket and a manufacturing capital — has been losing jobs, dollars

and people. “It all began in 1959 when the interstate highway system was

completed,” says Carl Schramm, professor of innovation and

entrepreneurship at Syracuse University. “That was also the year

commercial jets went into service and half the homes in Florida were

air-conditioned.”

Weather was certainly a contributing factor. Of the country’s 12 medium-

and large-sized cities with the heaviest annual snowfall, nine are in

upstate New York, with Syracuse on top of the list at 115 inches. Not

for nothing is the 363-mile long corridor of the old Erie Canal called

the “Snow Belt.”

But other states — New Hampshire, Minnesota, North and South Dakota,

Colorado — have similar weather and have not seen mass evacuation. The

difference is that upstate New York is tethered to New York City, whose

residents overwhelmingly support higher taxes, stricter regulation and

bigger spending than the national averages. Those policies are blamed

for upstate’s economic woes by many in the region.

“Basically what you’ve got in New York is a state tax code and

regulatory regimen written for New York City,” says Joseph Henchman,

vice president for state projects at the Tax Foundation in Washington.

“Legislators say, `Look, New York is a center of world commerce.

Businesses have to be here. It doesn’t matter how high we tax them.’ I

hear that a lot. But when you apply that same logic to upstate, the

impact is devastating.”

The exodus

The lives of Bill and Janet Sauter, brother and sister, sum up the sad

story of upstate New York. They grew up in the Long Island suburbs. He

went to Clarkson College in Potsdam, N.Y., near the Canadian border,

studied software and enjoyed a highly successful career in Texas’ oil

industry.

Janet went upstate too, marrying a minister and settling in rural East

Chatham, 30 miles south of Albany. In 1999, she and her husband wanted

to move to Texas to be closer to their daughter. But they couldn’t sell

their home. Months passed without a single inquiry. For Janet, there was

no escape from New York. Her neighbors had similar experiences, she

said.

Bill is now retired and living in Steamboat Springs, Colo., where he

skis at every opportunity — while Janet and her husband Bob are trying

to eke out a living in what has become one of the poorest regions in the

country. “There just isn’t much work around here,” says Janet, who

supplements her husband’s income by working all night in a home for the

elderly. “I’m lucky to have this job.”

Industry has fled upstate New York. “In 1988, Kodak employed 62,000

people in Rochester,” says Sandra Parker, president of the Rochester

Business Alliance. “Today it employs 4,000. Xerox has moved most of its

people out while Bausch & Lomb, which was founded in Rochester in

1858, has left entirely.”

As a result, Rochester is now the fifth poorest city in the country,

with 31 percent of the population living in poverty. Buffalo is right

behind at No. 6 (30 percent).

Syracuse was devastated when Carrier, the nation’s largest manufacturer

of air conditioners, General Electric and auto-parts manufacturer Magna

International shuttered their last manufacturing plants in Onandago

County. A Wall Street Journal survey of the nation’s 2,737 counties,

shows that only nine other counties have suffered greater job losses per

capita than Onandago County since 2009.

Bob and Janet Sauter were not alone in their desire to leave New York

for more prosperous parts of the country. New York state has lost

350,000 people in the past three years, according to the Empire Center

for New York State Policy, an Albany-based research group. This is the

largest out-migration of any state.

New York was the most populous state in the union in 1960, with 45

representatives in Congress. By 2012, New York fell to third place and

its congressional delegation plummeted to 28. The 2020 Census will

likely cost New York even more congressional seats. Without the hundreds

of thousands of immigrants moving into New York City, the state’s

depopulation would be even greater. A remarkable 36 percent of New York

City is foreign born — twice the percentage in 1970.

Read more at http://national.deseretnews.com/article/4039/How-high-taxes-and-regulati...

(Lorcan Roche Kelly)

The world’s central banks have a problem. When economic conditions

worsen, they react by reducing interest rates in order to stimulate the

economy. But, as has happened across the world in recent years, there

comes a point where those central banks run out of room to cut — they

can bring interest rates to zero, but reducing them further below that

is fraught with problems, the biggest of which is cash in the economy.

