Seller’s perception on loans

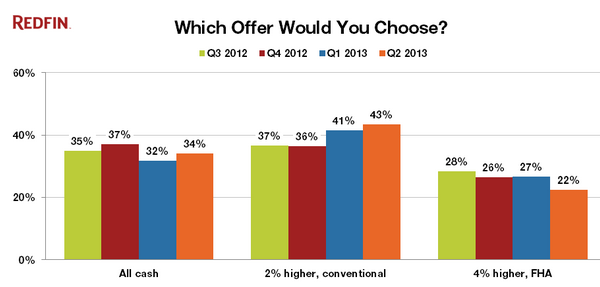

People are under the impression that sellers are somehow oblivious to the differing financing options out in the market. A recent Redfin survey asked potential home sellers what kind of financing option would they choose for their buyers?

Is it surprising that FHA is at the bottom of the list? And keep in mind this is for sellers in various regions. For prime locations, I assure you the figures are much more skewed. Why would anyone take an offer with such little skin in the game when you can simply go with an all-cash offer and know escrow will close without a problem? It really is a no brainer.

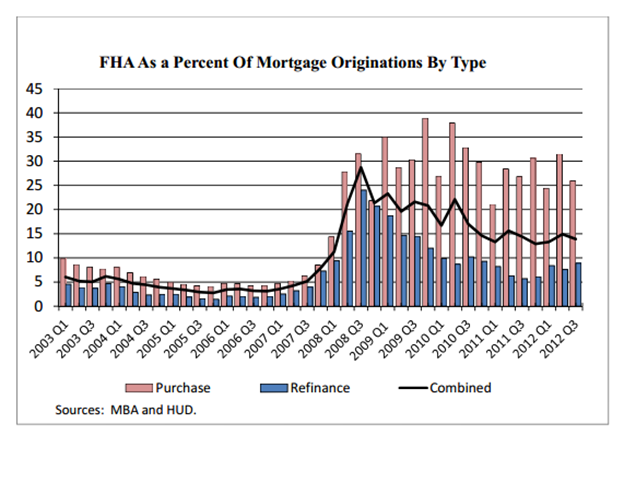

On the side of buyers, FHA insured loans have actually gotten much more expensive with mortgage insurance. It is crazy that FHA mortgage insurance premiums can add up to 1.55 percentage points to your overall effective FHA mortgage rate. That is very high in this rock bottom interest environment. Why is the rate so high? Because of legacy defaults but also the reality that you are giving people 30x leverage right off the bat.

FHA loan volume picked up right in line with the burst of the housing bubble:

Over $1.1 trillion in FHA insured loans are now outstanding. Keep in mind FHA insured loans were never intended to be a big part of the market. For many years they have consumed a large part of all mortgage originations. Even in Southern California FHA insured loans make up 22.9 percent of all purchases (another 34 percent came from all cash buyers).

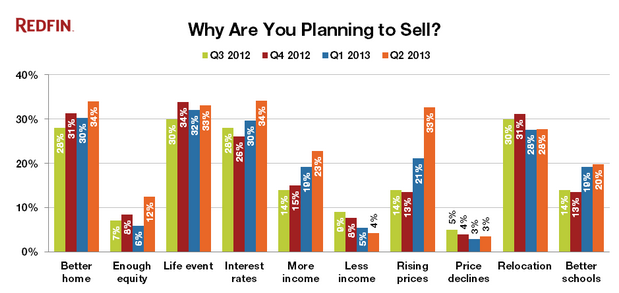

It is abundantly clear that the government and banks are all in on the housing market. We’ve recently talked about the reemergence of interest only mortgages. The market is now tilting to a full sense that home prices cannot and will not go down, regardless of underlying economic fundamentals. What is tenuous about this recovery is that it is being spurred on by massive monetary intervention that has never been witnessed in history. So those that claim they have a sense as to how this is all going to play out have a much better crystal ball. Yet one thing seems certain in the short-term and human nature and behavior is not going to evolve just because we had the worse financial crises since the Great Depression. Take a look at another piece of data from the Redfin survey:

Two big things jump out at me here. The first is that more people are planning to sell because home prices are going up. That makes sense. Yet adding more inventory is likely to help in keeping prices in place or lowering them depending on how much is put on the market. The next one is the “enough equity” section. Obviously perceptions are changing and many underwater homeowners are now reemerging from their negative equity positions.

In most of the country, owning a home makes a whole lot of sense today. Rock bottom interest rates and home prices that have adjusted from the peak make it a sensible move. In higher priced regions, the decision isn’t so clear cut. It is interesting that some think $200,000 is chump change when it comes to a down payment. Yet compounding $200,000 at 7 percent over 10 years will get you close to $400,000 during this time. Will a $600,000 home suddenly rise to $800,000 in this period if incomes are not going up? Right now homes are reaching max levels courtesy of all cash buying, hot foreign money flowing in, and people now leveraging up and entertaining interest only loans again. At least with the interest only loans of today, you need 20 percent down. FHA insured loans are not exactly the Ferrari option in the housing market.

No comments:

Post a Comment