China Matters

Over the past few days I have repeatedly heard the following statement:“China isn’t that important as it is only 7% of the U.S. economy.”While that may be a true statement in relation to the economy, it is a far different matter when it comes to the financial markets.

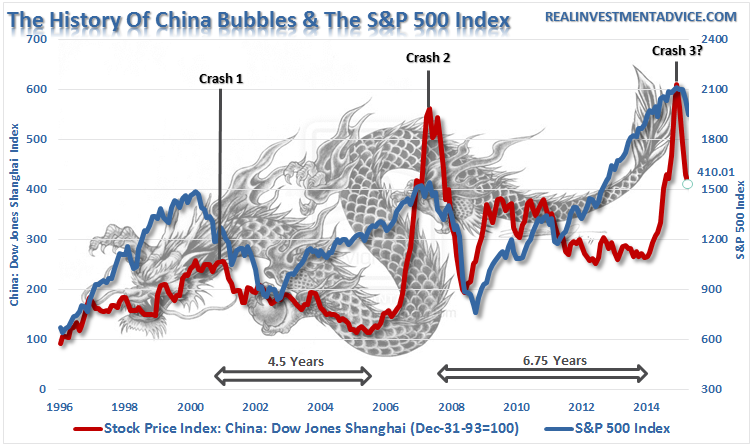

With financial markets so closely correlated, what happens in China has a direct and immediate impact on U.S. markets. Beginning in 2014, China financial markets went parabolic as investors levered up to speculate. This is not the first time this happened, and is a sharp reminder of why the perils of leverage should not be readily dismissed.

The problem is, as shown in the chart below, that what happens in China is not isolated just to China. As money flees those markets, it also rapidly exits the U.S. markets as fears of contagion spread.

While the Chinese government has injected liquidity, suspended trading in almost half of the listed equities and encouraged pension funds to buy securities, arrested short-sellers and “disappeared” corporate executives, these actions have done little to stem the decline as investors “panic sell” in a rush to safety.

That collapse, if history is any guide, is likely not done as yet which suggests that the financial rout in other markets are only just beginning.

Speaking Of Margin

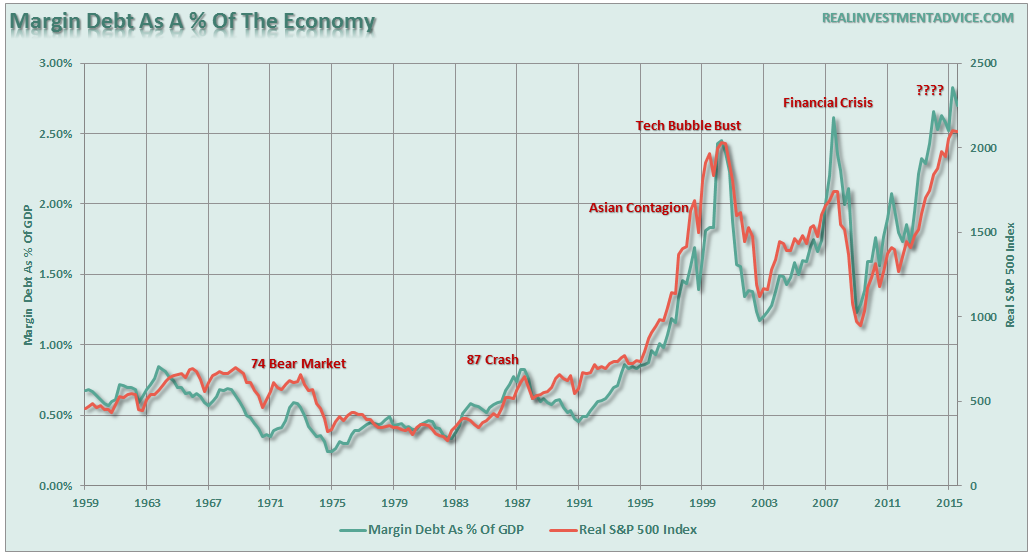

Last year, margin debt in China reached $264 Billion. After adjusting for the size of the two markets, is about double that of the roughly $500 billion in margin debt in the U.S.This difference in relative size was given as a prime example about how margin debt is not a problem for the U.S. This is incorrect, and just another example of the MSM’s willful blindness to the facts. The fact is that the relative size of margin debt in the past has not been a “safety net” that investors should rely on. As shown, the level of real (inflation-adjusted)margin debt as a percentage of real GDP has reached levels only witnessed at the peaks of the last two financial bubble peaks in the U.S.