In a new piece, Citi’s Willem Buiter looks at this problem, which is

known as the effective lower bound (ELB) on nominal interest rates.

Fundamentally, the ELB problem comes down to cash. According to

Buiter, the ELB only exists at all due to the existence of cash, which

is a bearer instrument that pays zero nominal rates. Why have your money

on deposit at a negative rate that reduces your wealth when you can

have it in cash and suffer no reduction?

Cash therefore gives people an easy and effective way of avoiding negative nominal rates.

Buiter’s note suggests three ways to address this problem:

Abolish currency.

Tax currency.

Remove the fixed exchange rate between currency and central bank reserves/deposits.

Yes, Buiter’s solution to cash’s ability to allow people to avoid

negative deposit rates is to abolish cash altogether. (Note that he’s

far from being the first to float this idea. Ken Rogoff has given his endorsement to the idea as well, as have others.)

Before looking at the practicalities of abolishing currency, we

should first look at whether it could ever be necessary. Due to the

costs of holding large amounts of cash, Buiter puts the actual nominal

rate at which the move to cash makes sense as closer to -100bp. So, in

order for a cash abolition to become necessary, central banks would need

to be in a position where they wished to set nominal rates much lower

than that.

Buiter does not have to go far to find an example of where a central

bank may have wanted to set interest rates much lower to -100bp. He uses

(a fairly aggressive) Taylor Rule to show that Federal Reserve rates

should have been as low as -6 percent during the financial crisis.

It seems Buiter is correct: Sometimes strongly negative nominal rates are called for.

Buiter is aware that his idea may be somewhat controversial, so he

goes to the effort of listing the disadvantages of abolishing cash.

Abolishing currency will constitute a noticeable change in many people’s lives and change often tends to be resisted.

Currency use remains high among the poor and some older people. (Buiter suggests that keeping low-denomination cash in circulation — nothing larger than $5 — might solve this.)

Central banks and governments would lose seigniorage revenue.

Abolishing currency would inevitably be

associated with a loss of privacy and create risks of excessive

intrusion by the government.

Switching exclusively to electronic payments may create new security and operational risks.

Buiter dismisses each of these concerns in turn, finishing with:

In summary, we therefore conclude that the arguments against abolishing currency seem rather weak.

Whatever the strength of the arguments, the chances of an

administration taking the decision to abolish cash seem vanishingly

small.

Why your doctors won't tell you about this Diabetes Breakthrough...

by John Rubino

Back in the early 2000s, General Electric — previously known as the

world’s biggest, best managed maker of cool, useful things like jet

engines and wind turbines — discovered that it could make even more

money by exploiting its AAA credit rating to borrow cheap currency and

lend it out at higher rates. It ramped up its vendor financing, enabling

customers to buy more of its stuff, and built a real estate empire that

spanned the globe.

It took a while for people to figure out the the company

image: http://images.intellitxt.com/ast/adTypes/icon1.png ,

via its GE Capital division, had in effect become one of the world’s

biggest, most highly-leveraged banks. But eventually they got it, and

when the real estate/derivatives bubble burst in 2008, being a major

bank was like being a dot-com in 2000 or a silver miner today: a very

bad thing in the eyes of shell-shocked investors. GE’s market value

reflected its new corporate persona:

image: http://dollarcollapse.com/wp-content/uploads/2015/04/GE-share-price.jpg

Now it appears that GE’s managers image: http://images.intellitxt.com/ast/adTypes/icon1.png

(unlike most of the people running today’s governments and big banks)

actually remember all the way back to the previous decade, and have

decided that they don’t want to live through a replay. This morning the

company announced that it is selling a big part of GE Capital’s real

estate assets and using the proceeds to buy back stock. Some details

from MarketWatch:

General Electric CEO image: http://images.intellitxt.com/ast/adTypes/icon1.png

Jeff Immelt has a good reason to be smiling, because he is delivering

on his promise of focusing the company on its core industrial

businesses.General Electric Co. just became a much safer stock for

long-term investors, as CEO Jeff Immelt has finally delivered on his

promise of turning the company back into an industrial powerhouse.

