Peak inequality

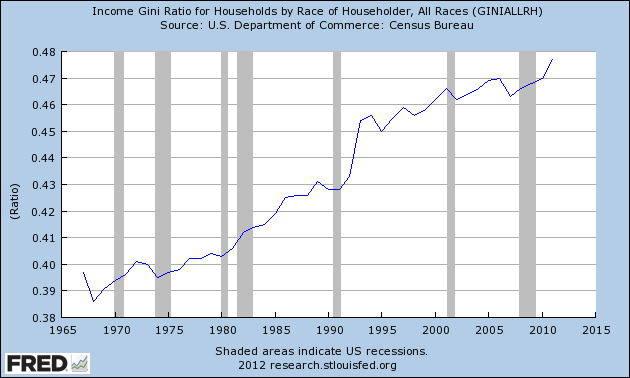

A measure of income inequality for a nation can be found via the Gini ratio. As you can see, income inequality is at a post World War II high:

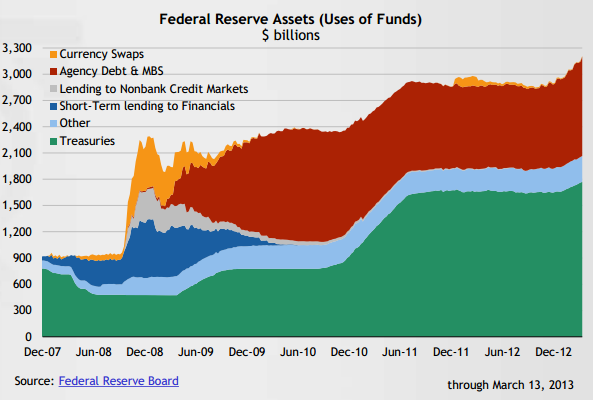

Most of the disparity started in the 1980s and hasn’t let up since. The Fed has also increased its balance sheet deep into uncharted territory. The current bailout dish of the day is QE3 with the Fed buying up mortgage backed securities. This has pushed the Fed balance sheet above $3.2 trillion:

Yet this has done very little to improve the economic landscape for average Americans. There is little hiding that inflation is hitting in very important areas including college tuition and healthcare. Even housing is getting expensive again but is hidden under the guise of low rates that mask the true underlying cost of a home. The Fed is betting that most Americans will ignore the sticker price and simply examine the monthly payment. The Fed is purchasing some $85 billion in MBS each month with no signs of stopping:

“(Bloomberg) Obviously, there has been improvement,” he said at a news conference in Washington today after the Fed decided to leave the pace of asset purchases unchanged at $85 billion a month. “One thing we would need is to make sure that this is not a temporary improvement.”Yet a growth strategy based on debt has not helped the vast majority of Americans:

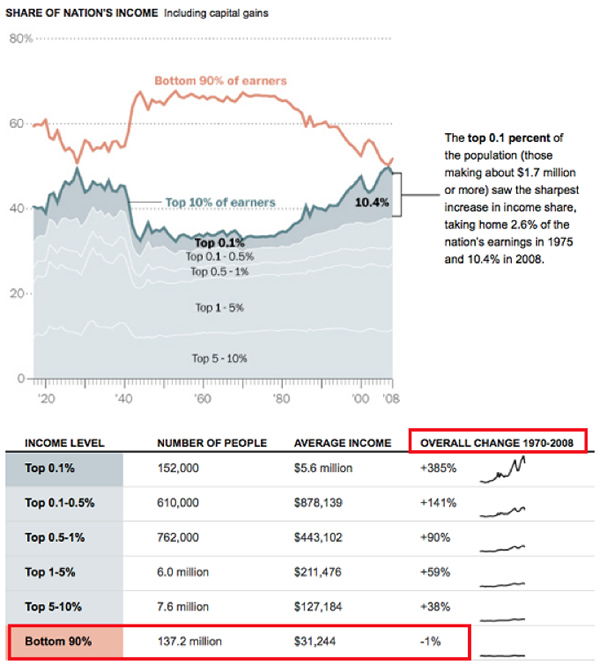

From 1970 to 2008 the bottom 90 percent of Americans have seen no real gain to their incomes. This may be surprising but also helps to explain why we have some 47+ million Americans receiving food stamps at a time when the stock market is reaching new highs.

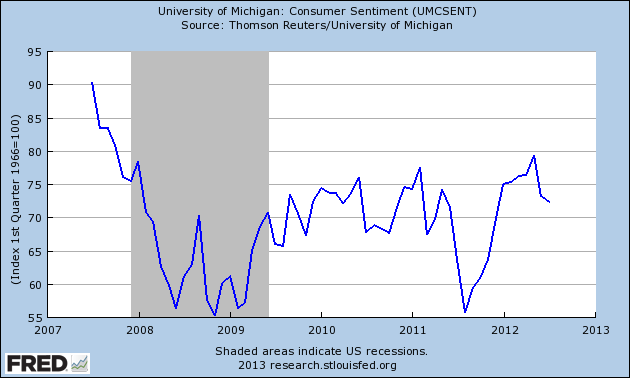

It also helps to explain why consumer sentiment is at levels that were last felt during the middle of the crisis in 2008:

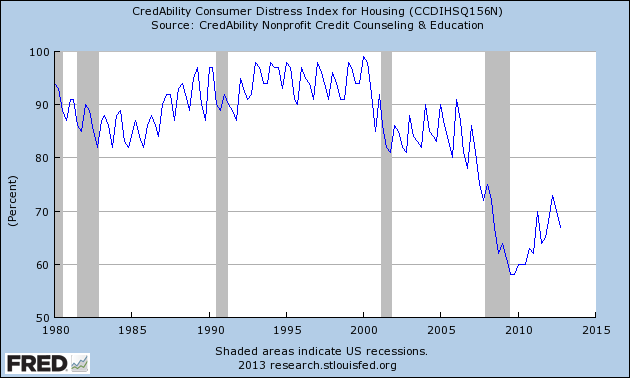

First, most Americans do not own any significant amount of stocks. Many organizations have boosted their profits by slashing wages and jobs. Good for stock prices but not good for workers. Also, many organizations now make a large amount of their profits abroad. And finally, many Americans derive the largest part of their net worth from housing. According to the CredAbility Distress Index things are still tough for many:

The Index score is tied to one of 5 general rating categories, which reflect the strength and stability of the consumer’s position.Low rates have not cured the 10 million homes that are still underwater. Prices might be rising in certain areas but this is a reflection of low rates courtesy of the Fed and this play might be played out. The Fed has pushed rates to negative territory. What is now happening is large investors are purchasing homes throughout the country for investments. Many looking to buy are finding very little inventory and are having to compete with large money investors. The Fed has made it easy for member banks to access easy money. Ironically access to credit for most Americans is still tough.

Less than 60 Emergency / Crisis

60 – 69 Distressed / Unstable

70 – 79 Weakening / At-Risk

80 – 89 Good / Stable

90 and Above Excellent / Secure

Wealthier Americans derive their wealth from stocks. So this resurgence in stocks is definitely increasing their bottom line but one out of three Americans has no savings and half are one paycheck away from being on the streets. The bailouts started occurring nearly five years ago so we can now look at the track record of what has occurred. What has happened is that for most Americans, a low wage system has been pushed into their lifestyle. No method of privatizing gains and socializing losses. Yet this is the current system that still reigns for a few. A peak for the Dow and speculation in real estate coming again thanks to low rates from the Fed. Are we to expect that this time around things are going to get better for the middle class?

No comments:

Post a Comment