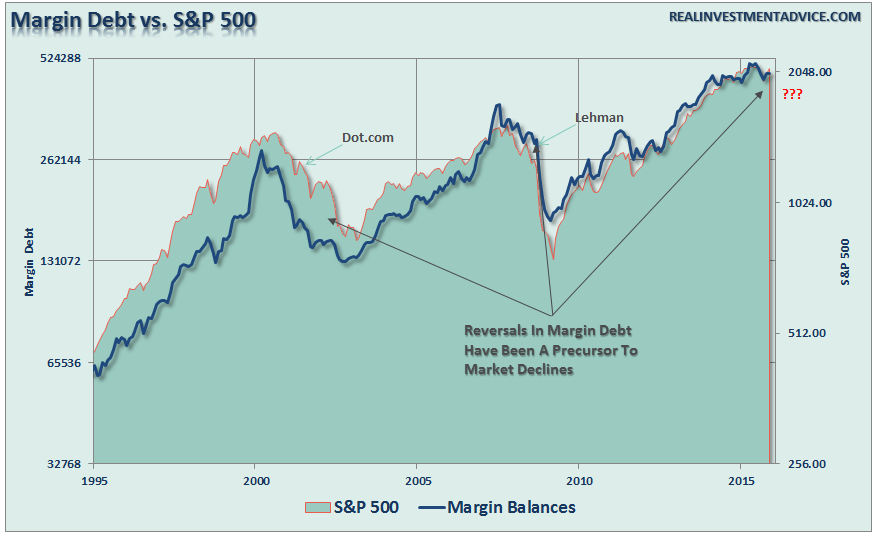

The same is seen in the raw levels of margin debt with respect to the financial markets.

While no single indicator should be relied upon as a measure to manage a portfolio, it should be well understood by now that leverage is a “double-edged sword.” While rising margin debt levels provide the additional liquidity to drive stock prices higher on the way up, it also cuts just as deeply when prices fall.

China is clearly showing the consequences of the unwinding of leverage. Despite government actions to stem the decline, investors are finding ways to extract their capital back out of the market in fears of a repeat of the 2008 crash. It is a lesson that should be studied and learned, again, by investors today.

Just as the Federal Reserve encouraged investors to jump into the financial markets by providing liquidity and suppressing interest rates, China also encouraged their population to do the same. Instead of taking actions to control the rise, they (both the U.S. and China) encouraged it. The problem is that when the “bubble” pops – it becomes uncontrollable.

As investors, it is our job to analyze the data and understand the inter-relationships between various data points and our portfolios. While margin debt is but only one “breadcrumb” on the trail, when combined with declining momentum, excessive deviations from long-term means, and weak economic growth, a larger picture of overall “risk” begins to emerge.

Does this mean that investors should “panic sell” immediately and run into the safety of cash? No. However, it does suggest that investors should be much more cautious about portfolio allocations and the degree of risk being undertaken as it relates to long-term investors objectives.