General Electric said on Friday that it would sell

most of the assets of GE Capital Real Estate for roughly $26.5 billion

to investment funds managed by Blackstone Group % with a portion of the

loans going to Wells Fargo & Co.

The asset sale will result in $16 billion in first-quarter after-tax charges, of which $12 billion will be noncash charges.

This move follows the initial public offering of Synchrony Financial,

GE Capital’s consumer finance unit, in August. GE holds 85% of

Synchrony’s stock, but plans to complete its full exit from the business image: http://images.intellitxt.com/ast/adTypes/icon1.png through a tax-free spinoff by the end of 2015.

GE Capital’s remaining activity will be limited to providing financing for the parent company’s industrial customers.

GE’s news release announcing its latest and greatest reduction of GE

Capital summed up the move beautifully, saying “the business model for

large wholesale-funded financial companies image: http://images.intellitxt.com/ast/adTypes/icon1.png has changed, making it increasingly difficult to generate acceptable returns going forward.”

“Wholesale-funded” refers to GE Capital’s traditional reliance on the

commercial paper market for liquidity. The problem with this short-term

funding model for a balance sheet with long-term assets is that during a

financial crisis, overnight liquidity tends to dry up as it did for GE

late in 2008. When the company had difficulty finding buyers for its

paper, the Federal Deposit Insurance Corp. stepped in and through its

Temporary Liquidity Guarantee Program (TLGP) was covering $21.8 billion

of GE commercial paper. GE Capital registered for up to $126 billion in

commercial-paper guarantees under the TLGP.

General Electric obviously wishes to avoid ever needing another

government bailout. When GE Capital’s ending net investment declines to

roughly $90 billion at the end of 2015, the company estimates needing

just $40 billion in funding, which is a relatively small amount. GE

Capital will also “work with regulators” to end the unit’s designation

by the Financial Stability Oversight Council as a “systemically

important financial institution.” This means it will no longer be

subject to the Federal Reserve’s annual stress tests or the regulator’s

heightened level of scrutiny for major lenders.

Some thoughts

Wise move, now that virtually every measure of financial leverage is

once again flashing red. Rich-world government debt has doubled in the

past five years, student loans and subprime auto loans have replaced

subprime mortgages at the junk paper buffet, and big-bank derivatives

books are, amazingly, even bigger than when they nearly destroyed the

global financial system. The next few years, in short, are going to be

another terrible time to be a big bank, and GE’s exit from that part of

its business will look a lot like Sam Zell’s exit from his real estate empire in 2007: really well-timed.

This won’t make GE immune to a global slowdown, of course, and that’s probably coming, given the oil debt and hedges

on which banks now have to make good, the soon to be soaring default

rates on subprime auto loans in the US and dollar carry trade plays in

the developing world. So the share buybacks will probably be seen, in

retrospect, as one of those peak-of-the-cycle cautionary tales for

future CEOs image: http://images.intellitxt.com/ast/adTypes/icon1.png .

But GE will at least be spared the indignity of another government bailout and share-price near-death experience.

Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

GE’s announcement that it would shed the bulk of the assets held by

GE Capital is a doozie of a deal. GE Finance, the seventh largest

financial institution in the US, generated $43 billion in revenues in

2014, compared to $108 billion of GE’s industrial operations. GE Capital

is so big that it has been designated a “systemically important

financial institution.” Regulators are crawling all over these SIFIs.

And it seems GE wants to get them out of its hair.

GE has been trimming down its financial

operations since the Financial Crisis. Back in 2007, GE Capital,

sporting an ending net investment (ENI) of $580 billion, generated 57%

of GE’s revenues. By now it’s down to 25%. After the deal is implemented

and $200 billion in financial assets have been sold, ENI drops to $90

billion. By then, GE Capital’s revenues are expected to be a mere 10% of

total revenues.

GE is immensely smart.

It got bailed out by the Fed during the Financial Crisis when it was

running out of liquidity – having borrowed short-term for long-term

investments, among other sins. TARP was peanuts compared to the money

the Fed handed out. The New York Fed handled these bailouts. And who was

a director of the New York Fed at the time? GE’s CEO Jeff Inmelt.

So now he wants to “create a simpler, more valuable industrial company image: http://images.intellitxt.com/ast/adTypes/icon1.png by selling most GE Capital assets,” GE claimed on Friday.

But there’s a price: On “day one,” income will get hit by $16 billion

in charges, including a $2.4 billion loss on the sale of its commercial

property assets, $6 billion in taxes payable on “repatriating” $36

billion in cash, and $5 billion in impairments. GE also expects an

additional $7 billion in costs, for a “total exit impact” of $23

billion, wiping out most of its $28 billion in 2013 and 2014 net income.

Becoming more “valuable” is expensive.

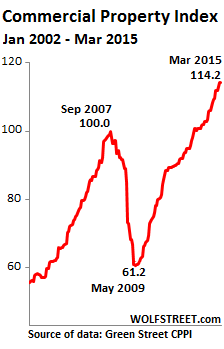

Did GE sell at the Peak of the Commercial Property Bubble?

image: http://wolfstreet.com/wp-content/uploads/2015/04/US-Commercial-Property-IndexGreen-Street.png

GE confessed to be a market timer: It’s a “strong seller’s market for financial assets,” it said.

So it’s dumping its commercial property assets of $26.5 billion.

Funds managed by Blackstone agreed to buy the bulk of the assets of GE

Capital Real Estate. Wells Fargo will pick up a portion of the

performing loans. Other buyers have agreed to buy another $4 billion in

commercial property assets.

It’s an “excellent environment for creating value from financial assets,” GE said.

Commercial property prices have soared 87% from May 2009, according to the Green Street Commercial Property Index

(CPPI), and are now 14% higher than they were in September 2007, at the

peak of the prior crazy commercial property bubble that collapsed so

spectacularly. GE is selling during what might turn out to be the final

phase of an even crazier commercial property bubble. Impeccable timing.

There are some quirks, however.

GE is selling the assets of GE Capital, but it’s not shedding the

liabilities: as part of the deal, it will fully and unconditionally

guarantee $210 billion in GE Capital debt. So it’s still on the hook for

the $210 billion. But most of the assets are gone, and so are the $43

billion in revenues.

To cover up the loss of income from GE Capital on an

earnings-per-share basis, it would buy back $50 billion of its own

shares by 2018, GE said. This will be the second largest share buyback

program ever, after Apple’s $90 billion program announced in early 2014.

This comes after GE’s $35 billion buyback announced in December 2012.

GE doesn’t have this kind of cash flow, not anywhere near. So it will

have to borrow much or all of this money. Hence more debt with fewer

assets to support it. To top it off, GE will continue to pay out rich

dividends.

Ironically, when GE announced the Alstom acquisition last year, it

claimed that it would exercise some restraint in these sorts of things.

But that was last year.

Selling $200 billion in financial assets, remaining on the hook for

$210 billion in associated debt, incurring $23 billion in costs to do

so, and buying back $50 billion in shares mostly with borrowed

money amounts to a masterpiece of financial engineering designed to

trick up its earnings per share. Not many companies image: http://images.intellitxt.com/ast/adTypes/icon1.png can pull this off.

But Moody’s had a cow.

And it slashed

GE’s credit rating. It saw “a growing level of financial risk

tolerance, in favor of equity holders and at the expense of creditors.”

And it’s the creditors that Moody’s serves. Here are some peppery

highlights:

The pending GE Capital asset sales, with virtually all

benefits inuring to equity owners, taken together with high share

repurchase activity and a high dividend payout in recent periods, and

the liquidity-consuming Alstom acquisition that is still pending,

reflect a noteworthy shift by GE to more aggressive financial policies.

GE has been increasing cash payments to shareholders for several

years but has not yet achieved a commensurate increase in operating

earnings and cash flow.