Technical Supports Under Attack

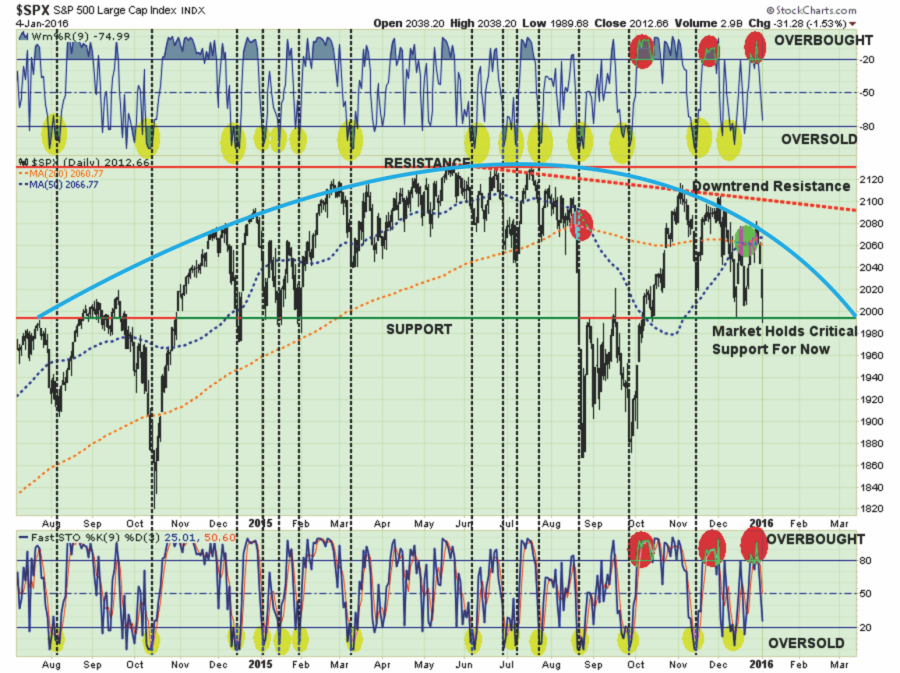

Earlier this week, I discussed the importance for the market to hold support at 1990 on the S&P 500. That level is under critical attack this morning as the market slides over concerns of China.“Importantly, the ongoing topping process continues in earnest. As shown in the two charts below, the current topping process is very akin to the processes witnessed at the previous two major market peaks in 2000 and 2007.

You can clearly see the topping process being made over the last 18 months in the market. Until, or unless, the market can break out of the current downward trend, the risk of lower asset prices remains elevated.”

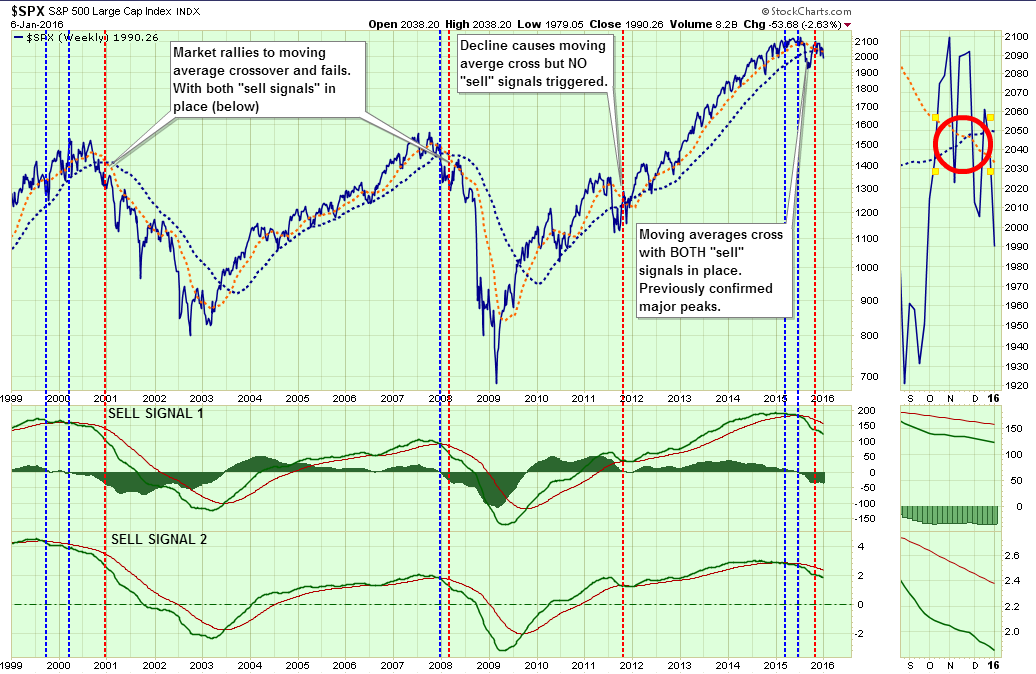

More importantly, if we step back to a “weekly” view of the markets we get a better picture of the level of deterioration currently in progress. As shown in the chart below, not only have both lower sell signals been triggered by deterioration in price momentum, the short and long-term moving averages have now crossed.

Since the turn of the century, the two primary moving averages have only crossed three other times – at the peak of the markets in 2001 and early 2008, and in 2011. The difference in 2011 is that while the sharp decline in the prices due to the debt ceiling debate caused the moving averages to cross, the two lower sell signals were not triggered. This kept portfolios allocated more towards equities at that time.

The current topping process, as discussed on Tuesday, is more akin to that seen in 2000 and early 2008. With primary moving averages now crossed, sell signals in place and markets trading below supports, rallies in equities should be used to rebalance portfolios and reduce risk.

While the markets are not “technically” in a “bear market” currently, it is important to remember that they weren’t in 2001 and early 2008 either.Waiting to make adjustments until after full recognition of the event doesn’t leave you many options.

Just some things to think about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In

No comments:

Post a Comment