In fact, the reduction of earnings and dividends

from GE Capital during a period of heavy investment by GE and under

difficult market conditions for many of GE’s industrial business

image: http://images.intellitxt.com/ast/adTypes/icon1.png

lines will further undercut financial ratios that we already expected

to be weaker than peers at the same rating level over the next several

years….

Moreover, the full and unconditional guarantee from GE of all

existing GE Capital debt imposes additional overhang relative to the

current income maintenance agreement and further exacerbates the

declining leverage profile that is already heavily strained by

substantially underfunded pension liabilities.

The current cash consumptive stage of GE’s business cycle and ongoing

heavy capital spend as anticipated will continue to constrain the

company’s free cash flow generating capability and earnings over the

next few years.

In other words, creditors end up with the short end of the stick.

So to heck with the creditors.

And with risks and leverage. So be it that the guarantees, if called

upon, would break the company. It can always get bailed out again by the

Fed. There are in fact no more risks in the financial world. The Fed

has removed them from the calculus.

It was a masterful stroke of “aggressive,” as Moody’s said, financial

engineering! It will be talked about for years to come. It will be the

model to follow. GE shares had been in decline since December 31, 2013,

despite all prior efforts at financial engineering, including $35

billion in share buybacks. And so the mere announcement on Friday caused

Wall Street to foam at the mouth, and the languishing shares jumped

nearly 11% in a single day! That’s how you do it!

But the Fed, which has encouraged this sort of thing, is now clueless

how to unscramble its omelet. It fears “outsized market reaction” to

even the smallest moves. Other central banks keep adding to the omelet.

Absurdity reigns. Read… Keep Pushing Until Something Really BIG Breaks?

by SRSrocco

The Western U.S. Dollar based monetary system is headed for a train

wreck. This isn’t a matter of IF, it’s a matter of WHEN. Investors

lulled to sleep by the low paper price of gold are losing out on the

best buying opportunity of a lifetime. The precious metals will be one

of the best insurance policies to own when the U.S. Dollar finally

catches on fire and burns down the entire system.

There are several gold theories circulating around

the alternative media on how the global financial situation will play

out going forward. While it’s impossible to really know how events will

turn out in the future, there are some that I can guarantee, WILL NOT

TAKE PLACE.

I will not get in to the particulars in this article, but rather

provide two charts and a bit of common sense that will destroy some of

what I label as FAULTY GOLD CONSPIRACIES.

There’s this notion put forth by some very intelligent people that

the world has a great deal more gold than stated by official sources

stashed away, hidden in vaults around the world. All we have to do is

take this gold and back the U.S. Dollar…. and then everything will be

OKAY. I have read estimates from 500,000 to 1,000,000 metric tons

(mt) of gold stored in different vaults throughout the world. I find

this claim simply astonishing as a bit of 3rd grade math would totally

destroy this lousy conspiracy theory. Let’s take a look at the next two charts: image: http://srsroccoreport.com/wp-content/uploads/World-Gold-Production-1493-2014.png

According to the figures put out by the U.S. Bureau

of Mines in their 1930 Summarized Gold Production data, the world

produced 714 mt of gold from 1493-1600, 897 mt from 1600-1700, more than

doubled to 1,904 mt during the next century, and went completely

exponential from 1900-2014 at a staggering 151,482 mt. Thus, 98% of all the gold mined since 1493 came after 1900.

Some readers may think this information was manipulated by the

so-called POWERS THAT BE. However, if governments were manipulating

gold production data prior to 1930, I would imagine they were INFLATING

the figures, rather than underestimating them. Why? If you read over

some of these older U.S. Bureau of Mines reports, you will see just how

detailed and meticulous they were. We must remember, gold was still the King Monetary Metal

prior to 1930, and countries with high production saw it as bragging

rights to share this data. So, I believe the estimates of

world gold production put forth by that report is very trustworthy… even

though the figures may not be 100% accurate.

In addition, there just weren’t many places in the world that had a

great deal of easy to find and extract gold before 1900. It wasn’t

until Americans expanded to the west of the country did we find a lot of

gold and silver. One such place and event was the Great California

Gold Rush.

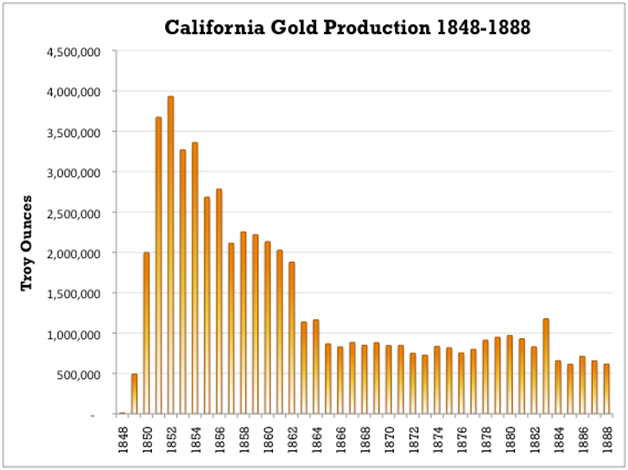

This following chart came from the article The Bakken Boom: Modern Day Gold Rush, which compared peak production during the California Gold Rush to what would take place in North Dakota Bakken oil production: image: http://srsroccoreport.com/wp-content/uploads/California_Gold_Production.png

Gold production in California started in 1848 and

peaked just four years later at 3.9 million ounces (Moz). Production

continued to decline, even with using high-tech techniques of hydraulic

mining by using massive amounts of water to wash away mountain sides to

get the gold.

The California Gold Rush from 1848 to 1888 yielded approximately 57 Moz of gold. How much is this in metric tons? It turns out to be 1,773 mt. This

was one of the biggest gold discoveries in the world at the time, but

it only accounted for 1.1% of the total 155,000 mt of gold mined in the

world since 1493.

Folks, there just weren’t that many big gold discoveries in the world

prior to the 1900’s. Of course the huge gold discovery in the late

1800’s in South Africa was another, but again… these were few and far in

between.

It wasn’t until oil was discovered in the late 1800’s were we able to

seriously ramp up gold production. Here is the breakdown since 1900: 1900-1960 = 47,242 mt 1960-2014 = 104,240 mt

In the first six decades, the world produced 47,242 mt of gold, but

it more than doubled in the next 54 years to 104,240 mt. I discussed

this in a recent interview titled, “Mad Rush Out of Paper Assets Coming “The Data to Prove It!” You can find this topic in PART 2 towards the last third of the interview.

The official sources such as GFMS state there were a total of 170,000

mt of gold mined in the world, and this to me is pretty accurate

assuming about 15-20,000 mt were mined before 1493. I say this is

pretty accurate because if we make a plot on a chart over the past 2,000

years and input world population, gold, silver, lead, copper and oil

production, they will all look flat up until the 1700’s. Yes, of course

oil production did not come in the picture until the late 1800’s… but

you will catch my drift here in a minute.

By the 1800’s world population, gold and

silver production started to move up higher and it wasn’t until the

1900’s did ALL OF THEM GO EXPONENTIAL. Why? You can thank the

exponential rise in oil production that impacted the same rate of

increase in world population, gold, silver, lead and copper production.

So, don’t count on some group to magically save the system by taking

the supposed 100,000’s mt of gold hidden in vaults around the world to

back the soon to be worthless Dollar. There’s a hell of a lot less gold

in the world than we realize.

And….. when the Dollar finally does die, I would imagine there will even be a great deal less to buy.

Two conclusions can be drawn from this:

Two conclusions can be drawn from this:

in the state.

in the state.

Now it appears that GE’s managers

Now it appears that GE’s managers GE confessed to be a market timer: It’s a “strong seller’s market for financial assets,” it said.

GE confessed to be a market timer: It’s a “strong seller’s market for financial assets,” it said. GE confessed to be a market timer: It’s a “strong seller’s market for financial assets,” it said.

GE confessed to be a market timer: It’s a “strong seller’s market for financial assets,” it said.